Equitable Holdings Porter's Five Forces Analysis

From Overview to Strategy Blueprint

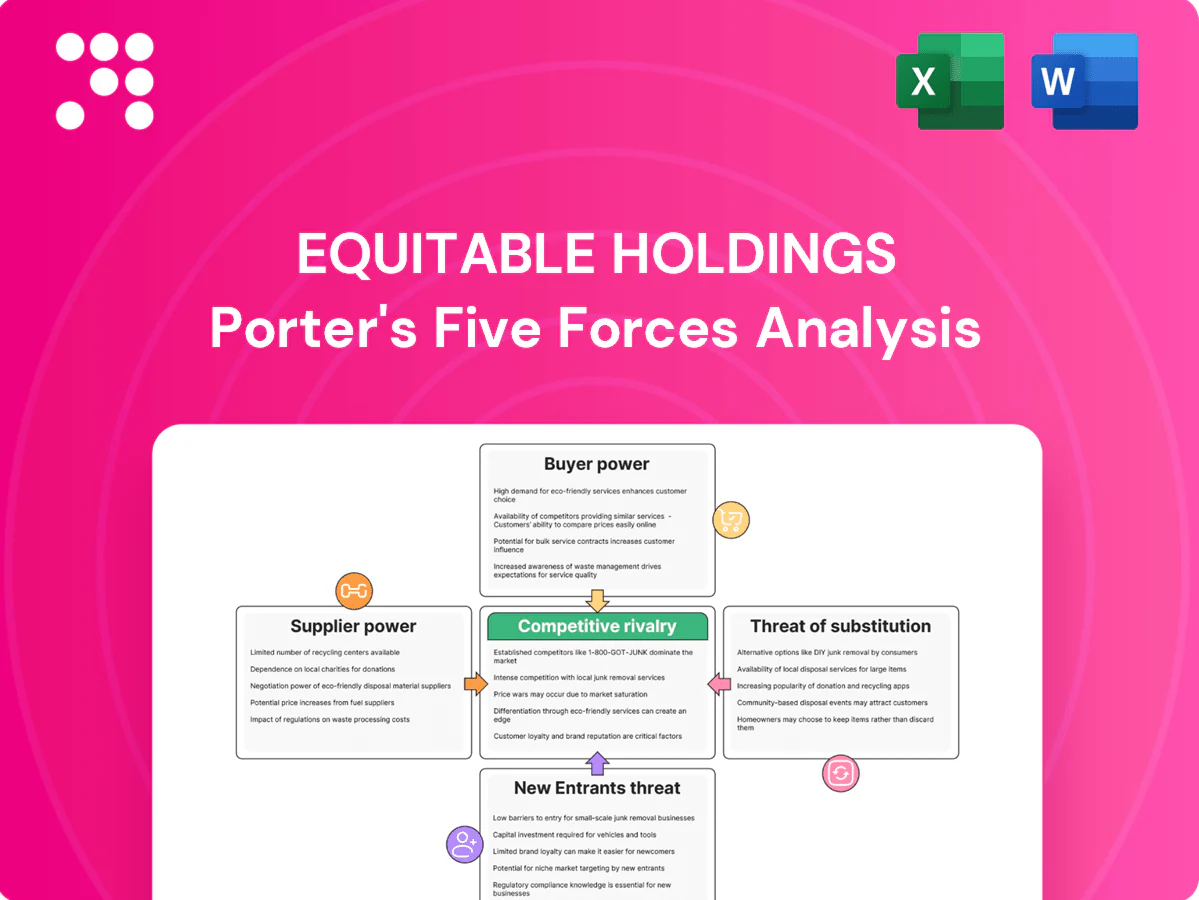

Equitable Holdings faces moderate buyer power, intense rivalry among incumbents, and regulatory-driven entry barriers that shape its profitability; supplier and substitute threats are evolving with fintech disruption. This snapshot highlights key competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights tailored to Equitable Holdings.

