Enova Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Enova faces intense buyer pressure, moderate supplier leverage, significant threat from fintech substitutes, and regulatory and entry barriers that shape its competitive landscape. This brief snapshot highlights strategic risks and growth levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Enova’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Funding sources concentration

Enova funds originations via credit facilities, securitizations and institutional investors; a concentrated set of warehouse lenders or ABS buyers can press pricing, covenants and advance rates. Tight 2024 capital markets raised funding costs and constrained growth, while Enova's diversified, committed facilities and roughly $1.0 billion of liquidity in 2024 reduced supplier leverage.

Data and credit bureau dependence

Enova depends on the three major credit bureaus—Experian, Equifax, TransUnion—plus alternative data and ID/fraud providers as critical inputs to underwriting, giving these suppliers strong bargaining power due to limited substitutability for high-quality datasets.

Volume-based contracting and multi-vendor sourcing are standard mitigants that can lower pricing pressure and supply risk.

Ongoing CFPB rulemaking and regulatory scrutiny of data use in 2023–24 can amplify dependence by restricting sources or increasing compliance costs for data suppliers and buyers alike.

Cloud and infrastructure platforms

Cloud providers (AWS ~32%, Azure ~23%, Google Cloud ~11% market share in 2024) plus core SaaS and decisioning tools underpin Enova’s real-time lending; high switching costs, integration complexity and strict uptime SLAs grant these suppliers strong bargaining leverage. Reserved instances can cut compute costs up to ~70% and multi-cloud architectures (92% of enterprises use multi-cloud in 2024) can temper dependency. Outages or price hikes directly hit unit economics and margins.

Payments and disbursement networks

Payments and disbursement networks (ACH rails, card networks, instant payout providers) are gatekeepers of customer experience; ACH fees typically run $0.20–$1.50 per transfer while card interchange and assessments average about 1–3% per transaction, and FedNow expanded to 100+ participants by 2024, increasing real-time options. Network fees, chargeback rules and dispute timelines directly drive cost and settlement speed; limited instant-disbursement alternatives strengthen supplier leverage, though multi-processor redundancy can lower pricing pressure and operational risk.

- ACH rails: low per-transfer fees, high latency

- Card networks: 1–3% average cost, strict chargeback rules

- Instant payouts: growing (FedNow 100+ banks by 2024), limited vendors

- Redundancy: multiple processors reduce single-vendor power

Specialized analytics talent

Specialized analytics talent—machine learning engineers (median US base pay ~USD 150,000 in 2024), risk modelers (~USD 130,000) and compliance experts (~USD 120,000)—are scarce and costly, giving candidates leverage on compensation and mobility; strong in-house tooling and culture cut turnover and dependency, while outsourcing analytics raises supplier power and IP risk.

- High pay & scarcity

- Candidate leverage

- Retention via tooling/culture

- Outsourcing = higher supplier/IP risk

Supplier power risks from concentrated funders, 3 bureaus, cloud fees, and scarce ML talent

Enova faces supplier leverage from concentrated funding partners despite ~$1.0B liquidity in 2024. Dependence on three credit bureaus and specialized data raises switching costs. Cloud and payments providers (AWS 32%/Azure 23%/GCP 11% in 2024; ACH $0.20–$1.50; card 1–3%) and scarce analytics talent (ML median ~$150k) strengthen supplier power.

| Supplier | 2024 metric |

|---|---|

| Liquidity | $1.0B |

| Cloud share | AWS32%/Azure23%/GCP11% |

| Credit bureaus | 3 |

| ACH fee | $0.20–$1.50 |

| ML pay | $150k |

What is included in the product

Tailored Porter's Five Forces for Enova that uncovers competitive intensity, buyer/supplier power, substitution risks, and entry barriers with strategic implications.

A concise, one-sheet Porter's Five Forces toolkit for Enova that visualizes competitive pressures, lets you tweak inputs for scenario testing, and exports clean charts for decks—eliminating manual synthesis and speeding board-level decisions.

