Erie Indemnity Porter's Five Forces Analysis

From Overview to Strategy Blueprint

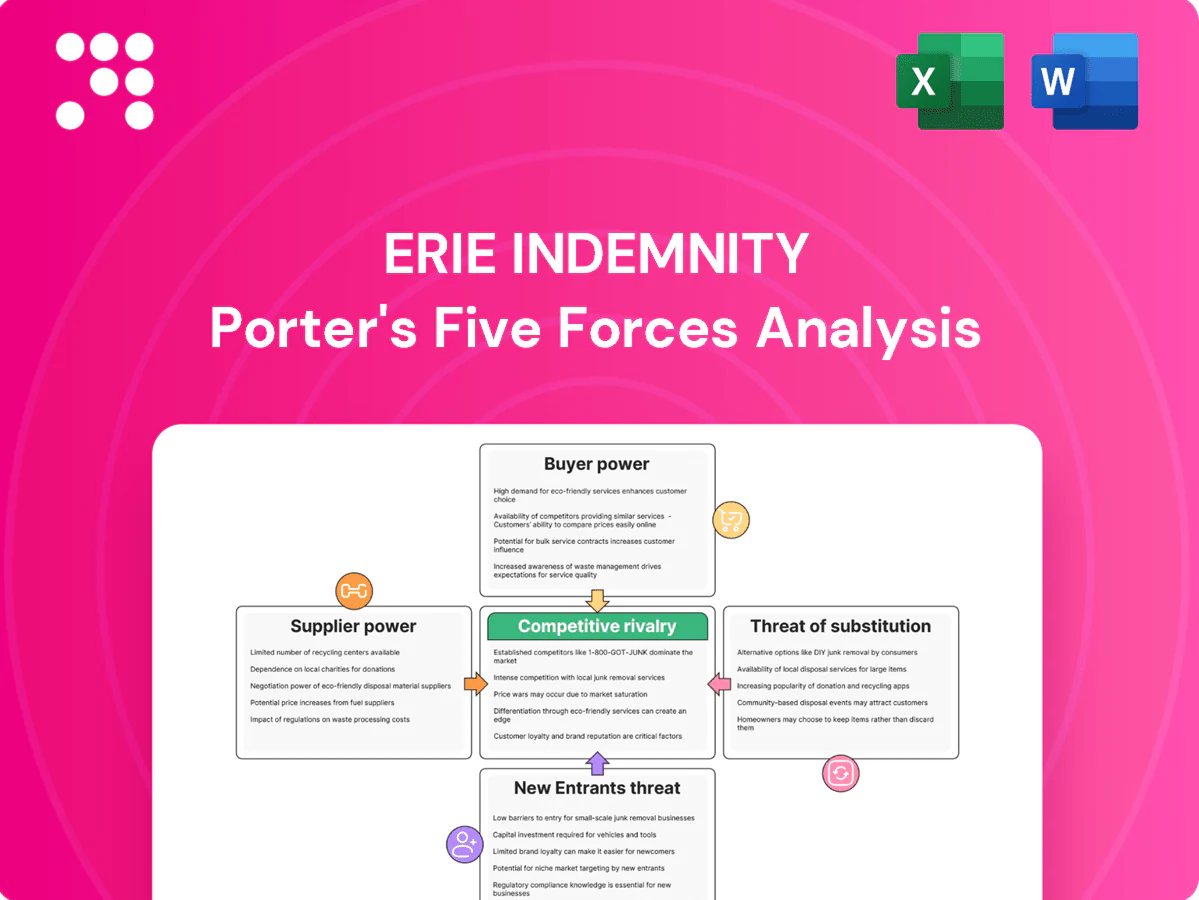

Erie Indemnity operates in a uniquely concentrated insurance services market where buyer loyalty, regulatory barriers, and scale-driven supplier relationships shape competitive intensity. Our concise snapshot flags moderate threat from substitutes and low new-entrant risk but higher rivalry among incumbents. Want force-by-force ratings, visuals, and strategic implications? Unlock the full Porter's Five Forces Analysis for actionable insights tailored to Erie Indemnity.

