Equifax Porter's Five Forces Analysis

From Overview to Strategy Blueprint

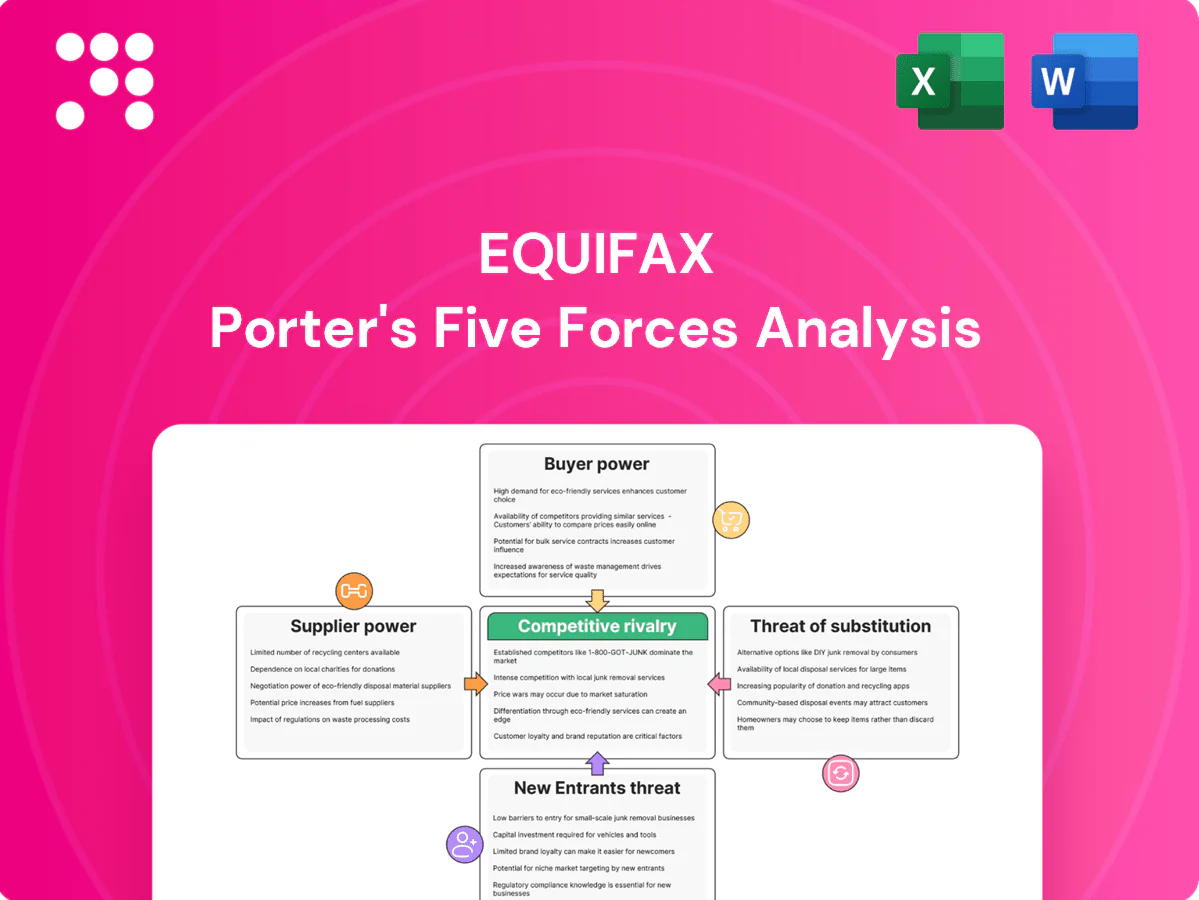

Equifax faces intense competitive rivalry from credit bureaus and fintechs, moderate buyer power from large enterprise clients, low supplier power, and persistent threats from new entrants and substitutes driven by alternative data and analytics. This snapshot highlights strategic pressure points—unlock the full Porter's Five Forces Analysis to access detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Critical data furnishers

Equifax depends on banks, lenders, card issuers and collections agencies to furnish tradeline data, and as of 2024 these furnishers still require bureau coverage to manage credit risk, which limits their bargaining power. Unique portfolios or temporary pullbacks in reporting can reduce data breadth and freshness, creating pressure on Equifax’s analytics. Strict data quality rules and furnishers’ compliance investments raise switching costs and influence negotiating leverage.

