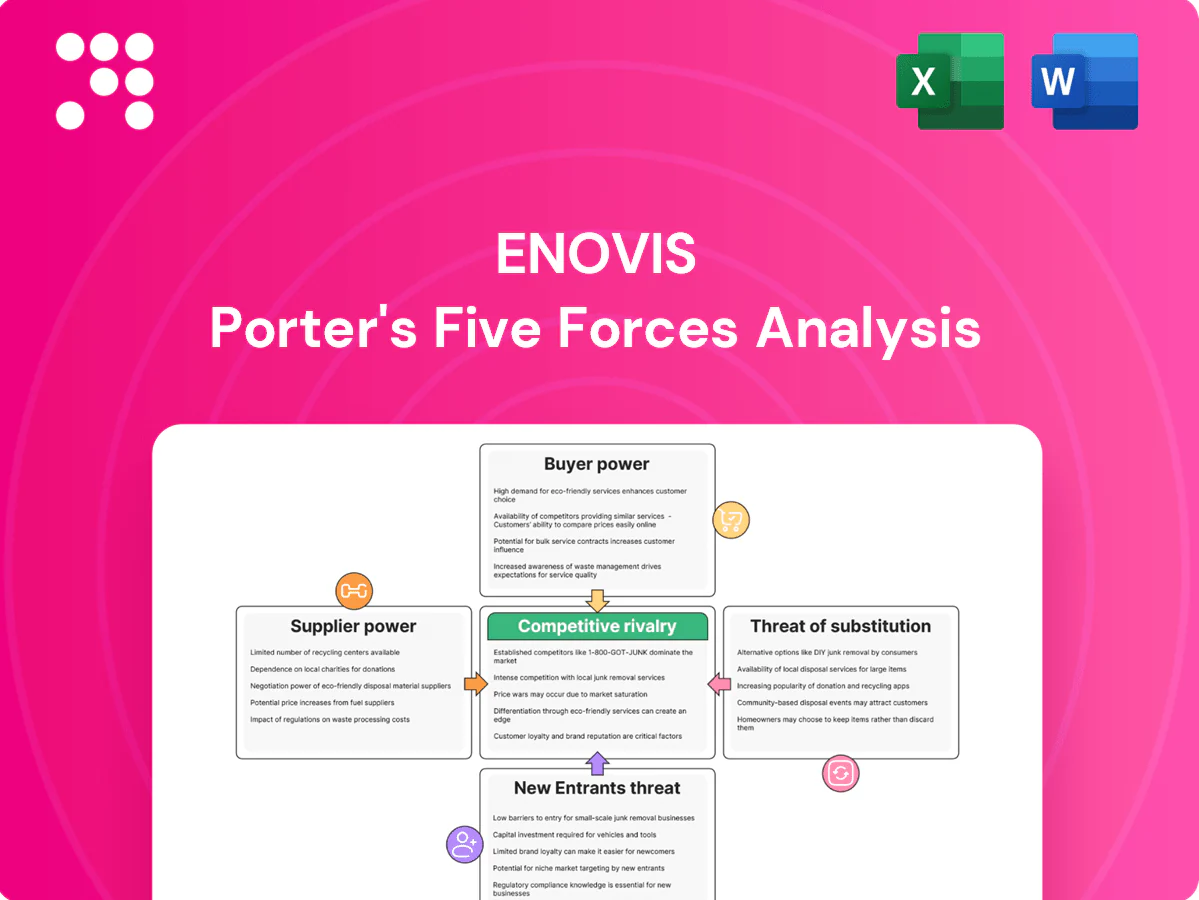

Enovis Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Enovis faces moderate supplier power, evolving buyer expectations, and competitive intensity from established orthopedic device makers and disruptive entrants; regulatory and reimbursement pressures further shape margins. Our snapshot highlights key pressure points and strategic levers but omits detailed ratings and visuals. Unlock the full Porter's Five Forces Analysis for force-by-force scoring, actionable implications, and consultant-grade charts to inform investment or strategy decisions.

