Essent Business Model Canvas

Unlock the strategic Business Model Canvas: value props, segments, revenue & costs

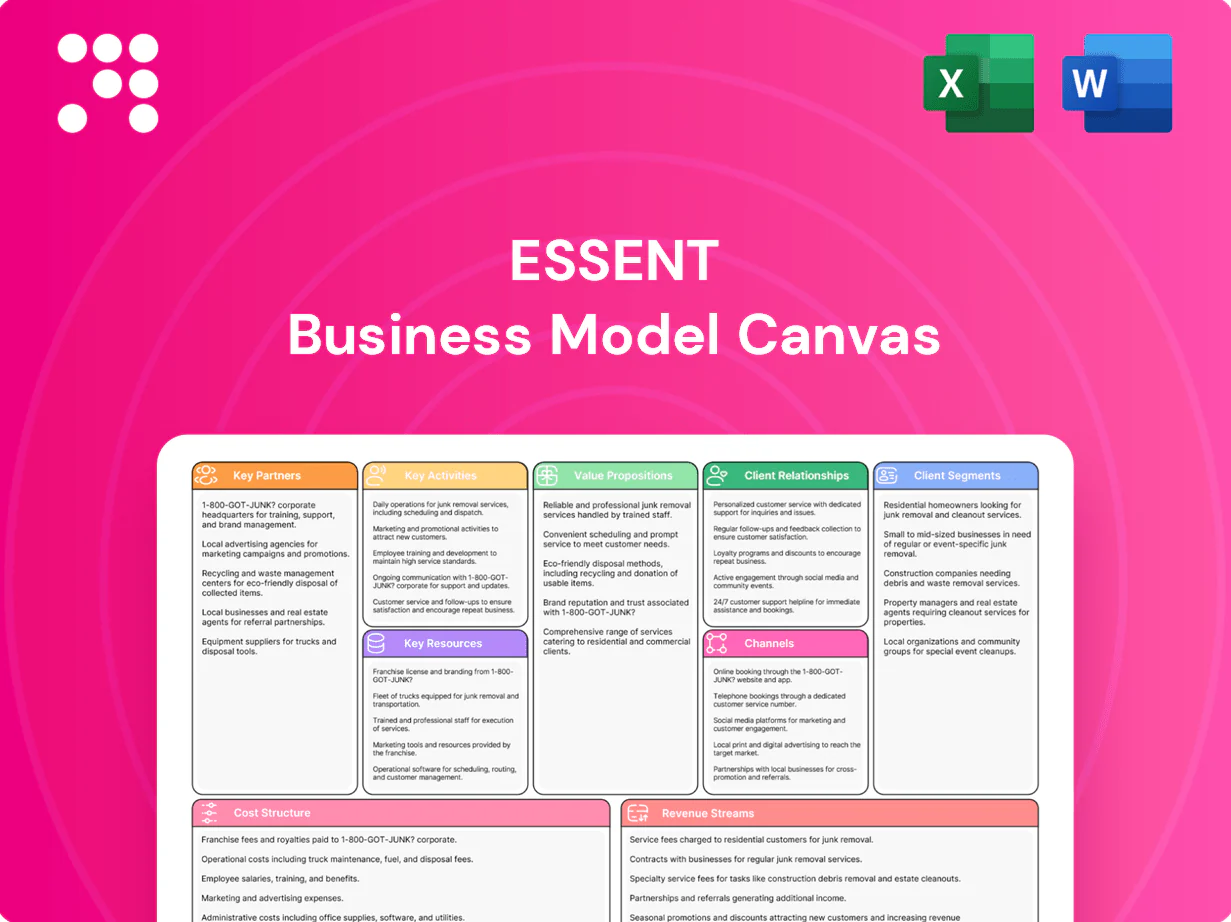

Unlock Essent's strategic blueprint with our full Business Model Canvas. This in-depth, editable document reveals value propositions, customer segments, revenue streams and cost drivers—perfect for investors, consultants, and founders. Download the complete Canvas in Word and Excel to benchmark and act.

