Encompass Health Porter's Five Forces Analysis

From Overview to Strategy Blueprint

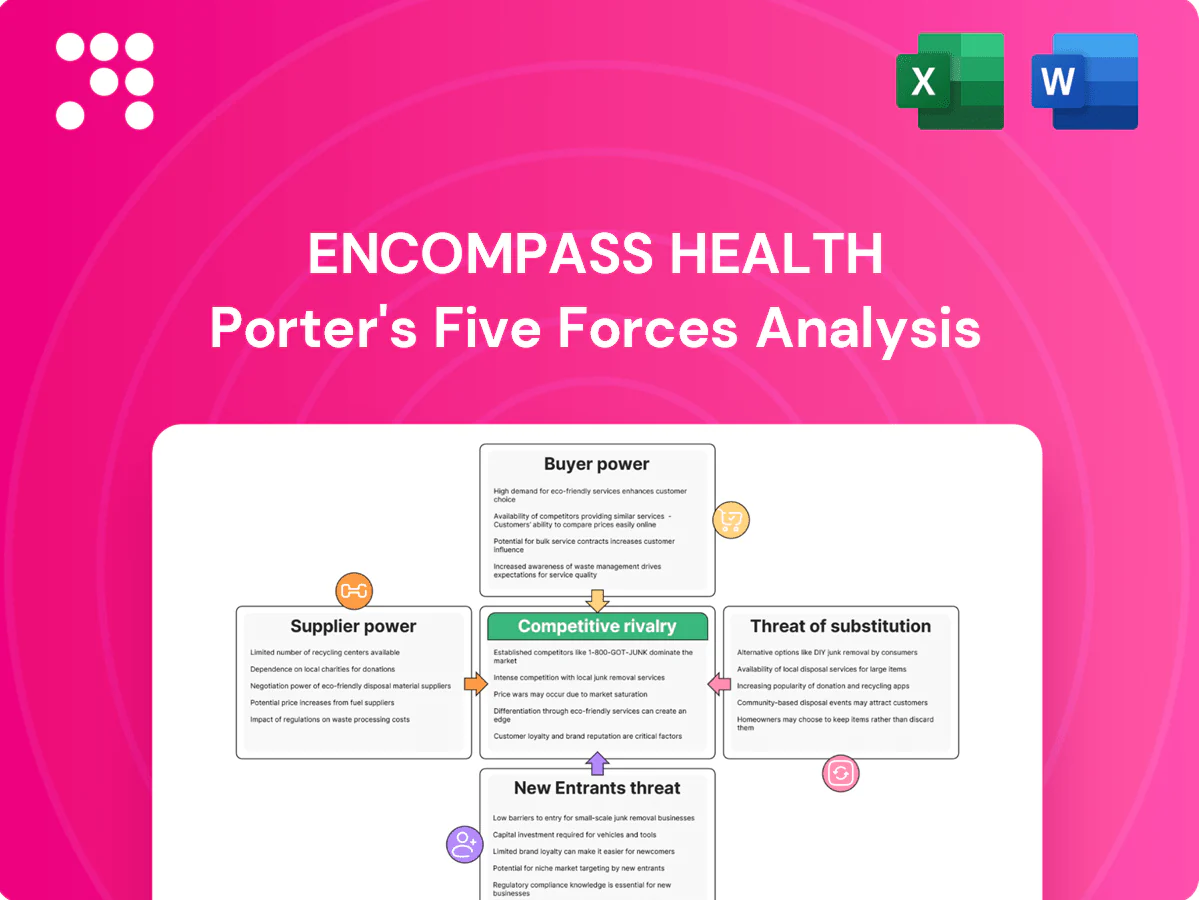

Encompass Health operates in a competitive post-acute care market where buyer bargaining, reimbursement pressures, and consolidation shape margins, while regulatory hurdles and substitute care models pose notable threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Encompass Health’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Clinical labor scarcity

Specialized therapists, nurses, and rehab physicians are core inputs and remain in short supply, elevating wage pressure and turnover risk. Reliance on travel staff and premium pay to fill gaps compresses margins and raises operating volatility. Strong employer brand and residency affiliations reduce supplier leverage by improving recruitment. Automation and scheduling efficiency help, but cannot fully offset scarcity given projected 18% demand growth for physical therapists (BLS 2022–32).