Suppliers Bargaining Power

Reinsurers’ pricing leverage

Equitable relies on reinsurance to manage mortality and longevity exposure, ceding blocks to major global reinsurers such as Munich Re, Swiss Re, Hannover Re, SCOR and RGA. Concentration among these players gives them pricing and terms leverage, notably during 2023–24 market volatility that tightened capacity and raised cession costs. Higher capital charges can constrain product design, while multi‑year treaties blunt short spikes but limit repricing flexibility.

Capital markets dependence

Annuity crediting rates and hedging programs are highly dependent on market liquidity and derivatives counterparties. Rising rates and spread volatility, with the 10-year Treasury around 4.6% at end-2024, shifted funding costs and asset yields and tightened guarantee economics. Dealers have widened collateral and pricing terms under stress; diversified counterparties and active collateral management help balance supplier power.

Technology and data vendors

Core policy admin, cloud, cyber and data vendors are specialized and sticky, so switching costs and integration risks give vendors moderate bargaining power over pricing and SLAs. Top three cloud providers held roughly 64% of the IaaS/PaaS market in 2024, raising dependence and resilience concerns. Multi-vendor architectures and growing in-house tooling (many firms retain 24–36 month contracts) temper vendor lock-in.

Distribution intermediaries

Distribution intermediaries—broker-dealers, independent agents and digital platforms—act as gatekeepers to end clients, allowing top channels to demand higher commissions, marketing support and tailored product features; large aggregators secure shelf space and preferred lists that increase their negotiating leverage over Equitable. Expanding proprietary advice channels and direct-to-consumer platforms reduces reliance on these intermediaries and improves margin capture.

- Gatekeepers: broker-dealers, agents, platforms

- Leverage: shelf space, preferred lists

- Demands: commissions, marketing, product features

- Mitigation: proprietary advice, D2C expansion

Specialized talent suppliers

Actuarial, risk, ALM and quant specialists are scarce and command premium pay; BLS reports a May 2023 median actuary wage of $124,450, underscoring high baseline compensation.

Wage inflation and retention packages—compensation rising roughly 5–7% in finance in 2023–24—lift operating costs and margin pressure for Equitable.

Talent concentration in NYC, Boston and London strengthens bargaining power, though strengthened training pipelines and automation (modeling, ML) can gradually ease pressure.

- Talent scarcity: high baseline pay

- Wage inflation: ~5–7% (2023–24)

- Hubs: NYC, Boston, London

- Relief: training pipelines, automation

Reinsurer and cloud concentration tighten supply; actuary median $124,450

Equitable depends on major reinsurers (Munich Re, Swiss Re, Hannover Re, SCOR, RGA), giving suppliers pricing leverage after 2023–24 capacity tightening. Derivatives counterparties and top cloud vendors (top three IaaS/PaaS ~64% in 2024) add concentration risk. Talent scarcity (median actuary $124,450 in May 2023) raises costs.

| Supplier | Concentration | Metric |

|---|---|---|

| Reinsurers | High | 5 firms dominant |

| Cloud | High | Top3 ~64% (2024) |

| Talent | Moderate‑High | Median actuary $124,450 (May 2023) |

What is included in the product

Tailored Porter's Five Forces analysis for Equitable Holdings, uncovering competitive intensity, buyer/supplier influence, threat of new entrants and substitutes, and identifying regulatory and technological disruptors that affect its pricing power and profitability.

Snapshot Porter's Five Forces for Equitable Holdings—condensed, decision-ready insights that eliminate analysis paralysis and let you compare competitive pressures instantly for strategic action.

Customers Bargaining Power

Advisor-driven selection

Financial advisors drive carrier and product choice for retail clients, with large RIA and broker-dealer networks—many managing over $1 trillion in client assets—able to negotiate lower fees and enhanced service terms. Heightened due diligence standards across platforms raise the bar for product approval, limiting options for weaker issuers. Strong wholesaling, robust advisor portals and training from Equitable can reduce buyer leverage by improving product stickiness and execution.

