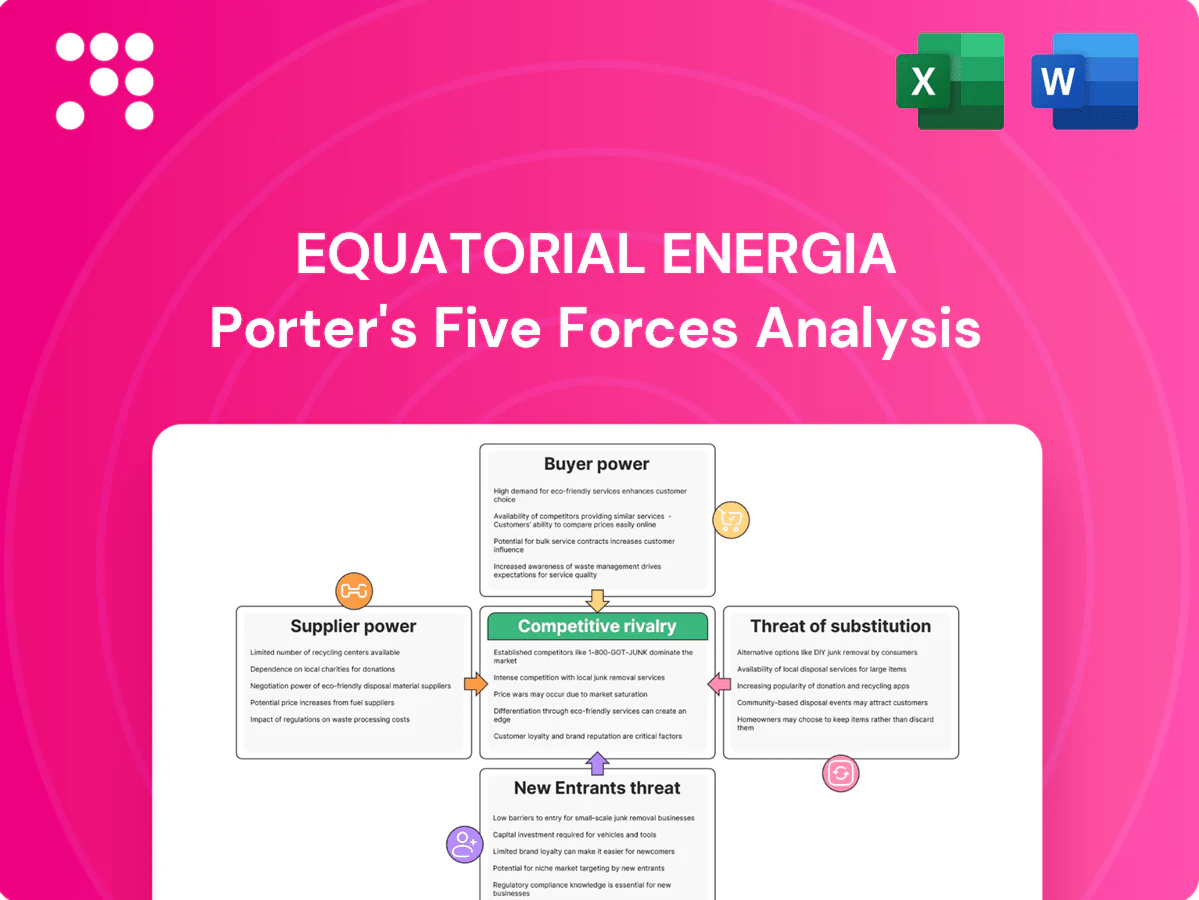

Equatorial Energia Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Equatorial Energia operates in a capital-intensive, regulated market where supplier leverage, regulatory shifts, and rival pricing tightly shape margins; our snapshot highlights these pressures and emerging risks. The analysis flags moderate buyer power, limited substitutes, and entry barriers that protect incumbents but invite efficiency-driven competition. Curious how each force quantitatively impacts valuation and strategy? Unlock the full Porter's Five Forces Analysis for a force-by-force breakdown, visuals, and actionable recommendations.

Suppliers Bargaining Power

Supplier Power 1

Equipment OEM concentration for transformers, meters and cables gives suppliers pricing and spec leverage; global transformer lead times, which rose to 30+ weeks in 2021–22, remained elevated into 2024, tightening availability and lifting input costs.