Suppliers Bargaining Power

Specialty materials and components

Orthopedic implants and braces depend on titanium, PEEK, advanced polymers, textiles and precision electronics, with the global orthopedics market roughly USD 53 billion in 2024, amplifying supplier leverage. A limited pool of certified suppliers raises prices and enforces MOQs, while qualification and validation create switching frictions that can take months. Dual-sourcing and multi-year contracts historically reduce supplier power and cap input-cost volatility.

Regulated contract manufacturing

ISO 13485 and FDA QSR-compliant CMOs and sterilization providers are concentrated, making qualified partners scarce and raising supplier leverage. Regulatory audits, validation protocols, and change-control requirements lock in processes and increase switching costs. Capacity constraints in qualified sterilization and cleanroom capacity can lengthen lead times and raise unit costs. A diversified global supplier network mitigates disruption and supply-risk concentration.

Proprietary tech and tooling

Custom molds, jigs and embedded firmware create path dependency for Enovis, raising switching friction and operational risk; as of 2024 industry tooling amortization typically spans 3–5 years with upfront mold/jig costs often in the $50k–$200k range, locking in specifications. Suppliers with proprietary know‑how can therefore extract better commercial terms and margin premia, while targeted standardization programs and multi-sourcing can reclaim buyer leverage.

Logistics and sterilization capacity

Sterilization (EO, gamma) and specialized logistics are persistent bottlenecks, with industry sterilization utilization reported above 85% in 2024, allowing suppliers to charge premiums and control scheduling; disruptions directly delay product launches and shipments, raising time-to-revenue risk; multi-vendor sterilization strategies reduce this exposure.

- Scarcity → premiums

- Utilization >85% (2024)

- Disruptions delay launches

- Multi-vendor mitigates risk

IP and raw material volatility

Patents on surface treatments and textiles concentrate supplier power for Enovis, with several proprietary coatings limiting switching; Enovis cited IP-driven supplier constraints in 2024 supplier disclosures. Metal and polymer price swings fed through to COGS—industry reports showed resin and specialty metal input volatility causing roughly ±4% COGS variance in 2024, partially offset by hedging and VAVE programs.

- IP concentration: proprietary coatings raise switching costs

- Input volatility: ~±4% COGS swing in 2024

- Mitigants: hedging + VAVE reduced exposure

- Design-for-substitution: lowers dependency over time

Supplier power: sterilizer >85%, COGS ±4%, hedging

Suppliers hold elevated leverage due to scarce certified inputs (titanium, PEEK), concentrated sterilization capacity (>85% utilization in 2024) and IP on coatings, driving switching costs and ±4% COGS volatility in 2024; multi-sourcing, hedging and VAVE reduce risk.

| Metric | 2024 |

|---|---|

| Sterilization utilization | >85% |

| COGS volatility | ±4% |

| Tooling cost | $50k–$200k |

What is included in the product

Tailored Porter’s Five Forces analysis for Enovis that uncovers key drivers of competitive rivalry, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary and a fully editable Word-ready format for investor reports, business plans, or internal strategy decks.

A clear one-sheet Porter's Five Forces for Enovis—instantly reveals competitive pressures and strategic risks so teams make faster, confident decisions without digging through dense reports.

Customers Bargaining Power

GPOs and centralized procurement

Hospitals (~6,000 US acute care) and ~5,800 ASCs predominantly buy through GPOs/IDNs that demand 10–20%+ discounts; bundled contracts and compliance tiers amplify price pressure and force deeper rebates. Enovis must offer value-based arrangements and outcomes-linked pricing to retain access; loss of a major GPO can cut volumes by low-to-mid double-digit percentages, materially impacting revenue.

