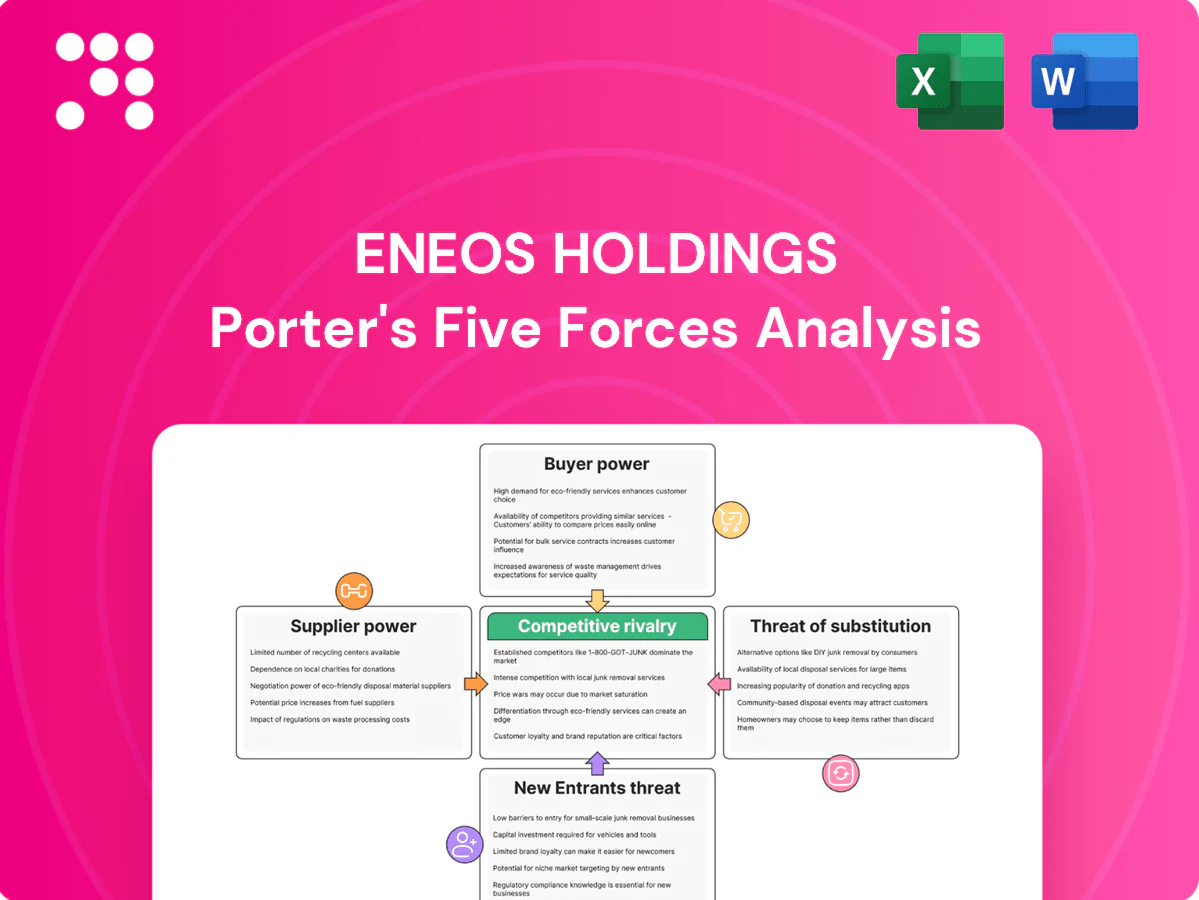

ENEOS Holdings Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

ENEOS Holdings faces moderate supplier power, intense industry rivalry, rising substitute threats from electrification, and regulatory plus capital barriers that jointly shape margins and strategic choices. This snapshot highlights key competitive pressures and implications for investors and managers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Concentrated crude sources

ENEOS relies on a concentrated set of crude suppliers, notably OPEC+ and Middle Eastern producers; OPEC+ supplied about 45% of global crude in 2024 and Japan sourced roughly 88% of its crude from the Middle East, concentrating feedstock risk. Supply curtailments or geopolitical events can rapidly tighten availability; long-term contracts and blending of diverse grades partly mitigate price spikes. Benchmarks like Brent pass through quickly to refining margins, making GRMs highly sensitive to crude moves.

