Endonovo Therapeutics Porter's Five Forces Analysis

From Overview to Strategy Blueprint

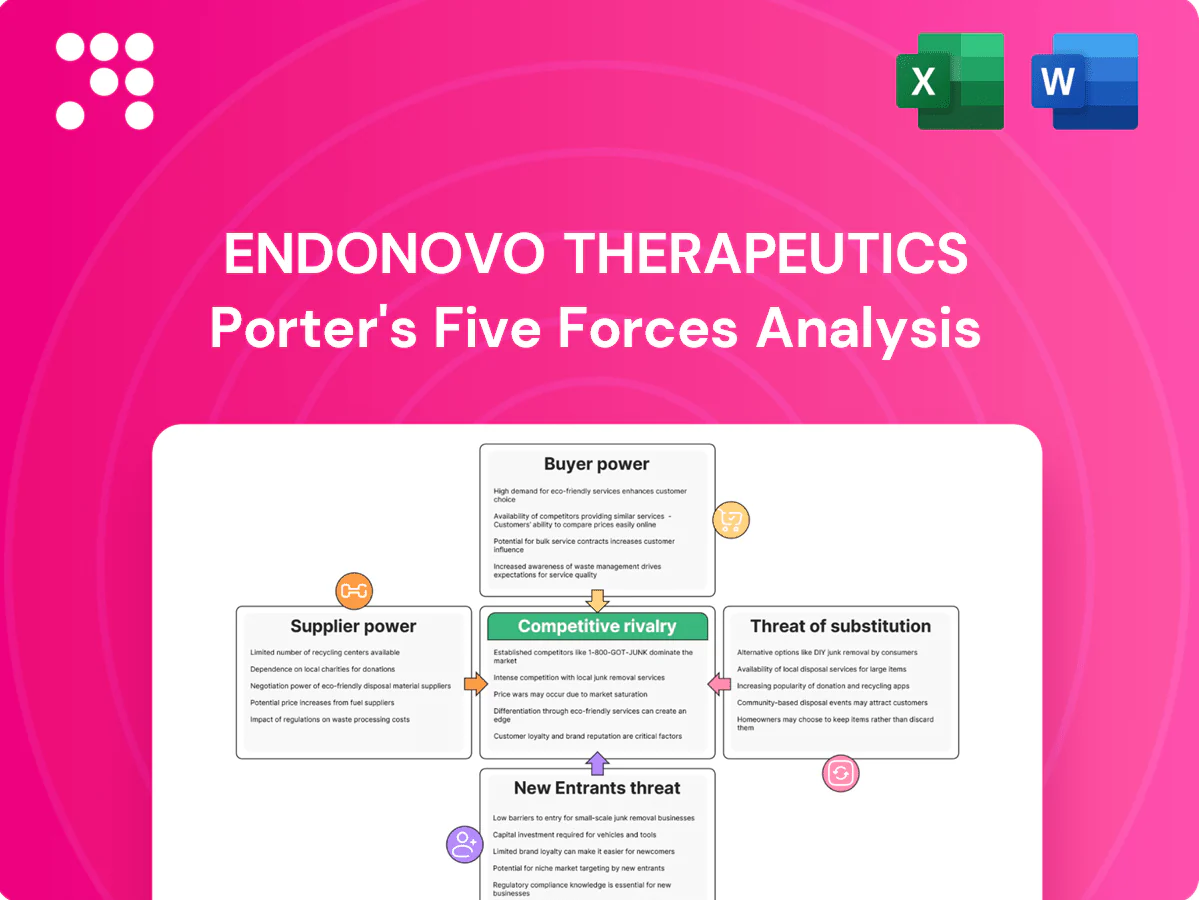

Endonovo Therapeutics faces moderate supplier and buyer power, high innovation-driven rivalry, and notable substitute and regulatory pressures shaping its market position. This snapshot highlights strategic risks and opportunity areas. The full Porter's Five Forces Analysis unpacks each force with force-by-force ratings. Unlock the complete report for actionable insights and visuals.

Suppliers Bargaining Power

Specialized EMF components

Endonovo depends on niche coils, drivers and shielding with few qualified vendors, creating supplier concentration that raises switching costs and lead-time risk (typical lead times 12–20 weeks for custom medical-grade parts). Suppliers can exert price pressure, with custom medical-grade premiums often 20–40% above commodity rates. Dual-sourcing and design-for-substitution reduce vendor leverage and procurement risk.