Price transparency

In 2024 fee disclosure regimes such as Form CRS and Reg BI continue to increase price transparency, while online comparison tools let clients benchmark M&E charges, surrender schedules and advisory fees across carriers. This visibility drives fee compression and pushes firms toward value-add bundling to protect margins. Equitable and peers respond with differentiated benefits and planning-led propositions to shift conversations from price to outcomes.

Switching and surrender frictions

Surrender charges and tax implications create meaningful annuity and life-policy switching costs, with typical industry surrender schedules starting around 6–8% and declining to 0% over 7–10 years. Over time declining schedules raise mobility; wealth-management accounts are easier to move via ACAT transfers (typically 3–7 business days) on custodial platforms. Retention programs and benefits riders improve persistency and mitigate churn.

Segment mix diversity

Equitable serves individuals, families and small businesses with varied bargaining power; in 2024 high-net-worth clients and group pension cases continued to secure bespoke terms while mass retail remained price sensitive. The segmented mix—from bespoke institutional deals to retail annuities—dampens overall buyer power and stabilizes revenue negotiation dynamics.

- High-net-worth: bespoke negotiation

- Group cases: strong leverage on terms

- Mass retail: price sensitive, lower leverage

- Net effect 2024: balanced buyer power

Service and digital expectations

- Faster onboarding: reduces churn

- Self-service: increases switching ease

- Transparent reporting: raises retention

Advisors >$1T steer product choice; 71% prefer digital, switch risk

Advisors and large RIA/broker networks (many >$1T AUM) largely dictate product choice and can negotiate fees, reducing retail buyer power. 2024 fee-disclosure (Form CRS, Reg BI) and comparator tools drive fee compression; surrender schedules (6–8% declining to 0% over 7–10 yrs) and tax costs limit switching. 71% of investors prefer digital self-service, raising expectations and switching ease.

| Metric | 2024 Value | Impact |

|---|---|---|

| RIA/Broker AUM | >$1T (many networks) | Negotiation leverage |

| Digital preference | 71% | Higher switching ease |

| Surrender schedule | 6–8% → 0% over 7–10 yrs | Retention barrier |

Full Version Awaits

Equitable Holdings Porter's Five Forces Analysis

This preview displays the exact Equitable Holdings Porter’s Five Forces analysis you'll receive—no placeholders or excerpts. The document is fully formatted and ready for immediate download after purchase. What you see here is the final deliverable, complete and usable for decision-making.

From Overview to Strategy Blueprint

Equitable Holdings faces moderate buyer power, intense rivalry among incumbents, and regulatory-driven entry barriers that shape its profitability; supplier and substitute threats are evolving with fintech disruption. This snapshot highlights key competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights tailored to Equitable Holdings.

Suppliers Bargaining Power

Reinsurers’ pricing leverage

Equitable relies on reinsurance to manage mortality and longevity exposure, ceding blocks to major global reinsurers such as Munich Re, Swiss Re, Hannover Re, SCOR and RGA. Concentration among these players gives them pricing and terms leverage, notably during 2023–24 market volatility that tightened capacity and raised cession costs. Higher capital charges can constrain product design, while multi‑year treaties blunt short spikes but limit repricing flexibility.

Capital markets dependence

Annuity crediting rates and hedging programs are highly dependent on market liquidity and derivatives counterparties. Rising rates and spread volatility, with the 10-year Treasury around 4.6% at end-2024, shifted funding costs and asset yields and tightened guarantee economics. Dealers have widened collateral and pricing terms under stress; diversified counterparties and active collateral management help balance supplier power.

Technology and data vendors

Core policy admin, cloud, cyber and data vendors are specialized and sticky, so switching costs and integration risks give vendors moderate bargaining power over pricing and SLAs. Top three cloud providers held roughly 64% of the IaaS/PaaS market in 2024, raising dependence and resilience concerns. Multi-vendor architectures and growing in-house tooling (many firms retain 24–36 month contracts) temper vendor lock-in.