Specialized refining inputs

Catalysts, process chemicals and turnaround services are supplied by a small set of global specialists, concentrating procurement risk and giving those vendors leverage over pricing and lead times. Vendor switching is complex due to lengthy qualification cycles and performance risks, raising switching costs. This supplier concentration strengthens negotiating power, though multi-sourcing and building in-house catalyst handling and maintenance capabilities can materially reduce ENEOSs dependence.

Logistics and shipping constraints

Tanker availability, freight rates and port slot congestion directly constrain ENEOS crude and product flows; 2024 saw tighter spot markets that raised short-term shipping costs. Regulatory shifts such as IMO rules and regional emissions measures increased compliance costs for carriers in 2024. Local pipeline and storage providers exert bargaining leverage on terminal terms. Long-term charters and integrated logistics reduce but do not eliminate cost spikes.

Renewables and hydrogen equipment

Solar modules, wind turbines, electrolyzers and batteries are supplied by concentrated OEMs and mineral chains (top five solar makers >70% of shipments in 2023–24; top five battery cell makers ~80% capacity), giving suppliers pricing power; lead times of 12–24 months and raw-material price swings can shift project economics and IRR by roughly 5–20 percentage points, while proprietary tech allows margin premia; strategic alliances and framework deals improve visibility and reduce execution risk.

- Concentration: top OEMs dominate supply

- Lead times: 12–24 months

- Price impact: IRR swings ~5–20pp

- Proprietary tech = higher margins

- Alliances/frameworks = better visibility

Power grid access

Grid operators and interconnection queues act as gatekeepers for new ENEOS projects, with US queues topping roughly 3,000 GW in 2024, heightening access competition. Delays and cost-sharing (network upgrades) shift capital and behave like supplier power, while curtailment risk can cut project IRRs by double digits. Early queue positioning and flexible siting mitigate exposure.

- Gatekeeping: queues >3,000 GW (2024)

- Cost shift: network upgrade charges raise CAPEX

- Curtailment: potential double-digit IRR impact

- Mitigation: early queue + flexible sites

OPEC+ ~45% and Japan 88% ME crude concentrate supply; renewables, grid gatekeepers add leverage

Supplier power is high: OPEC+ supplied ~45% of global crude in 2024 and Japan sourced ~88% of its crude from the Middle East, concentrating feedstock risk. Catalysts, tankers and specialized turnaround services come from few global vendors, raising switching costs. Renewable OEM concentration (top5 solar >70% shipments; top5 battery ~80% capacity) and grid gatekeepers (US queues ~3,000 GW in 2024) add leverage.

| Metric | Value |

|---|---|

| OPEC+ share (2024) | ~45% |

| Japan ME crude (2024) | ~88% |

| Top5 solar (2023–24) | >70% |

| Top5 battery (2024) | ~80% |

| US interconnection queues (2024) | ~3,000 GW |

What is included in the product

Tailored exclusively for ENEOS Holdings, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, threat of substitutes, and entry barriers—identifying disruptive forces and strategic vulnerabilities to inform pricing, profitability, and defensive growth strategies.

One-sheet Porter's Five Forces for ENEOS Holdings—customizable pressure levels and instant spider chart visualization to clarify competitive threats and opportunities. Clean, copy-ready layout with no macros, easy integration into decks or Excel dashboards for fast strategic decisions.

Customers Bargaining Power

Price-transparent fuels

Retail fuel prices are highly transparent and consumers compare pumps in real time, keeping demand price-elastic with short-run elasticity around -0.2 to -0.3 (2024 estimates).

Easy station switching constrains ENEOS pricing power; loyalty programs improve retention but are not decisive.

Retail margins in Japan remain thin—single-digit yen per liter in 2024—so profitability hinges on operational efficiency and ancillary sales (convenience stores, services).

Wholesale and industrial buyers

Large distributors, airlines, shippers and petrochemical buyers extract volume discounts through centralized procurement and frequent contract tenders, raising price pressure and service-level demands. Standardization of fuels keeps switching costs moderate, enabling buyers to play suppliers off each other. ENEOS can build stickiness via superior reliability and logistics performance, turning delivery consistency into a competitive moat.