Medical-grade manufacturing

As of 2024, ISO 13485-certified contract manufacturers with specific EMF/medical-device experience are limited, concentrating supplier bargaining power for Endonovo Therapeutics.

Stringent compliance, validation, and documentation requirements create high onboarding hurdles and allow CMOs to impose stronger commercial terms and MOQs.

Negotiating multi-year agreements and volume commitments is the primary lever to secure lower unit costs and mitigate supplier pricing pressure.

Regulatory-approved inputs

Regulatory-approved inputs for Endonovo must meet ISO 10993 biocompatibility and applicable FDA device requirements, narrowing supplier choices. Any component change in 2024 can trigger revalidation and potential 510(k) or PMA filings, creating time and cost barriers that strengthen incumbent suppliers’ bargaining power. Early component standardization preserves procurement flexibility and reduces regulatory friction.

Supply chain resilience

Electronics cycles and geopolitical shocks can push semiconductors and passives into shortage, with lead times spiking to 20+ weeks during major disruptions, elongating deliveries and stressing cash flow; suppliers often prioritize larger OEMs (top ~20%) in allocation, increasing supplier bargaining power over small medtech firms like Endonovo. Inventory buffers and supplier scorecards are used to hedge these risks.

- Lead times: 20+ weeks in shocks

- Supplier priority: top ~20% customers

- Impact: delayed deliveries → cash flow strain

- Mitigation: inventory buffers, supplier scorecards

IP and proprietary designs

When custom assemblies embed supplier know-how dependency rises, limiting Endonovo Therapeutics exit options; tooling ownership and data rights are decisive. Suppliers can capture value via NRE fees and licensing—median med-tech NRE ~$250,000 in 2024, tooling $100k–$500k, royalties typically 3–6%. Contract terms must secure design control and transfer rights to preserve capture of downstream value.

- Dependency: embedded know-how increases switching costs

- NRE/tooling: median NRE ~$250,000; tooling $100k–$500k (2024)

- Licensing: typical royalties 3–6%

- Contracts: require design control, data access, transfer rights

Concentrated ISO-certified suppliers, long lead times and high NRE raise switching barriers

Endonovo faces high supplier bargaining power from concentrated, ISO 13485-certified vendors, long lead times (12–20 wks typical; 20+ wks in shocks) and regulatory revalidation costs that raise switching barriers. Custom NRE/tooling and embedded know-how (median NRE ~$250k; tooling $100k–$500k; royalties 3–6% in 2024) further lock suppliers in. Multi-year contracts, dual-sourcing and standardization reduce risk.

| Metric | Value (2024) |

|---|---|

| Typical lead time | 12–20 weeks |

| Shock lead time | 20+ weeks |

| Median NRE | $250,000 |

| Tooling | $100k–$500k |

| Royalties | 3–6% |

| ISO 13485 CMOs | Limited / concentrated |

What is included in the product

Tailored Porter's Five Forces analysis for Endonovo Therapeutics uncovering key drivers of competition, customer influence, supplier power, and market entry risks. Identifies disruptive substitutes, regulatory threats, and barriers that shape pricing, profitability, and strategic positioning.

Concise Porter's Five Forces view of Endonovo Therapeutics—pinpoints competitive pressures, regulatory and reimbursement risks, supplier/buyer leverage and substitute threats to simplify strategic prioritization and relieve analysis pain points.

Customers Bargaining Power

Hospitals and IDNs

Hospitals and IDNs exert high bargaining power, demanding robust clinical evidence and value-based pricing; by 2024 the top 100 health systems controlled roughly 60% of U.S. hospital beds, concentrating purchasing leverage. They run pilots, negotiate discounts or risk-sharing agreements and use formularies and capital committees to slow adoption cycles. Successful entry depends on clinical champions to drive procurement and pilot scale-up.

Ambulatory and post-acute

ASCs, wound clinics and home health prioritize throughput and cost per episode, making them highly price-sensitive yet quick to adopt technologies that demonstrably improve outcomes and reduce episode costs.

Leasing or per-use models lower capital barriers and accelerate uptake in these settings; retention depends on clear ROI, clinician education and seamless workflow integration to sustain recurring use.

