Ericsson Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Ericsson faces intense rivalry, high buyer expectations, and evolving substitute threats driven by 5G and cloud shifts, while supplier dynamics and regulatory barriers shape strategic choices. This snapshot highlights key pressures but leaves out force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a complete, actionable view to inform investment or strategy.

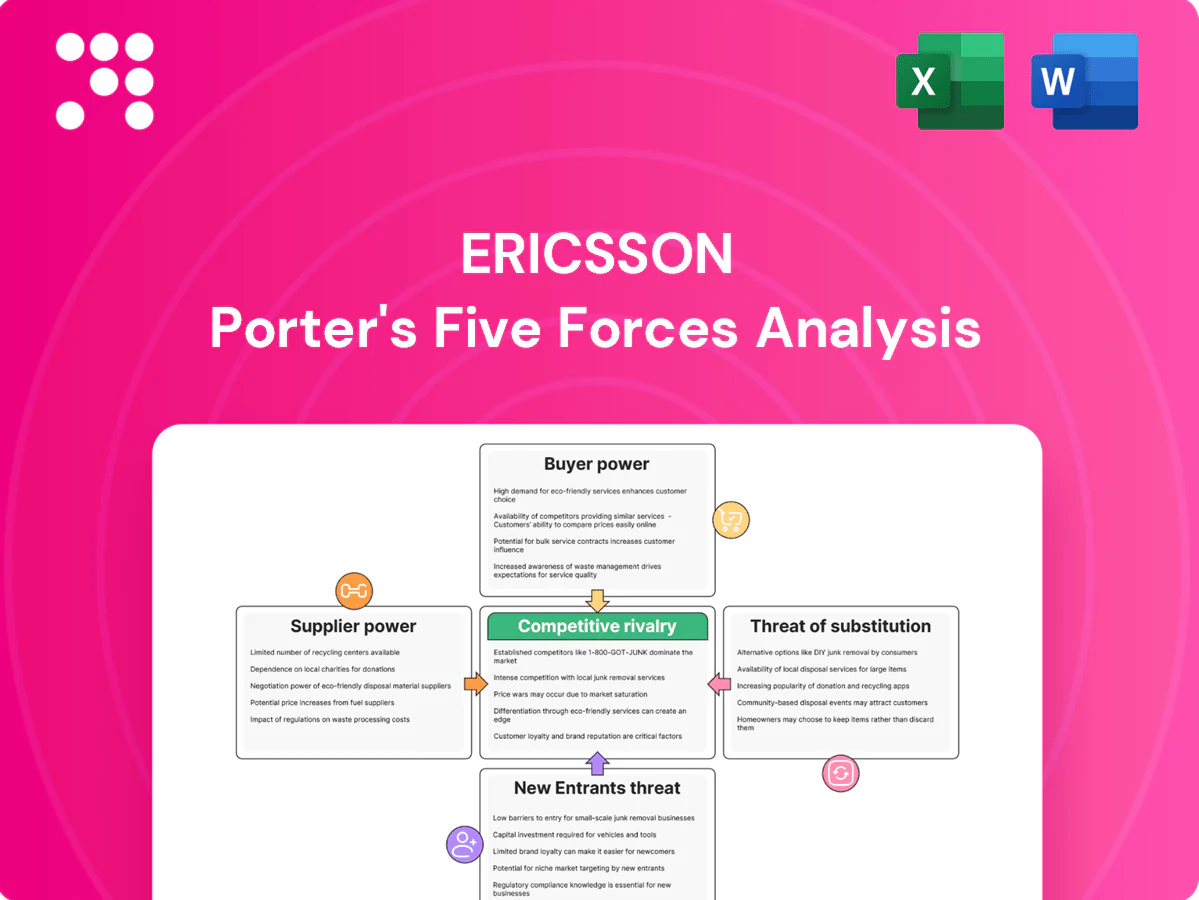

Suppliers Bargaining Power

Concentrated chip and RF supply

Advanced semiconductors (TSMC, Samsung, Intel), FPGAs (AMD/Xilinx) and RF components (Broadcom, Qorvo, Skyworks) are concentrated among few global leaders, raising switching costs and exposure to shortages that can delay 5G/Cloud RAN rollouts and squeeze margins. Long lead times give suppliers leverage on price and allocation. Ericsson mitigates via multi-sourcing, design optionality and inventory buffers.