Public and alternative data

Government records, utilities, telcos, payroll aggregators and other alternative data expand Equifax’s coverage and product features, with many public-record feeds commoditized while exclusive alt-data can command premiums. Access and usage are tightly constrained by FCRA in the US and GDPR/CCPA frameworks as of 2024, limiting portability and consent. Supplier concentration in niche datasets increases switching costs and pricing power for scarce feeds.

Cloud and analytics stack

Equifax relies on cloud infrastructure, data platforms and analytics tooling to process data at scale, exposing it to supplier leverage from major hyperscalers: 2024 market shares were roughly AWS 32%, Microsoft Azure 23% and Google Cloud 11% (Synergy Research). Multicloud deployments and long-term contracts partially mitigate price and egress fee risks, while performance, security SLAs and SOC/ISO certifications materially shape supplier power.

Identity and fraud tech vendors

Identity and fraud tech vendors supply device intelligence, document verification, and signal feeds that underpin Equifax fraud solutions; the global identity verification market was about 16 billion USD in 2024 and top providers control roughly 30 percent share, giving specialized vendors with proprietary graphs pricing power.

- 2024 market size ~16B USD

- Leading vendors ~30% market share

- Bundled contracts and Equifax in‑house models reduce dependency

- API standards and interoperability lower switching frictions

Cybersecurity and compliance services

Given regulatory exposure, security tooling and audits are mission-critical for Equifax after the 2017 breach that exposed 147 million consumers. Best-in-class vendors are hard to replace without risk; Equifax’s consumer settlement of up to 700 million USD elevated scrutiny and increases reliance on premium solutions. Diversified internal controls and multi-vendor strategies offset single-vendor bargaining power.

- Supplier risk: high

- Settlement impact: 700M USD

- Vendor dependency: mitigated by diversification

Moderate vendor power: hyperscalers, identity vendors hold pricing clout; regs raise switching costs

Supplier power moderate: core tradeline furnishers need credit bureaus, limiting leverage, but niche alternative-data and identity vendors plus hyperscalers have pricing power. Regulatory constraints (FCRA, GDPR/CCPA) and high security costs raise switching costs. Diversified vendors, in‑house models and multicloud reduce single-supplier dependence.

| Item | 2024 metric | Impact |

|---|---|---|

| Tradeline furnishers | High dependence | Low-moderate power |

| Hyperscalers | AWS 32%/Azure 23%/GCP 11% | Moderate power |

| Identity market | 16B USD; top vendors ~30% | High in niche |

| Regulatory cost | Settlement 700M USD | Raises switching cost |

What is included in the product

Tailored Porter's Five Forces analysis for Equifax assessing competitive rivalry, buyer and supplier power, barriers to entry, and substitution risks—highlighting data security, regulatory pressure, and fintech disruption as key forces shaping profitability.

A concise, one-sheet Porter's Five Forces for Equifax—instantly highlighting competitive intensity, regulatory and data-security risks, and supplier/customer bargaining power to speed strategic decision-making and boardroom discussions.

Customers Bargaining Power

Large financial institutions

Major banks, lenders and insurers routinely dual- or tri-source credit data with Experian and TransUnion, giving them outsized negotiating leverage over Equifax through high-volume RFPs and consolidated purchasing. Their ability to reallocate pull volumes to rivals pressures Equifax on price and contract terms. Custom integrations and proven model performance, however, raise short-term switching costs and preserve some supplier power for Equifax.

Fintechs and digital lenders

High-growth fintechs and digital lenders are highly price-sensitive and agile in vendor selection, increasingly evaluating alternative data and cash-flow underwriting as of 2024 to broaden options and reduce reliance on legacy bureaus; trials and usage-based pricing models amplify their bargaining power by lowering switching costs and enabling rapid proof-of-concept adoption, yet regulatory acceptance in 2024 continues to favor traditional bureau data in many compliance-driven workflows.