Distribution intermediaries

Distribution intermediaries—broker-dealers, independent agents and digital platforms—act as gatekeepers to end clients, allowing top channels to demand higher commissions, marketing support and tailored product features; large aggregators secure shelf space and preferred lists that increase their negotiating leverage over Equitable. Expanding proprietary advice channels and direct-to-consumer platforms reduces reliance on these intermediaries and improves margin capture.

- Gatekeepers: broker-dealers, agents, platforms

- Leverage: shelf space, preferred lists

- Demands: commissions, marketing, product features

- Mitigation: proprietary advice, D2C expansion

Specialized talent suppliers

Actuarial, risk, ALM and quant specialists are scarce and command premium pay; BLS reports a May 2023 median actuary wage of $124,450, underscoring high baseline compensation.

Wage inflation and retention packages—compensation rising roughly 5–7% in finance in 2023–24—lift operating costs and margin pressure for Equitable.

Talent concentration in NYC, Boston and London strengthens bargaining power, though strengthened training pipelines and automation (modeling, ML) can gradually ease pressure.

- Talent scarcity: high baseline pay

- Wage inflation: ~5–7% (2023–24)

- Hubs: NYC, Boston, London

- Relief: training pipelines, automation

Reinsurer and cloud concentration tighten supply; actuary median $124,450

Equitable depends on major reinsurers (Munich Re, Swiss Re, Hannover Re, SCOR, RGA), giving suppliers pricing leverage after 2023–24 capacity tightening. Derivatives counterparties and top cloud vendors (top three IaaS/PaaS ~64% in 2024) add concentration risk. Talent scarcity (median actuary $124,450 in May 2023) raises costs.

| Supplier | Concentration | Metric |

|---|---|---|

| Reinsurers | High | 5 firms dominant |

| Cloud | High | Top3 ~64% (2024) |

| Talent | Moderate‑High | Median actuary $124,450 (May 2023) |

What is included in the product

Tailored Porter's Five Forces analysis for Equitable Holdings, uncovering competitive intensity, buyer/supplier influence, threat of new entrants and substitutes, and identifying regulatory and technological disruptors that affect its pricing power and profitability.

Snapshot Porter's Five Forces for Equitable Holdings—condensed, decision-ready insights that eliminate analysis paralysis and let you compare competitive pressures instantly for strategic action.

Customers Bargaining Power

Advisor-driven selection

Financial advisors drive carrier and product choice for retail clients, with large RIA and broker-dealer networks—many managing over $1 trillion in client assets—able to negotiate lower fees and enhanced service terms. Heightened due diligence standards across platforms raise the bar for product approval, limiting options for weaker issuers. Strong wholesaling, robust advisor portals and training from Equitable can reduce buyer leverage by improving product stickiness and execution.

Price transparency

In 2024 fee disclosure regimes such as Form CRS and Reg BI continue to increase price transparency, while online comparison tools let clients benchmark M&E charges, surrender schedules and advisory fees across carriers. This visibility drives fee compression and pushes firms toward value-add bundling to protect margins. Equitable and peers respond with differentiated benefits and planning-led propositions to shift conversations from price to outcomes.

Switching and surrender frictions

Surrender charges and tax implications create meaningful annuity and life-policy switching costs, with typical industry surrender schedules starting around 6–8% and declining to 0% over 7–10 years. Over time declining schedules raise mobility; wealth-management accounts are easier to move via ACAT transfers (typically 3–7 business days) on custodial platforms. Retention programs and benefits riders improve persistency and mitigate churn.

Segment mix diversity

Equitable serves individuals, families and small businesses with varied bargaining power; in 2024 high-net-worth clients and group pension cases continued to secure bespoke terms while mass retail remained price sensitive. The segmented mix—from bespoke institutional deals to retail annuities—dampens overall buyer power and stabilizes revenue negotiation dynamics.