Equatorial limits exposure through multi-year framework agreements and diversified sourcing across domestic and international vendors, but critical items remain semi-commoditized with measurable quality differentials.

Brazilian localization rules and conformity testing further narrow supplier choice and can add 10–20% to lead times and compliance costs for imported equipment.

Supplier Power 2

During 2024 peak capex cycles, specialist EPC firms for grid expansion exert notable leverage over Equatorial Energia as qualified bidders often number fewer than 8, raising switching costs mid-project and complicating permitting; performance bonds mitigate some risk, but schedule slippage can still transfer cost overruns to Equatorial (often 5–10% of project value). Regional labor shortages and union negotiations in the Northeast raise wage and schedule pressure, further strengthening supplier power.

Supplier Power 3

Fuel and generation input costs matter for thermal plants though Equatorial focuses on distribution/transmission, with limited merchant exposure. Hydrology-driven reservoir levels and spot PLD volatility feed through to purchased energy costs under regulated pass-throughs. Contracted PPAs mitigate price swings but counterparty risk and Brazil’s distribution losses (~12% per ANEEL 2024) plus procurement rules limit sourcing flexibility.

Supplier Power 4

Digital/OT vendors for SCADA, smart meters and cybersecurity exert high bargaining power over Equatorial Energia via proprietary platforms and integration lock-in; switching core systems is costly and risks worsening SAIDI/SAIFI reliability metrics. Long vendor support cycles bind Equatorial to vendor roadmaps and pricing, while adoption of IEC 61850 and interoperability efforts partially reduce dependence.

- Vendor lock-in: proprietary stacks

- Switching risk: impacts SAIDI/SAIFI

- Long support cycles: roadmap dependency

- Mitigant: IEC 61850 interoperability

Supplier Power 5

Capital providers (banks, debentures, BNDES) strongly shape terms for Equatorial’s multi-decade assets; 2024 financing conditions (Selic average ~12.75% and Brazil EMBI ~320 bps) pushed WACC and auction bids higher. Covenant frameworks in project debt constrain capex timing and dividend distribution, while improved credit metrics and clearer ANEEL regulation in 2024 moderated lender leverage.

30+ wk lead times, +10-20% localization, Selic ~12.75% pressure on capex

Supplier power is moderate-high: concentrated OEMs and specialist EPCs limit competition and raised lead times (30+ weeks 2021–22, still elevated into 2024). Regulation and localization add 10–20% time/cost; digital vendors create lock-in and switching risk. Financing pressure (Selic ~12.75% 2024) increases capex sensitivity.

| Metric | 2024 |

|---|---|

| Transformer lead time | 30+ wks |

| Localization delay/cost | +10–20% |

| Selic | ~12.75% |

What is included in the product

Tailored Porter’s Five Forces assessment of Equatorial Energia, revealing competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and regulatory risks shaping its profitability and strategic positioning.

A concise one-sheet Porter's Five Forces for Equatorial Energia—customizable pressure levels and spider-chart visualization that instantly reveals regulatory and competitive pain points, ready to drop into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Buyer Power 1

Residential and small commercial customers in Equatorial’s concession areas are effectively captive, with low switching ability because distribution is concession-based and tariffs are set by ANEEL. ANEEL fixes tariffs and enforces quality via DEC/FEC targets and fines, limiting Equatorial’s room for direct price negotiation. High customer complaint volumes and political scrutiny over outages and bills increase exposure to penalties and reputational risk.

Buyer Power 2

Large industrials and free-market (ACL) customers wield significant bargaining power, sourcing supply via bilateral contracts and the CCEE spot market and leveraging competition among generators/retailers to push down margins; Equatorial faces compressed retail spreads as portfolio diversification and new retail entrants increase price pressure, making reliability and tailored solutions the key differentiator for retaining high-volume ACL clients.

Buyer Power 3

Distributed generation, especially rooftop solar, gives consumers partial bypass; Brazil reached about 19.5 GW of distributed generation and roughly 1.8 million consumer systems by 2024, keeping buyer leverage high. Net metering reforms reduced but did not remove self-generation incentives, and payback periods have stretched to roughly 6–12 years, moderating churn while high-tariff areas remain vulnerable. Equatorial can mitigate risk by offering grid services and time-of-use tariffs.

