Entain Porter's Five Forces Analysis

From Overview to Strategy Blueprint

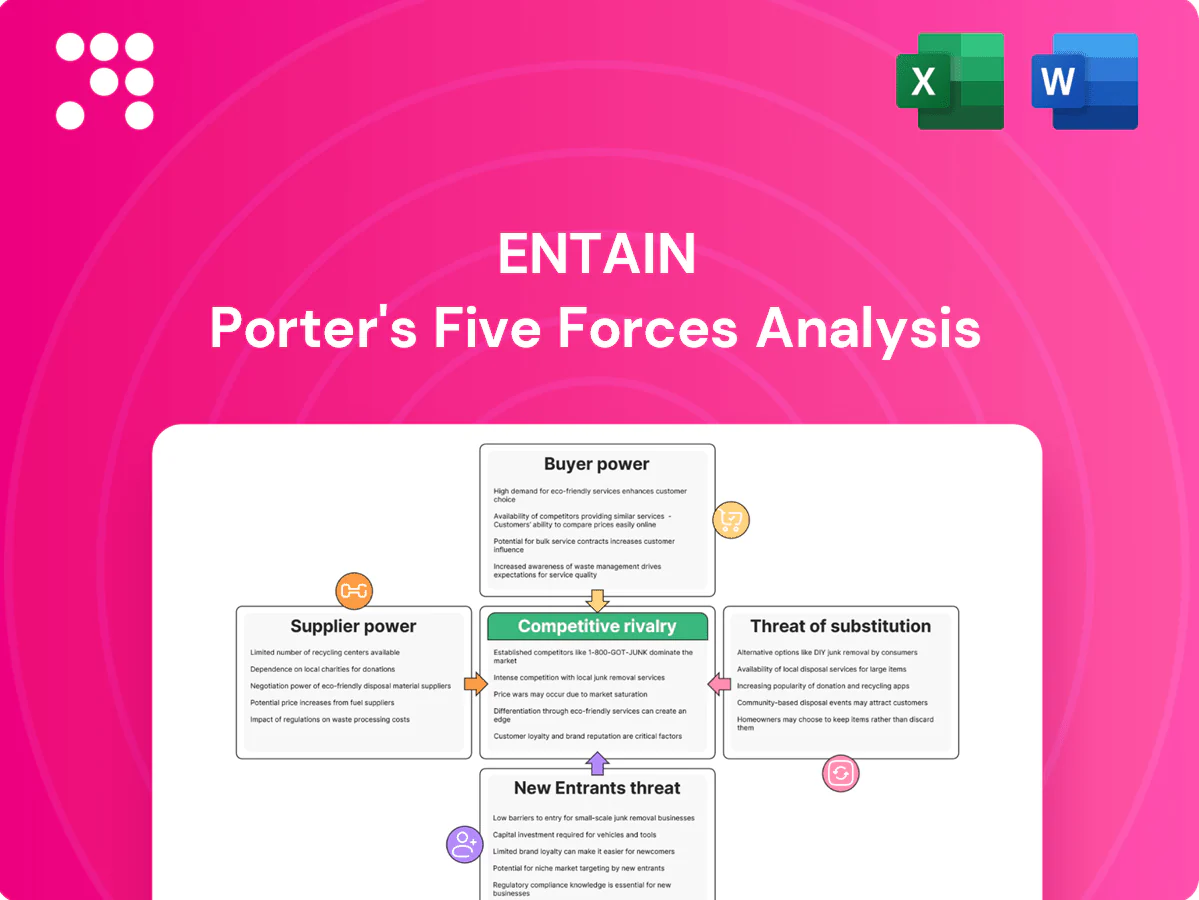

Entain faces intense competitive rivalry, rising regulatory scrutiny, and concentrated supplier and partner leverage that shape margins and growth prospects; buyer power and digital substitutes further pressure pricing and retention strategies. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Entain’s competitive dynamics and strategic opportunities in detail.