- High-net-worth: bespoke negotiation

- Group cases: strong leverage on terms

- Mass retail: price sensitive, lower leverage

- Net effect 2024: balanced buyer power

Service and digital expectations

- Faster onboarding: reduces churn

- Self-service: increases switching ease

- Transparent reporting: raises retention

Advisors >$1T steer product choice; 71% prefer digital, switch risk

Advisors and large RIA/broker networks (many >$1T AUM) largely dictate product choice and can negotiate fees, reducing retail buyer power. 2024 fee-disclosure (Form CRS, Reg BI) and comparator tools drive fee compression; surrender schedules (6–8% declining to 0% over 7–10 yrs) and tax costs limit switching. 71% of investors prefer digital self-service, raising expectations and switching ease.

| Metric | 2024 Value | Impact |

|---|---|---|

| RIA/Broker AUM | >$1T (many networks) | Negotiation leverage |

| Digital preference | 71% | Higher switching ease |

| Surrender schedule | 6–8% → 0% over 7–10 yrs | Retention barrier |

Full Version Awaits

Equitable Holdings Porter's Five Forces Analysis

This preview displays the exact Equitable Holdings Porter’s Five Forces analysis you'll receive—no placeholders or excerpts. The document is fully formatted and ready for immediate download after purchase. What you see here is the final deliverable, complete and usable for decision-making.

Description

From Overview to Strategy Blueprint

Equitable Holdings faces moderate buyer power, intense rivalry among incumbents, and regulatory-driven entry barriers that shape its profitability; supplier and substitute threats are evolving with fintech disruption. This snapshot highlights key competitive pressures and strategic levers. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights tailored to Equitable Holdings.

Suppliers Bargaining Power

Reinsurers’ pricing leverage

Equitable relies on reinsurance to manage mortality and longevity exposure, ceding blocks to major global reinsurers such as Munich Re, Swiss Re, Hannover Re, SCOR and RGA. Concentration among these players gives them pricing and terms leverage, notably during 2023–24 market volatility that tightened capacity and raised cession costs. Higher capital charges can constrain product design, while multi‑year treaties blunt short spikes but limit repricing flexibility.

Capital markets dependence

Annuity crediting rates and hedging programs are highly dependent on market liquidity and derivatives counterparties. Rising rates and spread volatility, with the 10-year Treasury around 4.6% at end-2024, shifted funding costs and asset yields and tightened guarantee economics. Dealers have widened collateral and pricing terms under stress; diversified counterparties and active collateral management help balance supplier power.

Technology and data vendors

Core policy admin, cloud, cyber and data vendors are specialized and sticky, so switching costs and integration risks give vendors moderate bargaining power over pricing and SLAs. Top three cloud providers held roughly 64% of the IaaS/PaaS market in 2024, raising dependence and resilience concerns. Multi-vendor architectures and growing in-house tooling (many firms retain 24–36 month contracts) temper vendor lock-in.

Distribution intermediaries

Distribution intermediaries—broker-dealers, independent agents and digital platforms—act as gatekeepers to end clients, allowing top channels to demand higher commissions, marketing support and tailored product features; large aggregators secure shelf space and preferred lists that increase their negotiating leverage over Equitable. Expanding proprietary advice channels and direct-to-consumer platforms reduces reliance on these intermediaries and improves margin capture.

- Gatekeepers: broker-dealers, agents, platforms

- Leverage: shelf space, preferred lists

- Demands: commissions, marketing, product features

- Mitigation: proprietary advice, D2C expansion

Specialized talent suppliers

Actuarial, risk, ALM and quant specialists are scarce and command premium pay; BLS reports a May 2023 median actuary wage of $124,450, underscoring high baseline compensation.

Wage inflation and retention packages—compensation rising roughly 5–7% in finance in 2023–24—lift operating costs and margin pressure for Equitable.

Talent concentration in NYC, Boston and London strengthens bargaining power, though strengthened training pipelines and automation (modeling, ML) can gradually ease pressure.