Standards and patent licensors

Standard-essential patent holders in 3GPP ecosystems—now comprising over 700 contributing organizations—can exert royalty pressure that raises OEM network build costs. Cross-licensing and portfolio swaps reduce net exposure but still shape cost structures and margins. Litigation risk and emergence of renewed 5G/IoT pools in 2023–24 increased uncertainty for licensing terms. Ericsson’s own thousands-strong SEP portfolio provides a counterbalance in negotiations.

Contract manufacturing and EMS

Outsourcing to EMS partners concentrates operational risk as key assembly and test functions sit with a few suppliers; volume commitments and strict quality specs limit rapid vendor shifts and renegotiation. Currency swings and wage inflation in major hubs have pushed component and labor costs higher, and Ericsson—with about 100,000 employees in 2024—uses dual-site sourcing and automation to retain flexibility and mitigate disruptions.

Cloud and software platform dependencies

RAN/vRAN and core increasingly run on COTS servers, accelerators and hyperscaler cloud stacks, creating supplier dependence; AWS, Azure and GCP together held roughly 65–70% of global IaaS/PaaS market in 2024, amplifying pricing and technical lock-in risks. API or certification changes from cloud vendors or silicon suppliers can force costly redesigns, so Ericsson deploys multi-cloud support, hardware abstraction layers and in-house orchestration to hedge exposure.

- Hyperscaler share ~65–70% (2024)

- API/cert changes = redesign risk

- Ericsson hedges: multi-cloud, hardware abstraction, in-house orchestration

Geopolitics and trade controls

Export controls and sanctions increasingly constrain access to specific chipsets and production tools, forcing Ericsson to redesign supply chains and qualify alternative suppliers for affected components.

Regionalization drives parallel BOMs and supplier requalification, raising compliance costs and logistics complexity, which strengthens suppliers able to deliver compliant parts.

Ericsson responds by diversifying sourcing across regions and building compliant supply corridors to mitigate disruption and reduce single-supplier exposure.

- Export controls: restrict certain chipsets and tools

- Regionalization: requires parallel BOMs and requalification

- Supplier leverage: higher compliance/logistics raises bargaining power

- Ericsson strategy: multi-region sourcing and compliant corridors

Supply concentration, SEP royalty risk and cloud lock-in 65–70%

Advanced chips, RF and FPGAs are concentrated among few suppliers, raising switching costs, lead-time risk and margin pressure; Ericsson hedges with multi-sourcing, design optionality and inventory (≈100,000 employees, 2024). SEP holders and licensing uncertainty (Ericsson holds a large SEP portfolio) add royalty leverage. Hyperscalers control ≈65–70% IaaS/PaaS (2024), increasing cloud lock-in risk.

| Metric | 2024 |

|---|---|

| Hyperscaler IaaS/PaaS share | 65–70% |

| Ericsson employees | ≈100,000 |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Ericsson, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying disruptive technologies and market dynamics that influence its pricing, profitability, and strategic positioning.

A clear, one-sheet Porter's Five Forces analysis for Ericsson—instantly highlight competitive pressures from 5G rivals, supplier bargaining, and regulatory & spectrum risks. Customizable pressure levels and a radar chart make it easy to adapt scenarios (5G rollout, M&A, regulation) for swift, board-ready decisions.

Customers Bargaining Power

Highly concentrated CSP buyers

National and multinational operators buy through large tenders, frequently exceeding $500m, giving buyers strong leverage and centralized negotiation power. A handful of key accounts typically drive a disproportionate share of vendor revenue, pressuring price concessions, strict SLAs, and roadmap influence. Ericsson responds with quantified TCO analyses and lifecycle-value propositions to protect margin and long-term contracts.

High but declining switching costs

Legacy RAN/core integration historically locked buyers to vendors, but virtualization, Open RAN and cloud-native interfaces are lowering exit barriers; by 2024 more than 60 operators were engaged in Open RAN trials, expanding buyer options. Multi-vendor trials and increased interoperability raise customer bargaining power, while Ericsson’s investments in interoperability and migration tools aim to keep customers sticky despite declining switching costs.

Aggressive cost focus and opex deflation

CSPs facing ARPU pressure and mandate capex efficiency and energy savings—over 70% of operators in 2024 ranked energy and opex reduction as top priorities—push vendors toward outcome-based pricing and managed-services consolidation, intensifying price benchmarking across Nokia, Samsung and others (driving ~10–20% RAN price pressure); Ericsson stresses energy‑efficient radios and automation to justify premium pricing through measurable opex cuts.