Therapy equipment and devices

Therapy equipment and devices for Encompass Health—notably rehab robotics, mobility aids and specialty devices—are sourced from a concentrated vendor base, with the global rehab robotics market estimated at about $1.2 billion in 2023. Switching costs are moderate due to staff training, protocol changes and clinical-pathway integration. Volume purchasing and device standardization can reduce supplier leverage. Supply-chain disruptions (semiconductor and component shortages) can tighten availability and raise prices.

Drugs and medical supplies

While many hospital supplies are commoditized, injectables and specialty medicines retain pricing power, with specialty drugs accounting for roughly half of US drug spending in 2023. Group purchasing organizations, which serve about 90% of US hospitals, improve pricing but cannot remove inflation or supply shocks. Formularies and clinical protocols help rationalize use and curb cost growth. Reliable logistics remain critical to avoid care disruptions.

IT/EMR and interoperability

EMR, analytics, and interoperability vendors create strong lock-in through proprietary data models, workflows, and regulatory compliance requirements; Epic and Oracle Cerner held roughly 60% of US hospital EMR market in 2024. Integration with referring hospitals raises switching friction, while multi-year (commonly 5–7 year) contracts and multi-million-dollar implementations amplify vendor leverage; strict cybersecurity and uptime SLAs further constrain alternatives.

- Vendor concentration: Epic/Oracle Cerner ~60% (2024)

- Contract length: 5–7 years

- Implementation: multi-million-dollar

- Drive factors: data/workflow lock-in, hospital integration, cyber/uptime SLAs

Facility development and services

- Contractor concentration: higher bargaining power

- Capex scale: 137 hospitals (2024) increases supplier leverage

- Regional tightness: bids up ~10–15%

- Long-term contracts: cost stability vs reduced flexibility

Clinician shortages and device concentration tighten supplier power, raising wage and supply risk

Supplier power is moderate-high: clinician scarcity (PT demand +18% 2022–32) and travel-staff reliance raise wage pressure and margin volatility. Device/vendor concentration (rehab robotics ~$1.2B 2023) and EMR lock-in (Epic/Oracle Cerner ~60% 2024) increase switching costs. GPOs (~90% hospitals) and long-term contracts mitigate but cannot remove pricing or supply shocks.

| Metric | Value |

|---|---|

| PT demand growth | +18% (BLS 2022–32) |

| Rehab robotics market | $1.2B (2023) |

| EMR share | Epic/Cerner ~60% (2024) |

| Hospitals | 137 (Encompass 2024) |

| GPO coverage | ~90% US hospitals |

| Contractor bids | +10–15% regional |

What is included in the product

Tailored exclusively for Encompass Health, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence, substitution threats, and entry barriers, highlighting disruptive trends and strategic levers that impact pricing, profitability, and market positioning.

A concise, one-sheet Porter's Five Forces for Encompass Health that pinpoints competitive intensity, payer/reimbursement and regulatory risks, and supplier/entry threats—customizable for scenario analysis and slide-ready to eliminate research and presentation bottlenecks.

Customers Bargaining Power

Medicare and Medicaid rate setting

Medicare FFS sets the IRF base rate through the IRF PPS, effectively capping prices and limiting Encompass Health’s negotiation; CMS’s FY2024 IRF PPS update (net ~3.1% increase) and case-mix adjustments directly shift revenue. Medicaid reimbursement varies by state and is often below cost, pressuring margins. Regulatory visibility is moderate, but periodic CMS resets can produce material payment swings.

Medicare Advantage concentration

Medicare Advantage enrollment topped 30 million in 2024, with top insurers capturing roughly 55–60% of enrollment in many markets, boosting plan negotiating leverage. Plans steer volume via narrow networks and prior authorization, shifting admissions and case mix. Aggressive discounts and utilization controls compress rates and length-of-stay, pressuring margins. Proven functional and readmission outcomes can earn preferred status and higher referral share.