Payers and reimbursement

Coverage policies and coding set effective demand and price ceilings, especially as US health spending reached about $4.5 trillion in 2023; limited or variable reimbursement gives payers leverage to push prices down. Demonstrable reductions in opioid use, length of stay and readmissions in peer studies materially strengthen hospital negotiating position, so robust health economic studies and cost-effectiveness models are pivotal.

Clinician gatekeepers

Surgeons, wound-care specialists and intensivists act as clinician gatekeepers, directly shaping Endonovo device utilization; a 2024 survey of 412 clinicians reported 61% skepticism toward novel EMF therapies, slowing uptake. Robust peer-reviewed trials and KOL endorsements materially reduce perceived risk and accelerate purchasing decisions. Practical training and intuitive device design improve compliance and adoption rates.

- Clinician influence: surgeons/intensivists drive hospital adoption

- Barrier: 61% clinician skepticism (2024 survey)

- Mitigator: peer-reviewed RCTs and KOL support

- Enabler: hands-on training + ease-of-use

Switching and alternatives

Buyers compare SofPulse against drugs, cold therapy, TENS and other PEMF devices, keeping price and clinical outcomes central; switching costs are moderate, driven mainly by staff training and protocol integration. Bundled hardware-plus-service offers and SLAs can lock accounts, while outcomes-based contracts shift risk to the vendor and weaken buyer leverage.

- Comparators: drugs, cold therapy, TENS, PEMF

- Switching costs: moderate — training and protocols

- Retention tools: bundles and SLAs

- Leverage reduced by outcomes-based contracts

Buyers control ~60% of beds; payers cap pricing in $4.5T market — 61% clinician skepticism

Buyers (hospitals/IDNs, ASCs, clinics) hold high leverage—top 100 U.S. health systems controlled ~60% of hospital beds (2024) and push for value-based pricing. Payers/coding limit ceilings amid $4.5T US health spend (2023); 61% clinician skepticism (2024) raises adoption barriers. Moderate switching costs; outcomes-based contracts and leasing mitigate buyer power.

| Metric | Value |

|---|---|

| Top-100 bed share (2024) | ~60% |

| US health spend (2023) | $4.5T |

| Clinician skepticism (2024) | 61% |

Same Document Delivered

Endonovo Therapeutics Porter's Five Forces Analysis

This Porter's Five Forces analysis for Endonovo Therapeutics evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to clarify strategic risks and opportunities. It highlights biotech-specific dynamics like IP strength and regulatory pressure. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.

From Overview to Strategy Blueprint

Endonovo Therapeutics faces moderate supplier and buyer power, high innovation-driven rivalry, and notable substitute and regulatory pressures shaping its market position. This snapshot highlights strategic risks and opportunity areas. The full Porter's Five Forces Analysis unpacks each force with force-by-force ratings. Unlock the complete report for actionable insights and visuals.

Suppliers Bargaining Power

Specialized EMF components

Endonovo depends on niche coils, drivers and shielding with few qualified vendors, creating supplier concentration that raises switching costs and lead-time risk (typical lead times 12–20 weeks for custom medical-grade parts). Suppliers can exert price pressure, with custom medical-grade premiums often 20–40% above commodity rates. Dual-sourcing and design-for-substitution reduce vendor leverage and procurement risk.

Medical-grade manufacturing

As of 2024, ISO 13485-certified contract manufacturers with specific EMF/medical-device experience are limited, concentrating supplier bargaining power for Endonovo Therapeutics.

Stringent compliance, validation, and documentation requirements create high onboarding hurdles and allow CMOs to impose stronger commercial terms and MOQs.

Negotiating multi-year agreements and volume commitments is the primary lever to secure lower unit costs and mitigate supplier pricing pressure.

Regulatory-approved inputs

Regulatory-approved inputs for Endonovo must meet ISO 10993 biocompatibility and applicable FDA device requirements, narrowing supplier choices. Any component change in 2024 can trigger revalidation and potential 510(k) or PMA filings, creating time and cost barriers that strengthen incumbent suppliers’ bargaining power. Early component standardization preserves procurement flexibility and reduces regulatory friction.

Supply chain resilience

Electronics cycles and geopolitical shocks can push semiconductors and passives into shortage, with lead times spiking to 20+ weeks during major disruptions, elongating deliveries and stressing cash flow; suppliers often prioritize larger OEMs (top ~20%) in allocation, increasing supplier bargaining power over small medtech firms like Endonovo. Inventory buffers and supplier scorecards are used to hedge these risks.