Regulatory and security requirements

Operators face stringent security and sovereignty rules (eg NIS2 and national data-localization moves in 2024) that heavily shape vendor selection; certification and cross-border approval processes add months to swaps and force deeper due diligence. Buyers use compliance clauses and certification status as negotiation leverage, while Ericsson’s established security offerings and local delivery footprint help defend share.

- Regulatory pressure: NIS2/2024

- Certification = slower swaps, higher due diligence

- Compliance used as bargaining tool

- Ericsson: security credentials + local delivery

Private networks and enterprise buyers

Enterprises evaluating 5G/IoT against Wi‑Fi and hyperscaler edge services drive strong comparative shopping; Gartner projects about 30% of organizations will have private cellular by 2025, boosting procurement scrutiny. Smaller average deal sizes (often sub‑$1M) but rising volume increase price sensitivity, while channel partners shape specs and discounts. Ericsson mitigates risk perception through packaged solutions and partner ecosystems, supporting faster procurement and predictable margins.

- Market adoption: Gartner ~30% of enterprises with private cellular by 2025

- Deal economics: average private 5G deals frequently below $1M

- Channel influence: partners drive specs and discounting

- Ericsson response: packaged solutions + ecosystem to lower perceived risk

Large tenders (>$500m) and Open RAN trials (>60) shift leverage to buyers

Large operator tenders (often >$500m) concentrate buying power; a few key accounts drive outsized revenue and demand price, SLA and roadmap concessions. Open RAN/cloud-native lowered switching costs — >60 operators in Open RAN trials by 2024 — raising bargaining leverage vs vendors. Energy/OPEX cuts are priority for >70% of operators in 2024, driving 10–20% RAN price pressure; NIS2/compliance further shapes deals.

| Metric | 2024 |

|---|---|

| Open RAN trials | >60 operators |

| Energy priority | >70% operators |

| RAN price pressure | 10–20% |

| Large tenders | >$500m |

Preview the Actual Deliverable

Ericsson Porter's Five Forces Analysis

This preview is the exact Ericsson Porter's Five Forces Analysis you'll receive after purchase—no mockups, no placeholders. The document is fully formatted, comprehensive and ready for download the moment you buy. You’ll get instant access to this same professional file, prepared for immediate use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Ericsson faces intense rivalry, high buyer expectations, and evolving substitute threats driven by 5G and cloud shifts, while supplier dynamics and regulatory barriers shape strategic choices. This snapshot highlights key pressures but leaves out force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a complete, actionable view to inform investment or strategy.

Suppliers Bargaining Power

Concentrated chip and RF supply

Advanced semiconductors (TSMC, Samsung, Intel), FPGAs (AMD/Xilinx) and RF components (Broadcom, Qorvo, Skyworks) are concentrated among few global leaders, raising switching costs and exposure to shortages that can delay 5G/Cloud RAN rollouts and squeeze margins. Long lead times give suppliers leverage on price and allocation. Ericsson mitigates via multi-sourcing, design optionality and inventory buffers.

Standards and patent licensors

Standard-essential patent holders in 3GPP ecosystems—now comprising over 700 contributing organizations—can exert royalty pressure that raises OEM network build costs. Cross-licensing and portfolio swaps reduce net exposure but still shape cost structures and margins. Litigation risk and emergence of renewed 5G/IoT pools in 2023–24 increased uncertainty for licensing terms. Ericsson’s own thousands-strong SEP portfolio provides a counterbalance in negotiations.

Contract manufacturing and EMS

Outsourcing to EMS partners concentrates operational risk as key assembly and test functions sit with a few suppliers; volume commitments and strict quality specs limit rapid vendor shifts and renegotiation. Currency swings and wage inflation in major hubs have pushed component and labor costs higher, and Ericsson—with about 100,000 employees in 2024—uses dual-site sourcing and automation to retain flexibility and mitigate disruptions.

Cloud and software platform dependencies

RAN/vRAN and core increasingly run on COTS servers, accelerators and hyperscaler cloud stacks, creating supplier dependence; AWS, Azure and GCP together held roughly 65–70% of global IaaS/PaaS market in 2024, amplifying pricing and technical lock-in risks. API or certification changes from cloud vendors or silicon suppliers can force costly redesigns, so Ericsson deploys multi-cloud support, hardware abstraction layers and in-house orchestration to hedge exposure.