- Talent scarcity: high baseline pay

- Wage inflation: ~5–7% (2023–24)

- Hubs: NYC, Boston, London

- Relief: training pipelines, automation

Reinsurer and cloud concentration tighten supply; actuary median $124,450

Equitable depends on major reinsurers (Munich Re, Swiss Re, Hannover Re, SCOR, RGA), giving suppliers pricing leverage after 2023–24 capacity tightening. Derivatives counterparties and top cloud vendors (top three IaaS/PaaS ~64% in 2024) add concentration risk. Talent scarcity (median actuary $124,450 in May 2023) raises costs.

| Supplier | Concentration | Metric |

|---|---|---|

| Reinsurers | High | 5 firms dominant |

| Cloud | High | Top3 ~64% (2024) |

| Talent | Moderate‑High | Median actuary $124,450 (May 2023) |

What is included in the product

Tailored Porter's Five Forces analysis for Equitable Holdings, uncovering competitive intensity, buyer/supplier influence, threat of new entrants and substitutes, and identifying regulatory and technological disruptors that affect its pricing power and profitability.

Snapshot Porter's Five Forces for Equitable Holdings—condensed, decision-ready insights that eliminate analysis paralysis and let you compare competitive pressures instantly for strategic action.

Customers Bargaining Power

Advisor-driven selection

Financial advisors drive carrier and product choice for retail clients, with large RIA and broker-dealer networks—many managing over $1 trillion in client assets—able to negotiate lower fees and enhanced service terms. Heightened due diligence standards across platforms raise the bar for product approval, limiting options for weaker issuers. Strong wholesaling, robust advisor portals and training from Equitable can reduce buyer leverage by improving product stickiness and execution.

Price transparency

In 2024 fee disclosure regimes such as Form CRS and Reg BI continue to increase price transparency, while online comparison tools let clients benchmark M&E charges, surrender schedules and advisory fees across carriers. This visibility drives fee compression and pushes firms toward value-add bundling to protect margins. Equitable and peers respond with differentiated benefits and planning-led propositions to shift conversations from price to outcomes.

Switching and surrender frictions

Surrender charges and tax implications create meaningful annuity and life-policy switching costs, with typical industry surrender schedules starting around 6–8% and declining to 0% over 7–10 years. Over time declining schedules raise mobility; wealth-management accounts are easier to move via ACAT transfers (typically 3–7 business days) on custodial platforms. Retention programs and benefits riders improve persistency and mitigate churn.

Segment mix diversity

Equitable serves individuals, families and small businesses with varied bargaining power; in 2024 high-net-worth clients and group pension cases continued to secure bespoke terms while mass retail remained price sensitive. The segmented mix—from bespoke institutional deals to retail annuities—dampens overall buyer power and stabilizes revenue negotiation dynamics.

- High-net-worth: bespoke negotiation

- Group cases: strong leverage on terms

- Mass retail: price sensitive, lower leverage

- Net effect 2024: balanced buyer power

Service and digital expectations

- Faster onboarding: reduces churn

- Self-service: increases switching ease

- Transparent reporting: raises retention

Advisors >$1T steer product choice; 71% prefer digital, switch risk

Advisors and large RIA/broker networks (many >$1T AUM) largely dictate product choice and can negotiate fees, reducing retail buyer power. 2024 fee-disclosure (Form CRS, Reg BI) and comparator tools drive fee compression; surrender schedules (6–8% declining to 0% over 7–10 yrs) and tax costs limit switching. 71% of investors prefer digital self-service, raising expectations and switching ease.

| Metric | 2024 Value | Impact |

|---|---|---|

| RIA/Broker AUM | >$1T (many networks) | Negotiation leverage |

| Digital preference | 71% | Higher switching ease |

| Surrender schedule | 6–8% → 0% over 7–10 yrs | Retention barrier |

Full Version Awaits

Equitable Holdings Porter's Five Forces Analysis

This preview displays the exact Equitable Holdings Porter’s Five Forces analysis you'll receive—no placeholders or excerpts. The document is fully formatted and ready for immediate download after purchase. What you see here is the final deliverable, complete and usable for decision-making.