Equals Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

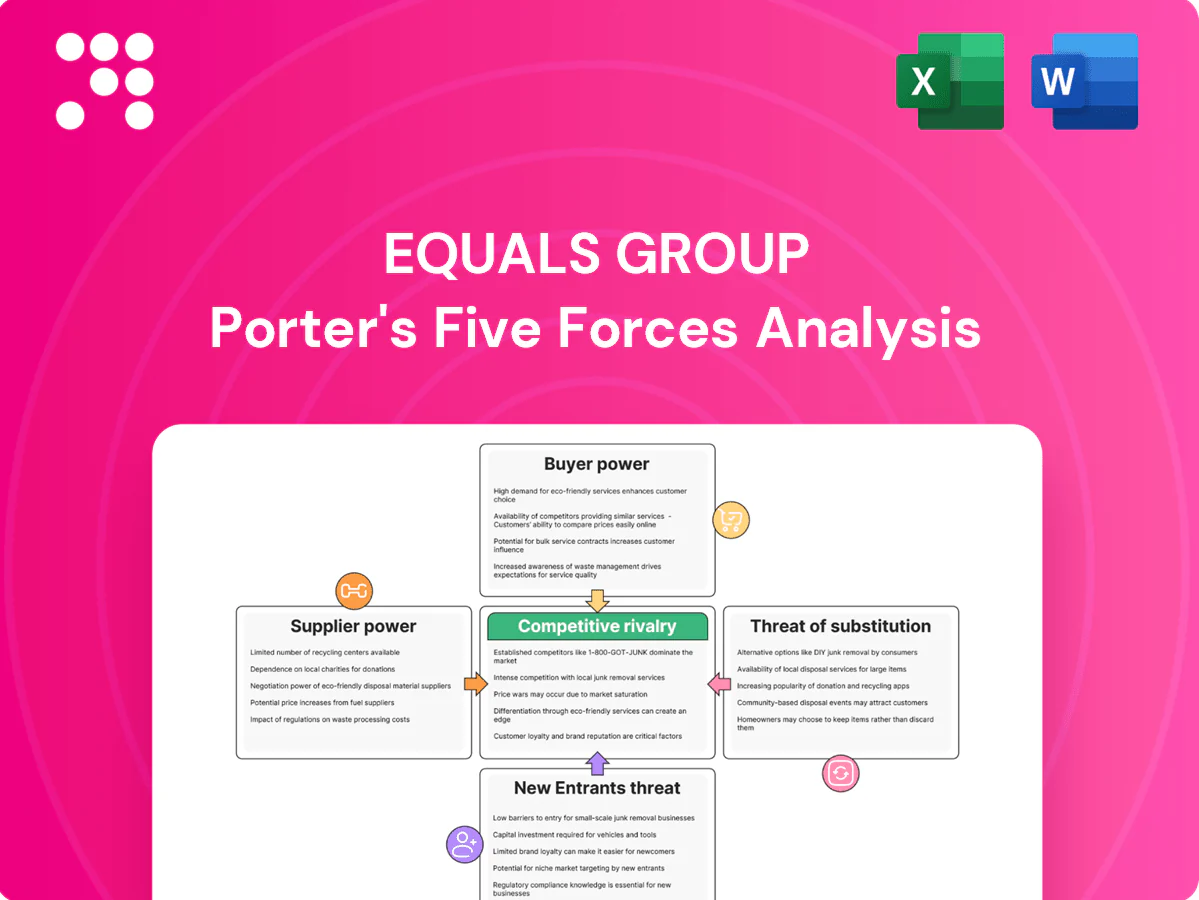

Equals Group faces moderate buyer power, niche supplier leverage, rising fintech entrants, and growing substitute channels that intensify rivalry—creating both pressure and opportunity for strategic differentiation. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Equals Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on FX liquidity providers

Equals relies on banks and market-makers for wholesale FX rates and liquidity, concentrating supplier influence and creating exposure when counterparties retract. In volatile sessions spreads and execution costs can widen materially, increasing Equals’ cost of goods sold. Diversified liquidity pools and smart routing mitigate but do not eliminate this dependency. Long-term partnerships and volume commitments support negotiation for tighter pricing.