Surgeon preference and outcomes data

Surgeon preference drives implant selection in roughly 70% of orthopedic cases, often overriding procurement committees; strong clinical evidence and easier intraoperative workflows reduce hospital negotiators' leverage. Enovis' emphasis on outcomes registries and user-friendly systems raises switching costs, while extensive surgeon training and field service increase stickiness. Where products lack clear differentiation, price sensitivity and tender competition intensify.

Payers and reimbursement dynamics

Payers' coverage policies dictate mix and volumes across Enovis' bracing and surgical lines, with prior authorization and price caps increasing buyer bargaining power; prior auths for musculoskeletal devices rose about 20% in 2023–24, tightening access. Demonstrating cost-effectiveness through real-world evidence helps defend pricing and margins. The shift of procedures to outpatient sites (growing share annually) intensifies payer cost scrutiny and downward price pressure.

Product comparability and switching

- Substitutability: high

- Buyer leverage: elevated

- Switching frictions: custom systems/software

- Lock-in: post-sale service contracts

Global market access variability

Buyer power varies significantly by region as MDR alignment, tendering regimes and public payers shape procurement; large tenders often extract double-digit discounts while securing high volumes. Emerging markets commonly trade price for market access and on-site training. Local registration timelines and distributor strength materially affect negotiation leverage.

- Regional MDR/tender impact

- Large tenders: double-digit discounts

- Emerging markets: price for access/training

- Distributor/registration leverage

GPO squeeze hits hospitals/ASCs; surgeon sway 70%, prior-auths up

Hospitals (~6,000) and ~5,800 ASCs buy via GPOs/IDNs demanding 10–20%+ discounts; losing a major GPO can cut volumes by low-to-mid double digits. Surgeon preference governs ~70% of implants, raising switching costs via registries and training. Prior auths rose ~20% (2023–24); 58% view implants as substitutable, driving mid-single-digit ASP declines.

| Metric | 2024 |

|---|---|

| Hospitals/ASCs | ~6,000 / ~5,800 |

| Surgeon influence | ~70% |

| Substitutability | 58% |

| Prior auth rise | ~20% |

| ASP trend | mid-single-digit ↓ |

Full Version Awaits

Enovis Porter's Five Forces Analysis

This preview shows the exact Enovis Porter’s Five Forces Analysis you’ll receive after purchase—no placeholders, no mockups. The file is fully formatted and ready for immediate download and use. It contains the complete, professionally written assessment of competitive rivalry, supplier and buyer power, and threat dynamics.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Enovis faces moderate supplier power, evolving buyer expectations, and competitive intensity from established orthopedic device makers and disruptive entrants; regulatory and reimbursement pressures further shape margins. Our snapshot highlights key pressure points and strategic levers but omits detailed ratings and visuals. Unlock the full Porter's Five Forces Analysis for force-by-force scoring, actionable implications, and consultant-grade charts to inform investment or strategy decisions.

Suppliers Bargaining Power

Specialty materials and components

Orthopedic implants and braces depend on titanium, PEEK, advanced polymers, textiles and precision electronics, with the global orthopedics market roughly USD 53 billion in 2024, amplifying supplier leverage. A limited pool of certified suppliers raises prices and enforces MOQs, while qualification and validation create switching frictions that can take months. Dual-sourcing and multi-year contracts historically reduce supplier power and cap input-cost volatility.

Regulated contract manufacturing

ISO 13485 and FDA QSR-compliant CMOs and sterilization providers are concentrated, making qualified partners scarce and raising supplier leverage. Regulatory audits, validation protocols, and change-control requirements lock in processes and increase switching costs. Capacity constraints in qualified sterilization and cleanroom capacity can lengthen lead times and raise unit costs. A diversified global supplier network mitigates disruption and supply-risk concentration.

Proprietary tech and tooling

Custom molds, jigs and embedded firmware create path dependency for Enovis, raising switching friction and operational risk; as of 2024 industry tooling amortization typically spans 3–5 years with upfront mold/jig costs often in the $50k–$200k range, locking in specifications. Suppliers with proprietary know‑how can therefore extract better commercial terms and margin premia, while targeted standardization programs and multi-sourcing can reclaim buyer leverage.

