E.ON Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

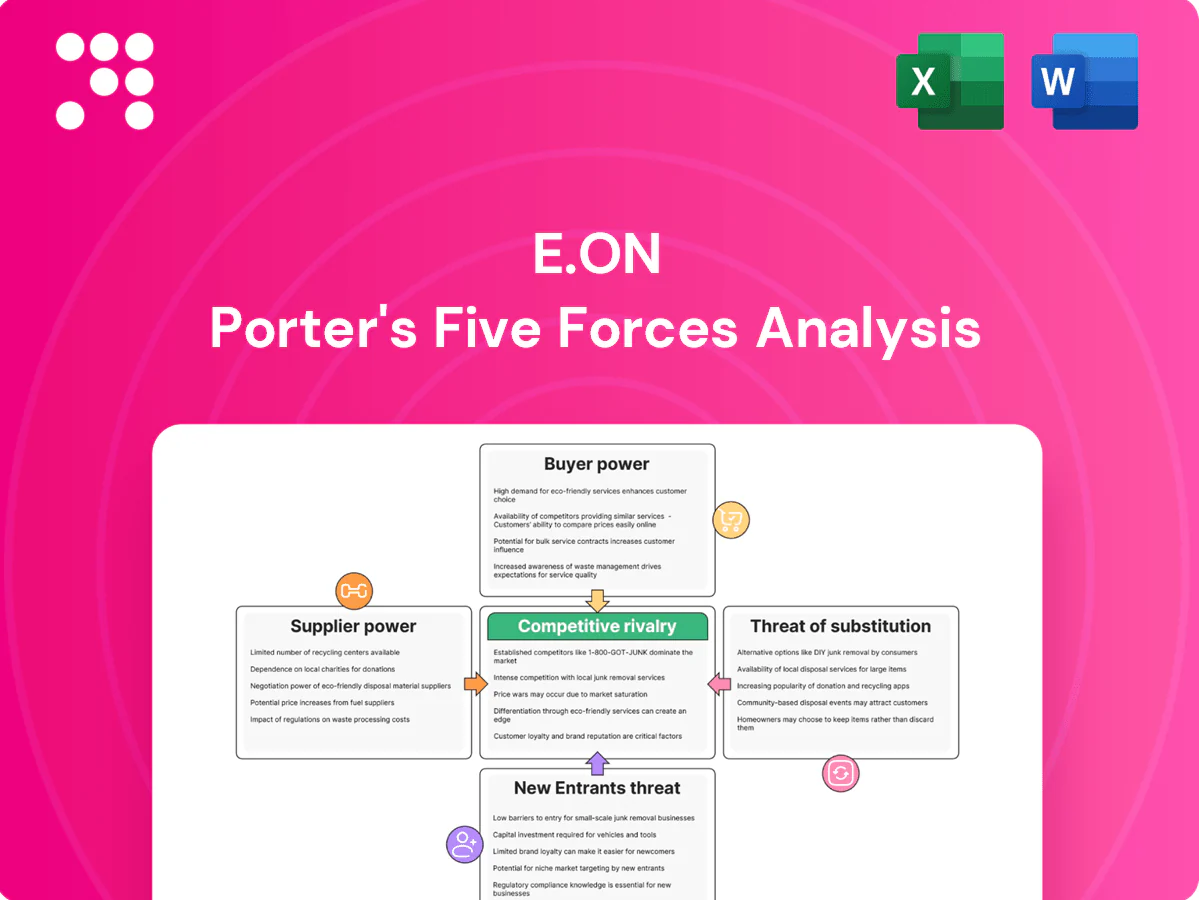

E.ON faces intense supplier negotiations, regulatory pressure, and evolving substitute risks from decentralised renewables, while buyer power and new entrants remain moderate; strategic moves will determine resilience. This snapshot highlights key tensions and opportunities. Unlock the full Porter's Five Forces Analysis for a force-by-force, data-driven strategic roadmap tailored to E.ON.

Suppliers Bargaining Power

Critical grid OEMs

High-voltage equipment, transformers and switchgear are concentrated among OEMs like Siemens Energy, ABB and GE, giving suppliers leverage on price and delivery. Lead times typically run 12–24 months and qualification cycles add 6–18 months, raising switching costs. E.ON mitigates this with framework contracts and scale purchasing, while regulated capex recovery mechanisms in Europe can allow partial pass-through of supplier cost increases.