- Hyperscaler share ~65–70% (2024)

- API/cert changes = redesign risk

- Ericsson hedges: multi-cloud, hardware abstraction, in-house orchestration

Geopolitics and trade controls

Export controls and sanctions increasingly constrain access to specific chipsets and production tools, forcing Ericsson to redesign supply chains and qualify alternative suppliers for affected components.

Regionalization drives parallel BOMs and supplier requalification, raising compliance costs and logistics complexity, which strengthens suppliers able to deliver compliant parts.

Ericsson responds by diversifying sourcing across regions and building compliant supply corridors to mitigate disruption and reduce single-supplier exposure.

- Export controls: restrict certain chipsets and tools

- Regionalization: requires parallel BOMs and requalification

- Supplier leverage: higher compliance/logistics raises bargaining power

- Ericsson strategy: multi-region sourcing and compliant corridors

Supply concentration, SEP royalty risk and cloud lock-in 65–70%

Advanced chips, RF and FPGAs are concentrated among few suppliers, raising switching costs, lead-time risk and margin pressure; Ericsson hedges with multi-sourcing, design optionality and inventory (≈100,000 employees, 2024). SEP holders and licensing uncertainty (Ericsson holds a large SEP portfolio) add royalty leverage. Hyperscalers control ≈65–70% IaaS/PaaS (2024), increasing cloud lock-in risk.

| Metric | 2024 |

|---|---|

| Hyperscaler IaaS/PaaS share | 65–70% |

| Ericsson employees | ≈100,000 |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Ericsson, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying disruptive technologies and market dynamics that influence its pricing, profitability, and strategic positioning.

A clear, one-sheet Porter's Five Forces analysis for Ericsson—instantly highlight competitive pressures from 5G rivals, supplier bargaining, and regulatory & spectrum risks. Customizable pressure levels and a radar chart make it easy to adapt scenarios (5G rollout, M&A, regulation) for swift, board-ready decisions.

Customers Bargaining Power

Highly concentrated CSP buyers

National and multinational operators buy through large tenders, frequently exceeding $500m, giving buyers strong leverage and centralized negotiation power. A handful of key accounts typically drive a disproportionate share of vendor revenue, pressuring price concessions, strict SLAs, and roadmap influence. Ericsson responds with quantified TCO analyses and lifecycle-value propositions to protect margin and long-term contracts.

High but declining switching costs

Legacy RAN/core integration historically locked buyers to vendors, but virtualization, Open RAN and cloud-native interfaces are lowering exit barriers; by 2024 more than 60 operators were engaged in Open RAN trials, expanding buyer options. Multi-vendor trials and increased interoperability raise customer bargaining power, while Ericsson’s investments in interoperability and migration tools aim to keep customers sticky despite declining switching costs.

Aggressive cost focus and opex deflation

CSPs facing ARPU pressure and mandate capex efficiency and energy savings—over 70% of operators in 2024 ranked energy and opex reduction as top priorities—push vendors toward outcome-based pricing and managed-services consolidation, intensifying price benchmarking across Nokia, Samsung and others (driving ~10–20% RAN price pressure); Ericsson stresses energy‑efficient radios and automation to justify premium pricing through measurable opex cuts.

Regulatory and security requirements

Operators face stringent security and sovereignty rules (eg NIS2 and national data-localization moves in 2024) that heavily shape vendor selection; certification and cross-border approval processes add months to swaps and force deeper due diligence. Buyers use compliance clauses and certification status as negotiation leverage, while Ericsson’s established security offerings and local delivery footprint help defend share.

- Regulatory pressure: NIS2/2024

- Certification = slower swaps, higher due diligence

- Compliance used as bargaining tool

- Ericsson: security credentials + local delivery

Private networks and enterprise buyers

Enterprises evaluating 5G/IoT against Wi‑Fi and hyperscaler edge services drive strong comparative shopping; Gartner projects about 30% of organizations will have private cellular by 2025, boosting procurement scrutiny. Smaller average deal sizes (often sub‑$1M) but rising volume increase price sensitivity, while channel partners shape specs and discounts. Ericsson mitigates risk perception through packaged solutions and partner ecosystems, supporting faster procurement and predictable margins.