Enterprises in telecom and utilities

Enterprises in telecom and utilities wield strong bargaining power with Equifax by negotiating large-scale bundles across verification, identity, and skip-trace solutions, leveraging volume commitments and multi-product procurement to drive discounts. Multi-year contracts create customer stickiness but shift leverage to buyers at renewal, where aggregated usage and renewal timing become key negotiation points. Service-level requirements, especially latency and uptime, are critical levers—enterprises routinely demand strict SLAs and penalties that shape pricing and deployment priorities.

Government and employers

- Procurement focus: compliance over price

- Financial impact: customizations raise deal costs

- Cycle effect: fewer switches, higher evaluation rigor

Consumers and small businesses

Consumers and small businesses have low per‑unit leverage but can switch among the three major national credit bureaus and numerous fintech apps; the FCRA grants dispute rights and free annual reports, limiting monetization. Brand trust and UX drive retention more than lock‑in; price promotions and bundling (common in 2024 digital offers) increase demand elasticity.

- Three major bureaus limit individual bargaining power

- FCRA: dispute rights + free annual reports

- UX, trust, promotions shape retention and elasticity

High-leverage buyers squeeze data providers; fintech alt-data raises 2024 switching risk

Major banks and insurers wield high leverage via multi-vendor sourcing and volume RFPs, forcing price and term concessions. Fintechs are price-sensitive and increasing alternative-data trials in 2024, raising switching risk despite regulatory reliance on bureau data. Enterprises and governments negotiate bundles and strict SLAs, compressing margins; Equifax reported ~$4.4B revenue in 2024 with ~15% enterprise margin pressure. Consumers have low per-unit leverage; FCRA limits monetization.

| Customer Segment | Leverage | 2024 Metric |

|---|---|---|

| Banks/Lenders | High | Dual/tri-sourcing, strong price pressure |

| Fintechs | Medium-High | Alt-data trials ↑ in 2024 |

| Enterprises/Govt | High | 15% margin pressure |

| Consumers/SMBs | Low | FCRA protections, free reports |

Preview Before You Purchase

Equifax Porter's Five Forces Analysis

This preview shows the exact Equifax Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The report covers competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and regulatory/contextual considerations, fully formatted and ready to download. Purchase grants instant access to this identical, final document.

From Overview to Strategy Blueprint

Equifax faces intense competitive rivalry from credit bureaus and fintechs, moderate buyer power from large enterprise clients, low supplier power, and persistent threats from new entrants and substitutes driven by alternative data and analytics. This snapshot highlights strategic pressure points—unlock the full Porter's Five Forces Analysis to access detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Critical data furnishers

Equifax depends on banks, lenders, card issuers and collections agencies to furnish tradeline data, and as of 2024 these furnishers still require bureau coverage to manage credit risk, which limits their bargaining power. Unique portfolios or temporary pullbacks in reporting can reduce data breadth and freshness, creating pressure on Equifax’s analytics. Strict data quality rules and furnishers’ compliance investments raise switching costs and influence negotiating leverage.

Public and alternative data

Government records, utilities, telcos, payroll aggregators and other alternative data expand Equifax’s coverage and product features, with many public-record feeds commoditized while exclusive alt-data can command premiums. Access and usage are tightly constrained by FCRA in the US and GDPR/CCPA frameworks as of 2024, limiting portability and consent. Supplier concentration in niche datasets increases switching costs and pricing power for scarce feeds.

Cloud and analytics stack

Equifax relies on cloud infrastructure, data platforms and analytics tooling to process data at scale, exposing it to supplier leverage from major hyperscalers: 2024 market shares were roughly AWS 32%, Microsoft Azure 23% and Google Cloud 11% (Synergy Research). Multicloud deployments and long-term contracts partially mitigate price and egress fee risks, while performance, security SLAs and SOC/ISO certifications materially shape supplier power.