Commercial payers and ACOs

Commercial insurers and ACOs increasingly push site-of-care shifts to lower-cost alternatives and use bundled payments and value-based contracts to scrutinize post-acute spend. Contract renewals hinge on outcomes, readmissions and cost per episode, with CMS readmission penalties up to 3% reinforcing this pressure. Larger integrated systems consistently extract better commercial terms than fragmented providers.

Hospital discharge planners

Hospital discharge planners act as gatekeepers for Encompass Health referrals, with acute-care placement decisions heavily swaying volumes; Encompass, the largest US post-acute provider, operated over 140 inpatient rehab hospitals in 2024, and co-located JVs demonstrably ease transfers and boost referral flow. Performance on throughput and care coordination directly changes discharge choices, so relationship management materially affects share.

- Gatekeeping: acute hospitals control referrals

- Co-located JVs: lower friction, higher flow

- Throughput/care coordination: impacts placement

- Relationship management: drives volume

Patients and caregivers

Individual patients have limited pricing power for Encompass Health because payers and clinical protocols determine coverage; in 2024 Encompass operated 137 inpatient rehab hospitals and ~257 home health/hospice sites, keeping consumer choice bounded by location and network. Patient satisfaction and functional outcomes strongly influence referrals and reputation, while price transparency tools are growing but remain secondary to payer networks.

- Low direct pricing power

- Networks/location limit choice

- Outcomes drive referrals

- Transparency rising but less decisive

Payers hold leverage; MA >30M, top plans ~55–60%; Medicare IRF PPS +3.1% risked

Payers (Medicare FFS/MA, Medicaid, commercial) hold strong bargaining power via rate-setting, prior auth and network steering; Medicare FY2024 IRF PPS net +3.1% but CMS resets can swing revenue. MA enrollment >30M (2024) with top plans at ~55–60% market share, pressuring rates and LOS. Hospitals gatekeep referrals; Encompass ran 137 IRFs and ~257 home health/hospice sites in 2024, limiting patient choice.

| Metric | 2024 Value |

|---|---|

| MA enrollment | 30+ million |

| Top plan share | ~55–60% |

| Encompass IRFs | 137 |

| Home health/hospice sites | ~257 |

| CMS FY2024 IRF PPS | net +3.1% |

| CMS readmission penalty | up to 3% |

What You See Is What You Get

Encompass Health Porter's Five Forces Analysis

This preview shows the exact Encompass Health Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable and will get instant access to this identical file upon payment.

From Overview to Strategy Blueprint

Encompass Health operates in a competitive post-acute care market where buyer bargaining, reimbursement pressures, and consolidation shape margins, while regulatory hurdles and substitute care models pose notable threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Encompass Health’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Clinical labor scarcity

Specialized therapists, nurses, and rehab physicians are core inputs and remain in short supply, elevating wage pressure and turnover risk. Reliance on travel staff and premium pay to fill gaps compresses margins and raises operating volatility. Strong employer brand and residency affiliations reduce supplier leverage by improving recruitment. Automation and scheduling efficiency help, but cannot fully offset scarcity given projected 18% demand growth for physical therapists (BLS 2022–32).

Therapy equipment and devices

Therapy equipment and devices for Encompass Health—notably rehab robotics, mobility aids and specialty devices—are sourced from a concentrated vendor base, with the global rehab robotics market estimated at about $1.2 billion in 2023. Switching costs are moderate due to staff training, protocol changes and clinical-pathway integration. Volume purchasing and device standardization can reduce supplier leverage. Supply-chain disruptions (semiconductor and component shortages) can tighten availability and raise prices.

Drugs and medical supplies

While many hospital supplies are commoditized, injectables and specialty medicines retain pricing power, with specialty drugs accounting for roughly half of US drug spending in 2023. Group purchasing organizations, which serve about 90% of US hospitals, improve pricing but cannot remove inflation or supply shocks. Formularies and clinical protocols help rationalize use and curb cost growth. Reliable logistics remain critical to avoid care disruptions.

