EQT Porter's Five Forces Analysis

From Overview to Strategy Blueprint

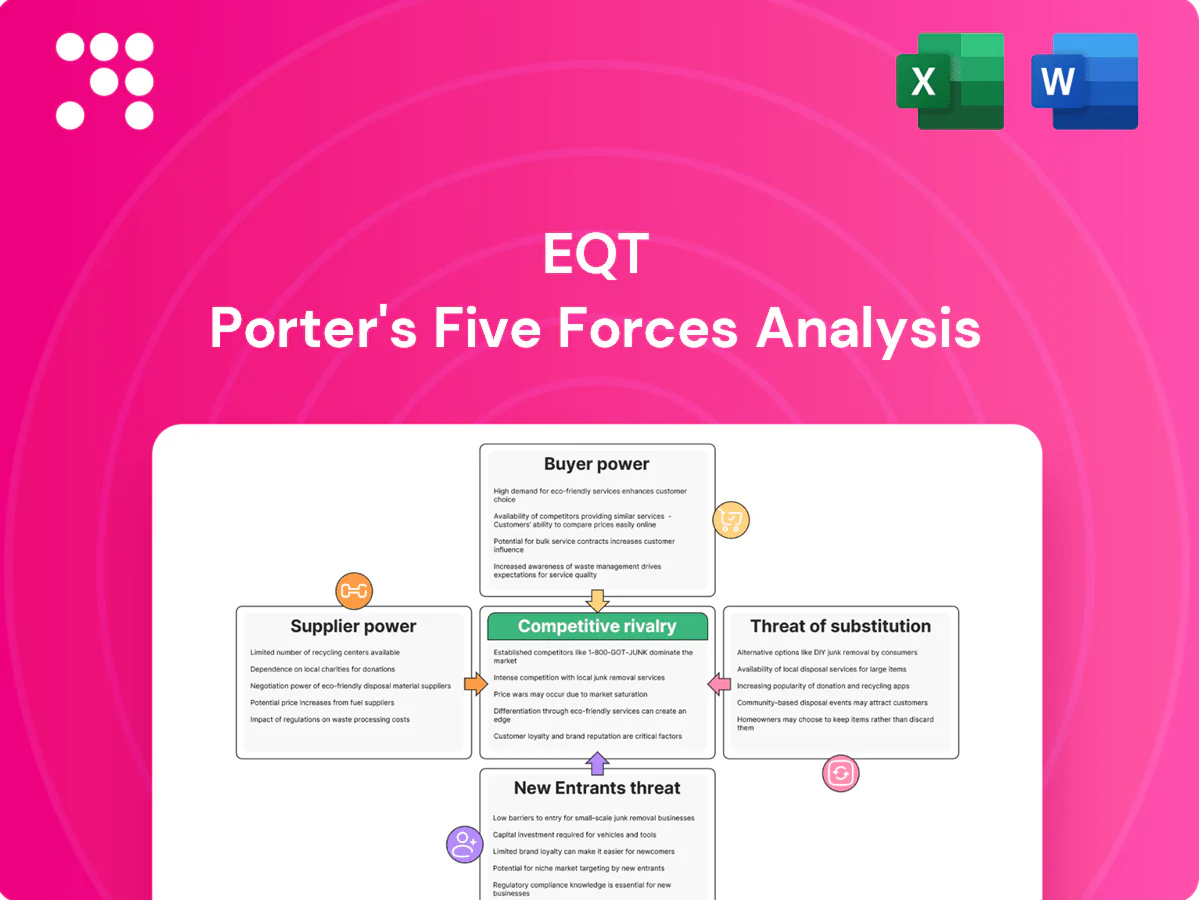

EQT faces distinct dynamics across supplier power, buyer influence, competitive rivalry and regulatory threats that shape deal flow and portfolio returns. Our snapshot highlights moderate supplier leverage, intense competition for assets and material sensitivity to macro and policy shifts. Strategic scale and sector focus mitigate some risks but substitute and entrant threats vary by market. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore EQT’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized oilfield inputs

EQT relies on specialized vendors for rigs, pressure pumping, OCTG, proppant, water and chemicals, and 2024 capacity cycles have tightened pricing and lengthened lead times, raising per‑well costs. Supplier consolidation in pressure pumping gives concentrated leverage, with the top three firms holding the majority of the 2024 market. EQT offsets this through multi‑year contracts and scale purchasing to smooth costs and secure capacity.