Suppliers Bargaining Power

Concentrated sports data rights

Live odds and official data remain concentrated among three main suppliers in 2024, boosting their leverage over pricing and access terms. Exclusive league partnerships further limit alternative sourcing, locking smaller operators out of key markets. Entain offsets this by leveraging scale and multi-sourcing where feasible. Persistent switching costs and 6–9 month integration timelines sustain supplier negotiating power.

Game content studios and aggregators

Popular slots, live casino and poker liquidity come from leading studios and networks—top live provider Evolution alone holds roughly 30% share of live supply—giving studios strong leverage for hit titles and exclusives that can command 20–40% premium fees. Entain’s ~26 million active customers in 2024 provide distribution scale enabling volume-based discounts, but platform differentiation still often requires costly exclusive content deals.

Payment processors and fraud tools

Compliance-heavy markets demand reliable payments, KYC, AML and risk tools, with PSD2 strong customer authentication enforced across the EEA as of 2024. A limited pool of fully compliant providers per jurisdiction raises supplier dependency. Entain’s scale gives it better pricing and duplicate rails for resilience, but card scheme rules and chargeback policies cap bargaining power. Local processor alternatives improve resilience yet add operational complexity.

Cloud and platform infrastructure

Reliance on hyperscale cloud and CDNs concentrates supplier power, with AWS, Microsoft and Google accounting for about two-thirds of global IaaS/PaaS capacity in 2024 (Synergy Research). Migration costs and 99.9–99.99% uptime SLAs create strong lock-in. Entain’s in‑house tech lowers vendor exposure but still demands scalable infra; reserved capacity and multi‑cloud use temper pricing pressure.

- Hyperscaler share ~66% (2024)

- Common SLAs 99.9–99.99%

- In‑house tech reduces but doesn’t remove reliance

- Reserved capacity + multi‑cloud = pricing leverage

Affiliate and media partners

Affiliate and media partners drive high-intent traffic that materially lowers acquisition costs; in 2024 affiliates remained a key source of new depositing customers for Entain, allowing lower CPA vs generic channels. Top affiliates in competitive markets can demand higher rev-share or CPAs, so Entain offsets by scaling direct brand marketing and CRM to dilute dependence. Regulatory limits on inducements in 2024 increased leverage for compliant premium publishers.

- High-intent traffic: lowers CPA

- Top affiliates: can command higher rev-share/CPA

- Entain: offsets via direct marketing & CRM

- 2024 rules on inducements: shift power to compliant publishers

High supplier power 2024: live-provider ~30% share, hyperscalers ~66% IaaS, 6–9m integrations

Supplier power is high in 2024: live-provider Evolution ~30% share, exclusive league data deals restrict alternatives, and hyperscalers hold ~66% IaaS capacity, creating lock‑in. Entain’s ~26M active users and multi‑sourcing/reserved capacity reduce but do not eliminate supplier leverage; integration timelines (6–9 months) and 20–40% premium fees sustain negotiations.

| Metric | 2024 |

|---|---|

| Evolution live share | ~30% |

| Entain active users | ~26M |

| Hyperscaler IaaS | ~66% |

| Integration time | 6–9m |

| Premium fees | 20–40% |

What is included in the product

Concise Porter's Five Forces analysis of Entain that reveals competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and regulatory/disruptive risks—providing strategic insights to assess pricing power, market positioning, and barriers protecting incumbency.

Compact Entain Porter's Five Forces one-sheet—customize pressure levels, swap in your data, and export a clean radar chart ready for decks or executive decision-making.

Customers Bargaining Power

Low switching costs for bettors

Low switching costs let bettors hold multiple wallets and jump for better odds, UX or promos; app stores and web access make multi-homing straightforward. Entain reported about 17 million active customers in 2024 and counters with personalization, loyalty tiers and omnichannel play to raise retention. Buyer power spikes when rivals run aggressive bonus campaigns, compressing margins and forcing higher marketing spend.