- Market adoption: Gartner ~30% of enterprises with private cellular by 2025

- Deal economics: average private 5G deals frequently below $1M

- Channel influence: partners drive specs and discounting

- Ericsson response: packaged solutions + ecosystem to lower perceived risk

Large tenders (>$500m) and Open RAN trials (>60) shift leverage to buyers

Large operator tenders (often >$500m) concentrate buying power; a few key accounts drive outsized revenue and demand price, SLA and roadmap concessions. Open RAN/cloud-native lowered switching costs — >60 operators in Open RAN trials by 2024 — raising bargaining leverage vs vendors. Energy/OPEX cuts are priority for >70% of operators in 2024, driving 10–20% RAN price pressure; NIS2/compliance further shapes deals.

| Metric | 2024 |

|---|---|

| Open RAN trials | >60 operators |

| Energy priority | >70% operators |

| RAN price pressure | 10–20% |

| Large tenders | >$500m |

Preview the Actual Deliverable

Ericsson Porter's Five Forces Analysis

This preview is the exact Ericsson Porter's Five Forces Analysis you'll receive after purchase—no mockups, no placeholders. The document is fully formatted, comprehensive and ready for download the moment you buy. You’ll get instant access to this same professional file, prepared for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Ericsson faces intense rivalry, high buyer expectations, and evolving substitute threats driven by 5G and cloud shifts, while supplier dynamics and regulatory barriers shape strategic choices. This snapshot highlights key pressures but leaves out force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a complete, actionable view to inform investment or strategy.

Suppliers Bargaining Power

Concentrated chip and RF supply

Advanced semiconductors (TSMC, Samsung, Intel), FPGAs (AMD/Xilinx) and RF components (Broadcom, Qorvo, Skyworks) are concentrated among few global leaders, raising switching costs and exposure to shortages that can delay 5G/Cloud RAN rollouts and squeeze margins. Long lead times give suppliers leverage on price and allocation. Ericsson mitigates via multi-sourcing, design optionality and inventory buffers.

Standards and patent licensors

Standard-essential patent holders in 3GPP ecosystems—now comprising over 700 contributing organizations—can exert royalty pressure that raises OEM network build costs. Cross-licensing and portfolio swaps reduce net exposure but still shape cost structures and margins. Litigation risk and emergence of renewed 5G/IoT pools in 2023–24 increased uncertainty for licensing terms. Ericsson’s own thousands-strong SEP portfolio provides a counterbalance in negotiations.

Contract manufacturing and EMS

Outsourcing to EMS partners concentrates operational risk as key assembly and test functions sit with a few suppliers; volume commitments and strict quality specs limit rapid vendor shifts and renegotiation. Currency swings and wage inflation in major hubs have pushed component and labor costs higher, and Ericsson—with about 100,000 employees in 2024—uses dual-site sourcing and automation to retain flexibility and mitigate disruptions.

Cloud and software platform dependencies

RAN/vRAN and core increasingly run on COTS servers, accelerators and hyperscaler cloud stacks, creating supplier dependence; AWS, Azure and GCP together held roughly 65–70% of global IaaS/PaaS market in 2024, amplifying pricing and technical lock-in risks. API or certification changes from cloud vendors or silicon suppliers can force costly redesigns, so Ericsson deploys multi-cloud support, hardware abstraction layers and in-house orchestration to hedge exposure.

- Hyperscaler share ~65–70% (2024)

- API/cert changes = redesign risk

- Ericsson hedges: multi-cloud, hardware abstraction, in-house orchestration

Geopolitics and trade controls

Export controls and sanctions increasingly constrain access to specific chipsets and production tools, forcing Ericsson to redesign supply chains and qualify alternative suppliers for affected components.

Regionalization drives parallel BOMs and supplier requalification, raising compliance costs and logistics complexity, which strengthens suppliers able to deliver compliant parts.

Ericsson responds by diversifying sourcing across regions and building compliant supply corridors to mitigate disruption and reduce single-supplier exposure.