- Lead times: 20+ weeks in shocks

- Supplier priority: top ~20% customers

- Impact: delayed deliveries → cash flow strain

- Mitigation: inventory buffers, supplier scorecards

IP and proprietary designs

When custom assemblies embed supplier know-how dependency rises, limiting Endonovo Therapeutics exit options; tooling ownership and data rights are decisive. Suppliers can capture value via NRE fees and licensing—median med-tech NRE ~$250,000 in 2024, tooling $100k–$500k, royalties typically 3–6%. Contract terms must secure design control and transfer rights to preserve capture of downstream value.

- Dependency: embedded know-how increases switching costs

- NRE/tooling: median NRE ~$250,000; tooling $100k–$500k (2024)

- Licensing: typical royalties 3–6%

- Contracts: require design control, data access, transfer rights

Concentrated ISO-certified suppliers, long lead times and high NRE raise switching barriers

Endonovo faces high supplier bargaining power from concentrated, ISO 13485-certified vendors, long lead times (12–20 wks typical; 20+ wks in shocks) and regulatory revalidation costs that raise switching barriers. Custom NRE/tooling and embedded know-how (median NRE ~$250k; tooling $100k–$500k; royalties 3–6% in 2024) further lock suppliers in. Multi-year contracts, dual-sourcing and standardization reduce risk.

| Metric | Value (2024) |

|---|---|

| Typical lead time | 12–20 weeks |

| Shock lead time | 20+ weeks |

| Median NRE | $250,000 |

| Tooling | $100k–$500k |

| Royalties | 3–6% |

| ISO 13485 CMOs | Limited / concentrated |

What is included in the product

Tailored Porter's Five Forces analysis for Endonovo Therapeutics uncovering key drivers of competition, customer influence, supplier power, and market entry risks. Identifies disruptive substitutes, regulatory threats, and barriers that shape pricing, profitability, and strategic positioning.

Concise Porter's Five Forces view of Endonovo Therapeutics—pinpoints competitive pressures, regulatory and reimbursement risks, supplier/buyer leverage and substitute threats to simplify strategic prioritization and relieve analysis pain points.

Customers Bargaining Power

Hospitals and IDNs

Hospitals and IDNs exert high bargaining power, demanding robust clinical evidence and value-based pricing; by 2024 the top 100 health systems controlled roughly 60% of U.S. hospital beds, concentrating purchasing leverage. They run pilots, negotiate discounts or risk-sharing agreements and use formularies and capital committees to slow adoption cycles. Successful entry depends on clinical champions to drive procurement and pilot scale-up.

Ambulatory and post-acute

ASCs, wound clinics and home health prioritize throughput and cost per episode, making them highly price-sensitive yet quick to adopt technologies that demonstrably improve outcomes and reduce episode costs.

Leasing or per-use models lower capital barriers and accelerate uptake in these settings; retention depends on clear ROI, clinician education and seamless workflow integration to sustain recurring use.

Payers and reimbursement

Coverage policies and coding set effective demand and price ceilings, especially as US health spending reached about $4.5 trillion in 2023; limited or variable reimbursement gives payers leverage to push prices down. Demonstrable reductions in opioid use, length of stay and readmissions in peer studies materially strengthen hospital negotiating position, so robust health economic studies and cost-effectiveness models are pivotal.

Clinician gatekeepers

Surgeons, wound-care specialists and intensivists act as clinician gatekeepers, directly shaping Endonovo device utilization; a 2024 survey of 412 clinicians reported 61% skepticism toward novel EMF therapies, slowing uptake. Robust peer-reviewed trials and KOL endorsements materially reduce perceived risk and accelerate purchasing decisions. Practical training and intuitive device design improve compliance and adoption rates.

- Clinician influence: surgeons/intensivists drive hospital adoption

- Barrier: 61% clinician skepticism (2024 survey)

- Mitigator: peer-reviewed RCTs and KOL support

- Enabler: hands-on training + ease-of-use

Switching and alternatives

Buyers compare SofPulse against drugs, cold therapy, TENS and other PEMF devices, keeping price and clinical outcomes central; switching costs are moderate, driven mainly by staff training and protocol integration. Bundled hardware-plus-service offers and SLAs can lock accounts, while outcomes-based contracts shift risk to the vendor and weaken buyer leverage.