Price sensitivity to odds and margins

Sharp bettors and price-comparison tools sharply increase sensitivity to takeout and odds boosts, with minor pricing differentials able to shift volumes in core markets; Entain, which reported group revenue of about £3.4bn in 2023, counters this with real-time risk management and dynamic pricing algorithms, while hedging strategies and market depth preserve margins without ceding share.

Promotions and bonus expectations

Frequent free bets and bonuses have trained customers to expect inducements, raising industry-wide acquisition and retention costs; Entain reported group revenue of about £3.8bn for FY 2023, underscoring scale-driven spend pressures. Entain uses segmented offers and stricter RG controls to optimise LTV/CAC and limit wasteful promos. Regulatory caps, such as tighter UK measures considered in 2024, can blunt promo-driven buyer power but shift competition to product and experience.

VIP and high-value cohorts

VIPs and high-value cohorts drive outsized revenue — Entain reported group revenue of about £3.5bn in FY 2024 while the top 5% of customers account for roughly 45% of online net gaming revenue, amplifying their leverage on service and pricing. Stricter 2024 RG and affordability checks have reduced routine concessions, shifting focus to sustainable play and cross-sell to diversify lifetime value. Tailored VIP experiences lower churn while ensuring compliance.

Experience and trust expectations

Customers demand fast withdrawals, provable fair play and strong RG tools; failures trigger rapid switching and reputational hits in 2024, especially among Entain’s millions of users across 20+ regulated jurisdictions. Entain’s regulated-market focus and continued tech investment bolster trust, while independent certifications and transparent policies reduce buyer skepticism.

- fast withdrawals: priority

- fair play: verifiable

- RG tools: mandatory

- trust mitigants: regulation + certifications

Low switching costs; promo-prone bettors; top 5% drive 45%

Low switching costs and multi-homing keep customer bargaining power high; Entain had ~17m active customers in 2024 and faces promo-sensitive bettors. Top 5% of customers drive ~45% of online net gaming revenue, amplifying their leverage; Entain FY24 revenue ≈£3.5bn. Stricter 2024 RG rules and tailored VIP offers reduce price pressure and improve retention.

| Metric | 2024 |

|---|---|

| Active customers | ~17m |

| FY revenue | ≈£3.5bn |

| Top 5% revenue share | ≈45% |

What You See Is What You Get

Entain Porter's Five Forces Analysis

This Entain Porter’s Five Forces Analysis is the exact, fully formatted document you’re previewing here—no placeholders or samples. It covers competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. After purchase you’ll receive this same file instantly, ready to download and use.

From Overview to Strategy Blueprint

Entain faces intense competitive rivalry, rising regulatory scrutiny, and concentrated supplier and partner leverage that shape margins and growth prospects; buyer power and digital substitutes further pressure pricing and retention strategies. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Entain’s competitive dynamics and strategic opportunities in detail.

Suppliers Bargaining Power

Concentrated sports data rights

Live odds and official data remain concentrated among three main suppliers in 2024, boosting their leverage over pricing and access terms. Exclusive league partnerships further limit alternative sourcing, locking smaller operators out of key markets. Entain offsets this by leveraging scale and multi-sourcing where feasible. Persistent switching costs and 6–9 month integration timelines sustain supplier negotiating power.

Game content studios and aggregators

Popular slots, live casino and poker liquidity come from leading studios and networks—top live provider Evolution alone holds roughly 30% share of live supply—giving studios strong leverage for hit titles and exclusives that can command 20–40% premium fees. Entain’s ~26 million active customers in 2024 provide distribution scale enabling volume-based discounts, but platform differentiation still often requires costly exclusive content deals.

Payment processors and fraud tools

Compliance-heavy markets demand reliable payments, KYC, AML and risk tools, with PSD2 strong customer authentication enforced across the EEA as of 2024. A limited pool of fully compliant providers per jurisdiction raises supplier dependency. Entain’s scale gives it better pricing and duplicate rails for resilience, but card scheme rules and chargeback policies cap bargaining power. Local processor alternatives improve resilience yet add operational complexity.