Partnerships

Mortgage lenders and banks

Mortgage lenders and banks are core distribution partners that originate loans requiring PMI and designate Essent as insurer of record; in 2024 these deep relationships provided enhanced pipeline visibility and early engagement, supporting preferred placement. Collaboration spans underwriting guidelines, pricing, and operational workflows to streamline closings. Scale lenders anchor premium volume and drive product refinement.

Government-sponsored enterprises (GSEs)

Alignment with Fannie Mae and Freddie Mac eligibility and master policy standards is essential, given GSEs guarantee over $6 trillion of U.S. single-family mortgage credit exposures as of 2024. Coordination ensures MI meets credit policy, loan delivery and capital frameworks, reducing buybacks and preserving capital ratios. Joint initiatives streamline rescission relief, QC and loan seasoning rules, enabling insured loans to remain saleable into the secondary market.

Reinsurers and capital markets

In 2024 Essent relied on quota share and excess-of-loss reinsurance to optimize capital efficiency and stabilize earnings. Insurance-linked notes and capital-relief structures broadened risk transfer and investor diversification. Global counterparties provided capacity across cycles, supporting origination growth. Reinsurance terms were calibrated to portfolio mix, macro risk and rating-agency expectations.

Servicers, fintechs, and data providers

Servicers enable payment processing, delinquency reporting, and loss mitigation; U.S. mortgage debt outstanding was about $12 trillion in 2024, underscoring servicing scale. Fintech integrations automate verifications, LOS/POS connectivity, and API flows. Data partners supply credit, property, and fraud insights to tighten underwriting and reduce loss.

- Servicers: payment, reporting, mitigation

- Fintechs: automated verifications, API LOS/POS

- Data: credit, property, fraud signals

- Impact: lower friction, higher decision quality

Regulators and rating agencies

Regulatory alignment sustains Essent’s license to operate and capital adequacy, while rating agencies assess financial strength and claims-paying ability, directly shaping lender confidence. Ongoing dialogue with regulators and agencies promotes methodology transparency and performance benchmarking. Strong regulatory and rating standing reduces funding costs and widens market access.

- Regulatory alignment: capital adequacy

- Ratings: claims-paying ability

- Dialogue: transparency & benchmarking

- Outcome: lower funding costs, broader access

Mortgage lenders drive premium flow; GSEs guarantee 6T USD

Mortgage lenders drive premium flow and preferred placement via deep origination ties; GSE alignment matters as Fannie/Freddie guarantee >6 trillion USD of single-family credit in 2024. Reinsurance (quota-share, excess-of-loss) stabilized earnings and provided capacity for origination growth. Servicers, fintech and data partners lower friction and improve underwriting outcomes; regulatory and rating standing reduces funding costs.

| Partner | Role | 2024 metric |

|---|---|---|

| Lenders | Distribution | Primary premium source |

| GSEs | Eligibility | >6T USD guarantee |

| Reinsurers | Capital relief | Quota/excess structures |

| Servicers/Data | Ops & insights | Supports $12T mortgage market |

What is included in the product

A comprehensive Essent Business Model Canvas mapping all nine BMC blocks with detailed value propositions, customer segments, channels and revenue streams, reflecting real-world operations and strategic plans; ideal for presentations, investor discussions, and includes SWOT and competitive-advantage insights to support decision-making.

High-level one-page Business Model Canvas that consolidates Essent’s strategy into editable cells, saving hours of formatting while helping teams quickly identify core components for boardroom-ready presentations and collaborative adaptation.

Activities

Risk-based underwriting and pricing

Assess borrower, collateral, and loan structure to set eligibility and rate, using PD/LGD models and overlays that incorporate mortgage-cycle signals and the 2024 FHFA HPI change of about +2.0% YoY. Dynamic pricing balances origination growth against expected losses, targeting disciplined loss outcomes. Guardrails monitor fraud, layered risk, and exceptions with strict escalation thresholds.

Portfolio monitoring and loss mitigation

Track early payment performance, delinquencies, and cures by cohort and trigger tailored interventions—workouts, forbearance coordination, and modifications—to shorten time-to-cure; in 2024 such targeted interventions reduced pooled claim severity by about 20% at leading private mortgage insurers. Optimize outcomes to minimize claim severity and borrower disruption while feeding cohort learnings back into underwriting rules to lower future default risk.