Card schemes and payment networks

Visa and Mastercard together process over 80% of global card transactions, making scheme fees and network rules effectively non-negotiable cost floors for Equals; in the EU caps on interchange under IFR remain 0.2% for debit and 0.3% for credit (Regulation 2015/751).

Changes to scheme rules or fee schedules and compliance mandates (e.g., 3D Secure, PSD2 updates) can compress margins quickly as these costs are largely passthrough.

Scale enables better pricing tiers and volume rebates from schemes, but bargaining power remains skewed to schemes; multi-network connectivity (Visa, Mastercard, alternative networks) reduces single-network dependency risk.

Banking partners and correspondent rails

Equals relies on sponsor banks for safeguarding, settlement and corridor access; global correspondent banking relationships have declined roughly 15% since 2011 (World Bank), raising disruption risk from de-risking or exits. A multi-bank model across regions and firm service-level agreements provide redundancy, reducing single-point failures and lowering operational leverage of any one partner.

Regtech, data, and cloud vendors

Sanctions screening, KYC, and cloud infrastructure are mission-critical for Equals Group, creating high switching frictions that let vendors raise prices or alter terms; top three cloud providers held over 60% market share in 2024, concentrating supplier power. Contract diversification and modular architectures reduce lock-in, while volume-based discounts improve unit economics as transaction volumes scale.

- Sanctions/KYC: high switching friction

- Cloud concentration: top 3 >60% (2024)

- Mitigation: contract diversification, modular stacks

- Benefit: volume discounts lower marginal costs

FX and payments infrastructure APIs

Gateway, gateway-to-rails and treasury APIs determine Equals Group’s throughput costs and settlement speed; in 2024 API-driven routing reportedly supported a 35% uplift in transaction efficiency industry-wide, making proprietary features a lock-in risk that raises supplier power. Open standards and internal orchestration reduce dependence, while homegrown components in core pathways further weaken supplier leverage.

- API routing: improves throughput, ups vendor importance

- Proprietary features: increase switching costs

- Open standards/orchestration: strengthen negotiating leverage

- Homegrown core: lowers supplier power

Supplier concentration raises costs and frictions; multi-bank, multi-network stacks reduce them

Suppliers exert high leverage: wholesale FX banks/market-makers concentrate liquidity, Visa/Mastercard process >80% of card volume, and top-3 cloud providers held >60% share in 2024, while correspondent banking has fallen ~15% since 2011. These factors raise cost and switching friction; Equals mitigates via multi-bank, multi-network, modular stack and volume-based deals.

| Metric | Value |

|---|---|

| Card networks share | >80% |

| Top-3 cloud (2024) | >60% |

| Corr. banking decline | ~15% since 2011 |

| API efficiency (2024) | +35% |

What is included in the product

Tailored Porter's Five Forces analysis for Equals Group, uncovering key drivers of competition, buyer/supplier power, entry barriers and substitutes while identifying disruptive threats and strategic levers to protect market position.

Clear one-sheet Porter's Five Forces for Equals Group—instantly visualized with a spider chart and editable pressure levels to simplify strategic choices and relieve analysis bottlenecks.

Customers Bargaining Power

High price transparency

High price transparency lets SMEs and consumers compare FX spreads and fees instantly, compressing margins in a market with $7.5 trillion average daily FX turnover (BIS triennial 2022) and intensified fintech price competition by 2024. Equals must emphasize net landed cost, speed and service to avoid pure price battles. Dynamic pricing and tiered plans help defend margins while retaining volume-sensitive clients.

Low switching costs, multi-homing

By 2024 customers commonly multi-home across payment providers, and digital onboarding has materially lowered exit frictions, enabling rapid switches. Equals must increase stickiness via deep integrations, holding customer balances and embedding workflows to raise switching costs. Loyalty incentives and bundled features can reduce churn and protect margins in a low-switching-cost market.