Midstream and takeaway access

Gathering and transmission capacity is essential in Appalachia, where basis differentials remained volatile in 2024, often swinging more than 0.50 $/MMBtu and stressing netbacks. Limited new pipeline buildout has given midstream owners measurable bargaining leverage, with tariffs and minimum volume commitments compressing producer margins. EQT offsets exposure through owned and contracted infrastructure and active flow-assurance strategies to protect realized prices.

Land and mineral rights holders

Acreage quality and continuity hinge on leasing terms from mineral owners; competitive leasing and renewals can lift upfront bonuses and royalty burdens, while unitization and surface-use agreements add complexity and potential delays. EQT, the largest U.S. natural gas producer in 2024, benefits from a large, contiguous Appalachian position that reduces exposure to piecemeal negotiations and transactional holdouts.

Skilled labor and services

Field crews, engineers and HSE specialists are finite, with Baker Hughes reporting a roughly 15% rise in US rig activity in 2024 that tightened labor markets; tightness has pushed day rates higher and slowed pad schedules. Safety and compliance requirements limit substitutability, making skilled providers sticky. EQT uses standardization and digital tools to cut labor intensity per well and shorten cycle times.

- Labor tightness: Baker Hughes ~15% US rig activity rise in 2024

- Cost pressure: higher day rates and delayed pad schedules

- Low substitutability: HSE and certified specialists required

- EQT response: standardization and tech to reduce crew-hours per well

Water sourcing and disposal

Fracturing depends on reliable water logistics and disposal/recycling partners, giving local service providers bargaining leverage over operators. Regulatory scrutiny and routing constraints in 2024 have raised compliance costs and amplified supplier power in some basins. Saltwater disposal availability and long trucking distances materially worsen well economics, increasing per-well operating costs.

- 2024: EQT expanding recycling and produced-water pipelines to reduce third-party exposure

- Regulatory limits ↑ supplier leverage in constrained counties

- Longer trucking distances increase OPEX and supplier bargaining power

Pressure-pump consolidation, +15% rigs and midstream scarcity drove >$0.50/MMBtu basis swings

Specialized vendors and consolidated pressure‑pumping (top three firms hold the 2024 majority) tightened pricing and lead times; midstream capacity scarcity drove basis swings >0.50 $/MMBtu in 2024, compressing netbacks. Baker Hughes reported ~15% US rig activity rise in 2024, tightening crews and day rates. EQT mitigates via owned pipelines, multi‑year contracts and recycling investment.

| Metric | 2024 |

|---|---|

| Rig activity (Baker Hughes) | +15% |

| Basis volatility | >0.50 $/MMBtu |

| Pressure pump market | Top 3 = majority |

| EQT position | Largest US gas producer |

What is included in the product

Tailored Porter's Five Forces analysis for EQT that uncovers competitive drivers, buyer and supplier power, entry barriers, substitute threats, and emerging disruptors to evaluate pricing leverage and long-term profitability.

Instantly visualise EQT's competitive pressures across all five forces for faster strategic decisions; editable pressure levels and a powerful radar chart make trade-offs clear. Clean, one-sheet layout requires no macros—easy to copy into decks or integrate into dashboards.

Customers Bargaining Power

Commodity buyers with price transparency

Utilities, LDCs, LNG exporters and industrials buy gas at market-linked prices, with 2024 Henry Hub averaging about $2.73/MMBtu and Appalachia basis driving local pricing, which constrains EQT’s pricing discretion; transparent hubs let buyers time purchases and hedge, boosting their leverage. EQT counters with active hedging programs, diversified outlets (pipeline/LNG) and basis optimization to protect realized prices.

Low switching costs among producers

Gas is largely standardized within quality specs, so buyers can switch suppliers readily, intensifying price-based competition; Henry Hub averaged about 2.99 USD/MMBtu in 2024, tightening margins. Contracts therefore emphasize reliability, scheduling and credit terms over brand. EQT, the largest U.S. gas producer in 2024, counters by leveraging scale, high uptime and firm transportation commitments to guarantee deliveries.

Contract mix and terms

Buyers negotiate volumes, take-or-pay and price formulas, forcing EQT to lock volumes while ceding pricing upside; EQT, the largest U.S. gas producer, ran an approximate 60/40 term-to-spot sales mix in 2024 to balance risk. Long-term offtakes stabilize cash flows but can shift value to buyers in downcycles when Henry Hub averaged about 2.8 USD/MMBtu in 2024. Spot exposure raises earnings volatility and buyer optionality, so EQT blends term contracts with spot sales to optimize realizations.