Cloud and platform infrastructure

Reliance on hyperscale cloud and CDNs concentrates supplier power, with AWS, Microsoft and Google accounting for about two-thirds of global IaaS/PaaS capacity in 2024 (Synergy Research). Migration costs and 99.9–99.99% uptime SLAs create strong lock-in. Entain’s in‑house tech lowers vendor exposure but still demands scalable infra; reserved capacity and multi‑cloud use temper pricing pressure.

- Hyperscaler share ~66% (2024)

- Common SLAs 99.9–99.99%

- In‑house tech reduces but doesn’t remove reliance

- Reserved capacity + multi‑cloud = pricing leverage

Affiliate and media partners

Affiliate and media partners drive high-intent traffic that materially lowers acquisition costs; in 2024 affiliates remained a key source of new depositing customers for Entain, allowing lower CPA vs generic channels. Top affiliates in competitive markets can demand higher rev-share or CPAs, so Entain offsets by scaling direct brand marketing and CRM to dilute dependence. Regulatory limits on inducements in 2024 increased leverage for compliant premium publishers.

- High-intent traffic: lowers CPA

- Top affiliates: can command higher rev-share/CPA

- Entain: offsets via direct marketing & CRM

- 2024 rules on inducements: shift power to compliant publishers

High supplier power 2024: live-provider ~30% share, hyperscalers ~66% IaaS, 6–9m integrations

Supplier power is high in 2024: live-provider Evolution ~30% share, exclusive league data deals restrict alternatives, and hyperscalers hold ~66% IaaS capacity, creating lock‑in. Entain’s ~26M active users and multi‑sourcing/reserved capacity reduce but do not eliminate supplier leverage; integration timelines (6–9 months) and 20–40% premium fees sustain negotiations.

| Metric | 2024 |

|---|---|

| Evolution live share | ~30% |

| Entain active users | ~26M |

| Hyperscaler IaaS | ~66% |

| Integration time | 6–9m |

| Premium fees | 20–40% |

What is included in the product

Concise Porter's Five Forces analysis of Entain that reveals competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and regulatory/disruptive risks—providing strategic insights to assess pricing power, market positioning, and barriers protecting incumbency.

Compact Entain Porter's Five Forces one-sheet—customize pressure levels, swap in your data, and export a clean radar chart ready for decks or executive decision-making.

Customers Bargaining Power

Low switching costs for bettors

Low switching costs let bettors hold multiple wallets and jump for better odds, UX or promos; app stores and web access make multi-homing straightforward. Entain reported about 17 million active customers in 2024 and counters with personalization, loyalty tiers and omnichannel play to raise retention. Buyer power spikes when rivals run aggressive bonus campaigns, compressing margins and forcing higher marketing spend.

Price sensitivity to odds and margins

Sharp bettors and price-comparison tools sharply increase sensitivity to takeout and odds boosts, with minor pricing differentials able to shift volumes in core markets; Entain, which reported group revenue of about £3.4bn in 2023, counters this with real-time risk management and dynamic pricing algorithms, while hedging strategies and market depth preserve margins without ceding share.

Promotions and bonus expectations

Frequent free bets and bonuses have trained customers to expect inducements, raising industry-wide acquisition and retention costs; Entain reported group revenue of about £3.8bn for FY 2023, underscoring scale-driven spend pressures. Entain uses segmented offers and stricter RG controls to optimise LTV/CAC and limit wasteful promos. Regulatory caps, such as tighter UK measures considered in 2024, can blunt promo-driven buyer power but shift competition to product and experience.

VIP and high-value cohorts

VIPs and high-value cohorts drive outsized revenue — Entain reported group revenue of about £3.5bn in FY 2024 while the top 5% of customers account for roughly 45% of online net gaming revenue, amplifying their leverage on service and pricing. Stricter 2024 RG and affordability checks have reduced routine concessions, shifting focus to sustainable play and cross-sell to diversify lifetime value. Tailored VIP experiences lower churn while ensuring compliance.