Smart tech & IT vendors

Smart tech and cybersecurity platforms for advanced metering and grid automation come from specialized vendors, creating dependency as E.ON serves around 50 million customers across Europe. Integration and data migration raise switching costs and operational risk, but E.ON counters with modular architectures and multi-vendor procurement. Still, rapid 2024 tech cycles and suppliers with unique AI or OT security capabilities can quickly restore bargaining leverage.

Wholesale energy providers

E.ON buys electricity and gas from volatile wholesale markets and generators, where tight supply can create scarcity premia and boost generators’ bargaining power. Robust hedging programs and long-term contracts reduce E.ON’s spot exposure. European market liquidity and diverse generation sources generally prevent any single supplier from dominating. Hedging and contracts remain core to managing cost spikes.

Skilled labor & contractors

Grid modernization elevates supplier power as scarce engineers and field technicians drive contractor pricing pressure; E.ON reported about 72,000 employees in 2023, underpinning its internal skills base. Safety and certification requirements limit substitutability, so E.ON leans on training pipelines and long-term contractor partnerships while using flexible scheduling to smooth peak labor costs.

- Scarcity: specialized technicians limited, raising bargaining power

- Regulation: certifications restrict replacement options

- Mitigation: internal training pipelines, long-term contracts

- Operational: flexible scheduling reduces peak-rate exposure

Capital providers

- Capex intensity: high

- ECB rate 2024: ~4%

- Credit profile: investment‑grade (S&P BBB+)

- Mitigant: regulatory WACC recognition; ESG funding broadens options

Concentrated OEM power raises high-voltage supply risk; scale and long-term hedges mitigate

Supplier power is elevated for high‑voltage OEMs and specialized smart‑grid vendors (Siemens Energy, ABB, GE) due to concentration, long lead times (12–24m) and costly qualification, though E.ON’s scale, framework contracts and modular multi‑vendor architecture reduce exposure; wholesale generators can exert spot pressure but hedging and long‑term contracts cut volatility.

| Metric | 2024 value |

|---|---|

| Retail customers | ~50m |

| OEM lead times | 12–24 months |

| ECB rate | ~4% |

| Credit rating | S&P BBB+ |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, substitutes and entry risks for E.ON, assessing how regulatory shifts, renewables and grid investments reshape its profitability and defensive advantages.

Clear, one-sheet Porter's Five Forces for E.ON that highlights supplier, buyer, rivalry, substitute and entrant pressures to speed board decisions and scenario planning.

Customers Bargaining Power

Household customers

Household customers face low switching costs in liberalized markets, driving high price sensitivity; European household annual switching averaged about 6% in 2024. Comparison sites and aggregators now influence a majority of moves, amplifying transparency and churn risk. Many customers remain sticky due to inertia and bundled heating, broadband or green tariffs. Regulated network tariffs, covering roughly 40% of typical household bills, insulate a large earnings base from direct household bargaining.

Large industrials

Large industrials negotiate bespoke contracts and run competitive tenders, concentrating purchasing power and demanding flexibility and green attributes; E.ON, serving roughly 50 million customers, counters with PPAs, demand-response and onsite solutions to protect margin. In 2024 E.ON increased corporate PPA capacity and uses credit-risk screening and collateral requirements to mitigate counterparty leverage and default exposure.

Municipalities & DSOs interface

Franchise-style concessions with roughly 11,000 German municipalities shape local-service terms, with contracts commonly spanning 10–20 years, limiting renegotiation frequency but raising long-term performance obligations. Municipalities and DSOs press E.ON for reliability, resilience and affordability, tying payments to service-level metrics. Co-investment models and joint capex programs align incentives and dilute pure buyer leverage by sharing risk and returns.

Regulated end-users

- Regulated pricing: set by regulators, not negotiation

- Buyer power: capped but offset by quality penalties

- Scale: c.50 million customers

- Key focus: compliance and transparent cost reporting to protect allowed returns

Corporate sustainability buyers

Corporate sustainability buyers demand decarbonization roadmaps, green tariffs and guarantees of origin, shifting specification power toward solution value rather than price; E.ON, serving about 50 million customers, leverages efficiency, EV and PPA bundles to blunt buyer leverage. Long-term decarbonization contracts further stabilize relationships and reduce churn.