Regional basis and congestion

Appalachian basis discounts give buyers leverage during takeaway constraints; 2024 winter spreads exceeded $2/MMBtu at times, and seasonal demand plus maintenance windows routinely widen spreads allowing buyers to arbitrage basin differentials. EQT’s ~3 Bcf/d transport portfolio and sales into multiple hubs reduce basis-driven buyer power by enabling diversion and firm-offtake management.

- Appalachian discounts enable leverage

- Seasonal/maintenance spreads >$2/MMBtu

- Buyers arbitrage basin differentials

- EQT ~3 Bcf/d transport cuts buyer power

Credit and counterparty concentration

Larger utilities and LNG offtakers exert strong negotiation leverage through scale and credit quality, often demanding credit support and performance guarantees; in 2024 EQT reported using collateral and contractual protections to mitigate such demands. Counterparty diversification reduces concentration risk, and EQT manages exposure via formal credit policies and multiple sales channels including direct offtake and third‑party marketers.

- Offtaker leverage: scale + credit quality

- Common demands: letters of credit, guarantees

- Mitigation: diversification of counterparties

- EQT 2024: formal credit policies, diversified sales channels

Market-linked gas: buyers use hedges; 60/40 term/spot, 3 Bcf/d transport

Buyers purchase at market-linked prices (Henry Hub avg ~2.73 USD/MMBtu in 2024), with transparent hubs and hedging options increasing buyer leverage. Gas is standardized so switching is easy; EQT offsets with scale, high uptime and ~3 Bcf/d transport. Large offtakers demand credit and terms; EQT ran ~60/40 term-to-spot sales and diversified counterparties in 2024.

| Metric | 2024 |

|---|---|

| Henry Hub avg | ~2.73 USD/MMBtu |

| Appalachian winter spreads | >2 USD/MMBtu |

| EQT transport | ~3 Bcf/d |

| Sales mix | ~60/40 term/spot |

Preview the Actual Deliverable

EQT Porter's Five Forces Analysis

This preview displays the complete EQT Porter’s Five Forces analysis you’ll receive—no samples, no placeholders. The file shown is fully formatted and ready for download the moment you complete your purchase. You’re viewing the exact deliverable, prepared for immediate use.

From Overview to Strategy Blueprint

EQT faces distinct dynamics across supplier power, buyer influence, competitive rivalry and regulatory threats that shape deal flow and portfolio returns. Our snapshot highlights moderate supplier leverage, intense competition for assets and material sensitivity to macro and policy shifts. Strategic scale and sector focus mitigate some risks but substitute and entrant threats vary by market. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore EQT’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized oilfield inputs

EQT relies on specialized vendors for rigs, pressure pumping, OCTG, proppant, water and chemicals, and 2024 capacity cycles have tightened pricing and lengthened lead times, raising per‑well costs. Supplier consolidation in pressure pumping gives concentrated leverage, with the top three firms holding the majority of the 2024 market. EQT offsets this through multi‑year contracts and scale purchasing to smooth costs and secure capacity.

Midstream and takeaway access

Gathering and transmission capacity is essential in Appalachia, where basis differentials remained volatile in 2024, often swinging more than 0.50 $/MMBtu and stressing netbacks. Limited new pipeline buildout has given midstream owners measurable bargaining leverage, with tariffs and minimum volume commitments compressing producer margins. EQT offsets exposure through owned and contracted infrastructure and active flow-assurance strategies to protect realized prices.

Land and mineral rights holders

Acreage quality and continuity hinge on leasing terms from mineral owners; competitive leasing and renewals can lift upfront bonuses and royalty burdens, while unitization and surface-use agreements add complexity and potential delays. EQT, the largest U.S. natural gas producer in 2024, benefits from a large, contiguous Appalachian position that reduces exposure to piecemeal negotiations and transactional holdouts.

Skilled labor and services

Field crews, engineers and HSE specialists are finite, with Baker Hughes reporting a roughly 15% rise in US rig activity in 2024 that tightened labor markets; tightness has pushed day rates higher and slowed pad schedules. Safety and compliance requirements limit substitutability, making skilled providers sticky. EQT uses standardization and digital tools to cut labor intensity per well and shorten cycle times.