Identity and fraud tech vendors

Identity and fraud tech vendors supply device intelligence, document verification, and signal feeds that underpin Equifax fraud solutions; the global identity verification market was about 16 billion USD in 2024 and top providers control roughly 30 percent share, giving specialized vendors with proprietary graphs pricing power.

- 2024 market size ~16B USD

- Leading vendors ~30% market share

- Bundled contracts and Equifax in‑house models reduce dependency

- API standards and interoperability lower switching frictions

Cybersecurity and compliance services

Given regulatory exposure, security tooling and audits are mission-critical for Equifax after the 2017 breach that exposed 147 million consumers. Best-in-class vendors are hard to replace without risk; Equifax’s consumer settlement of up to 700 million USD elevated scrutiny and increases reliance on premium solutions. Diversified internal controls and multi-vendor strategies offset single-vendor bargaining power.

- Supplier risk: high

- Settlement impact: 700M USD

- Vendor dependency: mitigated by diversification

Moderate vendor power: hyperscalers, identity vendors hold pricing clout; regs raise switching costs

Supplier power moderate: core tradeline furnishers need credit bureaus, limiting leverage, but niche alternative-data and identity vendors plus hyperscalers have pricing power. Regulatory constraints (FCRA, GDPR/CCPA) and high security costs raise switching costs. Diversified vendors, in‑house models and multicloud reduce single-supplier dependence.

| Item | 2024 metric | Impact |

|---|---|---|

| Tradeline furnishers | High dependence | Low-moderate power |

| Hyperscalers | AWS 32%/Azure 23%/GCP 11% | Moderate power |

| Identity market | 16B USD; top vendors ~30% | High in niche |

| Regulatory cost | Settlement 700M USD | Raises switching cost |

What is included in the product

Tailored Porter's Five Forces analysis for Equifax assessing competitive rivalry, buyer and supplier power, barriers to entry, and substitution risks—highlighting data security, regulatory pressure, and fintech disruption as key forces shaping profitability.

A concise, one-sheet Porter's Five Forces for Equifax—instantly highlighting competitive intensity, regulatory and data-security risks, and supplier/customer bargaining power to speed strategic decision-making and boardroom discussions.

Customers Bargaining Power

Large financial institutions

Major banks, lenders and insurers routinely dual- or tri-source credit data with Experian and TransUnion, giving them outsized negotiating leverage over Equifax through high-volume RFPs and consolidated purchasing. Their ability to reallocate pull volumes to rivals pressures Equifax on price and contract terms. Custom integrations and proven model performance, however, raise short-term switching costs and preserve some supplier power for Equifax.

Fintechs and digital lenders

High-growth fintechs and digital lenders are highly price-sensitive and agile in vendor selection, increasingly evaluating alternative data and cash-flow underwriting as of 2024 to broaden options and reduce reliance on legacy bureaus; trials and usage-based pricing models amplify their bargaining power by lowering switching costs and enabling rapid proof-of-concept adoption, yet regulatory acceptance in 2024 continues to favor traditional bureau data in many compliance-driven workflows.

Enterprises in telecom and utilities

Enterprises in telecom and utilities wield strong bargaining power with Equifax by negotiating large-scale bundles across verification, identity, and skip-trace solutions, leveraging volume commitments and multi-product procurement to drive discounts. Multi-year contracts create customer stickiness but shift leverage to buyers at renewal, where aggregated usage and renewal timing become key negotiation points. Service-level requirements, especially latency and uptime, are critical levers—enterprises routinely demand strict SLAs and penalties that shape pricing and deployment priorities.

Government and employers

- Procurement focus: compliance over price

- Financial impact: customizations raise deal costs

- Cycle effect: fewer switches, higher evaluation rigor

Consumers and small businesses

Consumers and small businesses have low per‑unit leverage but can switch among the three major national credit bureaus and numerous fintech apps; the FCRA grants dispute rights and free annual reports, limiting monetization. Brand trust and UX drive retention more than lock‑in; price promotions and bundling (common in 2024 digital offers) increase demand elasticity.