Buyer Power 4

Public-sector and large municipal accounts exert high leverage over Equatorial Energia, with 2024 municipal contracts accounting for roughly 25% of regional demand in served areas, enabling stricter service-level and reliability clauses. Payment risk and political cycles raise negotiation pressure on debt restructuring and receivables: delayed municipal payments climbed in 2024 by about 8% year-on-year, increasing exposure. The visibility of essential services amplifies reputational stakes, so tailored billing and reliability programs (pilot loyalty tariffs rolled out to 120,000 clients in 2024) help lock in long-term customer loyalty.

- Scale leverage: municipal accounts ~25% of demand

- Payment risk: delayed municipal payments +8% YoY (2024)

- Reputation: essential-service scrutiny

- Retention tactics: 120,000 clients on loyalty/reliability pilots (2024)

Buyer Power 5

Commercial clients increasingly demand bundled offers (efficiency, storage, demand response) from Equatorial Energia as integrated solutions drive retention.

Growing numbers of alternative ESCOs expand choice and pressure margins, while Brazil's internet penetration (~82% in 2024) and digital interfaces make switching easier.

Value-added services (analytics, demand response) can offset pure price sensitivity and protect ARPU.

- Bundled solutions expected

- More ESCOs = higher choice

- 82% internet penetration raises switching ease

- Value-added services reduce price pressure

Municipal 25% demand, +8% delays raise negotiation risk

Residential customers captive under ANEEL limits price bargaining; municipal accounts ~25% demand with delayed payments +8% YoY (2024) raising negotiation risk. Large industrial/ACL buyers and 19.5 GW/1.8M distributed generation (2024) boost buyer power; value-added services and 120,000 loyalty pilots help retain high-value clients.

| Metric | 2024 |

|---|---|

| Municipal demand share | ~25% |

| Delayed municipal payments | +8% YoY |

| Distributed generation capacity | 19.5 GW |

| Distributed systems | ~1.8M |

| Internet penetration | 82% |

| Loyalty pilot clients | 120,000 |

What You See Is What You Get

Equatorial Energia Porter's Five Forces Analysis

This preview shows the exact Equatorial Energia Porter’s Five Forces analysis you’ll receive after purchase—no mockups, no placeholders. The file is fully formatted, ready to download, and contains the same comprehensive competitive assessment displayed here. Buy once for instant access to this final deliverable.

A Must-Have Tool for Decision-Makers

Equatorial Energia operates in a capital-intensive, regulated market where supplier leverage, regulatory shifts, and rival pricing tightly shape margins; our snapshot highlights these pressures and emerging risks. The analysis flags moderate buyer power, limited substitutes, and entry barriers that protect incumbents but invite efficiency-driven competition. Curious how each force quantitatively impacts valuation and strategy? Unlock the full Porter's Five Forces Analysis for a force-by-force breakdown, visuals, and actionable recommendations.

Suppliers Bargaining Power

Supplier Power 1

Equipment OEM concentration for transformers, meters and cables gives suppliers pricing and spec leverage; global transformer lead times, which rose to 30+ weeks in 2021–22, remained elevated into 2024, tightening availability and lifting input costs.

Equatorial limits exposure through multi-year framework agreements and diversified sourcing across domestic and international vendors, but critical items remain semi-commoditized with measurable quality differentials.

Brazilian localization rules and conformity testing further narrow supplier choice and can add 10–20% to lead times and compliance costs for imported equipment.

Supplier Power 2

During 2024 peak capex cycles, specialist EPC firms for grid expansion exert notable leverage over Equatorial Energia as qualified bidders often number fewer than 8, raising switching costs mid-project and complicating permitting; performance bonds mitigate some risk, but schedule slippage can still transfer cost overruns to Equatorial (often 5–10% of project value). Regional labor shortages and union negotiations in the Northeast raise wage and schedule pressure, further strengthening supplier power.

Supplier Power 3

Fuel and generation input costs matter for thermal plants though Equatorial focuses on distribution/transmission, with limited merchant exposure. Hydrology-driven reservoir levels and spot PLD volatility feed through to purchased energy costs under regulated pass-throughs. Contracted PPAs mitigate price swings but counterparty risk and Brazil’s distribution losses (~12% per ANEEL 2024) plus procurement rules limit sourcing flexibility.