Utilities and PPA counterparties

Utilities and PPA counterparties exert strong bargaining power: auctions and bilateral PPAs subject pricing to tight scrutiny, with typical PPA tenors of 10–20 years and bankability clauses favoring buyers. Curtailment and revenue-protection terms are often buyer-centric, so ENEOS leverages its credit strength and multi‑year delivery track record to differentiate. Co‑development deals are used to rebalance terms and de‑risk projects; ENEOS targets ~2 GW renewables by 2030 to strengthen its position.

Lubricants and specialty products

- Differentiation: OEM approvals

- Switching friction: warranties

- Buyer pressure: fleets seek low bids

- Margin defense: services & contracts

Hydrogen early adopters

Hydrogen early adopters face a nascent, subsidy-driven market with few anchor customers, giving buyers outsized leverage on offtake price and purity specs; long-term offtake contracts are critical to project financing. Japan targets about 300,000 tonnes/year of hydrogen by 2030, underscoring policy-driven demand. Co-location and integration (electrolyzer + renewables) materially lower delivered cost and risk.

- Market stage: nascent, subsidy-driven

- Buyer leverage: high on price & specs

- Financing: long-term offtakes essential

- Cost mitigation: co-location cuts delivery costs

Buyer power tightens fuel margins; lubricants and hydrogen shift industry leverage

Customers have high bargaining power: retail price transparency keeps short-run price elasticity around -0.2 to -0.3 (2024), and station switching is easy. Retail margins remain thin—single-digit yen per liter in 2024—so volume buyers and fleets extract discounts. Lubricants (global market ~USD 42bn in 2024) and OEM approvals reduce buyer power; hydrogen buyers hold strong leverage in a nascent market.

| Metric | 2024/Target |

|---|---|

| Retail elasticity | -0.2 to -0.3 |

| Retail margin | Single-digit JPY/L |

| Lubricants market | ~USD 42bn |

| Renewables target (ENEOS) | ~2 GW by 2030 |

Preview Before You Purchase

ENEOS Holdings Porter's Five Forces Analysis

This preview shows the exact ENEOS Holdings Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders. It provides a full, professionally formatted assessment of competitive rivalry, supplier and buyer power, and threats of substitution and entry. The document includes clear strategic implications and is available for instant download, ready to use.

Go Beyond the Preview—Access the Full Strategic Report

ENEOS Holdings faces moderate supplier power, intense industry rivalry, rising substitute threats from electrification, and regulatory plus capital barriers that jointly shape margins and strategic choices. This snapshot highlights key competitive pressures and implications for investors and managers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Concentrated crude sources

ENEOS relies on a concentrated set of crude suppliers, notably OPEC+ and Middle Eastern producers; OPEC+ supplied about 45% of global crude in 2024 and Japan sourced roughly 88% of its crude from the Middle East, concentrating feedstock risk. Supply curtailments or geopolitical events can rapidly tighten availability; long-term contracts and blending of diverse grades partly mitigate price spikes. Benchmarks like Brent pass through quickly to refining margins, making GRMs highly sensitive to crude moves.

Specialized refining inputs

Catalysts, process chemicals and turnaround services are supplied by a small set of global specialists, concentrating procurement risk and giving those vendors leverage over pricing and lead times. Vendor switching is complex due to lengthy qualification cycles and performance risks, raising switching costs. This supplier concentration strengthens negotiating power, though multi-sourcing and building in-house catalyst handling and maintenance capabilities can materially reduce ENEOSs dependence.

Logistics and shipping constraints

Tanker availability, freight rates and port slot congestion directly constrain ENEOS crude and product flows; 2024 saw tighter spot markets that raised short-term shipping costs. Regulatory shifts such as IMO rules and regional emissions measures increased compliance costs for carriers in 2024. Local pipeline and storage providers exert bargaining leverage on terminal terms. Long-term charters and integrated logistics reduce but do not eliminate cost spikes.