- Three major bureaus limit individual bargaining power

- FCRA: dispute rights + free annual reports

- UX, trust, promotions shape retention and elasticity

High-leverage buyers squeeze data providers; fintech alt-data raises 2024 switching risk

Major banks and insurers wield high leverage via multi-vendor sourcing and volume RFPs, forcing price and term concessions. Fintechs are price-sensitive and increasing alternative-data trials in 2024, raising switching risk despite regulatory reliance on bureau data. Enterprises and governments negotiate bundles and strict SLAs, compressing margins; Equifax reported ~$4.4B revenue in 2024 with ~15% enterprise margin pressure. Consumers have low per-unit leverage; FCRA limits monetization.

| Customer Segment | Leverage | 2024 Metric |

|---|---|---|

| Banks/Lenders | High | Dual/tri-sourcing, strong price pressure |

| Fintechs | Medium-High | Alt-data trials ↑ in 2024 |

| Enterprises/Govt | High | 15% margin pressure |

| Consumers/SMBs | Low | FCRA protections, free reports |

Preview Before You Purchase

Equifax Porter's Five Forces Analysis

This preview shows the exact Equifax Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The report covers competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and regulatory/contextual considerations, fully formatted and ready to download. Purchase grants instant access to this identical, final document.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Equifax faces intense competitive rivalry from credit bureaus and fintechs, moderate buyer power from large enterprise clients, low supplier power, and persistent threats from new entrants and substitutes driven by alternative data and analytics. This snapshot highlights strategic pressure points—unlock the full Porter's Five Forces Analysis to access detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Critical data furnishers

Equifax depends on banks, lenders, card issuers and collections agencies to furnish tradeline data, and as of 2024 these furnishers still require bureau coverage to manage credit risk, which limits their bargaining power. Unique portfolios or temporary pullbacks in reporting can reduce data breadth and freshness, creating pressure on Equifax’s analytics. Strict data quality rules and furnishers’ compliance investments raise switching costs and influence negotiating leverage.

Public and alternative data

Government records, utilities, telcos, payroll aggregators and other alternative data expand Equifax’s coverage and product features, with many public-record feeds commoditized while exclusive alt-data can command premiums. Access and usage are tightly constrained by FCRA in the US and GDPR/CCPA frameworks as of 2024, limiting portability and consent. Supplier concentration in niche datasets increases switching costs and pricing power for scarce feeds.

Cloud and analytics stack

Equifax relies on cloud infrastructure, data platforms and analytics tooling to process data at scale, exposing it to supplier leverage from major hyperscalers: 2024 market shares were roughly AWS 32%, Microsoft Azure 23% and Google Cloud 11% (Synergy Research). Multicloud deployments and long-term contracts partially mitigate price and egress fee risks, while performance, security SLAs and SOC/ISO certifications materially shape supplier power.

Identity and fraud tech vendors

Identity and fraud tech vendors supply device intelligence, document verification, and signal feeds that underpin Equifax fraud solutions; the global identity verification market was about 16 billion USD in 2024 and top providers control roughly 30 percent share, giving specialized vendors with proprietary graphs pricing power.

- 2024 market size ~16B USD

- Leading vendors ~30% market share

- Bundled contracts and Equifax in‑house models reduce dependency

- API standards and interoperability lower switching frictions

Cybersecurity and compliance services

Given regulatory exposure, security tooling and audits are mission-critical for Equifax after the 2017 breach that exposed 147 million consumers. Best-in-class vendors are hard to replace without risk; Equifax’s consumer settlement of up to 700 million USD elevated scrutiny and increases reliance on premium solutions. Diversified internal controls and multi-vendor strategies offset single-vendor bargaining power.