Customers Bargaining Power

Price sensitivity of non-prime borrowers

Customers of non-prime products are highly price sensitive in 2024, as APRs commonly exceed 100% for short-term loans and small dollar differences in APR/fees drive switching in commoditized offers. Clear disclosures and regulatory limits such as 36% caps in some jurisdictions heighten rate comparison. Fast approval and high instant-decision rates (often under 60 seconds) can blunt some price pressure by delivering value through speed and certainty.

Low switching costs and multi-homing

By 2024 online borrowers commonly apply to multiple lenders simultaneously, with lead marketplaces and broker funnels enabling rapid side-by-side comparisons that erode pricing power. This shifts lender competition toward approval speed and UX differentiation rather than rate alone. Loyalty programs and repeat-customer pricing are increasingly deployed to raise switching frictions and retain higher-value borrowers.

SMB bargaining via brokers

Small businesses commonly source credit through ISOs and online marketplaces, with SMBs comprising 99.9% of US firms per SBA; these intermediaries aggregate dozens of lender options, increasing buyer leverage on rates and covenants. Referral fees, typically 1–5% of loan proceeds, compress lender margins and raise effective borrowing costs. Growth of direct-to-SMB channels and fintech origination lowered intermediary share in 2024, reducing broker pricing power.

Regulatory and reputational leverage

Preference for speed and convenience

Customers value instant decisions and fast funding as much as price; Enova’s 2024 investor materials emphasize approvals in minutes and same-day funding capability, supporting willingness to pay for speed.

Analytics-driven approvals raise conversion and yield, but competitors matching speed in 2024 reintroduce price pressure, keeping buyer power moderate.

- Enova 2024: approvals in minutes; same-day funding

- Speed drives willingness to pay

- Rivals matching speed => price pressure

- UX leadership sustains moderate buyer power

Price-sensitive non-prime market: over 100% APR, sub-60s approval

Customers of non-prime products are highly price sensitive in 2024 with APRs commonly >100% and small fee differences driving switching. Online multi-application behavior and marketplaces erode pricing power; approval speed under 60 seconds and same-day funding provide willingness to pay. SMBs leverage ISOs; 99.9% of US firms are SMBs and referral fees of 1–5% compress margins.