Logistics and sterilization capacity

Sterilization (EO, gamma) and specialized logistics are persistent bottlenecks, with industry sterilization utilization reported above 85% in 2024, allowing suppliers to charge premiums and control scheduling; disruptions directly delay product launches and shipments, raising time-to-revenue risk; multi-vendor sterilization strategies reduce this exposure.

- Scarcity → premiums

- Utilization >85% (2024)

- Disruptions delay launches

- Multi-vendor mitigates risk

IP and raw material volatility

Patents on surface treatments and textiles concentrate supplier power for Enovis, with several proprietary coatings limiting switching; Enovis cited IP-driven supplier constraints in 2024 supplier disclosures. Metal and polymer price swings fed through to COGS—industry reports showed resin and specialty metal input volatility causing roughly ±4% COGS variance in 2024, partially offset by hedging and VAVE programs.

- IP concentration: proprietary coatings raise switching costs

- Input volatility: ~±4% COGS swing in 2024

- Mitigants: hedging + VAVE reduced exposure

- Design-for-substitution: lowers dependency over time

Supplier power: sterilizer >85%, COGS ±4%, hedging

Suppliers hold elevated leverage due to scarce certified inputs (titanium, PEEK), concentrated sterilization capacity (>85% utilization in 2024) and IP on coatings, driving switching costs and ±4% COGS volatility in 2024; multi-sourcing, hedging and VAVE reduce risk.

| Metric | 2024 |

|---|---|

| Sterilization utilization | >85% |

| COGS volatility | ±4% |

| Tooling cost | $50k–$200k |

What is included in the product

Tailored Porter’s Five Forces analysis for Enovis that uncovers key drivers of competitive rivalry, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary and a fully editable Word-ready format for investor reports, business plans, or internal strategy decks.

A clear one-sheet Porter's Five Forces for Enovis—instantly reveals competitive pressures and strategic risks so teams make faster, confident decisions without digging through dense reports.

Customers Bargaining Power

GPOs and centralized procurement

Hospitals (~6,000 US acute care) and ~5,800 ASCs predominantly buy through GPOs/IDNs that demand 10–20%+ discounts; bundled contracts and compliance tiers amplify price pressure and force deeper rebates. Enovis must offer value-based arrangements and outcomes-linked pricing to retain access; loss of a major GPO can cut volumes by low-to-mid double-digit percentages, materially impacting revenue.

Surgeon preference and outcomes data

Surgeon preference drives implant selection in roughly 70% of orthopedic cases, often overriding procurement committees; strong clinical evidence and easier intraoperative workflows reduce hospital negotiators' leverage. Enovis' emphasis on outcomes registries and user-friendly systems raises switching costs, while extensive surgeon training and field service increase stickiness. Where products lack clear differentiation, price sensitivity and tender competition intensify.

Payers and reimbursement dynamics

Payers' coverage policies dictate mix and volumes across Enovis' bracing and surgical lines, with prior authorization and price caps increasing buyer bargaining power; prior auths for musculoskeletal devices rose about 20% in 2023–24, tightening access. Demonstrating cost-effectiveness through real-world evidence helps defend pricing and margins. The shift of procedures to outpatient sites (growing share annually) intensifies payer cost scrutiny and downward price pressure.

Product comparability and switching

- Substitutability: high

- Buyer leverage: elevated

- Switching frictions: custom systems/software

- Lock-in: post-sale service contracts

Global market access variability

Buyer power varies significantly by region as MDR alignment, tendering regimes and public payers shape procurement; large tenders often extract double-digit discounts while securing high volumes. Emerging markets commonly trade price for market access and on-site training. Local registration timelines and distributor strength materially affect negotiation leverage.