Corporate RFP and volume leverage

Larger SMEs and mid-market firms increasingly use corporate RFPs in 2024 to pressure pricing and SLAs, forcing Equals to defend spreads and delivery windows. Volume tiers and corridor commitments commonly trade 5–20% margin for share in FX corridors, intensifying customer bargaining. Equals offsets pressure with value-added hedging, automated reconciliation and premium support. Data-driven pricing and unit-economics dashboards preserve margin visibility.

Service reliability and SLA sensitivity

Customers punish downtime with rapid switching; fintech SLAs of 99.99% (≈52.6 minutes annual downtime) versus 99.999% (≈5.26 minutes) are meaningful benchmarks, and clients demand 24/7 support plus predictable settlement windows (T+0 to T+2 common). Investing in resilience, realtime incident transparency and redundant infrastructure reduces perceived risk and churn. Premium support tiers allow direct monetization of higher-availability promises.

- High SLA benchmark: 99.99% ≈52.6 min/yr

- Higher tier: 99.999% ≈5.26 min/yr

- Settlement sensitivity: T+0–T+2

- 24/7 support expected

Integration and workflow expectations

Clients increasingly demand ERP and accounting plugins, robust APIs, sandbox tooling, and bulk payments, making deep integration a key buyer requirement that raises switching costs and reduces customer bargaining power. Equals should prioritize expanding connectors and developer sandboxes to lock in workflows and accelerate adoption. Embedded finance partnerships further entrench usage by embedding payments and treasury services into client systems.

- ERP plugins

- APIs & sandbox tooling

- Bulk payments

- Embedded finance

Sell speed and SLA resilience as FX transparency and fintech pricing squeeze margins

High price transparency (FX vol $7.5T avg daily, BIS 2022) and intensified fintech pricing in 2024 compress margins; Equals must sell speed, net landed cost and service not just price. Rapid multi‑homing and low onboarding frictions raise customer leverage; deep integrations, balances and APIs increase stickiness. Corporate RFPs push 5–20% corridor discounts; premium SLAs and tooling monetize resilience.

| Metric | 2024/Source |

|---|---|

| FX turnover | $7.5T avg/day (BIS 2022) |

| SLA benchmarks | 99.99% / 99.999% |

| Settlement | T+0–T+2 |

| RFP corridor impact | 5–20% margin trade |

What You See Is What You Get

Equals Group Porter's Five Forces Analysis

This Porter’s Five Forces analysis for Equals Group is the full, professionally formatted document you see in preview—covering competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. After purchase you’ll receive this exact file instantly, ready for use.

Go Beyond the Preview—Access the Full Strategic Report

Equals Group faces moderate buyer power, niche supplier leverage, rising fintech entrants, and growing substitute channels that intensify rivalry—creating both pressure and opportunity for strategic differentiation. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Equals Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on FX liquidity providers

Equals relies on banks and market-makers for wholesale FX rates and liquidity, concentrating supplier influence and creating exposure when counterparties retract. In volatile sessions spreads and execution costs can widen materially, increasing Equals’ cost of goods sold. Diversified liquidity pools and smart routing mitigate but do not eliminate this dependency. Long-term partnerships and volume commitments support negotiation for tighter pricing.

Card schemes and payment networks

Visa and Mastercard together process over 80% of global card transactions, making scheme fees and network rules effectively non-negotiable cost floors for Equals; in the EU caps on interchange under IFR remain 0.2% for debit and 0.3% for credit (Regulation 2015/751).

Changes to scheme rules or fee schedules and compliance mandates (e.g., 3D Secure, PSD2 updates) can compress margins quickly as these costs are largely passthrough.

Scale enables better pricing tiers and volume rebates from schemes, but bargaining power remains skewed to schemes; multi-network connectivity (Visa, Mastercard, alternative networks) reduces single-network dependency risk.

Banking partners and correspondent rails

Equals relies on sponsor banks for safeguarding, settlement and corridor access; global correspondent banking relationships have declined roughly 15% since 2011 (World Bank), raising disruption risk from de-risking or exits. A multi-bank model across regions and firm service-level agreements provide redundancy, reducing single-point failures and lowering operational leverage of any one partner.