Experience and trust expectations

Customers demand fast withdrawals, provable fair play and strong RG tools; failures trigger rapid switching and reputational hits in 2024, especially among Entain’s millions of users across 20+ regulated jurisdictions. Entain’s regulated-market focus and continued tech investment bolster trust, while independent certifications and transparent policies reduce buyer skepticism.

- fast withdrawals: priority

- fair play: verifiable

- RG tools: mandatory

- trust mitigants: regulation + certifications

Low switching costs; promo-prone bettors; top 5% drive 45%

Low switching costs and multi-homing keep customer bargaining power high; Entain had ~17m active customers in 2024 and faces promo-sensitive bettors. Top 5% of customers drive ~45% of online net gaming revenue, amplifying their leverage; Entain FY24 revenue ≈£3.5bn. Stricter 2024 RG rules and tailored VIP offers reduce price pressure and improve retention.

| Metric | 2024 |

|---|---|

| Active customers | ~17m |

| FY revenue | ≈£3.5bn |

| Top 5% revenue share | ≈45% |

What You See Is What You Get

Entain Porter's Five Forces Analysis

This Entain Porter’s Five Forces Analysis is the exact, fully formatted document you’re previewing here—no placeholders or samples. It covers competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. After purchase you’ll receive this same file instantly, ready to download and use.

Description

From Overview to Strategy Blueprint

Entain faces intense competitive rivalry, rising regulatory scrutiny, and concentrated supplier and partner leverage that shape margins and growth prospects; buyer power and digital substitutes further pressure pricing and retention strategies. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Entain’s competitive dynamics and strategic opportunities in detail.

Suppliers Bargaining Power

Concentrated sports data rights

Live odds and official data remain concentrated among three main suppliers in 2024, boosting their leverage over pricing and access terms. Exclusive league partnerships further limit alternative sourcing, locking smaller operators out of key markets. Entain offsets this by leveraging scale and multi-sourcing where feasible. Persistent switching costs and 6–9 month integration timelines sustain supplier negotiating power.

Game content studios and aggregators

Popular slots, live casino and poker liquidity come from leading studios and networks—top live provider Evolution alone holds roughly 30% share of live supply—giving studios strong leverage for hit titles and exclusives that can command 20–40% premium fees. Entain’s ~26 million active customers in 2024 provide distribution scale enabling volume-based discounts, but platform differentiation still often requires costly exclusive content deals.

Payment processors and fraud tools

Compliance-heavy markets demand reliable payments, KYC, AML and risk tools, with PSD2 strong customer authentication enforced across the EEA as of 2024. A limited pool of fully compliant providers per jurisdiction raises supplier dependency. Entain’s scale gives it better pricing and duplicate rails for resilience, but card scheme rules and chargeback policies cap bargaining power. Local processor alternatives improve resilience yet add operational complexity.

Cloud and platform infrastructure

Reliance on hyperscale cloud and CDNs concentrates supplier power, with AWS, Microsoft and Google accounting for about two-thirds of global IaaS/PaaS capacity in 2024 (Synergy Research). Migration costs and 99.9–99.99% uptime SLAs create strong lock-in. Entain’s in‑house tech lowers vendor exposure but still demands scalable infra; reserved capacity and multi‑cloud use temper pricing pressure.

- Hyperscaler share ~66% (2024)

- Common SLAs 99.9–99.99%

- In‑house tech reduces but doesn’t remove reliance

- Reserved capacity + multi‑cloud = pricing leverage

Affiliate and media partners

Affiliate and media partners drive high-intent traffic that materially lowers acquisition costs; in 2024 affiliates remained a key source of new depositing customers for Entain, allowing lower CPA vs generic channels. Top affiliates in competitive markets can demand higher rev-share or CPAs, so Entain offsets by scaling direct brand marketing and CRM to dilute dependence. Regulatory limits on inducements in 2024 increased leverage for compliant premium publishers.