Suppliers Bargaining Power

Concentrated data/tech vendors

Erie Indemnity relies on specialized core systems, cloud hosting and data providers for underwriting, billing and claims analytics. Vendor switching costs are high due to deep integrations and regulatory compliance. Cloud concentration (AWS 33%, Azure 23%, GCP 11% in 2024) and dominant analytics/data vendors boost suppliers' pricing power. Contracting discipline and multi-vendor strategies partially mitigate but do not eliminate this risk.

Independent repair and claims networks

Auto/body shops, glass repair vendors and adjuster networks materially affect cycle times and indemnity costs; the US collision repair market was roughly $46 billion in 2024, concentrating bargaining power locally. Local capacity constraints after storms can elevate prices and extend cycle times, sometimes driving double-digit cost spikes. Preferred networks and performance-based contracts have cut repair cycle times and claims costs for many carriers. Catastrophe events temporarily spike supplier power and market rates.

Distribution-enabling tools for agents

Third-party quoting, CRM, and comparative raters used by roughly 11,000 independent agencies (2024 Erie filings) shape Erie’s underwriting and distribution workflows. Dependence on these vendors gives them leverage over integration priorities and fee structures, impacting time-to-bind and expense ratios. Building proprietary interfaces can reduce that reliance but often slows agent adoption and digital take-up. Open APIs and co-marketing partnerships help balance control and channel growth.

Specialist services (legal, SIU, catastrophe models)

Specialist suppliers—defense counsel, SIU vendors and catastrophe-model providers—are niche and hard to substitute; the US legal services market was about 343 billion USD in 2023 and the cat-modeling market ~1.4 billion USD in 2023, boosting supplier leverage as expertise and regulatory stakes rise. Panel optimization and volume commitments can secure fee discounts and preferred access, while in-sourcing core expertise reduces long-run dependency and bargaining power.

- Defense counsel: concentrated spend, high switching costs

- SIU: recoveries often exceed ~3x investigative spend, raising vendor leverage

- Cat-models: few providers dominate scenario access and validation

Talent as a critical supplier

Claims adjusters, underwriters and data scientists are scarce and mobile, boosting supplier leverage as US wages rose about 4.1% year-over-year in 2024 (BLS Employment Cost Index); hybrid work expectations further raise bargaining power and turnover risk. Training pipelines and targeted automation can reduce per-claim cost pressure, while stronger culture and clear career paths improve retention and limit wage-driven margin erosion.

- Scarcity: high mobility of technical talent

- Wage pressure: ECI ~4.1% (2024)

- Mitigants: training pipelines, automation

- Retention: culture and career paths lower costs

Supplier power rising: cloud concentration, $46B collision, wage squeeze

Supplier power is moderate-high: cloud/data vendors (AWS 33%/Azure 23%/GCP 11% in 2024) and niche cat-model providers raise costs. Collision repair ($46B 2024) and local capacity spikes boost vendor leverage after storms. Agent tech (11,000 agencies in Erie filings, 2024) and legal/cat-model concentration (US legal $343B 2023; cat-model $1.4B 2023) increase switching costs; talent ECI ~4.1% (2024) tightens labor supply.

| Metric | Value |

|---|---|

| AWS/Azure/GCP (2024) | 33%/23%/11% |

| Collision repair (2024) | $46B |

| Erie agency filings (2024) | ~11,000 |

| US legal / cat-model (2023) | $343B / $1.4B |

| ECI wage growth (2024) | ~4.1% |

What is included in the product

Tailored Porter’s Five Forces analysis of Erie Indemnity that uncovers competitive intensity, buyer/supplier power, entry barriers, substitute threats, and emerging disruptors—actionable for strategy, investor materials, or academic use.

Concise one-sheet Porter's Five Forces for Erie Indemnity that visualizes competitive pressure with a customizable spider chart—update inputs for new data or scenarios and drop straight into decks or dashboards without macros.

Customers Bargaining Power

High dependence on Erie Insurance Exchange

In 2024 the Erie Insurance Exchange remains the sole material buyer of Erie Indemnity’s management services, accounting for essentially all management fee income, creating pronounced buyer concentration. The Exchange exerts direct influence over scope, pricing mechanics and service-level expectations. Operational complexity and regulatory approvals make switching managers difficult, tempering the Exchange’s leverage. Strong governance links between the entities moderate potential conflicts.