IT/EMR and interoperability

EMR, analytics, and interoperability vendors create strong lock-in through proprietary data models, workflows, and regulatory compliance requirements; Epic and Oracle Cerner held roughly 60% of US hospital EMR market in 2024. Integration with referring hospitals raises switching friction, while multi-year (commonly 5–7 year) contracts and multi-million-dollar implementations amplify vendor leverage; strict cybersecurity and uptime SLAs further constrain alternatives.

- Vendor concentration: Epic/Oracle Cerner ~60% (2024)

- Contract length: 5–7 years

- Implementation: multi-million-dollar

- Drive factors: data/workflow lock-in, hospital integration, cyber/uptime SLAs

Facility development and services

- Contractor concentration: higher bargaining power

- Capex scale: 137 hospitals (2024) increases supplier leverage

- Regional tightness: bids up ~10–15%

- Long-term contracts: cost stability vs reduced flexibility

Clinician shortages and device concentration tighten supplier power, raising wage and supply risk

Supplier power is moderate-high: clinician scarcity (PT demand +18% 2022–32) and travel-staff reliance raise wage pressure and margin volatility. Device/vendor concentration (rehab robotics ~$1.2B 2023) and EMR lock-in (Epic/Oracle Cerner ~60% 2024) increase switching costs. GPOs (~90% hospitals) and long-term contracts mitigate but cannot remove pricing or supply shocks.

| Metric | Value |

|---|---|

| PT demand growth | +18% (BLS 2022–32) |

| Rehab robotics market | $1.2B (2023) |

| EMR share | Epic/Cerner ~60% (2024) |

| Hospitals | 137 (Encompass 2024) |

| GPO coverage | ~90% US hospitals |

| Contractor bids | +10–15% regional |

What is included in the product

Tailored exclusively for Encompass Health, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence, substitution threats, and entry barriers, highlighting disruptive trends and strategic levers that impact pricing, profitability, and market positioning.

A concise, one-sheet Porter's Five Forces for Encompass Health that pinpoints competitive intensity, payer/reimbursement and regulatory risks, and supplier/entry threats—customizable for scenario analysis and slide-ready to eliminate research and presentation bottlenecks.

Customers Bargaining Power

Medicare and Medicaid rate setting

Medicare FFS sets the IRF base rate through the IRF PPS, effectively capping prices and limiting Encompass Health’s negotiation; CMS’s FY2024 IRF PPS update (net ~3.1% increase) and case-mix adjustments directly shift revenue. Medicaid reimbursement varies by state and is often below cost, pressuring margins. Regulatory visibility is moderate, but periodic CMS resets can produce material payment swings.

Medicare Advantage concentration

Medicare Advantage enrollment topped 30 million in 2024, with top insurers capturing roughly 55–60% of enrollment in many markets, boosting plan negotiating leverage. Plans steer volume via narrow networks and prior authorization, shifting admissions and case mix. Aggressive discounts and utilization controls compress rates and length-of-stay, pressuring margins. Proven functional and readmission outcomes can earn preferred status and higher referral share.

Commercial payers and ACOs

Commercial insurers and ACOs increasingly push site-of-care shifts to lower-cost alternatives and use bundled payments and value-based contracts to scrutinize post-acute spend. Contract renewals hinge on outcomes, readmissions and cost per episode, with CMS readmission penalties up to 3% reinforcing this pressure. Larger integrated systems consistently extract better commercial terms than fragmented providers.

Hospital discharge planners

Hospital discharge planners act as gatekeepers for Encompass Health referrals, with acute-care placement decisions heavily swaying volumes; Encompass, the largest US post-acute provider, operated over 140 inpatient rehab hospitals in 2024, and co-located JVs demonstrably ease transfers and boost referral flow. Performance on throughput and care coordination directly changes discharge choices, so relationship management materially affects share.

- Gatekeeping: acute hospitals control referrals

- Co-located JVs: lower friction, higher flow

- Throughput/care coordination: impacts placement

- Relationship management: drives volume

Patients and caregivers

Individual patients have limited pricing power for Encompass Health because payers and clinical protocols determine coverage; in 2024 Encompass operated 137 inpatient rehab hospitals and ~257 home health/hospice sites, keeping consumer choice bounded by location and network. Patient satisfaction and functional outcomes strongly influence referrals and reputation, while price transparency tools are growing but remain secondary to payer networks.