- High-intent traffic: lowers CPA

- Top affiliates: can command higher rev-share/CPA

- Entain: offsets via direct marketing & CRM

- 2024 rules on inducements: shift power to compliant publishers

High supplier power 2024: live-provider ~30% share, hyperscalers ~66% IaaS, 6–9m integrations

Supplier power is high in 2024: live-provider Evolution ~30% share, exclusive league data deals restrict alternatives, and hyperscalers hold ~66% IaaS capacity, creating lock‑in. Entain’s ~26M active users and multi‑sourcing/reserved capacity reduce but do not eliminate supplier leverage; integration timelines (6–9 months) and 20–40% premium fees sustain negotiations.

| Metric | 2024 |

|---|---|

| Evolution live share | ~30% |

| Entain active users | ~26M |

| Hyperscaler IaaS | ~66% |

| Integration time | 6–9m |

| Premium fees | 20–40% |

What is included in the product

Concise Porter's Five Forces analysis of Entain that reveals competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and regulatory/disruptive risks—providing strategic insights to assess pricing power, market positioning, and barriers protecting incumbency.

Compact Entain Porter's Five Forces one-sheet—customize pressure levels, swap in your data, and export a clean radar chart ready for decks or executive decision-making.

Customers Bargaining Power

Low switching costs for bettors

Low switching costs let bettors hold multiple wallets and jump for better odds, UX or promos; app stores and web access make multi-homing straightforward. Entain reported about 17 million active customers in 2024 and counters with personalization, loyalty tiers and omnichannel play to raise retention. Buyer power spikes when rivals run aggressive bonus campaigns, compressing margins and forcing higher marketing spend.

Price sensitivity to odds and margins

Sharp bettors and price-comparison tools sharply increase sensitivity to takeout and odds boosts, with minor pricing differentials able to shift volumes in core markets; Entain, which reported group revenue of about £3.4bn in 2023, counters this with real-time risk management and dynamic pricing algorithms, while hedging strategies and market depth preserve margins without ceding share.

Promotions and bonus expectations

Frequent free bets and bonuses have trained customers to expect inducements, raising industry-wide acquisition and retention costs; Entain reported group revenue of about £3.8bn for FY 2023, underscoring scale-driven spend pressures. Entain uses segmented offers and stricter RG controls to optimise LTV/CAC and limit wasteful promos. Regulatory caps, such as tighter UK measures considered in 2024, can blunt promo-driven buyer power but shift competition to product and experience.

VIP and high-value cohorts

VIPs and high-value cohorts drive outsized revenue — Entain reported group revenue of about £3.5bn in FY 2024 while the top 5% of customers account for roughly 45% of online net gaming revenue, amplifying their leverage on service and pricing. Stricter 2024 RG and affordability checks have reduced routine concessions, shifting focus to sustainable play and cross-sell to diversify lifetime value. Tailored VIP experiences lower churn while ensuring compliance.

Experience and trust expectations

Customers demand fast withdrawals, provable fair play and strong RG tools; failures trigger rapid switching and reputational hits in 2024, especially among Entain’s millions of users across 20+ regulated jurisdictions. Entain’s regulated-market focus and continued tech investment bolster trust, while independent certifications and transparent policies reduce buyer skepticism.

- fast withdrawals: priority

- fair play: verifiable

- RG tools: mandatory

- trust mitigants: regulation + certifications

Low switching costs; promo-prone bettors; top 5% drive 45%

Low switching costs and multi-homing keep customer bargaining power high; Entain had ~17m active customers in 2024 and faces promo-sensitive bettors. Top 5% of customers drive ~45% of online net gaming revenue, amplifying their leverage; Entain FY24 revenue ≈£3.5bn. Stricter 2024 RG rules and tailored VIP offers reduce price pressure and improve retention.

| Metric | 2024 |

|---|---|

| Active customers | ~17m |

| FY revenue | ≈£3.5bn |

| Top 5% revenue share | ≈45% |

What You See Is What You Get

Entain Porter's Five Forces Analysis

This Entain Porter’s Five Forces Analysis is the exact, fully formatted document you’re previewing here—no placeholders or samples. It covers competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. After purchase you’ll receive this same file instantly, ready to download and use.