| Metric | 2024 |

|---|---|

| Typical APR (non-prime) | >100% |

| Approval time | <60s |

| SMB share of US firms | 99.9% |

| Referral fees | 1–5% |

Same Document Delivered

Enova Porter's Five Forces Analysis

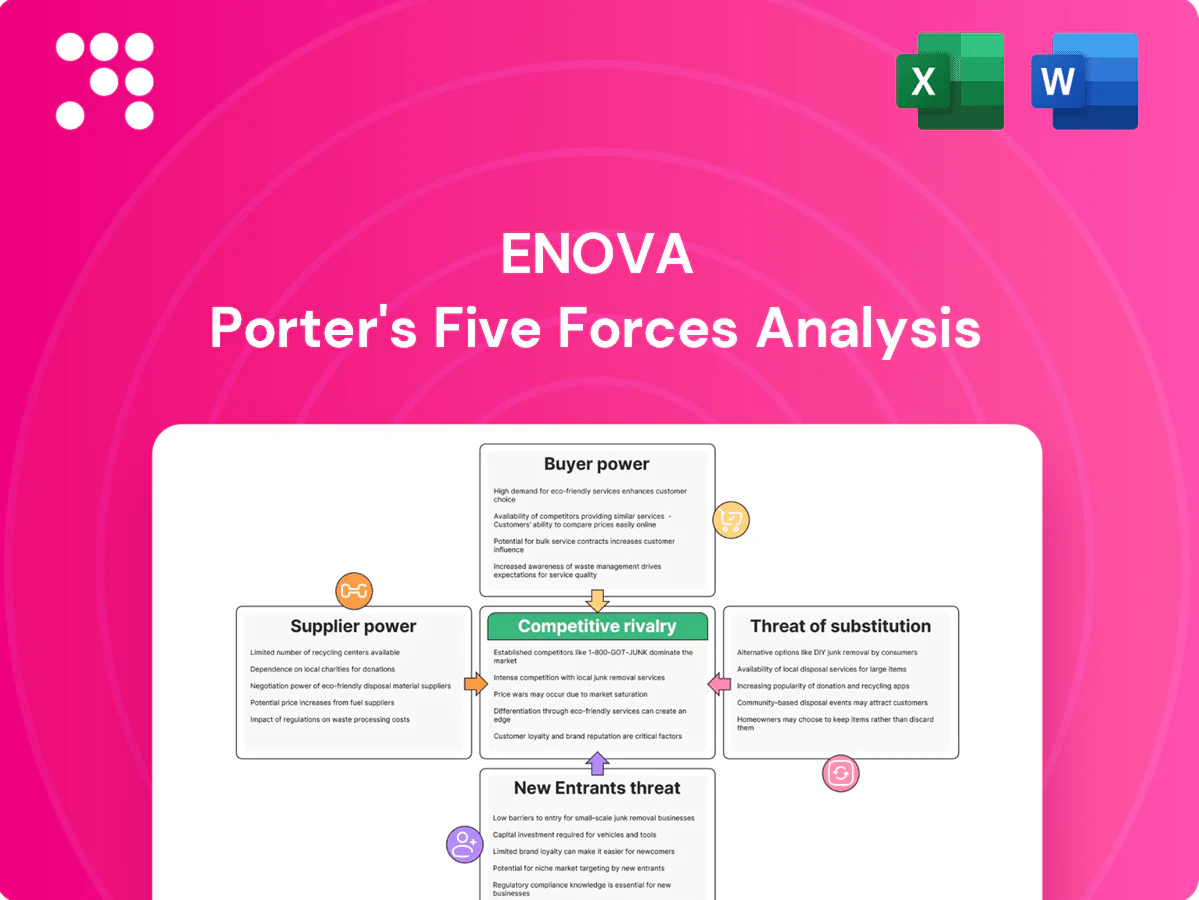

This preview shows the exact Enova Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is the complete, professionally formatted file covering threat of new entrants, bargaining power of buyers and suppliers, threat of substitutes, and competitive rivalry. You’ll get instant access to this identical downloadable file.

A Must-Have Tool for Decision-Makers

Enova faces intense buyer pressure, moderate supplier leverage, significant threat from fintech substitutes, and regulatory and entry barriers that shape its competitive landscape. This brief snapshot highlights strategic risks and growth levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Enova’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Funding sources concentration

Enova funds originations via credit facilities, securitizations and institutional investors; a concentrated set of warehouse lenders or ABS buyers can press pricing, covenants and advance rates. Tight 2024 capital markets raised funding costs and constrained growth, while Enova's diversified, committed facilities and roughly $1.0 billion of liquidity in 2024 reduced supplier leverage.

Data and credit bureau dependence

Enova depends on the three major credit bureaus—Experian, Equifax, TransUnion—plus alternative data and ID/fraud providers as critical inputs to underwriting, giving these suppliers strong bargaining power due to limited substitutability for high-quality datasets.

Volume-based contracting and multi-vendor sourcing are standard mitigants that can lower pricing pressure and supply risk.

Ongoing CFPB rulemaking and regulatory scrutiny of data use in 2023–24 can amplify dependence by restricting sources or increasing compliance costs for data suppliers and buyers alike.

Cloud and infrastructure platforms

Cloud providers (AWS ~32%, Azure ~23%, Google Cloud ~11% market share in 2024) plus core SaaS and decisioning tools underpin Enova’s real-time lending; high switching costs, integration complexity and strict uptime SLAs grant these suppliers strong bargaining leverage. Reserved instances can cut compute costs up to ~70% and multi-cloud architectures (92% of enterprises use multi-cloud in 2024) can temper dependency. Outages or price hikes directly hit unit economics and margins.