- Low direct pricing power

- Networks/location limit choice

- Outcomes drive referrals

- Transparency rising but less decisive

Payers hold leverage; MA >30M, top plans ~55–60%; Medicare IRF PPS +3.1% risked

Payers (Medicare FFS/MA, Medicaid, commercial) hold strong bargaining power via rate-setting, prior auth and network steering; Medicare FY2024 IRF PPS net +3.1% but CMS resets can swing revenue. MA enrollment >30M (2024) with top plans at ~55–60% market share, pressuring rates and LOS. Hospitals gatekeep referrals; Encompass ran 137 IRFs and ~257 home health/hospice sites in 2024, limiting patient choice.

| Metric | 2024 Value |

|---|---|

| MA enrollment | 30+ million |

| Top plan share | ~55–60% |

| Encompass IRFs | 137 |

| Home health/hospice sites | ~257 |

| CMS FY2024 IRF PPS | net +3.1% |

| CMS readmission penalty | up to 3% |

What You See Is What You Get

Encompass Health Porter's Five Forces Analysis

This preview shows the exact Encompass Health Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable and will get instant access to this identical file upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Encompass Health operates in a competitive post-acute care market where buyer bargaining, reimbursement pressures, and consolidation shape margins, while regulatory hurdles and substitute care models pose notable threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Encompass Health’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Clinical labor scarcity

Specialized therapists, nurses, and rehab physicians are core inputs and remain in short supply, elevating wage pressure and turnover risk. Reliance on travel staff and premium pay to fill gaps compresses margins and raises operating volatility. Strong employer brand and residency affiliations reduce supplier leverage by improving recruitment. Automation and scheduling efficiency help, but cannot fully offset scarcity given projected 18% demand growth for physical therapists (BLS 2022–32).

Therapy equipment and devices

Therapy equipment and devices for Encompass Health—notably rehab robotics, mobility aids and specialty devices—are sourced from a concentrated vendor base, with the global rehab robotics market estimated at about $1.2 billion in 2023. Switching costs are moderate due to staff training, protocol changes and clinical-pathway integration. Volume purchasing and device standardization can reduce supplier leverage. Supply-chain disruptions (semiconductor and component shortages) can tighten availability and raise prices.

Drugs and medical supplies

While many hospital supplies are commoditized, injectables and specialty medicines retain pricing power, with specialty drugs accounting for roughly half of US drug spending in 2023. Group purchasing organizations, which serve about 90% of US hospitals, improve pricing but cannot remove inflation or supply shocks. Formularies and clinical protocols help rationalize use and curb cost growth. Reliable logistics remain critical to avoid care disruptions.

IT/EMR and interoperability

EMR, analytics, and interoperability vendors create strong lock-in through proprietary data models, workflows, and regulatory compliance requirements; Epic and Oracle Cerner held roughly 60% of US hospital EMR market in 2024. Integration with referring hospitals raises switching friction, while multi-year (commonly 5–7 year) contracts and multi-million-dollar implementations amplify vendor leverage; strict cybersecurity and uptime SLAs further constrain alternatives.

- Vendor concentration: Epic/Oracle Cerner ~60% (2024)

- Contract length: 5–7 years

- Implementation: multi-million-dollar

- Drive factors: data/workflow lock-in, hospital integration, cyber/uptime SLAs

Facility development and services

- Contractor concentration: higher bargaining power

- Capex scale: 137 hospitals (2024) increases supplier leverage

- Regional tightness: bids up ~10–15%

- Long-term contracts: cost stability vs reduced flexibility

Clinician shortages and device concentration tighten supplier power, raising wage and supply risk

Supplier power is moderate-high: clinician scarcity (PT demand +18% 2022–32) and travel-staff reliance raise wage pressure and margin volatility. Device/vendor concentration (rehab robotics ~$1.2B 2023) and EMR lock-in (Epic/Oracle Cerner ~60% 2024) increase switching costs. GPOs (~90% hospitals) and long-term contracts mitigate but cannot remove pricing or supply shocks.

| Metric | Value |

|---|---|

| PT demand growth | +18% (BLS 2022–32) |

| Rehab robotics market | $1.2B (2023) |

| EMR share | Epic/Cerner ~60% (2024) |

| Hospitals | 137 (Encompass 2024) |

| GPO coverage | ~90% US hospitals |

| Contractor bids | +10–15% regional |

What is included in the product

Tailored exclusively for Encompass Health, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence, substitution threats, and entry barriers, highlighting disruptive trends and strategic levers that impact pricing, profitability, and market positioning.