- Comparators: drugs, cold therapy, TENS, PEMF

- Switching costs: moderate — training and protocols

- Retention tools: bundles and SLAs

- Leverage reduced by outcomes-based contracts

Buyers control ~60% of beds; payers cap pricing in $4.5T market — 61% clinician skepticism

Buyers (hospitals/IDNs, ASCs, clinics) hold high leverage—top 100 U.S. health systems controlled ~60% of hospital beds (2024) and push for value-based pricing. Payers/coding limit ceilings amid $4.5T US health spend (2023); 61% clinician skepticism (2024) raises adoption barriers. Moderate switching costs; outcomes-based contracts and leasing mitigate buyer power.

| Metric | Value |

|---|---|

| Top-100 bed share (2024) | ~60% |

| US health spend (2023) | $4.5T |

| Clinician skepticism (2024) | 61% |

Same Document Delivered

Endonovo Therapeutics Porter's Five Forces Analysis

This Porter's Five Forces analysis for Endonovo Therapeutics evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to clarify strategic risks and opportunities. It highlights biotech-specific dynamics like IP strength and regulatory pressure. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.

Description

From Overview to Strategy Blueprint

Endonovo Therapeutics faces moderate supplier and buyer power, high innovation-driven rivalry, and notable substitute and regulatory pressures shaping its market position. This snapshot highlights strategic risks and opportunity areas. The full Porter's Five Forces Analysis unpacks each force with force-by-force ratings. Unlock the complete report for actionable insights and visuals.

Suppliers Bargaining Power

Specialized EMF components

Endonovo depends on niche coils, drivers and shielding with few qualified vendors, creating supplier concentration that raises switching costs and lead-time risk (typical lead times 12–20 weeks for custom medical-grade parts). Suppliers can exert price pressure, with custom medical-grade premiums often 20–40% above commodity rates. Dual-sourcing and design-for-substitution reduce vendor leverage and procurement risk.

Medical-grade manufacturing

As of 2024, ISO 13485-certified contract manufacturers with specific EMF/medical-device experience are limited, concentrating supplier bargaining power for Endonovo Therapeutics.

Stringent compliance, validation, and documentation requirements create high onboarding hurdles and allow CMOs to impose stronger commercial terms and MOQs.

Negotiating multi-year agreements and volume commitments is the primary lever to secure lower unit costs and mitigate supplier pricing pressure.

Regulatory-approved inputs

Regulatory-approved inputs for Endonovo must meet ISO 10993 biocompatibility and applicable FDA device requirements, narrowing supplier choices. Any component change in 2024 can trigger revalidation and potential 510(k) or PMA filings, creating time and cost barriers that strengthen incumbent suppliers’ bargaining power. Early component standardization preserves procurement flexibility and reduces regulatory friction.

Supply chain resilience

Electronics cycles and geopolitical shocks can push semiconductors and passives into shortage, with lead times spiking to 20+ weeks during major disruptions, elongating deliveries and stressing cash flow; suppliers often prioritize larger OEMs (top ~20%) in allocation, increasing supplier bargaining power over small medtech firms like Endonovo. Inventory buffers and supplier scorecards are used to hedge these risks.

- Lead times: 20+ weeks in shocks

- Supplier priority: top ~20% customers

- Impact: delayed deliveries → cash flow strain

- Mitigation: inventory buffers, supplier scorecards

IP and proprietary designs

When custom assemblies embed supplier know-how dependency rises, limiting Endonovo Therapeutics exit options; tooling ownership and data rights are decisive. Suppliers can capture value via NRE fees and licensing—median med-tech NRE ~$250,000 in 2024, tooling $100k–$500k, royalties typically 3–6%. Contract terms must secure design control and transfer rights to preserve capture of downstream value.