Payments and disbursement networks

Payments and disbursement networks (ACH rails, card networks, instant payout providers) are gatekeepers of customer experience; ACH fees typically run $0.20–$1.50 per transfer while card interchange and assessments average about 1–3% per transaction, and FedNow expanded to 100+ participants by 2024, increasing real-time options. Network fees, chargeback rules and dispute timelines directly drive cost and settlement speed; limited instant-disbursement alternatives strengthen supplier leverage, though multi-processor redundancy can lower pricing pressure and operational risk.

- ACH rails: low per-transfer fees, high latency

- Card networks: 1–3% average cost, strict chargeback rules

- Instant payouts: growing (FedNow 100+ banks by 2024), limited vendors

- Redundancy: multiple processors reduce single-vendor power

Specialized analytics talent

Specialized analytics talent—machine learning engineers (median US base pay ~USD 150,000 in 2024), risk modelers (~USD 130,000) and compliance experts (~USD 120,000)—are scarce and costly, giving candidates leverage on compensation and mobility; strong in-house tooling and culture cut turnover and dependency, while outsourcing analytics raises supplier power and IP risk.

- High pay & scarcity

- Candidate leverage

- Retention via tooling/culture

- Outsourcing = higher supplier/IP risk

Supplier power risks from concentrated funders, 3 bureaus, cloud fees, and scarce ML talent

Enova faces supplier leverage from concentrated funding partners despite ~$1.0B liquidity in 2024. Dependence on three credit bureaus and specialized data raises switching costs. Cloud and payments providers (AWS 32%/Azure 23%/GCP 11% in 2024; ACH $0.20–$1.50; card 1–3%) and scarce analytics talent (ML median ~$150k) strengthen supplier power.

| Supplier | 2024 metric |

|---|---|

| Liquidity | $1.0B |

| Cloud share | AWS32%/Azure23%/GCP11% |

| Credit bureaus | 3 |

| ACH fee | $0.20–$1.50 |

| ML pay | $150k |

What is included in the product

Tailored Porter's Five Forces for Enova that uncovers competitive intensity, buyer/supplier power, substitution risks, and entry barriers with strategic implications.

A concise, one-sheet Porter's Five Forces toolkit for Enova that visualizes competitive pressures, lets you tweak inputs for scenario testing, and exports clean charts for decks—eliminating manual synthesis and speeding board-level decisions.

Customers Bargaining Power

Price sensitivity of non-prime borrowers

Customers of non-prime products are highly price sensitive in 2024, as APRs commonly exceed 100% for short-term loans and small dollar differences in APR/fees drive switching in commoditized offers. Clear disclosures and regulatory limits such as 36% caps in some jurisdictions heighten rate comparison. Fast approval and high instant-decision rates (often under 60 seconds) can blunt some price pressure by delivering value through speed and certainty.

Low switching costs and multi-homing

By 2024 online borrowers commonly apply to multiple lenders simultaneously, with lead marketplaces and broker funnels enabling rapid side-by-side comparisons that erode pricing power. This shifts lender competition toward approval speed and UX differentiation rather than rate alone. Loyalty programs and repeat-customer pricing are increasingly deployed to raise switching frictions and retain higher-value borrowers.

SMB bargaining via brokers

Small businesses commonly source credit through ISOs and online marketplaces, with SMBs comprising 99.9% of US firms per SBA; these intermediaries aggregate dozens of lender options, increasing buyer leverage on rates and covenants. Referral fees, typically 1–5% of loan proceeds, compress lender margins and raise effective borrowing costs. Growth of direct-to-SMB channels and fintech origination lowered intermediary share in 2024, reducing broker pricing power.

Regulatory and reputational leverage

Preference for speed and convenience

Customers value instant decisions and fast funding as much as price; Enova’s 2024 investor materials emphasize approvals in minutes and same-day funding capability, supporting willingness to pay for speed.