A concise, one-sheet Porter's Five Forces for Encompass Health that pinpoints competitive intensity, payer/reimbursement and regulatory risks, and supplier/entry threats—customizable for scenario analysis and slide-ready to eliminate research and presentation bottlenecks.

Customers Bargaining Power

Medicare and Medicaid rate setting

Medicare FFS sets the IRF base rate through the IRF PPS, effectively capping prices and limiting Encompass Health’s negotiation; CMS’s FY2024 IRF PPS update (net ~3.1% increase) and case-mix adjustments directly shift revenue. Medicaid reimbursement varies by state and is often below cost, pressuring margins. Regulatory visibility is moderate, but periodic CMS resets can produce material payment swings.

Medicare Advantage concentration

Medicare Advantage enrollment topped 30 million in 2024, with top insurers capturing roughly 55–60% of enrollment in many markets, boosting plan negotiating leverage. Plans steer volume via narrow networks and prior authorization, shifting admissions and case mix. Aggressive discounts and utilization controls compress rates and length-of-stay, pressuring margins. Proven functional and readmission outcomes can earn preferred status and higher referral share.

Commercial payers and ACOs

Commercial insurers and ACOs increasingly push site-of-care shifts to lower-cost alternatives and use bundled payments and value-based contracts to scrutinize post-acute spend. Contract renewals hinge on outcomes, readmissions and cost per episode, with CMS readmission penalties up to 3% reinforcing this pressure. Larger integrated systems consistently extract better commercial terms than fragmented providers.

Hospital discharge planners

Hospital discharge planners act as gatekeepers for Encompass Health referrals, with acute-care placement decisions heavily swaying volumes; Encompass, the largest US post-acute provider, operated over 140 inpatient rehab hospitals in 2024, and co-located JVs demonstrably ease transfers and boost referral flow. Performance on throughput and care coordination directly changes discharge choices, so relationship management materially affects share.

- Gatekeeping: acute hospitals control referrals

- Co-located JVs: lower friction, higher flow

- Throughput/care coordination: impacts placement

- Relationship management: drives volume

Patients and caregivers

Individual patients have limited pricing power for Encompass Health because payers and clinical protocols determine coverage; in 2024 Encompass operated 137 inpatient rehab hospitals and ~257 home health/hospice sites, keeping consumer choice bounded by location and network. Patient satisfaction and functional outcomes strongly influence referrals and reputation, while price transparency tools are growing but remain secondary to payer networks.

- Low direct pricing power

- Networks/location limit choice

- Outcomes drive referrals

- Transparency rising but less decisive

Payers hold leverage; MA >30M, top plans ~55–60%; Medicare IRF PPS +3.1% risked

Payers (Medicare FFS/MA, Medicaid, commercial) hold strong bargaining power via rate-setting, prior auth and network steering; Medicare FY2024 IRF PPS net +3.1% but CMS resets can swing revenue. MA enrollment >30M (2024) with top plans at ~55–60% market share, pressuring rates and LOS. Hospitals gatekeep referrals; Encompass ran 137 IRFs and ~257 home health/hospice sites in 2024, limiting patient choice.

| Metric | 2024 Value |

|---|---|

| MA enrollment | 30+ million |

| Top plan share | ~55–60% |

| Encompass IRFs | 137 |

| Home health/hospice sites | ~257 |

| CMS FY2024 IRF PPS | net +3.1% |

| CMS readmission penalty | up to 3% |

What You See Is What You Get

Encompass Health Porter's Five Forces Analysis

This preview shows the exact Encompass Health Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable and will get instant access to this identical file upon payment.