Policyholder price sensitivity

P&C customers are highly price-sensitive and shop frequently, which pressures service costs and operational efficiency for distributors like Erie Indemnity. Although Erie Indemnity does not underwrite risk, its service operations directly influence expense ratios and policyholder experience. Poor service performance can increase churn at the Exchange, so service quality materially amplifies buyer bargaining power.

Independent agent expectations

Agents demand competitive commissions, fast underwriting and intuitive digital tools and can switch carriers if workflows lag; industry surveys show distribution churn rises when digital onboarding delays exceed days. Erie’s 100+ year agent network and AM Best A+ (2024) rating reduce defection risk but do not eliminate it. Ongoing platform upgrades and API integrations in 2024 aim to limit agent bargaining leverage.

Regulatory influence on fees and service

Regulatory and governance frameworks constrain Erie Indemnity’s fee structures and service practices, limiting the manager’s ability to unilaterally raise prices. Oversight and disclosure requirements give buyers greater transparency and protection. Compliance-driven processes increase operating rigidity, reducing negotiation flexibility for customized fee terms.

- Regulatory caps on fees

- Transparency improves buyer leverage

- Compliance reduces pricing flexibility

Availability of alternative TPAs/MGAs

Large insurers often self-perform, while TPAs/MGAs offer comparable underwriting, claims and administration, increasing buyer leverage in negotiations; however, Erie’s deep integration with agents, multi-decade service history and embedded systems raise tangible switching costs that soften but do not eliminate customer bargaining power.

- Alternatives available: elevates buyer leverage

- Erie strengths: integration, agent relationships, service longevity

- Net effect: reduced but persistent buyer power

Single buyer controls ≈100% of fees; > 100-year agent network and A+ rating

The Erie Exchange is the sole material buyer of Erie Indemnity’s management services, representing ≈100% of management fees (2024), creating high buyer concentration. Agents are price-sensitive but Erie’s 100+ year agent network and AM Best A+ (2024) rating limit defections. Regulatory oversight and compliance constraints (2024) cap fees and enhance buyer transparency.

| Metric | Value (2024) |

|---|---|

| Management fee concentration | ≈100% |

| AM Best rating | A+ |

| Agent network age | >100 years |

Same Document Delivered

Erie Indemnity Porter's Five Forces Analysis

This preview shows the exact Erie Indemnity Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical file.

From Overview to Strategy Blueprint

Erie Indemnity operates in a uniquely concentrated insurance services market where buyer loyalty, regulatory barriers, and scale-driven supplier relationships shape competitive intensity. Our concise snapshot flags moderate threat from substitutes and low new-entrant risk but higher rivalry among incumbents. Want force-by-force ratings, visuals, and strategic implications? Unlock the full Porter's Five Forces Analysis for actionable insights tailored to Erie Indemnity.

Suppliers Bargaining Power

Concentrated data/tech vendors

Erie Indemnity relies on specialized core systems, cloud hosting and data providers for underwriting, billing and claims analytics. Vendor switching costs are high due to deep integrations and regulatory compliance. Cloud concentration (AWS 33%, Azure 23%, GCP 11% in 2024) and dominant analytics/data vendors boost suppliers' pricing power. Contracting discipline and multi-vendor strategies partially mitigate but do not eliminate this risk.

Independent repair and claims networks

Auto/body shops, glass repair vendors and adjuster networks materially affect cycle times and indemnity costs; the US collision repair market was roughly $46 billion in 2024, concentrating bargaining power locally. Local capacity constraints after storms can elevate prices and extend cycle times, sometimes driving double-digit cost spikes. Preferred networks and performance-based contracts have cut repair cycle times and claims costs for many carriers. Catastrophe events temporarily spike supplier power and market rates.

Distribution-enabling tools for agents

Third-party quoting, CRM, and comparative raters used by roughly 11,000 independent agencies (2024 Erie filings) shape Erie’s underwriting and distribution workflows. Dependence on these vendors gives them leverage over integration priorities and fee structures, impacting time-to-bind and expense ratios. Building proprietary interfaces can reduce that reliance but often slows agent adoption and digital take-up. Open APIs and co-marketing partnerships help balance control and channel growth.