- Export controls: restrict certain chipsets and tools

- Regionalization: requires parallel BOMs and requalification

- Supplier leverage: higher compliance/logistics raises bargaining power

- Ericsson strategy: multi-region sourcing and compliant corridors

Supply concentration, SEP royalty risk and cloud lock-in 65–70%

Advanced chips, RF and FPGAs are concentrated among few suppliers, raising switching costs, lead-time risk and margin pressure; Ericsson hedges with multi-sourcing, design optionality and inventory (≈100,000 employees, 2024). SEP holders and licensing uncertainty (Ericsson holds a large SEP portfolio) add royalty leverage. Hyperscalers control ≈65–70% IaaS/PaaS (2024), increasing cloud lock-in risk.

| Metric | 2024 |

|---|---|

| Hyperscaler IaaS/PaaS share | 65–70% |

| Ericsson employees | ≈100,000 |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Ericsson, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying disruptive technologies and market dynamics that influence its pricing, profitability, and strategic positioning.

A clear, one-sheet Porter's Five Forces analysis for Ericsson—instantly highlight competitive pressures from 5G rivals, supplier bargaining, and regulatory & spectrum risks. Customizable pressure levels and a radar chart make it easy to adapt scenarios (5G rollout, M&A, regulation) for swift, board-ready decisions.

Customers Bargaining Power

Highly concentrated CSP buyers

National and multinational operators buy through large tenders, frequently exceeding $500m, giving buyers strong leverage and centralized negotiation power. A handful of key accounts typically drive a disproportionate share of vendor revenue, pressuring price concessions, strict SLAs, and roadmap influence. Ericsson responds with quantified TCO analyses and lifecycle-value propositions to protect margin and long-term contracts.

High but declining switching costs

Legacy RAN/core integration historically locked buyers to vendors, but virtualization, Open RAN and cloud-native interfaces are lowering exit barriers; by 2024 more than 60 operators were engaged in Open RAN trials, expanding buyer options. Multi-vendor trials and increased interoperability raise customer bargaining power, while Ericsson’s investments in interoperability and migration tools aim to keep customers sticky despite declining switching costs.

Aggressive cost focus and opex deflation

CSPs facing ARPU pressure and mandate capex efficiency and energy savings—over 70% of operators in 2024 ranked energy and opex reduction as top priorities—push vendors toward outcome-based pricing and managed-services consolidation, intensifying price benchmarking across Nokia, Samsung and others (driving ~10–20% RAN price pressure); Ericsson stresses energy‑efficient radios and automation to justify premium pricing through measurable opex cuts.

Regulatory and security requirements

Operators face stringent security and sovereignty rules (eg NIS2 and national data-localization moves in 2024) that heavily shape vendor selection; certification and cross-border approval processes add months to swaps and force deeper due diligence. Buyers use compliance clauses and certification status as negotiation leverage, while Ericsson’s established security offerings and local delivery footprint help defend share.

- Regulatory pressure: NIS2/2024

- Certification = slower swaps, higher due diligence

- Compliance used as bargaining tool

- Ericsson: security credentials + local delivery

Private networks and enterprise buyers

Enterprises evaluating 5G/IoT against Wi‑Fi and hyperscaler edge services drive strong comparative shopping; Gartner projects about 30% of organizations will have private cellular by 2025, boosting procurement scrutiny. Smaller average deal sizes (often sub‑$1M) but rising volume increase price sensitivity, while channel partners shape specs and discounts. Ericsson mitigates risk perception through packaged solutions and partner ecosystems, supporting faster procurement and predictable margins.

- Market adoption: Gartner ~30% of enterprises with private cellular by 2025

- Deal economics: average private 5G deals frequently below $1M

- Channel influence: partners drive specs and discounting

- Ericsson response: packaged solutions + ecosystem to lower perceived risk

Large tenders (>$500m) and Open RAN trials (>60) shift leverage to buyers

Large operator tenders (often >$500m) concentrate buying power; a few key accounts drive outsized revenue and demand price, SLA and roadmap concessions. Open RAN/cloud-native lowered switching costs — >60 operators in Open RAN trials by 2024 — raising bargaining leverage vs vendors. Energy/OPEX cuts are priority for >70% of operators in 2024, driving 10–20% RAN price pressure; NIS2/compliance further shapes deals.

| Metric | 2024 |

|---|---|

| Open RAN trials | >60 operators |

| Energy priority | >70% operators |

| RAN price pressure | 10–20% |

| Large tenders | >$500m |

Preview the Actual Deliverable

Ericsson Porter's Five Forces Analysis

This preview is the exact Ericsson Porter's Five Forces Analysis you'll receive after purchase—no mockups, no placeholders. The document is fully formatted, comprehensive and ready for download the moment you buy. You’ll get instant access to this same professional file, prepared for immediate use.