- Labor tightness: Baker Hughes ~15% US rig activity rise in 2024

- Cost pressure: higher day rates and delayed pad schedules

- Low substitutability: HSE and certified specialists required

- EQT response: standardization and tech to reduce crew-hours per well

Water sourcing and disposal

Fracturing depends on reliable water logistics and disposal/recycling partners, giving local service providers bargaining leverage over operators. Regulatory scrutiny and routing constraints in 2024 have raised compliance costs and amplified supplier power in some basins. Saltwater disposal availability and long trucking distances materially worsen well economics, increasing per-well operating costs.

- 2024: EQT expanding recycling and produced-water pipelines to reduce third-party exposure

- Regulatory limits ↑ supplier leverage in constrained counties

- Longer trucking distances increase OPEX and supplier bargaining power

Pressure-pump consolidation, +15% rigs and midstream scarcity drove >$0.50/MMBtu basis swings

Specialized vendors and consolidated pressure‑pumping (top three firms hold the 2024 majority) tightened pricing and lead times; midstream capacity scarcity drove basis swings >0.50 $/MMBtu in 2024, compressing netbacks. Baker Hughes reported ~15% US rig activity rise in 2024, tightening crews and day rates. EQT mitigates via owned pipelines, multi‑year contracts and recycling investment.

| Metric | 2024 |

|---|---|

| Rig activity (Baker Hughes) | +15% |

| Basis volatility | >0.50 $/MMBtu |

| Pressure pump market | Top 3 = majority |

| EQT position | Largest US gas producer |

What is included in the product

Tailored Porter's Five Forces analysis for EQT that uncovers competitive drivers, buyer and supplier power, entry barriers, substitute threats, and emerging disruptors to evaluate pricing leverage and long-term profitability.

Instantly visualise EQT's competitive pressures across all five forces for faster strategic decisions; editable pressure levels and a powerful radar chart make trade-offs clear. Clean, one-sheet layout requires no macros—easy to copy into decks or integrate into dashboards.

Customers Bargaining Power

Commodity buyers with price transparency

Utilities, LDCs, LNG exporters and industrials buy gas at market-linked prices, with 2024 Henry Hub averaging about $2.73/MMBtu and Appalachia basis driving local pricing, which constrains EQT’s pricing discretion; transparent hubs let buyers time purchases and hedge, boosting their leverage. EQT counters with active hedging programs, diversified outlets (pipeline/LNG) and basis optimization to protect realized prices.

Low switching costs among producers

Gas is largely standardized within quality specs, so buyers can switch suppliers readily, intensifying price-based competition; Henry Hub averaged about 2.99 USD/MMBtu in 2024, tightening margins. Contracts therefore emphasize reliability, scheduling and credit terms over brand. EQT, the largest U.S. gas producer in 2024, counters by leveraging scale, high uptime and firm transportation commitments to guarantee deliveries.

Contract mix and terms

Buyers negotiate volumes, take-or-pay and price formulas, forcing EQT to lock volumes while ceding pricing upside; EQT, the largest U.S. gas producer, ran an approximate 60/40 term-to-spot sales mix in 2024 to balance risk. Long-term offtakes stabilize cash flows but can shift value to buyers in downcycles when Henry Hub averaged about 2.8 USD/MMBtu in 2024. Spot exposure raises earnings volatility and buyer optionality, so EQT blends term contracts with spot sales to optimize realizations.

Regional basis and congestion

Appalachian basis discounts give buyers leverage during takeaway constraints; 2024 winter spreads exceeded $2/MMBtu at times, and seasonal demand plus maintenance windows routinely widen spreads allowing buyers to arbitrage basin differentials. EQT’s ~3 Bcf/d transport portfolio and sales into multiple hubs reduce basis-driven buyer power by enabling diversion and firm-offtake management.

- Appalachian discounts enable leverage

- Seasonal/maintenance spreads >$2/MMBtu

- Buyers arbitrage basin differentials

- EQT ~3 Bcf/d transport cuts buyer power

Credit and counterparty concentration

Larger utilities and LNG offtakers exert strong negotiation leverage through scale and credit quality, often demanding credit support and performance guarantees; in 2024 EQT reported using collateral and contractual protections to mitigate such demands. Counterparty diversification reduces concentration risk, and EQT manages exposure via formal credit policies and multiple sales channels including direct offtake and third‑party marketers.