Specialist services (legal, SIU, catastrophe models)

Specialist suppliers—defense counsel, SIU vendors and catastrophe-model providers—are niche and hard to substitute; the US legal services market was about 343 billion USD in 2023 and the cat-modeling market ~1.4 billion USD in 2023, boosting supplier leverage as expertise and regulatory stakes rise. Panel optimization and volume commitments can secure fee discounts and preferred access, while in-sourcing core expertise reduces long-run dependency and bargaining power.

- Defense counsel: concentrated spend, high switching costs

- SIU: recoveries often exceed ~3x investigative spend, raising vendor leverage

- Cat-models: few providers dominate scenario access and validation

Talent as a critical supplier

Claims adjusters, underwriters and data scientists are scarce and mobile, boosting supplier leverage as US wages rose about 4.1% year-over-year in 2024 (BLS Employment Cost Index); hybrid work expectations further raise bargaining power and turnover risk. Training pipelines and targeted automation can reduce per-claim cost pressure, while stronger culture and clear career paths improve retention and limit wage-driven margin erosion.

- Scarcity: high mobility of technical talent

- Wage pressure: ECI ~4.1% (2024)

- Mitigants: training pipelines, automation

- Retention: culture and career paths lower costs

Supplier power rising: cloud concentration, $46B collision, wage squeeze

Supplier power is moderate-high: cloud/data vendors (AWS 33%/Azure 23%/GCP 11% in 2024) and niche cat-model providers raise costs. Collision repair ($46B 2024) and local capacity spikes boost vendor leverage after storms. Agent tech (11,000 agencies in Erie filings, 2024) and legal/cat-model concentration (US legal $343B 2023; cat-model $1.4B 2023) increase switching costs; talent ECI ~4.1% (2024) tightens labor supply.

| Metric | Value |

|---|---|

| AWS/Azure/GCP (2024) | 33%/23%/11% |

| Collision repair (2024) | $46B |

| Erie agency filings (2024) | ~11,000 |

| US legal / cat-model (2023) | $343B / $1.4B |

| ECI wage growth (2024) | ~4.1% |

What is included in the product

Tailored Porter’s Five Forces analysis of Erie Indemnity that uncovers competitive intensity, buyer/supplier power, entry barriers, substitute threats, and emerging disruptors—actionable for strategy, investor materials, or academic use.

Concise one-sheet Porter's Five Forces for Erie Indemnity that visualizes competitive pressure with a customizable spider chart—update inputs for new data or scenarios and drop straight into decks or dashboards without macros.

Customers Bargaining Power

High dependence on Erie Insurance Exchange

In 2024 the Erie Insurance Exchange remains the sole material buyer of Erie Indemnity’s management services, accounting for essentially all management fee income, creating pronounced buyer concentration. The Exchange exerts direct influence over scope, pricing mechanics and service-level expectations. Operational complexity and regulatory approvals make switching managers difficult, tempering the Exchange’s leverage. Strong governance links between the entities moderate potential conflicts.

Policyholder price sensitivity

P&C customers are highly price-sensitive and shop frequently, which pressures service costs and operational efficiency for distributors like Erie Indemnity. Although Erie Indemnity does not underwrite risk, its service operations directly influence expense ratios and policyholder experience. Poor service performance can increase churn at the Exchange, so service quality materially amplifies buyer bargaining power.

Independent agent expectations

Agents demand competitive commissions, fast underwriting and intuitive digital tools and can switch carriers if workflows lag; industry surveys show distribution churn rises when digital onboarding delays exceed days. Erie’s 100+ year agent network and AM Best A+ (2024) rating reduce defection risk but do not eliminate it. Ongoing platform upgrades and API integrations in 2024 aim to limit agent bargaining leverage.

Regulatory influence on fees and service

Regulatory and governance frameworks constrain Erie Indemnity’s fee structures and service practices, limiting the manager’s ability to unilaterally raise prices. Oversight and disclosure requirements give buyers greater transparency and protection. Compliance-driven processes increase operating rigidity, reducing negotiation flexibility for customized fee terms.