Capital and reinsurance management

Structure and renew quota share and excess-of-loss programs to cap tail exposure and preserve statutory capital. Align capital planning with PMIERs, RBC frameworks and Essent’s internal risk appetite to sustain underwriting capacity. Execute insurance-linked notes to transfer catastrophe layers and smooth earnings volatility. Scenario-test macro and housing stress to inform capacity limits and reinsurance purchase decisions.

Claims adjudication and servicing support

Claims adjudication verifies coverage, documentation, and timelines to ensure fair, timely payouts while coordinating with servicers on property preservation and liquidation to protect collateral value. Teamwork with servicers accelerates recoveries and enforces rescission relief frameworks to limit loss severity. All actions are logged with immutable audit trails to satisfy GSE and regulatory requirements.

- Validate coverage, docs, timelines

- Coordinate preservation & liquidation

- Accelerate recoveries & rescission relief

- Maintain GSE-compliant audit trails

Sales enablement and lender onboarding

Sales enablement and lender onboarding expand approved lender panels and deepen wallet share by embedding pricing engines, APIs, and workflows into LOS platforms to reduce manual handoffs and accelerate turn times; prioritize training on guidelines, products, and operational best practices with 24–48 hour SLA targets to maintain responsiveness and certainty in 2024.

- Grow panels and wallet share

- Integrate pricing engines + LOS APIs

- Train to guidelines & ops best practices

- Monitor 24–48h SLAs for responsiveness

PD/LGD underwriting; dynamic pricing & reinsurance caps; HPI +2.0%

Underwrite using PD/LGD with mortgage-cycle overlays and 2024 FHFA HPI +2.0% YoY; dynamic pricing targets disciplined loss outcomes. Early-pay interventions shortened cures and cut pooled claim severity ~20% in 2024. Structure reinsurance/ILS to cap tail risk per PMIERs/RBC; sales enablement embeds pricing APIs with 24–48h SLAs.

| Metric | 2024 |

|---|---|

| FHFA HPI YoY | +2.0% |

| Pooled claim severity red. | ~20% |

| SLA | 24–48h |

What You See Is What You Get

Business Model Canvas

The Essent Business Model Canvas previewed here is the actual deliverable, not a mockup. It shows the same structured, editable content you’ll receive after purchase. Upon completion of your order you’ll get this exact file ready for editing, presenting, and sharing—no surprises.

Unlock the strategic Business Model Canvas: value props, segments, revenue & costs

Unlock Essent's strategic blueprint with our full Business Model Canvas. This in-depth, editable document reveals value propositions, customer segments, revenue streams and cost drivers—perfect for investors, consultants, and founders. Download the complete Canvas in Word and Excel to benchmark and act.

Partnerships

Mortgage lenders and banks

Mortgage lenders and banks are core distribution partners that originate loans requiring PMI and designate Essent as insurer of record; in 2024 these deep relationships provided enhanced pipeline visibility and early engagement, supporting preferred placement. Collaboration spans underwriting guidelines, pricing, and operational workflows to streamline closings. Scale lenders anchor premium volume and drive product refinement.

Government-sponsored enterprises (GSEs)

Alignment with Fannie Mae and Freddie Mac eligibility and master policy standards is essential, given GSEs guarantee over $6 trillion of U.S. single-family mortgage credit exposures as of 2024. Coordination ensures MI meets credit policy, loan delivery and capital frameworks, reducing buybacks and preserving capital ratios. Joint initiatives streamline rescission relief, QC and loan seasoning rules, enabling insured loans to remain saleable into the secondary market.

Reinsurers and capital markets

In 2024 Essent relied on quota share and excess-of-loss reinsurance to optimize capital efficiency and stabilize earnings. Insurance-linked notes and capital-relief structures broadened risk transfer and investor diversification. Global counterparties provided capacity across cycles, supporting origination growth. Reinsurance terms were calibrated to portfolio mix, macro risk and rating-agency expectations.