- Offtaker leverage: scale + credit quality

- Common demands: letters of credit, guarantees

- Mitigation: diversification of counterparties

- EQT 2024: formal credit policies, diversified sales channels

Market-linked gas: buyers use hedges; 60/40 term/spot, 3 Bcf/d transport

Buyers purchase at market-linked prices (Henry Hub avg ~2.73 USD/MMBtu in 2024), with transparent hubs and hedging options increasing buyer leverage. Gas is standardized so switching is easy; EQT offsets with scale, high uptime and ~3 Bcf/d transport. Large offtakers demand credit and terms; EQT ran ~60/40 term-to-spot sales and diversified counterparties in 2024.

| Metric | 2024 |

|---|---|

| Henry Hub avg | ~2.73 USD/MMBtu |

| Appalachian winter spreads | >2 USD/MMBtu |

| EQT transport | ~3 Bcf/d |

| Sales mix | ~60/40 term/spot |

Preview the Actual Deliverable

EQT Porter's Five Forces Analysis

This preview displays the complete EQT Porter’s Five Forces analysis you’ll receive—no samples, no placeholders. The file shown is fully formatted and ready for download the moment you complete your purchase. You’re viewing the exact deliverable, prepared for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

EQT faces distinct dynamics across supplier power, buyer influence, competitive rivalry and regulatory threats that shape deal flow and portfolio returns. Our snapshot highlights moderate supplier leverage, intense competition for assets and material sensitivity to macro and policy shifts. Strategic scale and sector focus mitigate some risks but substitute and entrant threats vary by market. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore EQT’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized oilfield inputs

EQT relies on specialized vendors for rigs, pressure pumping, OCTG, proppant, water and chemicals, and 2024 capacity cycles have tightened pricing and lengthened lead times, raising per‑well costs. Supplier consolidation in pressure pumping gives concentrated leverage, with the top three firms holding the majority of the 2024 market. EQT offsets this through multi‑year contracts and scale purchasing to smooth costs and secure capacity.

Midstream and takeaway access

Gathering and transmission capacity is essential in Appalachia, where basis differentials remained volatile in 2024, often swinging more than 0.50 $/MMBtu and stressing netbacks. Limited new pipeline buildout has given midstream owners measurable bargaining leverage, with tariffs and minimum volume commitments compressing producer margins. EQT offsets exposure through owned and contracted infrastructure and active flow-assurance strategies to protect realized prices.

Land and mineral rights holders

Acreage quality and continuity hinge on leasing terms from mineral owners; competitive leasing and renewals can lift upfront bonuses and royalty burdens, while unitization and surface-use agreements add complexity and potential delays. EQT, the largest U.S. natural gas producer in 2024, benefits from a large, contiguous Appalachian position that reduces exposure to piecemeal negotiations and transactional holdouts.

Skilled labor and services

Field crews, engineers and HSE specialists are finite, with Baker Hughes reporting a roughly 15% rise in US rig activity in 2024 that tightened labor markets; tightness has pushed day rates higher and slowed pad schedules. Safety and compliance requirements limit substitutability, making skilled providers sticky. EQT uses standardization and digital tools to cut labor intensity per well and shorten cycle times.

- Labor tightness: Baker Hughes ~15% US rig activity rise in 2024

- Cost pressure: higher day rates and delayed pad schedules

- Low substitutability: HSE and certified specialists required

- EQT response: standardization and tech to reduce crew-hours per well

Water sourcing and disposal

Fracturing depends on reliable water logistics and disposal/recycling partners, giving local service providers bargaining leverage over operators. Regulatory scrutiny and routing constraints in 2024 have raised compliance costs and amplified supplier power in some basins. Saltwater disposal availability and long trucking distances materially worsen well economics, increasing per-well operating costs.

- 2024: EQT expanding recycling and produced-water pipelines to reduce third-party exposure

- Regulatory limits ↑ supplier leverage in constrained counties

- Longer trucking distances increase OPEX and supplier bargaining power

Pressure-pump consolidation, +15% rigs and midstream scarcity drove >$0.50/MMBtu basis swings

Specialized vendors and consolidated pressure‑pumping (top three firms hold the 2024 majority) tightened pricing and lead times; midstream capacity scarcity drove basis swings >0.50 $/MMBtu in 2024, compressing netbacks. Baker Hughes reported ~15% US rig activity rise in 2024, tightening crews and day rates. EQT mitigates via owned pipelines, multi‑year contracts and recycling investment.

| Metric | 2024 |

|---|---|

| Rig activity (Baker Hughes) | +15% |

| Basis volatility | >0.50 $/MMBtu |

| Pressure pump market | Top 3 = majority |

| EQT position | Largest US gas producer |

What is included in the product

Tailored Porter's Five Forces analysis for EQT that uncovers competitive drivers, buyer and supplier power, entry barriers, substitute threats, and emerging disruptors to evaluate pricing leverage and long-term profitability.