Supplier Power 4

Digital/OT vendors for SCADA, smart meters and cybersecurity exert high bargaining power over Equatorial Energia via proprietary platforms and integration lock-in; switching core systems is costly and risks worsening SAIDI/SAIFI reliability metrics. Long vendor support cycles bind Equatorial to vendor roadmaps and pricing, while adoption of IEC 61850 and interoperability efforts partially reduce dependence.

- Vendor lock-in: proprietary stacks

- Switching risk: impacts SAIDI/SAIFI

- Long support cycles: roadmap dependency

- Mitigant: IEC 61850 interoperability

Supplier Power 5

Capital providers (banks, debentures, BNDES) strongly shape terms for Equatorial’s multi-decade assets; 2024 financing conditions (Selic average ~12.75% and Brazil EMBI ~320 bps) pushed WACC and auction bids higher. Covenant frameworks in project debt constrain capex timing and dividend distribution, while improved credit metrics and clearer ANEEL regulation in 2024 moderated lender leverage.

30+ wk lead times, +10-20% localization, Selic ~12.75% pressure on capex

Supplier power is moderate-high: concentrated OEMs and specialist EPCs limit competition and raised lead times (30+ weeks 2021–22, still elevated into 2024). Regulation and localization add 10–20% time/cost; digital vendors create lock-in and switching risk. Financing pressure (Selic ~12.75% 2024) increases capex sensitivity.

| Metric | 2024 |

|---|---|

| Transformer lead time | 30+ wks |

| Localization delay/cost | +10–20% |

| Selic | ~12.75% |

What is included in the product

Tailored Porter’s Five Forces assessment of Equatorial Energia, revealing competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and regulatory risks shaping its profitability and strategic positioning.

A concise one-sheet Porter's Five Forces for Equatorial Energia—customizable pressure levels and spider-chart visualization that instantly reveals regulatory and competitive pain points, ready to drop into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Buyer Power 1

Residential and small commercial customers in Equatorial’s concession areas are effectively captive, with low switching ability because distribution is concession-based and tariffs are set by ANEEL. ANEEL fixes tariffs and enforces quality via DEC/FEC targets and fines, limiting Equatorial’s room for direct price negotiation. High customer complaint volumes and political scrutiny over outages and bills increase exposure to penalties and reputational risk.

Buyer Power 2

Large industrials and free-market (ACL) customers wield significant bargaining power, sourcing supply via bilateral contracts and the CCEE spot market and leveraging competition among generators/retailers to push down margins; Equatorial faces compressed retail spreads as portfolio diversification and new retail entrants increase price pressure, making reliability and tailored solutions the key differentiator for retaining high-volume ACL clients.

Buyer Power 3

Distributed generation, especially rooftop solar, gives consumers partial bypass; Brazil reached about 19.5 GW of distributed generation and roughly 1.8 million consumer systems by 2024, keeping buyer leverage high. Net metering reforms reduced but did not remove self-generation incentives, and payback periods have stretched to roughly 6–12 years, moderating churn while high-tariff areas remain vulnerable. Equatorial can mitigate risk by offering grid services and time-of-use tariffs.

Buyer Power 4

Public-sector and large municipal accounts exert high leverage over Equatorial Energia, with 2024 municipal contracts accounting for roughly 25% of regional demand in served areas, enabling stricter service-level and reliability clauses. Payment risk and political cycles raise negotiation pressure on debt restructuring and receivables: delayed municipal payments climbed in 2024 by about 8% year-on-year, increasing exposure. The visibility of essential services amplifies reputational stakes, so tailored billing and reliability programs (pilot loyalty tariffs rolled out to 120,000 clients in 2024) help lock in long-term customer loyalty.

- Scale leverage: municipal accounts ~25% of demand

- Payment risk: delayed municipal payments +8% YoY (2024)

- Reputation: essential-service scrutiny

- Retention tactics: 120,000 clients on loyalty/reliability pilots (2024)

Buyer Power 5

Commercial clients increasingly demand bundled offers (efficiency, storage, demand response) from Equatorial Energia as integrated solutions drive retention.

Growing numbers of alternative ESCOs expand choice and pressure margins, while Brazil's internet penetration (~82% in 2024) and digital interfaces make switching easier.