- Regulatory caps on fees

- Transparency improves buyer leverage

- Compliance reduces pricing flexibility

Availability of alternative TPAs/MGAs

Large insurers often self-perform, while TPAs/MGAs offer comparable underwriting, claims and administration, increasing buyer leverage in negotiations; however, Erie’s deep integration with agents, multi-decade service history and embedded systems raise tangible switching costs that soften but do not eliminate customer bargaining power.

- Alternatives available: elevates buyer leverage

- Erie strengths: integration, agent relationships, service longevity

- Net effect: reduced but persistent buyer power

Single buyer controls ≈100% of fees; > 100-year agent network and A+ rating

The Erie Exchange is the sole material buyer of Erie Indemnity’s management services, representing ≈100% of management fees (2024), creating high buyer concentration. Agents are price-sensitive but Erie’s 100+ year agent network and AM Best A+ (2024) rating limit defections. Regulatory oversight and compliance constraints (2024) cap fees and enhance buyer transparency.

| Metric | Value (2024) |

|---|---|

| Management fee concentration | ≈100% |

| AM Best rating | A+ |

| Agent network age | >100 years |

Same Document Delivered

Erie Indemnity Porter's Five Forces Analysis

This preview shows the exact Erie Indemnity Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical file.

Description

From Overview to Strategy Blueprint

Erie Indemnity operates in a uniquely concentrated insurance services market where buyer loyalty, regulatory barriers, and scale-driven supplier relationships shape competitive intensity. Our concise snapshot flags moderate threat from substitutes and low new-entrant risk but higher rivalry among incumbents. Want force-by-force ratings, visuals, and strategic implications? Unlock the full Porter's Five Forces Analysis for actionable insights tailored to Erie Indemnity.

Suppliers Bargaining Power

Concentrated data/tech vendors

Erie Indemnity relies on specialized core systems, cloud hosting and data providers for underwriting, billing and claims analytics. Vendor switching costs are high due to deep integrations and regulatory compliance. Cloud concentration (AWS 33%, Azure 23%, GCP 11% in 2024) and dominant analytics/data vendors boost suppliers' pricing power. Contracting discipline and multi-vendor strategies partially mitigate but do not eliminate this risk.

Independent repair and claims networks

Auto/body shops, glass repair vendors and adjuster networks materially affect cycle times and indemnity costs; the US collision repair market was roughly $46 billion in 2024, concentrating bargaining power locally. Local capacity constraints after storms can elevate prices and extend cycle times, sometimes driving double-digit cost spikes. Preferred networks and performance-based contracts have cut repair cycle times and claims costs for many carriers. Catastrophe events temporarily spike supplier power and market rates.

Distribution-enabling tools for agents

Third-party quoting, CRM, and comparative raters used by roughly 11,000 independent agencies (2024 Erie filings) shape Erie’s underwriting and distribution workflows. Dependence on these vendors gives them leverage over integration priorities and fee structures, impacting time-to-bind and expense ratios. Building proprietary interfaces can reduce that reliance but often slows agent adoption and digital take-up. Open APIs and co-marketing partnerships help balance control and channel growth.

Specialist services (legal, SIU, catastrophe models)

Specialist suppliers—defense counsel, SIU vendors and catastrophe-model providers—are niche and hard to substitute; the US legal services market was about 343 billion USD in 2023 and the cat-modeling market ~1.4 billion USD in 2023, boosting supplier leverage as expertise and regulatory stakes rise. Panel optimization and volume commitments can secure fee discounts and preferred access, while in-sourcing core expertise reduces long-run dependency and bargaining power.

- Defense counsel: concentrated spend, high switching costs

- SIU: recoveries often exceed ~3x investigative spend, raising vendor leverage

- Cat-models: few providers dominate scenario access and validation

Talent as a critical supplier

Claims adjusters, underwriters and data scientists are scarce and mobile, boosting supplier leverage as US wages rose about 4.1% year-over-year in 2024 (BLS Employment Cost Index); hybrid work expectations further raise bargaining power and turnover risk. Training pipelines and targeted automation can reduce per-claim cost pressure, while stronger culture and clear career paths improve retention and limit wage-driven margin erosion.