Instantly visualise EQT's competitive pressures across all five forces for faster strategic decisions; editable pressure levels and a powerful radar chart make trade-offs clear. Clean, one-sheet layout requires no macros—easy to copy into decks or integrate into dashboards.

Customers Bargaining Power

Commodity buyers with price transparency

Utilities, LDCs, LNG exporters and industrials buy gas at market-linked prices, with 2024 Henry Hub averaging about $2.73/MMBtu and Appalachia basis driving local pricing, which constrains EQT’s pricing discretion; transparent hubs let buyers time purchases and hedge, boosting their leverage. EQT counters with active hedging programs, diversified outlets (pipeline/LNG) and basis optimization to protect realized prices.

Low switching costs among producers

Gas is largely standardized within quality specs, so buyers can switch suppliers readily, intensifying price-based competition; Henry Hub averaged about 2.99 USD/MMBtu in 2024, tightening margins. Contracts therefore emphasize reliability, scheduling and credit terms over brand. EQT, the largest U.S. gas producer in 2024, counters by leveraging scale, high uptime and firm transportation commitments to guarantee deliveries.

Contract mix and terms

Buyers negotiate volumes, take-or-pay and price formulas, forcing EQT to lock volumes while ceding pricing upside; EQT, the largest U.S. gas producer, ran an approximate 60/40 term-to-spot sales mix in 2024 to balance risk. Long-term offtakes stabilize cash flows but can shift value to buyers in downcycles when Henry Hub averaged about 2.8 USD/MMBtu in 2024. Spot exposure raises earnings volatility and buyer optionality, so EQT blends term contracts with spot sales to optimize realizations.

Regional basis and congestion

Appalachian basis discounts give buyers leverage during takeaway constraints; 2024 winter spreads exceeded $2/MMBtu at times, and seasonal demand plus maintenance windows routinely widen spreads allowing buyers to arbitrage basin differentials. EQT’s ~3 Bcf/d transport portfolio and sales into multiple hubs reduce basis-driven buyer power by enabling diversion and firm-offtake management.

- Appalachian discounts enable leverage

- Seasonal/maintenance spreads >$2/MMBtu

- Buyers arbitrage basin differentials

- EQT ~3 Bcf/d transport cuts buyer power

Credit and counterparty concentration

Larger utilities and LNG offtakers exert strong negotiation leverage through scale and credit quality, often demanding credit support and performance guarantees; in 2024 EQT reported using collateral and contractual protections to mitigate such demands. Counterparty diversification reduces concentration risk, and EQT manages exposure via formal credit policies and multiple sales channels including direct offtake and third‑party marketers.

- Offtaker leverage: scale + credit quality

- Common demands: letters of credit, guarantees

- Mitigation: diversification of counterparties

- EQT 2024: formal credit policies, diversified sales channels

Market-linked gas: buyers use hedges; 60/40 term/spot, 3 Bcf/d transport

Buyers purchase at market-linked prices (Henry Hub avg ~2.73 USD/MMBtu in 2024), with transparent hubs and hedging options increasing buyer leverage. Gas is standardized so switching is easy; EQT offsets with scale, high uptime and ~3 Bcf/d transport. Large offtakers demand credit and terms; EQT ran ~60/40 term-to-spot sales and diversified counterparties in 2024.

| Metric | 2024 |

|---|---|

| Henry Hub avg | ~2.73 USD/MMBtu |

| Appalachian winter spreads | >2 USD/MMBtu |

| EQT transport | ~3 Bcf/d |

| Sales mix | ~60/40 term/spot |

Preview the Actual Deliverable

EQT Porter's Five Forces Analysis

This preview displays the complete EQT Porter’s Five Forces analysis you’ll receive—no samples, no placeholders. The file shown is fully formatted and ready for download the moment you complete your purchase. You’re viewing the exact deliverable, prepared for immediate use.