- Decarbonization focus: roadmap + GO + green tariffs

- E.ON scale: ~50 million customers

- Portfolio edge: efficiency, EV, PPA bundles

- Contracts: long-term deals lower buyer bargaining power

6% household switching boosts price sensitivity; regulated tariffs ~40% cap bargaining

Household switching ~6% pa (2024) increases price sensitivity while regulated network tariffs ~40% of bills cap direct bargaining. E.ON scale ~50m customers and corporate PPAs reduce buyer leverage. ~11,000 German municipal concessions create long-term contracts and co-investment that dilute pure buyer power.

| Metric | Value | Note |

|---|---|---|

| Customers | ~50m | Europe |

| Household switching | 6% (2024) | EU average |

| Regulated share | ~40% | Typical household bill |

| Municipal concessions (DE) | ~11,000 | Long-term contracts |

Same Document Delivered

E.ON Porter's Five Forces Analysis

This preview shows the exact E.ON Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The file is the complete, professionally formatted report ready for download and use. It covers supplier and buyer power, competitive rivalry, and threats of entry and substitution as applied to E.ON. You'll get instant access to this identical document upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

E.ON faces intense supplier negotiations, regulatory pressure, and evolving substitute risks from decentralised renewables, while buyer power and new entrants remain moderate; strategic moves will determine resilience. This snapshot highlights key tensions and opportunities. Unlock the full Porter's Five Forces Analysis for a force-by-force, data-driven strategic roadmap tailored to E.ON.

Suppliers Bargaining Power

Critical grid OEMs

High-voltage equipment, transformers and switchgear are concentrated among OEMs like Siemens Energy, ABB and GE, giving suppliers leverage on price and delivery. Lead times typically run 12–24 months and qualification cycles add 6–18 months, raising switching costs. E.ON mitigates this with framework contracts and scale purchasing, while regulated capex recovery mechanisms in Europe can allow partial pass-through of supplier cost increases.

Smart tech & IT vendors

Smart tech and cybersecurity platforms for advanced metering and grid automation come from specialized vendors, creating dependency as E.ON serves around 50 million customers across Europe. Integration and data migration raise switching costs and operational risk, but E.ON counters with modular architectures and multi-vendor procurement. Still, rapid 2024 tech cycles and suppliers with unique AI or OT security capabilities can quickly restore bargaining leverage.

Wholesale energy providers

E.ON buys electricity and gas from volatile wholesale markets and generators, where tight supply can create scarcity premia and boost generators’ bargaining power. Robust hedging programs and long-term contracts reduce E.ON’s spot exposure. European market liquidity and diverse generation sources generally prevent any single supplier from dominating. Hedging and contracts remain core to managing cost spikes.

Skilled labor & contractors

Grid modernization elevates supplier power as scarce engineers and field technicians drive contractor pricing pressure; E.ON reported about 72,000 employees in 2023, underpinning its internal skills base. Safety and certification requirements limit substitutability, so E.ON leans on training pipelines and long-term contractor partnerships while using flexible scheduling to smooth peak labor costs.

- Scarcity: specialized technicians limited, raising bargaining power

- Regulation: certifications restrict replacement options

- Mitigation: internal training pipelines, long-term contracts

- Operational: flexible scheduling reduces peak-rate exposure

Capital providers

- Capex intensity: high

- ECB rate 2024: ~4%

- Credit profile: investment‑grade (S&P BBB+)

- Mitigant: regulatory WACC recognition; ESG funding broadens options

Concentrated OEM power raises high-voltage supply risk; scale and long-term hedges mitigate

Supplier power is elevated for high‑voltage OEMs and specialized smart‑grid vendors (Siemens Energy, ABB, GE) due to concentration, long lead times (12–24m) and costly qualification, though E.ON’s scale, framework contracts and modular multi‑vendor architecture reduce exposure; wholesale generators can exert spot pressure but hedging and long‑term contracts cut volatility.

| Metric | 2024 value |

|---|---|

| Retail customers | ~50m |

| OEM lead times | 12–24 months |

| ECB rate | ~4% |

| Credit rating | S&P BBB+ |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, substitutes and entry risks for E.ON, assessing how regulatory shifts, renewables and grid investments reshape its profitability and defensive advantages.

Clear, one-sheet Porter's Five Forces for E.ON that highlights supplier, buyer, rivalry, substitute and entrant pressures to speed board decisions and scenario planning.

Customers Bargaining Power

Household customers

Household customers face low switching costs in liberalized markets, driving high price sensitivity; European household annual switching averaged about 6% in 2024. Comparison sites and aggregators now influence a majority of moves, amplifying transparency and churn risk. Many customers remain sticky due to inertia and bundled heating, broadband or green tariffs. Regulated network tariffs, covering roughly 40% of typical household bills, insulate a large earnings base from direct household bargaining.