Regtech, data, and cloud vendors

Sanctions screening, KYC, and cloud infrastructure are mission-critical for Equals Group, creating high switching frictions that let vendors raise prices or alter terms; top three cloud providers held over 60% market share in 2024, concentrating supplier power. Contract diversification and modular architectures reduce lock-in, while volume-based discounts improve unit economics as transaction volumes scale.

- Sanctions/KYC: high switching friction

- Cloud concentration: top 3 >60% (2024)

- Mitigation: contract diversification, modular stacks

- Benefit: volume discounts lower marginal costs

FX and payments infrastructure APIs

Gateway, gateway-to-rails and treasury APIs determine Equals Group’s throughput costs and settlement speed; in 2024 API-driven routing reportedly supported a 35% uplift in transaction efficiency industry-wide, making proprietary features a lock-in risk that raises supplier power. Open standards and internal orchestration reduce dependence, while homegrown components in core pathways further weaken supplier leverage.

- API routing: improves throughput, ups vendor importance

- Proprietary features: increase switching costs

- Open standards/orchestration: strengthen negotiating leverage

- Homegrown core: lowers supplier power

Supplier concentration raises costs and frictions; multi-bank, multi-network stacks reduce them

Suppliers exert high leverage: wholesale FX banks/market-makers concentrate liquidity, Visa/Mastercard process >80% of card volume, and top-3 cloud providers held >60% share in 2024, while correspondent banking has fallen ~15% since 2011. These factors raise cost and switching friction; Equals mitigates via multi-bank, multi-network, modular stack and volume-based deals.

| Metric | Value |

|---|---|

| Card networks share | >80% |

| Top-3 cloud (2024) | >60% |

| Corr. banking decline | ~15% since 2011 |

| API efficiency (2024) | +35% |

What is included in the product

Tailored Porter's Five Forces analysis for Equals Group, uncovering key drivers of competition, buyer/supplier power, entry barriers and substitutes while identifying disruptive threats and strategic levers to protect market position.

Clear one-sheet Porter's Five Forces for Equals Group—instantly visualized with a spider chart and editable pressure levels to simplify strategic choices and relieve analysis bottlenecks.

Customers Bargaining Power

High price transparency

High price transparency lets SMEs and consumers compare FX spreads and fees instantly, compressing margins in a market with $7.5 trillion average daily FX turnover (BIS triennial 2022) and intensified fintech price competition by 2024. Equals must emphasize net landed cost, speed and service to avoid pure price battles. Dynamic pricing and tiered plans help defend margins while retaining volume-sensitive clients.

Low switching costs, multi-homing

By 2024 customers commonly multi-home across payment providers, and digital onboarding has materially lowered exit frictions, enabling rapid switches. Equals must increase stickiness via deep integrations, holding customer balances and embedding workflows to raise switching costs. Loyalty incentives and bundled features can reduce churn and protect margins in a low-switching-cost market.

Corporate RFP and volume leverage

Larger SMEs and mid-market firms increasingly use corporate RFPs in 2024 to pressure pricing and SLAs, forcing Equals to defend spreads and delivery windows. Volume tiers and corridor commitments commonly trade 5–20% margin for share in FX corridors, intensifying customer bargaining. Equals offsets pressure with value-added hedging, automated reconciliation and premium support. Data-driven pricing and unit-economics dashboards preserve margin visibility.

Service reliability and SLA sensitivity

Customers punish downtime with rapid switching; fintech SLAs of 99.99% (≈52.6 minutes annual downtime) versus 99.999% (≈5.26 minutes) are meaningful benchmarks, and clients demand 24/7 support plus predictable settlement windows (T+0 to T+2 common). Investing in resilience, realtime incident transparency and redundant infrastructure reduces perceived risk and churn. Premium support tiers allow direct monetization of higher-availability promises.

- High SLA benchmark: 99.99% ≈52.6 min/yr

- Higher tier: 99.999% ≈5.26 min/yr

- Settlement sensitivity: T+0–T+2

- 24/7 support expected

Integration and workflow expectations

Clients increasingly demand ERP and accounting plugins, robust APIs, sandbox tooling, and bulk payments, making deep integration a key buyer requirement that raises switching costs and reduces customer bargaining power. Equals should prioritize expanding connectors and developer sandboxes to lock in workflows and accelerate adoption. Embedded finance partnerships further entrench usage by embedding payments and treasury services into client systems.