- Scarcity: high mobility of technical talent

- Wage pressure: ECI ~4.1% (2024)

- Mitigants: training pipelines, automation

- Retention: culture and career paths lower costs

Supplier power rising: cloud concentration, $46B collision, wage squeeze

Supplier power is moderate-high: cloud/data vendors (AWS 33%/Azure 23%/GCP 11% in 2024) and niche cat-model providers raise costs. Collision repair ($46B 2024) and local capacity spikes boost vendor leverage after storms. Agent tech (11,000 agencies in Erie filings, 2024) and legal/cat-model concentration (US legal $343B 2023; cat-model $1.4B 2023) increase switching costs; talent ECI ~4.1% (2024) tightens labor supply.

| Metric | Value |

|---|---|

| AWS/Azure/GCP (2024) | 33%/23%/11% |

| Collision repair (2024) | $46B |

| Erie agency filings (2024) | ~11,000 |

| US legal / cat-model (2023) | $343B / $1.4B |

| ECI wage growth (2024) | ~4.1% |

What is included in the product

Tailored Porter’s Five Forces analysis of Erie Indemnity that uncovers competitive intensity, buyer/supplier power, entry barriers, substitute threats, and emerging disruptors—actionable for strategy, investor materials, or academic use.

Concise one-sheet Porter's Five Forces for Erie Indemnity that visualizes competitive pressure with a customizable spider chart—update inputs for new data or scenarios and drop straight into decks or dashboards without macros.

Customers Bargaining Power

High dependence on Erie Insurance Exchange

In 2024 the Erie Insurance Exchange remains the sole material buyer of Erie Indemnity’s management services, accounting for essentially all management fee income, creating pronounced buyer concentration. The Exchange exerts direct influence over scope, pricing mechanics and service-level expectations. Operational complexity and regulatory approvals make switching managers difficult, tempering the Exchange’s leverage. Strong governance links between the entities moderate potential conflicts.

Policyholder price sensitivity

P&C customers are highly price-sensitive and shop frequently, which pressures service costs and operational efficiency for distributors like Erie Indemnity. Although Erie Indemnity does not underwrite risk, its service operations directly influence expense ratios and policyholder experience. Poor service performance can increase churn at the Exchange, so service quality materially amplifies buyer bargaining power.

Independent agent expectations

Agents demand competitive commissions, fast underwriting and intuitive digital tools and can switch carriers if workflows lag; industry surveys show distribution churn rises when digital onboarding delays exceed days. Erie’s 100+ year agent network and AM Best A+ (2024) rating reduce defection risk but do not eliminate it. Ongoing platform upgrades and API integrations in 2024 aim to limit agent bargaining leverage.

Regulatory influence on fees and service

Regulatory and governance frameworks constrain Erie Indemnity’s fee structures and service practices, limiting the manager’s ability to unilaterally raise prices. Oversight and disclosure requirements give buyers greater transparency and protection. Compliance-driven processes increase operating rigidity, reducing negotiation flexibility for customized fee terms.

- Regulatory caps on fees

- Transparency improves buyer leverage

- Compliance reduces pricing flexibility

Availability of alternative TPAs/MGAs

Large insurers often self-perform, while TPAs/MGAs offer comparable underwriting, claims and administration, increasing buyer leverage in negotiations; however, Erie’s deep integration with agents, multi-decade service history and embedded systems raise tangible switching costs that soften but do not eliminate customer bargaining power.

- Alternatives available: elevates buyer leverage

- Erie strengths: integration, agent relationships, service longevity

- Net effect: reduced but persistent buyer power

Single buyer controls ≈100% of fees; > 100-year agent network and A+ rating

The Erie Exchange is the sole material buyer of Erie Indemnity’s management services, representing ≈100% of management fees (2024), creating high buyer concentration. Agents are price-sensitive but Erie’s 100+ year agent network and AM Best A+ (2024) rating limit defections. Regulatory oversight and compliance constraints (2024) cap fees and enhance buyer transparency.

| Metric | Value (2024) |

|---|---|

| Management fee concentration | ≈100% |

| AM Best rating | A+ |

| Agent network age | >100 years |

Same Document Delivered

Erie Indemnity Porter's Five Forces Analysis

This preview shows the exact Erie Indemnity Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; purchase grants instant access to this identical file.