Large industrials

Large industrials negotiate bespoke contracts and run competitive tenders, concentrating purchasing power and demanding flexibility and green attributes; E.ON, serving roughly 50 million customers, counters with PPAs, demand-response and onsite solutions to protect margin. In 2024 E.ON increased corporate PPA capacity and uses credit-risk screening and collateral requirements to mitigate counterparty leverage and default exposure.

Municipalities & DSOs interface

Franchise-style concessions with roughly 11,000 German municipalities shape local-service terms, with contracts commonly spanning 10–20 years, limiting renegotiation frequency but raising long-term performance obligations. Municipalities and DSOs press E.ON for reliability, resilience and affordability, tying payments to service-level metrics. Co-investment models and joint capex programs align incentives and dilute pure buyer leverage by sharing risk and returns.

Regulated end-users

- Regulated pricing: set by regulators, not negotiation

- Buyer power: capped but offset by quality penalties

- Scale: c.50 million customers

- Key focus: compliance and transparent cost reporting to protect allowed returns

Corporate sustainability buyers

Corporate sustainability buyers demand decarbonization roadmaps, green tariffs and guarantees of origin, shifting specification power toward solution value rather than price; E.ON, serving about 50 million customers, leverages efficiency, EV and PPA bundles to blunt buyer leverage. Long-term decarbonization contracts further stabilize relationships and reduce churn.

- Decarbonization focus: roadmap + GO + green tariffs

- E.ON scale: ~50 million customers

- Portfolio edge: efficiency, EV, PPA bundles

- Contracts: long-term deals lower buyer bargaining power

6% household switching boosts price sensitivity; regulated tariffs ~40% cap bargaining

Household switching ~6% pa (2024) increases price sensitivity while regulated network tariffs ~40% of bills cap direct bargaining. E.ON scale ~50m customers and corporate PPAs reduce buyer leverage. ~11,000 German municipal concessions create long-term contracts and co-investment that dilute pure buyer power.

| Metric | Value | Note |

|---|---|---|

| Customers | ~50m | Europe |

| Household switching | 6% (2024) | EU average |

| Regulated share | ~40% | Typical household bill |

| Municipal concessions (DE) | ~11,000 | Long-term contracts |

Same Document Delivered

E.ON Porter's Five Forces Analysis

This preview shows the exact E.ON Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The file is the complete, professionally formatted report ready for download and use. It covers supplier and buyer power, competitive rivalry, and threats of entry and substitution as applied to E.ON. You'll get instant access to this identical document upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

E.ON faces intense supplier negotiations, regulatory pressure, and evolving substitute risks from decentralised renewables, while buyer power and new entrants remain moderate; strategic moves will determine resilience. This snapshot highlights key tensions and opportunities. Unlock the full Porter's Five Forces Analysis for a force-by-force, data-driven strategic roadmap tailored to E.ON.

Suppliers Bargaining Power

Critical grid OEMs

High-voltage equipment, transformers and switchgear are concentrated among OEMs like Siemens Energy, ABB and GE, giving suppliers leverage on price and delivery. Lead times typically run 12–24 months and qualification cycles add 6–18 months, raising switching costs. E.ON mitigates this with framework contracts and scale purchasing, while regulated capex recovery mechanisms in Europe can allow partial pass-through of supplier cost increases.

Smart tech & IT vendors

Smart tech and cybersecurity platforms for advanced metering and grid automation come from specialized vendors, creating dependency as E.ON serves around 50 million customers across Europe. Integration and data migration raise switching costs and operational risk, but E.ON counters with modular architectures and multi-vendor procurement. Still, rapid 2024 tech cycles and suppliers with unique AI or OT security capabilities can quickly restore bargaining leverage.

Wholesale energy providers

E.ON buys electricity and gas from volatile wholesale markets and generators, where tight supply can create scarcity premia and boost generators’ bargaining power. Robust hedging programs and long-term contracts reduce E.ON’s spot exposure. European market liquidity and diverse generation sources generally prevent any single supplier from dominating. Hedging and contracts remain core to managing cost spikes.

Skilled labor & contractors

Grid modernization elevates supplier power as scarce engineers and field technicians drive contractor pricing pressure; E.ON reported about 72,000 employees in 2023, underpinning its internal skills base. Safety and certification requirements limit substitutability, so E.ON leans on training pipelines and long-term contractor partnerships while using flexible scheduling to smooth peak labor costs.