- ERP plugins

- APIs & sandbox tooling

- Bulk payments

- Embedded finance

Sell speed and SLA resilience as FX transparency and fintech pricing squeeze margins

High price transparency (FX vol $7.5T avg daily, BIS 2022) and intensified fintech pricing in 2024 compress margins; Equals must sell speed, net landed cost and service not just price. Rapid multi‑homing and low onboarding frictions raise customer leverage; deep integrations, balances and APIs increase stickiness. Corporate RFPs push 5–20% corridor discounts; premium SLAs and tooling monetize resilience.

| Metric | 2024/Source |

|---|---|

| FX turnover | $7.5T avg/day (BIS 2022) |

| SLA benchmarks | 99.99% / 99.999% |

| Settlement | T+0–T+2 |

| RFP corridor impact | 5–20% margin trade |

What You See Is What You Get

Equals Group Porter's Five Forces Analysis

This Porter’s Five Forces analysis for Equals Group is the full, professionally formatted document you see in preview—covering competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. After purchase you’ll receive this exact file instantly, ready for use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Equals Group faces moderate buyer power, niche supplier leverage, rising fintech entrants, and growing substitute channels that intensify rivalry—creating both pressure and opportunity for strategic differentiation. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Equals Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on FX liquidity providers

Equals relies on banks and market-makers for wholesale FX rates and liquidity, concentrating supplier influence and creating exposure when counterparties retract. In volatile sessions spreads and execution costs can widen materially, increasing Equals’ cost of goods sold. Diversified liquidity pools and smart routing mitigate but do not eliminate this dependency. Long-term partnerships and volume commitments support negotiation for tighter pricing.

Card schemes and payment networks

Visa and Mastercard together process over 80% of global card transactions, making scheme fees and network rules effectively non-negotiable cost floors for Equals; in the EU caps on interchange under IFR remain 0.2% for debit and 0.3% for credit (Regulation 2015/751).

Changes to scheme rules or fee schedules and compliance mandates (e.g., 3D Secure, PSD2 updates) can compress margins quickly as these costs are largely passthrough.

Scale enables better pricing tiers and volume rebates from schemes, but bargaining power remains skewed to schemes; multi-network connectivity (Visa, Mastercard, alternative networks) reduces single-network dependency risk.

Banking partners and correspondent rails

Equals relies on sponsor banks for safeguarding, settlement and corridor access; global correspondent banking relationships have declined roughly 15% since 2011 (World Bank), raising disruption risk from de-risking or exits. A multi-bank model across regions and firm service-level agreements provide redundancy, reducing single-point failures and lowering operational leverage of any one partner.

Regtech, data, and cloud vendors

Sanctions screening, KYC, and cloud infrastructure are mission-critical for Equals Group, creating high switching frictions that let vendors raise prices or alter terms; top three cloud providers held over 60% market share in 2024, concentrating supplier power. Contract diversification and modular architectures reduce lock-in, while volume-based discounts improve unit economics as transaction volumes scale.

- Sanctions/KYC: high switching friction

- Cloud concentration: top 3 >60% (2024)

- Mitigation: contract diversification, modular stacks

- Benefit: volume discounts lower marginal costs

FX and payments infrastructure APIs

Gateway, gateway-to-rails and treasury APIs determine Equals Group’s throughput costs and settlement speed; in 2024 API-driven routing reportedly supported a 35% uplift in transaction efficiency industry-wide, making proprietary features a lock-in risk that raises supplier power. Open standards and internal orchestration reduce dependence, while homegrown components in core pathways further weaken supplier leverage.