Renewables and hydrogen equipment

Solar modules, wind turbines, electrolyzers and batteries are supplied by concentrated OEMs and mineral chains (top five solar makers >70% of shipments in 2023–24; top five battery cell makers ~80% capacity), giving suppliers pricing power; lead times of 12–24 months and raw-material price swings can shift project economics and IRR by roughly 5–20 percentage points, while proprietary tech allows margin premia; strategic alliances and framework deals improve visibility and reduce execution risk.

- Concentration: top OEMs dominate supply

- Lead times: 12–24 months

- Price impact: IRR swings ~5–20pp

- Proprietary tech = higher margins

- Alliances/frameworks = better visibility

Power grid access

Grid operators and interconnection queues act as gatekeepers for new ENEOS projects, with US queues topping roughly 3,000 GW in 2024, heightening access competition. Delays and cost-sharing (network upgrades) shift capital and behave like supplier power, while curtailment risk can cut project IRRs by double digits. Early queue positioning and flexible siting mitigate exposure.

- Gatekeeping: queues >3,000 GW (2024)

- Cost shift: network upgrade charges raise CAPEX

- Curtailment: potential double-digit IRR impact

- Mitigation: early queue + flexible sites

OPEC+ ~45% and Japan 88% ME crude concentrate supply; renewables, grid gatekeepers add leverage

Supplier power is high: OPEC+ supplied ~45% of global crude in 2024 and Japan sourced ~88% of its crude from the Middle East, concentrating feedstock risk. Catalysts, tankers and specialized turnaround services come from few global vendors, raising switching costs. Renewable OEM concentration (top5 solar >70% shipments; top5 battery ~80% capacity) and grid gatekeepers (US queues ~3,000 GW in 2024) add leverage.

| Metric | Value |

|---|---|

| OPEC+ share (2024) | ~45% |

| Japan ME crude (2024) | ~88% |

| Top5 solar (2023–24) | >70% |

| Top5 battery (2024) | ~80% |

| US interconnection queues (2024) | ~3,000 GW |

What is included in the product

Tailored exclusively for ENEOS Holdings, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, threat of substitutes, and entry barriers—identifying disruptive forces and strategic vulnerabilities to inform pricing, profitability, and defensive growth strategies.

One-sheet Porter's Five Forces for ENEOS Holdings—customizable pressure levels and instant spider chart visualization to clarify competitive threats and opportunities. Clean, copy-ready layout with no macros, easy integration into decks or Excel dashboards for fast strategic decisions.

Customers Bargaining Power

Price-transparent fuels

Retail fuel prices are highly transparent and consumers compare pumps in real time, keeping demand price-elastic with short-run elasticity around -0.2 to -0.3 (2024 estimates).

Easy station switching constrains ENEOS pricing power; loyalty programs improve retention but are not decisive.

Retail margins in Japan remain thin—single-digit yen per liter in 2024—so profitability hinges on operational efficiency and ancillary sales (convenience stores, services).

Wholesale and industrial buyers

Large distributors, airlines, shippers and petrochemical buyers extract volume discounts through centralized procurement and frequent contract tenders, raising price pressure and service-level demands. Standardization of fuels keeps switching costs moderate, enabling buyers to play suppliers off each other. ENEOS can build stickiness via superior reliability and logistics performance, turning delivery consistency into a competitive moat.

Utilities and PPA counterparties

Utilities and PPA counterparties exert strong bargaining power: auctions and bilateral PPAs subject pricing to tight scrutiny, with typical PPA tenors of 10–20 years and bankability clauses favoring buyers. Curtailment and revenue-protection terms are often buyer-centric, so ENEOS leverages its credit strength and multi‑year delivery track record to differentiate. Co‑development deals are used to rebalance terms and de‑risk projects; ENEOS targets ~2 GW renewables by 2030 to strengthen its position.

Lubricants and specialty products

- Differentiation: OEM approvals

- Switching friction: warranties

- Buyer pressure: fleets seek low bids

- Margin defense: services & contracts

Hydrogen early adopters

Hydrogen early adopters face a nascent, subsidy-driven market with few anchor customers, giving buyers outsized leverage on offtake price and purity specs; long-term offtake contracts are critical to project financing. Japan targets about 300,000 tonnes/year of hydrogen by 2030, underscoring policy-driven demand. Co-location and integration (electrolyzer + renewables) materially lower delivered cost and risk.