- Scarcity: specialized technicians limited, raising bargaining power

- Regulation: certifications restrict replacement options

- Mitigation: internal training pipelines, long-term contracts

- Operational: flexible scheduling reduces peak-rate exposure

Capital providers

- Capex intensity: high

- ECB rate 2024: ~4%

- Credit profile: investment‑grade (S&P BBB+)

- Mitigant: regulatory WACC recognition; ESG funding broadens options

Concentrated OEM power raises high-voltage supply risk; scale and long-term hedges mitigate

Supplier power is elevated for high‑voltage OEMs and specialized smart‑grid vendors (Siemens Energy, ABB, GE) due to concentration, long lead times (12–24m) and costly qualification, though E.ON’s scale, framework contracts and modular multi‑vendor architecture reduce exposure; wholesale generators can exert spot pressure but hedging and long‑term contracts cut volatility.

| Metric | 2024 value |

|---|---|

| Retail customers | ~50m |

| OEM lead times | 12–24 months |

| ECB rate | ~4% |

| Credit rating | S&P BBB+ |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, substitutes and entry risks for E.ON, assessing how regulatory shifts, renewables and grid investments reshape its profitability and defensive advantages.

Clear, one-sheet Porter's Five Forces for E.ON that highlights supplier, buyer, rivalry, substitute and entrant pressures to speed board decisions and scenario planning.

Customers Bargaining Power

Household customers

Household customers face low switching costs in liberalized markets, driving high price sensitivity; European household annual switching averaged about 6% in 2024. Comparison sites and aggregators now influence a majority of moves, amplifying transparency and churn risk. Many customers remain sticky due to inertia and bundled heating, broadband or green tariffs. Regulated network tariffs, covering roughly 40% of typical household bills, insulate a large earnings base from direct household bargaining.

Large industrials

Large industrials negotiate bespoke contracts and run competitive tenders, concentrating purchasing power and demanding flexibility and green attributes; E.ON, serving roughly 50 million customers, counters with PPAs, demand-response and onsite solutions to protect margin. In 2024 E.ON increased corporate PPA capacity and uses credit-risk screening and collateral requirements to mitigate counterparty leverage and default exposure.

Municipalities & DSOs interface

Franchise-style concessions with roughly 11,000 German municipalities shape local-service terms, with contracts commonly spanning 10–20 years, limiting renegotiation frequency but raising long-term performance obligations. Municipalities and DSOs press E.ON for reliability, resilience and affordability, tying payments to service-level metrics. Co-investment models and joint capex programs align incentives and dilute pure buyer leverage by sharing risk and returns.

Regulated end-users

- Regulated pricing: set by regulators, not negotiation

- Buyer power: capped but offset by quality penalties

- Scale: c.50 million customers

- Key focus: compliance and transparent cost reporting to protect allowed returns

Corporate sustainability buyers

Corporate sustainability buyers demand decarbonization roadmaps, green tariffs and guarantees of origin, shifting specification power toward solution value rather than price; E.ON, serving about 50 million customers, leverages efficiency, EV and PPA bundles to blunt buyer leverage. Long-term decarbonization contracts further stabilize relationships and reduce churn.

- Decarbonization focus: roadmap + GO + green tariffs

- E.ON scale: ~50 million customers

- Portfolio edge: efficiency, EV, PPA bundles

- Contracts: long-term deals lower buyer bargaining power

6% household switching boosts price sensitivity; regulated tariffs ~40% cap bargaining

Household switching ~6% pa (2024) increases price sensitivity while regulated network tariffs ~40% of bills cap direct bargaining. E.ON scale ~50m customers and corporate PPAs reduce buyer leverage. ~11,000 German municipal concessions create long-term contracts and co-investment that dilute pure buyer power.

| Metric | Value | Note |

|---|---|---|

| Customers | ~50m | Europe |

| Household switching | 6% (2024) | EU average |

| Regulated share | ~40% | Typical household bill |

| Municipal concessions (DE) | ~11,000 | Long-term contracts |

Same Document Delivered

E.ON Porter's Five Forces Analysis

This preview shows the exact E.ON Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The file is the complete, professionally formatted report ready for download and use. It covers supplier and buyer power, competitive rivalry, and threats of entry and substitution as applied to E.ON. You'll get instant access to this identical document upon payment.