Value-added services (analytics, demand response) can offset pure price sensitivity and protect ARPU.

- Bundled solutions expected

- More ESCOs = higher choice

- 82% internet penetration raises switching ease

- Value-added services reduce price pressure

Municipal 25% demand, +8% delays raise negotiation risk

Residential customers captive under ANEEL limits price bargaining; municipal accounts ~25% demand with delayed payments +8% YoY (2024) raising negotiation risk. Large industrial/ACL buyers and 19.5 GW/1.8M distributed generation (2024) boost buyer power; value-added services and 120,000 loyalty pilots help retain high-value clients.

| Metric | 2024 |

|---|---|

| Municipal demand share | ~25% |

| Delayed municipal payments | +8% YoY |

| Distributed generation capacity | 19.5 GW |

| Distributed systems | ~1.8M |

| Internet penetration | 82% |

| Loyalty pilot clients | 120,000 |

What You See Is What You Get

Equatorial Energia Porter's Five Forces Analysis

This preview shows the exact Equatorial Energia Porter’s Five Forces analysis you’ll receive after purchase—no mockups, no placeholders. The file is fully formatted, ready to download, and contains the same comprehensive competitive assessment displayed here. Buy once for instant access to this final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Equatorial Energia operates in a capital-intensive, regulated market where supplier leverage, regulatory shifts, and rival pricing tightly shape margins; our snapshot highlights these pressures and emerging risks. The analysis flags moderate buyer power, limited substitutes, and entry barriers that protect incumbents but invite efficiency-driven competition. Curious how each force quantitatively impacts valuation and strategy? Unlock the full Porter's Five Forces Analysis for a force-by-force breakdown, visuals, and actionable recommendations.

Suppliers Bargaining Power

Supplier Power 1

Equipment OEM concentration for transformers, meters and cables gives suppliers pricing and spec leverage; global transformer lead times, which rose to 30+ weeks in 2021–22, remained elevated into 2024, tightening availability and lifting input costs.

Equatorial limits exposure through multi-year framework agreements and diversified sourcing across domestic and international vendors, but critical items remain semi-commoditized with measurable quality differentials.

Brazilian localization rules and conformity testing further narrow supplier choice and can add 10–20% to lead times and compliance costs for imported equipment.

Supplier Power 2

During 2024 peak capex cycles, specialist EPC firms for grid expansion exert notable leverage over Equatorial Energia as qualified bidders often number fewer than 8, raising switching costs mid-project and complicating permitting; performance bonds mitigate some risk, but schedule slippage can still transfer cost overruns to Equatorial (often 5–10% of project value). Regional labor shortages and union negotiations in the Northeast raise wage and schedule pressure, further strengthening supplier power.

Supplier Power 3

Fuel and generation input costs matter for thermal plants though Equatorial focuses on distribution/transmission, with limited merchant exposure. Hydrology-driven reservoir levels and spot PLD volatility feed through to purchased energy costs under regulated pass-throughs. Contracted PPAs mitigate price swings but counterparty risk and Brazil’s distribution losses (~12% per ANEEL 2024) plus procurement rules limit sourcing flexibility.

Supplier Power 4

Digital/OT vendors for SCADA, smart meters and cybersecurity exert high bargaining power over Equatorial Energia via proprietary platforms and integration lock-in; switching core systems is costly and risks worsening SAIDI/SAIFI reliability metrics. Long vendor support cycles bind Equatorial to vendor roadmaps and pricing, while adoption of IEC 61850 and interoperability efforts partially reduce dependence.

- Vendor lock-in: proprietary stacks

- Switching risk: impacts SAIDI/SAIFI

- Long support cycles: roadmap dependency

- Mitigant: IEC 61850 interoperability

Supplier Power 5

Capital providers (banks, debentures, BNDES) strongly shape terms for Equatorial’s multi-decade assets; 2024 financing conditions (Selic average ~12.75% and Brazil EMBI ~320 bps) pushed WACC and auction bids higher. Covenant frameworks in project debt constrain capex timing and dividend distribution, while improved credit metrics and clearer ANEEL regulation in 2024 moderated lender leverage.