Analytics-driven approvals raise conversion and yield, but competitors matching speed in 2024 reintroduce price pressure, keeping buyer power moderate.

- Enova 2024: approvals in minutes; same-day funding

- Speed drives willingness to pay

- Rivals matching speed => price pressure

- UX leadership sustains moderate buyer power

Price-sensitive non-prime market: over 100% APR, sub-60s approval

Customers of non-prime products are highly price sensitive in 2024 with APRs commonly >100% and small fee differences driving switching. Online multi-application behavior and marketplaces erode pricing power; approval speed under 60 seconds and same-day funding provide willingness to pay. SMBs leverage ISOs; 99.9% of US firms are SMBs and referral fees of 1–5% compress margins.

| Metric | 2024 |

|---|---|

| Typical APR (non-prime) | >100% |

| Approval time | <60s |

| SMB share of US firms | 99.9% |

| Referral fees | 1–5% |

Same Document Delivered

Enova Porter's Five Forces Analysis

This preview shows the exact Enova Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is the complete, professionally formatted file covering threat of new entrants, bargaining power of buyers and suppliers, threat of substitutes, and competitive rivalry. You’ll get instant access to this identical downloadable file.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Enova faces intense buyer pressure, moderate supplier leverage, significant threat from fintech substitutes, and regulatory and entry barriers that shape its competitive landscape. This brief snapshot highlights strategic risks and growth levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Enova’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Funding sources concentration

Enova funds originations via credit facilities, securitizations and institutional investors; a concentrated set of warehouse lenders or ABS buyers can press pricing, covenants and advance rates. Tight 2024 capital markets raised funding costs and constrained growth, while Enova's diversified, committed facilities and roughly $1.0 billion of liquidity in 2024 reduced supplier leverage.

Data and credit bureau dependence

Enova depends on the three major credit bureaus—Experian, Equifax, TransUnion—plus alternative data and ID/fraud providers as critical inputs to underwriting, giving these suppliers strong bargaining power due to limited substitutability for high-quality datasets.

Volume-based contracting and multi-vendor sourcing are standard mitigants that can lower pricing pressure and supply risk.

Ongoing CFPB rulemaking and regulatory scrutiny of data use in 2023–24 can amplify dependence by restricting sources or increasing compliance costs for data suppliers and buyers alike.

Cloud and infrastructure platforms

Cloud providers (AWS ~32%, Azure ~23%, Google Cloud ~11% market share in 2024) plus core SaaS and decisioning tools underpin Enova’s real-time lending; high switching costs, integration complexity and strict uptime SLAs grant these suppliers strong bargaining leverage. Reserved instances can cut compute costs up to ~70% and multi-cloud architectures (92% of enterprises use multi-cloud in 2024) can temper dependency. Outages or price hikes directly hit unit economics and margins.

Payments and disbursement networks

Payments and disbursement networks (ACH rails, card networks, instant payout providers) are gatekeepers of customer experience; ACH fees typically run $0.20–$1.50 per transfer while card interchange and assessments average about 1–3% per transaction, and FedNow expanded to 100+ participants by 2024, increasing real-time options. Network fees, chargeback rules and dispute timelines directly drive cost and settlement speed; limited instant-disbursement alternatives strengthen supplier leverage, though multi-processor redundancy can lower pricing pressure and operational risk.

- ACH rails: low per-transfer fees, high latency

- Card networks: 1–3% average cost, strict chargeback rules

- Instant payouts: growing (FedNow 100+ banks by 2024), limited vendors

- Redundancy: multiple processors reduce single-vendor power

Specialized analytics talent

Specialized analytics talent—machine learning engineers (median US base pay ~USD 150,000 in 2024), risk modelers (~USD 130,000) and compliance experts (~USD 120,000)—are scarce and costly, giving candidates leverage on compensation and mobility; strong in-house tooling and culture cut turnover and dependency, while outsourcing analytics raises supplier power and IP risk.