- Regional MDR/tender impact

- Large tenders: double-digit discounts

- Emerging markets: price for access/training

- Distributor/registration leverage

GPO squeeze hits hospitals/ASCs; surgeon sway 70%, prior-auths up

Hospitals (~6,000) and ~5,800 ASCs buy via GPOs/IDNs demanding 10–20%+ discounts; losing a major GPO can cut volumes by low-to-mid double digits. Surgeon preference governs ~70% of implants, raising switching costs via registries and training. Prior auths rose ~20% (2023–24); 58% view implants as substitutable, driving mid-single-digit ASP declines.

| Metric | 2024 |

|---|---|

| Hospitals/ASCs | ~6,000 / ~5,800 |

| Surgeon influence | ~70% |

| Substitutability | 58% |

| Prior auth rise | ~20% |

| ASP trend | mid-single-digit ↓ |

Full Version Awaits

Enovis Porter's Five Forces Analysis

This preview shows the exact Enovis Porter’s Five Forces Analysis you’ll receive after purchase—no placeholders, no mockups. The file is fully formatted and ready for immediate download and use. It contains the complete, professionally written assessment of competitive rivalry, supplier and buyer power, and threat dynamics.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Enovis faces moderate supplier power, evolving buyer expectations, and competitive intensity from established orthopedic device makers and disruptive entrants; regulatory and reimbursement pressures further shape margins. Our snapshot highlights key pressure points and strategic levers but omits detailed ratings and visuals. Unlock the full Porter's Five Forces Analysis for force-by-force scoring, actionable implications, and consultant-grade charts to inform investment or strategy decisions.

Suppliers Bargaining Power

Specialty materials and components

Orthopedic implants and braces depend on titanium, PEEK, advanced polymers, textiles and precision electronics, with the global orthopedics market roughly USD 53 billion in 2024, amplifying supplier leverage. A limited pool of certified suppliers raises prices and enforces MOQs, while qualification and validation create switching frictions that can take months. Dual-sourcing and multi-year contracts historically reduce supplier power and cap input-cost volatility.

Regulated contract manufacturing

ISO 13485 and FDA QSR-compliant CMOs and sterilization providers are concentrated, making qualified partners scarce and raising supplier leverage. Regulatory audits, validation protocols, and change-control requirements lock in processes and increase switching costs. Capacity constraints in qualified sterilization and cleanroom capacity can lengthen lead times and raise unit costs. A diversified global supplier network mitigates disruption and supply-risk concentration.

Proprietary tech and tooling

Custom molds, jigs and embedded firmware create path dependency for Enovis, raising switching friction and operational risk; as of 2024 industry tooling amortization typically spans 3–5 years with upfront mold/jig costs often in the $50k–$200k range, locking in specifications. Suppliers with proprietary know‑how can therefore extract better commercial terms and margin premia, while targeted standardization programs and multi-sourcing can reclaim buyer leverage.

Logistics and sterilization capacity

Sterilization (EO, gamma) and specialized logistics are persistent bottlenecks, with industry sterilization utilization reported above 85% in 2024, allowing suppliers to charge premiums and control scheduling; disruptions directly delay product launches and shipments, raising time-to-revenue risk; multi-vendor sterilization strategies reduce this exposure.

- Scarcity → premiums

- Utilization >85% (2024)

- Disruptions delay launches

- Multi-vendor mitigates risk

IP and raw material volatility

Patents on surface treatments and textiles concentrate supplier power for Enovis, with several proprietary coatings limiting switching; Enovis cited IP-driven supplier constraints in 2024 supplier disclosures. Metal and polymer price swings fed through to COGS—industry reports showed resin and specialty metal input volatility causing roughly ±4% COGS variance in 2024, partially offset by hedging and VAVE programs.