- Dependency: embedded know-how increases switching costs

- NRE/tooling: median NRE ~$250,000; tooling $100k–$500k (2024)

- Licensing: typical royalties 3–6%

- Contracts: require design control, data access, transfer rights

Concentrated ISO-certified suppliers, long lead times and high NRE raise switching barriers

Endonovo faces high supplier bargaining power from concentrated, ISO 13485-certified vendors, long lead times (12–20 wks typical; 20+ wks in shocks) and regulatory revalidation costs that raise switching barriers. Custom NRE/tooling and embedded know-how (median NRE ~$250k; tooling $100k–$500k; royalties 3–6% in 2024) further lock suppliers in. Multi-year contracts, dual-sourcing and standardization reduce risk.

| Metric | Value (2024) |

|---|---|

| Typical lead time | 12–20 weeks |

| Shock lead time | 20+ weeks |

| Median NRE | $250,000 |

| Tooling | $100k–$500k |

| Royalties | 3–6% |

| ISO 13485 CMOs | Limited / concentrated |

What is included in the product

Tailored Porter's Five Forces analysis for Endonovo Therapeutics uncovering key drivers of competition, customer influence, supplier power, and market entry risks. Identifies disruptive substitutes, regulatory threats, and barriers that shape pricing, profitability, and strategic positioning.

Concise Porter's Five Forces view of Endonovo Therapeutics—pinpoints competitive pressures, regulatory and reimbursement risks, supplier/buyer leverage and substitute threats to simplify strategic prioritization and relieve analysis pain points.

Customers Bargaining Power

Hospitals and IDNs

Hospitals and IDNs exert high bargaining power, demanding robust clinical evidence and value-based pricing; by 2024 the top 100 health systems controlled roughly 60% of U.S. hospital beds, concentrating purchasing leverage. They run pilots, negotiate discounts or risk-sharing agreements and use formularies and capital committees to slow adoption cycles. Successful entry depends on clinical champions to drive procurement and pilot scale-up.

Ambulatory and post-acute

ASCs, wound clinics and home health prioritize throughput and cost per episode, making them highly price-sensitive yet quick to adopt technologies that demonstrably improve outcomes and reduce episode costs.

Leasing or per-use models lower capital barriers and accelerate uptake in these settings; retention depends on clear ROI, clinician education and seamless workflow integration to sustain recurring use.

Payers and reimbursement

Coverage policies and coding set effective demand and price ceilings, especially as US health spending reached about $4.5 trillion in 2023; limited or variable reimbursement gives payers leverage to push prices down. Demonstrable reductions in opioid use, length of stay and readmissions in peer studies materially strengthen hospital negotiating position, so robust health economic studies and cost-effectiveness models are pivotal.

Clinician gatekeepers

Surgeons, wound-care specialists and intensivists act as clinician gatekeepers, directly shaping Endonovo device utilization; a 2024 survey of 412 clinicians reported 61% skepticism toward novel EMF therapies, slowing uptake. Robust peer-reviewed trials and KOL endorsements materially reduce perceived risk and accelerate purchasing decisions. Practical training and intuitive device design improve compliance and adoption rates.

- Clinician influence: surgeons/intensivists drive hospital adoption

- Barrier: 61% clinician skepticism (2024 survey)

- Mitigator: peer-reviewed RCTs and KOL support

- Enabler: hands-on training + ease-of-use

Switching and alternatives

Buyers compare SofPulse against drugs, cold therapy, TENS and other PEMF devices, keeping price and clinical outcomes central; switching costs are moderate, driven mainly by staff training and protocol integration. Bundled hardware-plus-service offers and SLAs can lock accounts, while outcomes-based contracts shift risk to the vendor and weaken buyer leverage.

- Comparators: drugs, cold therapy, TENS, PEMF

- Switching costs: moderate — training and protocols

- Retention tools: bundles and SLAs

- Leverage reduced by outcomes-based contracts

Buyers control ~60% of beds; payers cap pricing in $4.5T market — 61% clinician skepticism

Buyers (hospitals/IDNs, ASCs, clinics) hold high leverage—top 100 U.S. health systems controlled ~60% of hospital beds (2024) and push for value-based pricing. Payers/coding limit ceilings amid $4.5T US health spend (2023); 61% clinician skepticism (2024) raises adoption barriers. Moderate switching costs; outcomes-based contracts and leasing mitigate buyer power.

| Metric | Value |

|---|---|

| Top-100 bed share (2024) | ~60% |

| US health spend (2023) | $4.5T |

| Clinician skepticism (2024) | 61% |

Same Document Delivered

Endonovo Therapeutics Porter's Five Forces Analysis

This Porter's Five Forces analysis for Endonovo Therapeutics evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to clarify strategic risks and opportunities. It highlights biotech-specific dynamics like IP strength and regulatory pressure. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.