- High pay & scarcity

- Candidate leverage

- Retention via tooling/culture

- Outsourcing = higher supplier/IP risk

Supplier power risks from concentrated funders, 3 bureaus, cloud fees, and scarce ML talent

Enova faces supplier leverage from concentrated funding partners despite ~$1.0B liquidity in 2024. Dependence on three credit bureaus and specialized data raises switching costs. Cloud and payments providers (AWS 32%/Azure 23%/GCP 11% in 2024; ACH $0.20–$1.50; card 1–3%) and scarce analytics talent (ML median ~$150k) strengthen supplier power.

| Supplier | 2024 metric |

|---|---|

| Liquidity | $1.0B |

| Cloud share | AWS32%/Azure23%/GCP11% |

| Credit bureaus | 3 |

| ACH fee | $0.20–$1.50 |

| ML pay | $150k |

What is included in the product

Tailored Porter's Five Forces for Enova that uncovers competitive intensity, buyer/supplier power, substitution risks, and entry barriers with strategic implications.

A concise, one-sheet Porter's Five Forces toolkit for Enova that visualizes competitive pressures, lets you tweak inputs for scenario testing, and exports clean charts for decks—eliminating manual synthesis and speeding board-level decisions.

Customers Bargaining Power

Price sensitivity of non-prime borrowers

Customers of non-prime products are highly price sensitive in 2024, as APRs commonly exceed 100% for short-term loans and small dollar differences in APR/fees drive switching in commoditized offers. Clear disclosures and regulatory limits such as 36% caps in some jurisdictions heighten rate comparison. Fast approval and high instant-decision rates (often under 60 seconds) can blunt some price pressure by delivering value through speed and certainty.

Low switching costs and multi-homing

By 2024 online borrowers commonly apply to multiple lenders simultaneously, with lead marketplaces and broker funnels enabling rapid side-by-side comparisons that erode pricing power. This shifts lender competition toward approval speed and UX differentiation rather than rate alone. Loyalty programs and repeat-customer pricing are increasingly deployed to raise switching frictions and retain higher-value borrowers.

SMB bargaining via brokers

Small businesses commonly source credit through ISOs and online marketplaces, with SMBs comprising 99.9% of US firms per SBA; these intermediaries aggregate dozens of lender options, increasing buyer leverage on rates and covenants. Referral fees, typically 1–5% of loan proceeds, compress lender margins and raise effective borrowing costs. Growth of direct-to-SMB channels and fintech origination lowered intermediary share in 2024, reducing broker pricing power.

Regulatory and reputational leverage

Preference for speed and convenience

Customers value instant decisions and fast funding as much as price; Enova’s 2024 investor materials emphasize approvals in minutes and same-day funding capability, supporting willingness to pay for speed.

Analytics-driven approvals raise conversion and yield, but competitors matching speed in 2024 reintroduce price pressure, keeping buyer power moderate.

- Enova 2024: approvals in minutes; same-day funding

- Speed drives willingness to pay

- Rivals matching speed => price pressure

- UX leadership sustains moderate buyer power

Price-sensitive non-prime market: over 100% APR, sub-60s approval

Customers of non-prime products are highly price sensitive in 2024 with APRs commonly >100% and small fee differences driving switching. Online multi-application behavior and marketplaces erode pricing power; approval speed under 60 seconds and same-day funding provide willingness to pay. SMBs leverage ISOs; 99.9% of US firms are SMBs and referral fees of 1–5% compress margins.

| Metric | 2024 |

|---|---|

| Typical APR (non-prime) | >100% |

| Approval time | <60s |

| SMB share of US firms | 99.9% |

| Referral fees | 1–5% |

Same Document Delivered

Enova Porter's Five Forces Analysis

This preview shows the exact Enova Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is the complete, professionally formatted file covering threat of new entrants, bargaining power of buyers and suppliers, threat of substitutes, and competitive rivalry. You’ll get instant access to this identical downloadable file.