- IP concentration: proprietary coatings raise switching costs

- Input volatility: ~±4% COGS swing in 2024

- Mitigants: hedging + VAVE reduced exposure

- Design-for-substitution: lowers dependency over time

Supplier power: sterilizer >85%, COGS ±4%, hedging

Suppliers hold elevated leverage due to scarce certified inputs (titanium, PEEK), concentrated sterilization capacity (>85% utilization in 2024) and IP on coatings, driving switching costs and ±4% COGS volatility in 2024; multi-sourcing, hedging and VAVE reduce risk.

| Metric | 2024 |

|---|---|

| Sterilization utilization | >85% |

| COGS volatility | ±4% |

| Tooling cost | $50k–$200k |

What is included in the product

Tailored Porter’s Five Forces analysis for Enovis that uncovers key drivers of competitive rivalry, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary and a fully editable Word-ready format for investor reports, business plans, or internal strategy decks.

A clear one-sheet Porter's Five Forces for Enovis—instantly reveals competitive pressures and strategic risks so teams make faster, confident decisions without digging through dense reports.

Customers Bargaining Power

GPOs and centralized procurement

Hospitals (~6,000 US acute care) and ~5,800 ASCs predominantly buy through GPOs/IDNs that demand 10–20%+ discounts; bundled contracts and compliance tiers amplify price pressure and force deeper rebates. Enovis must offer value-based arrangements and outcomes-linked pricing to retain access; loss of a major GPO can cut volumes by low-to-mid double-digit percentages, materially impacting revenue.

Surgeon preference and outcomes data

Surgeon preference drives implant selection in roughly 70% of orthopedic cases, often overriding procurement committees; strong clinical evidence and easier intraoperative workflows reduce hospital negotiators' leverage. Enovis' emphasis on outcomes registries and user-friendly systems raises switching costs, while extensive surgeon training and field service increase stickiness. Where products lack clear differentiation, price sensitivity and tender competition intensify.

Payers and reimbursement dynamics

Payers' coverage policies dictate mix and volumes across Enovis' bracing and surgical lines, with prior authorization and price caps increasing buyer bargaining power; prior auths for musculoskeletal devices rose about 20% in 2023–24, tightening access. Demonstrating cost-effectiveness through real-world evidence helps defend pricing and margins. The shift of procedures to outpatient sites (growing share annually) intensifies payer cost scrutiny and downward price pressure.

Product comparability and switching

- Substitutability: high

- Buyer leverage: elevated

- Switching frictions: custom systems/software

- Lock-in: post-sale service contracts

Global market access variability

Buyer power varies significantly by region as MDR alignment, tendering regimes and public payers shape procurement; large tenders often extract double-digit discounts while securing high volumes. Emerging markets commonly trade price for market access and on-site training. Local registration timelines and distributor strength materially affect negotiation leverage.

- Regional MDR/tender impact

- Large tenders: double-digit discounts

- Emerging markets: price for access/training

- Distributor/registration leverage

GPO squeeze hits hospitals/ASCs; surgeon sway 70%, prior-auths up

Hospitals (~6,000) and ~5,800 ASCs buy via GPOs/IDNs demanding 10–20%+ discounts; losing a major GPO can cut volumes by low-to-mid double digits. Surgeon preference governs ~70% of implants, raising switching costs via registries and training. Prior auths rose ~20% (2023–24); 58% view implants as substitutable, driving mid-single-digit ASP declines.

| Metric | 2024 |

|---|---|

| Hospitals/ASCs | ~6,000 / ~5,800 |

| Surgeon influence | ~70% |

| Substitutability | 58% |

| Prior auth rise | ~20% |

| ASP trend | mid-single-digit ↓ |

Full Version Awaits

Enovis Porter's Five Forces Analysis

This preview shows the exact Enovis Porter’s Five Forces Analysis you’ll receive after purchase—no placeholders, no mockups. The file is fully formatted and ready for immediate download and use. It contains the complete, professionally written assessment of competitive rivalry, supplier and buyer power, and threat dynamics.