30+ wk lead times, +10-20% localization, Selic ~12.75% pressure on capex

Supplier power is moderate-high: concentrated OEMs and specialist EPCs limit competition and raised lead times (30+ weeks 2021–22, still elevated into 2024). Regulation and localization add 10–20% time/cost; digital vendors create lock-in and switching risk. Financing pressure (Selic ~12.75% 2024) increases capex sensitivity.

| Metric | 2024 |

|---|---|

| Transformer lead time | 30+ wks |

| Localization delay/cost | +10–20% |

| Selic | ~12.75% |

What is included in the product

Tailored Porter’s Five Forces assessment of Equatorial Energia, revealing competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and regulatory risks shaping its profitability and strategic positioning.

A concise one-sheet Porter's Five Forces for Equatorial Energia—customizable pressure levels and spider-chart visualization that instantly reveals regulatory and competitive pain points, ready to drop into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Buyer Power 1

Residential and small commercial customers in Equatorial’s concession areas are effectively captive, with low switching ability because distribution is concession-based and tariffs are set by ANEEL. ANEEL fixes tariffs and enforces quality via DEC/FEC targets and fines, limiting Equatorial’s room for direct price negotiation. High customer complaint volumes and political scrutiny over outages and bills increase exposure to penalties and reputational risk.

Buyer Power 2

Large industrials and free-market (ACL) customers wield significant bargaining power, sourcing supply via bilateral contracts and the CCEE spot market and leveraging competition among generators/retailers to push down margins; Equatorial faces compressed retail spreads as portfolio diversification and new retail entrants increase price pressure, making reliability and tailored solutions the key differentiator for retaining high-volume ACL clients.

Buyer Power 3

Distributed generation, especially rooftop solar, gives consumers partial bypass; Brazil reached about 19.5 GW of distributed generation and roughly 1.8 million consumer systems by 2024, keeping buyer leverage high. Net metering reforms reduced but did not remove self-generation incentives, and payback periods have stretched to roughly 6–12 years, moderating churn while high-tariff areas remain vulnerable. Equatorial can mitigate risk by offering grid services and time-of-use tariffs.

Buyer Power 4

Public-sector and large municipal accounts exert high leverage over Equatorial Energia, with 2024 municipal contracts accounting for roughly 25% of regional demand in served areas, enabling stricter service-level and reliability clauses. Payment risk and political cycles raise negotiation pressure on debt restructuring and receivables: delayed municipal payments climbed in 2024 by about 8% year-on-year, increasing exposure. The visibility of essential services amplifies reputational stakes, so tailored billing and reliability programs (pilot loyalty tariffs rolled out to 120,000 clients in 2024) help lock in long-term customer loyalty.

- Scale leverage: municipal accounts ~25% of demand

- Payment risk: delayed municipal payments +8% YoY (2024)

- Reputation: essential-service scrutiny

- Retention tactics: 120,000 clients on loyalty/reliability pilots (2024)

Buyer Power 5

Commercial clients increasingly demand bundled offers (efficiency, storage, demand response) from Equatorial Energia as integrated solutions drive retention.

Growing numbers of alternative ESCOs expand choice and pressure margins, while Brazil's internet penetration (~82% in 2024) and digital interfaces make switching easier.

Value-added services (analytics, demand response) can offset pure price sensitivity and protect ARPU.

- Bundled solutions expected

- More ESCOs = higher choice

- 82% internet penetration raises switching ease

- Value-added services reduce price pressure

Municipal 25% demand, +8% delays raise negotiation risk

Residential customers captive under ANEEL limits price bargaining; municipal accounts ~25% demand with delayed payments +8% YoY (2024) raising negotiation risk. Large industrial/ACL buyers and 19.5 GW/1.8M distributed generation (2024) boost buyer power; value-added services and 120,000 loyalty pilots help retain high-value clients.

| Metric | 2024 |

|---|---|

| Municipal demand share | ~25% |

| Delayed municipal payments | +8% YoY |

| Distributed generation capacity | 19.5 GW |

| Distributed systems | ~1.8M |

| Internet penetration | 82% |

| Loyalty pilot clients | 120,000 |

What You See Is What You Get

Equatorial Energia Porter's Five Forces Analysis

This preview shows the exact Equatorial Energia Porter’s Five Forces analysis you’ll receive after purchase—no mockups, no placeholders. The file is fully formatted, ready to download, and contains the same comprehensive competitive assessment displayed here. Buy once for instant access to this final deliverable.