- Supplier risk: high

- Settlement impact: 700M USD

- Vendor dependency: mitigated by diversification

Moderate vendor power: hyperscalers, identity vendors hold pricing clout; regs raise switching costs

Supplier power moderate: core tradeline furnishers need credit bureaus, limiting leverage, but niche alternative-data and identity vendors plus hyperscalers have pricing power. Regulatory constraints (FCRA, GDPR/CCPA) and high security costs raise switching costs. Diversified vendors, in‑house models and multicloud reduce single-supplier dependence.

| Item | 2024 metric | Impact |

|---|---|---|

| Tradeline furnishers | High dependence | Low-moderate power |

| Hyperscalers | AWS 32%/Azure 23%/GCP 11% | Moderate power |

| Identity market | 16B USD; top vendors ~30% | High in niche |

| Regulatory cost | Settlement 700M USD | Raises switching cost |

What is included in the product

Tailored Porter's Five Forces analysis for Equifax assessing competitive rivalry, buyer and supplier power, barriers to entry, and substitution risks—highlighting data security, regulatory pressure, and fintech disruption as key forces shaping profitability.

A concise, one-sheet Porter's Five Forces for Equifax—instantly highlighting competitive intensity, regulatory and data-security risks, and supplier/customer bargaining power to speed strategic decision-making and boardroom discussions.

Customers Bargaining Power

Large financial institutions

Major banks, lenders and insurers routinely dual- or tri-source credit data with Experian and TransUnion, giving them outsized negotiating leverage over Equifax through high-volume RFPs and consolidated purchasing. Their ability to reallocate pull volumes to rivals pressures Equifax on price and contract terms. Custom integrations and proven model performance, however, raise short-term switching costs and preserve some supplier power for Equifax.

Fintechs and digital lenders

High-growth fintechs and digital lenders are highly price-sensitive and agile in vendor selection, increasingly evaluating alternative data and cash-flow underwriting as of 2024 to broaden options and reduce reliance on legacy bureaus; trials and usage-based pricing models amplify their bargaining power by lowering switching costs and enabling rapid proof-of-concept adoption, yet regulatory acceptance in 2024 continues to favor traditional bureau data in many compliance-driven workflows.

Enterprises in telecom and utilities

Enterprises in telecom and utilities wield strong bargaining power with Equifax by negotiating large-scale bundles across verification, identity, and skip-trace solutions, leveraging volume commitments and multi-product procurement to drive discounts. Multi-year contracts create customer stickiness but shift leverage to buyers at renewal, where aggregated usage and renewal timing become key negotiation points. Service-level requirements, especially latency and uptime, are critical levers—enterprises routinely demand strict SLAs and penalties that shape pricing and deployment priorities.

Government and employers

- Procurement focus: compliance over price

- Financial impact: customizations raise deal costs

- Cycle effect: fewer switches, higher evaluation rigor

Consumers and small businesses

Consumers and small businesses have low per‑unit leverage but can switch among the three major national credit bureaus and numerous fintech apps; the FCRA grants dispute rights and free annual reports, limiting monetization. Brand trust and UX drive retention more than lock‑in; price promotions and bundling (common in 2024 digital offers) increase demand elasticity.

- Three major bureaus limit individual bargaining power

- FCRA: dispute rights + free annual reports

- UX, trust, promotions shape retention and elasticity

High-leverage buyers squeeze data providers; fintech alt-data raises 2024 switching risk

Major banks and insurers wield high leverage via multi-vendor sourcing and volume RFPs, forcing price and term concessions. Fintechs are price-sensitive and increasing alternative-data trials in 2024, raising switching risk despite regulatory reliance on bureau data. Enterprises and governments negotiate bundles and strict SLAs, compressing margins; Equifax reported ~$4.4B revenue in 2024 with ~15% enterprise margin pressure. Consumers have low per-unit leverage; FCRA limits monetization.

| Customer Segment | Leverage | 2024 Metric |

|---|---|---|

| Banks/Lenders | High | Dual/tri-sourcing, strong price pressure |

| Fintechs | Medium-High | Alt-data trials ↑ in 2024 |

| Enterprises/Govt | High | 15% margin pressure |

| Consumers/SMBs | Low | FCRA protections, free reports |

Preview Before You Purchase

Equifax Porter's Five Forces Analysis

This preview shows the exact Equifax Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The report covers competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and regulatory/contextual considerations, fully formatted and ready to download. Purchase grants instant access to this identical, final document.