- Market stage: nascent, subsidy-driven

- Buyer leverage: high on price & specs

- Financing: long-term offtakes essential

- Cost mitigation: co-location cuts delivery costs

Buyer power tightens fuel margins; lubricants and hydrogen shift industry leverage

Customers have high bargaining power: retail price transparency keeps short-run price elasticity around -0.2 to -0.3 (2024), and station switching is easy. Retail margins remain thin—single-digit yen per liter in 2024—so volume buyers and fleets extract discounts. Lubricants (global market ~USD 42bn in 2024) and OEM approvals reduce buyer power; hydrogen buyers hold strong leverage in a nascent market.

| Metric | 2024/Target |

|---|---|

| Retail elasticity | -0.2 to -0.3 |

| Retail margin | Single-digit JPY/L |

| Lubricants market | ~USD 42bn |

| Renewables target (ENEOS) | ~2 GW by 2030 |

Preview Before You Purchase

ENEOS Holdings Porter's Five Forces Analysis

This preview shows the exact ENEOS Holdings Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders. It provides a full, professionally formatted assessment of competitive rivalry, supplier and buyer power, and threats of substitution and entry. The document includes clear strategic implications and is available for instant download, ready to use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

ENEOS Holdings faces moderate supplier power, intense industry rivalry, rising substitute threats from electrification, and regulatory plus capital barriers that jointly shape margins and strategic choices. This snapshot highlights key competitive pressures and implications for investors and managers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations to guide investment or strategy.

Suppliers Bargaining Power

Concentrated crude sources

ENEOS relies on a concentrated set of crude suppliers, notably OPEC+ and Middle Eastern producers; OPEC+ supplied about 45% of global crude in 2024 and Japan sourced roughly 88% of its crude from the Middle East, concentrating feedstock risk. Supply curtailments or geopolitical events can rapidly tighten availability; long-term contracts and blending of diverse grades partly mitigate price spikes. Benchmarks like Brent pass through quickly to refining margins, making GRMs highly sensitive to crude moves.

Specialized refining inputs

Catalysts, process chemicals and turnaround services are supplied by a small set of global specialists, concentrating procurement risk and giving those vendors leverage over pricing and lead times. Vendor switching is complex due to lengthy qualification cycles and performance risks, raising switching costs. This supplier concentration strengthens negotiating power, though multi-sourcing and building in-house catalyst handling and maintenance capabilities can materially reduce ENEOSs dependence.

Logistics and shipping constraints

Tanker availability, freight rates and port slot congestion directly constrain ENEOS crude and product flows; 2024 saw tighter spot markets that raised short-term shipping costs. Regulatory shifts such as IMO rules and regional emissions measures increased compliance costs for carriers in 2024. Local pipeline and storage providers exert bargaining leverage on terminal terms. Long-term charters and integrated logistics reduce but do not eliminate cost spikes.

Renewables and hydrogen equipment

Solar modules, wind turbines, electrolyzers and batteries are supplied by concentrated OEMs and mineral chains (top five solar makers >70% of shipments in 2023–24; top five battery cell makers ~80% capacity), giving suppliers pricing power; lead times of 12–24 months and raw-material price swings can shift project economics and IRR by roughly 5–20 percentage points, while proprietary tech allows margin premia; strategic alliances and framework deals improve visibility and reduce execution risk.

- Concentration: top OEMs dominate supply

- Lead times: 12–24 months

- Price impact: IRR swings ~5–20pp

- Proprietary tech = higher margins

- Alliances/frameworks = better visibility

Power grid access

Grid operators and interconnection queues act as gatekeepers for new ENEOS projects, with US queues topping roughly 3,000 GW in 2024, heightening access competition. Delays and cost-sharing (network upgrades) shift capital and behave like supplier power, while curtailment risk can cut project IRRs by double digits. Early queue positioning and flexible siting mitigate exposure.