- API routing: improves throughput, ups vendor importance

- Proprietary features: increase switching costs

- Open standards/orchestration: strengthen negotiating leverage

- Homegrown core: lowers supplier power

Supplier concentration raises costs and frictions; multi-bank, multi-network stacks reduce them

Suppliers exert high leverage: wholesale FX banks/market-makers concentrate liquidity, Visa/Mastercard process >80% of card volume, and top-3 cloud providers held >60% share in 2024, while correspondent banking has fallen ~15% since 2011. These factors raise cost and switching friction; Equals mitigates via multi-bank, multi-network, modular stack and volume-based deals.

| Metric | Value |

|---|---|

| Card networks share | >80% |

| Top-3 cloud (2024) | >60% |

| Corr. banking decline | ~15% since 2011 |

| API efficiency (2024) | +35% |

What is included in the product

Tailored Porter's Five Forces analysis for Equals Group, uncovering key drivers of competition, buyer/supplier power, entry barriers and substitutes while identifying disruptive threats and strategic levers to protect market position.

Clear one-sheet Porter's Five Forces for Equals Group—instantly visualized with a spider chart and editable pressure levels to simplify strategic choices and relieve analysis bottlenecks.

Customers Bargaining Power

High price transparency

High price transparency lets SMEs and consumers compare FX spreads and fees instantly, compressing margins in a market with $7.5 trillion average daily FX turnover (BIS triennial 2022) and intensified fintech price competition by 2024. Equals must emphasize net landed cost, speed and service to avoid pure price battles. Dynamic pricing and tiered plans help defend margins while retaining volume-sensitive clients.

Low switching costs, multi-homing

By 2024 customers commonly multi-home across payment providers, and digital onboarding has materially lowered exit frictions, enabling rapid switches. Equals must increase stickiness via deep integrations, holding customer balances and embedding workflows to raise switching costs. Loyalty incentives and bundled features can reduce churn and protect margins in a low-switching-cost market.

Corporate RFP and volume leverage

Larger SMEs and mid-market firms increasingly use corporate RFPs in 2024 to pressure pricing and SLAs, forcing Equals to defend spreads and delivery windows. Volume tiers and corridor commitments commonly trade 5–20% margin for share in FX corridors, intensifying customer bargaining. Equals offsets pressure with value-added hedging, automated reconciliation and premium support. Data-driven pricing and unit-economics dashboards preserve margin visibility.

Service reliability and SLA sensitivity

Customers punish downtime with rapid switching; fintech SLAs of 99.99% (≈52.6 minutes annual downtime) versus 99.999% (≈5.26 minutes) are meaningful benchmarks, and clients demand 24/7 support plus predictable settlement windows (T+0 to T+2 common). Investing in resilience, realtime incident transparency and redundant infrastructure reduces perceived risk and churn. Premium support tiers allow direct monetization of higher-availability promises.

- High SLA benchmark: 99.99% ≈52.6 min/yr

- Higher tier: 99.999% ≈5.26 min/yr

- Settlement sensitivity: T+0–T+2

- 24/7 support expected

Integration and workflow expectations

Clients increasingly demand ERP and accounting plugins, robust APIs, sandbox tooling, and bulk payments, making deep integration a key buyer requirement that raises switching costs and reduces customer bargaining power. Equals should prioritize expanding connectors and developer sandboxes to lock in workflows and accelerate adoption. Embedded finance partnerships further entrench usage by embedding payments and treasury services into client systems.

- ERP plugins

- APIs & sandbox tooling

- Bulk payments

- Embedded finance

Sell speed and SLA resilience as FX transparency and fintech pricing squeeze margins

High price transparency (FX vol $7.5T avg daily, BIS 2022) and intensified fintech pricing in 2024 compress margins; Equals must sell speed, net landed cost and service not just price. Rapid multi‑homing and low onboarding frictions raise customer leverage; deep integrations, balances and APIs increase stickiness. Corporate RFPs push 5–20% corridor discounts; premium SLAs and tooling monetize resilience.

| Metric | 2024/Source |

|---|---|

| FX turnover | $7.5T avg/day (BIS 2022) |

| SLA benchmarks | 99.99% / 99.999% |

| Settlement | T+0–T+2 |

| RFP corridor impact | 5–20% margin trade |

What You See Is What You Get

Equals Group Porter's Five Forces Analysis

This Porter’s Five Forces analysis for Equals Group is the full, professionally formatted document you see in preview—covering competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. After purchase you’ll receive this exact file instantly, ready for use.