- Gatekeeping: queues >3,000 GW (2024)

- Cost shift: network upgrade charges raise CAPEX

- Curtailment: potential double-digit IRR impact

- Mitigation: early queue + flexible sites

OPEC+ ~45% and Japan 88% ME crude concentrate supply; renewables, grid gatekeepers add leverage

Supplier power is high: OPEC+ supplied ~45% of global crude in 2024 and Japan sourced ~88% of its crude from the Middle East, concentrating feedstock risk. Catalysts, tankers and specialized turnaround services come from few global vendors, raising switching costs. Renewable OEM concentration (top5 solar >70% shipments; top5 battery ~80% capacity) and grid gatekeepers (US queues ~3,000 GW in 2024) add leverage.

| Metric | Value |

|---|---|

| OPEC+ share (2024) | ~45% |

| Japan ME crude (2024) | ~88% |

| Top5 solar (2023–24) | >70% |

| Top5 battery (2024) | ~80% |

| US interconnection queues (2024) | ~3,000 GW |

What is included in the product

Tailored exclusively for ENEOS Holdings, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, threat of substitutes, and entry barriers—identifying disruptive forces and strategic vulnerabilities to inform pricing, profitability, and defensive growth strategies.

One-sheet Porter's Five Forces for ENEOS Holdings—customizable pressure levels and instant spider chart visualization to clarify competitive threats and opportunities. Clean, copy-ready layout with no macros, easy integration into decks or Excel dashboards for fast strategic decisions.

Customers Bargaining Power

Price-transparent fuels

Retail fuel prices are highly transparent and consumers compare pumps in real time, keeping demand price-elastic with short-run elasticity around -0.2 to -0.3 (2024 estimates).

Easy station switching constrains ENEOS pricing power; loyalty programs improve retention but are not decisive.

Retail margins in Japan remain thin—single-digit yen per liter in 2024—so profitability hinges on operational efficiency and ancillary sales (convenience stores, services).

Wholesale and industrial buyers

Large distributors, airlines, shippers and petrochemical buyers extract volume discounts through centralized procurement and frequent contract tenders, raising price pressure and service-level demands. Standardization of fuels keeps switching costs moderate, enabling buyers to play suppliers off each other. ENEOS can build stickiness via superior reliability and logistics performance, turning delivery consistency into a competitive moat.

Utilities and PPA counterparties

Utilities and PPA counterparties exert strong bargaining power: auctions and bilateral PPAs subject pricing to tight scrutiny, with typical PPA tenors of 10–20 years and bankability clauses favoring buyers. Curtailment and revenue-protection terms are often buyer-centric, so ENEOS leverages its credit strength and multi‑year delivery track record to differentiate. Co‑development deals are used to rebalance terms and de‑risk projects; ENEOS targets ~2 GW renewables by 2030 to strengthen its position.

Lubricants and specialty products

- Differentiation: OEM approvals

- Switching friction: warranties

- Buyer pressure: fleets seek low bids

- Margin defense: services & contracts

Hydrogen early adopters

Hydrogen early adopters face a nascent, subsidy-driven market with few anchor customers, giving buyers outsized leverage on offtake price and purity specs; long-term offtake contracts are critical to project financing. Japan targets about 300,000 tonnes/year of hydrogen by 2030, underscoring policy-driven demand. Co-location and integration (electrolyzer + renewables) materially lower delivered cost and risk.

- Market stage: nascent, subsidy-driven

- Buyer leverage: high on price & specs

- Financing: long-term offtakes essential

- Cost mitigation: co-location cuts delivery costs

Buyer power tightens fuel margins; lubricants and hydrogen shift industry leverage

Customers have high bargaining power: retail price transparency keeps short-run price elasticity around -0.2 to -0.3 (2024), and station switching is easy. Retail margins remain thin—single-digit yen per liter in 2024—so volume buyers and fleets extract discounts. Lubricants (global market ~USD 42bn in 2024) and OEM approvals reduce buyer power; hydrogen buyers hold strong leverage in a nascent market.

| Metric | 2024/Target |

|---|---|

| Retail elasticity | -0.2 to -0.3 |

| Retail margin | Single-digit JPY/L |

| Lubricants market | ~USD 42bn |

| Renewables target (ENEOS) | ~2 GW by 2030 |

Preview Before You Purchase

ENEOS Holdings Porter's Five Forces Analysis

This preview shows the exact ENEOS Holdings Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders. It provides a full, professionally formatted assessment of competitive rivalry, supplier and buyer power, and threats of substitution and entry. The document includes clear strategic implications and is available for instant download, ready to use.