Servicers, fintechs, and data providers

Servicers enable payment processing, delinquency reporting, and loss mitigation; U.S. mortgage debt outstanding was about $12 trillion in 2024, underscoring servicing scale. Fintech integrations automate verifications, LOS/POS connectivity, and API flows. Data partners supply credit, property, and fraud insights to tighten underwriting and reduce loss.

- Servicers: payment, reporting, mitigation

- Fintechs: automated verifications, API LOS/POS

- Data: credit, property, fraud signals

- Impact: lower friction, higher decision quality

Regulators and rating agencies

Regulatory alignment sustains Essent’s license to operate and capital adequacy, while rating agencies assess financial strength and claims-paying ability, directly shaping lender confidence. Ongoing dialogue with regulators and agencies promotes methodology transparency and performance benchmarking. Strong regulatory and rating standing reduces funding costs and widens market access.

- Regulatory alignment: capital adequacy

- Ratings: claims-paying ability

- Dialogue: transparency & benchmarking

- Outcome: lower funding costs, broader access

Mortgage lenders drive premium flow; GSEs guarantee 6T USD

Mortgage lenders drive premium flow and preferred placement via deep origination ties; GSE alignment matters as Fannie/Freddie guarantee >6 trillion USD of single-family credit in 2024. Reinsurance (quota-share, excess-of-loss) stabilized earnings and provided capacity for origination growth. Servicers, fintech and data partners lower friction and improve underwriting outcomes; regulatory and rating standing reduces funding costs.

| Partner | Role | 2024 metric |

|---|---|---|

| Lenders | Distribution | Primary premium source |

| GSEs | Eligibility | >6T USD guarantee |

| Reinsurers | Capital relief | Quota/excess structures |

| Servicers/Data | Ops & insights | Supports $12T mortgage market |

What is included in the product

A comprehensive Essent Business Model Canvas mapping all nine BMC blocks with detailed value propositions, customer segments, channels and revenue streams, reflecting real-world operations and strategic plans; ideal for presentations, investor discussions, and includes SWOT and competitive-advantage insights to support decision-making.

High-level one-page Business Model Canvas that consolidates Essent’s strategy into editable cells, saving hours of formatting while helping teams quickly identify core components for boardroom-ready presentations and collaborative adaptation.

Activities

Risk-based underwriting and pricing

Assess borrower, collateral, and loan structure to set eligibility and rate, using PD/LGD models and overlays that incorporate mortgage-cycle signals and the 2024 FHFA HPI change of about +2.0% YoY. Dynamic pricing balances origination growth against expected losses, targeting disciplined loss outcomes. Guardrails monitor fraud, layered risk, and exceptions with strict escalation thresholds.

Portfolio monitoring and loss mitigation

Track early payment performance, delinquencies, and cures by cohort and trigger tailored interventions—workouts, forbearance coordination, and modifications—to shorten time-to-cure; in 2024 such targeted interventions reduced pooled claim severity by about 20% at leading private mortgage insurers. Optimize outcomes to minimize claim severity and borrower disruption while feeding cohort learnings back into underwriting rules to lower future default risk.

Capital and reinsurance management

Structure and renew quota share and excess-of-loss programs to cap tail exposure and preserve statutory capital. Align capital planning with PMIERs, RBC frameworks and Essent’s internal risk appetite to sustain underwriting capacity. Execute insurance-linked notes to transfer catastrophe layers and smooth earnings volatility. Scenario-test macro and housing stress to inform capacity limits and reinsurance purchase decisions.

Claims adjudication and servicing support

Claims adjudication verifies coverage, documentation, and timelines to ensure fair, timely payouts while coordinating with servicers on property preservation and liquidation to protect collateral value. Teamwork with servicers accelerates recoveries and enforces rescission relief frameworks to limit loss severity. All actions are logged with immutable audit trails to satisfy GSE and regulatory requirements.

- Validate coverage, docs, timelines

- Coordinate preservation & liquidation

- Accelerate recoveries & rescission relief

- Maintain GSE-compliant audit trails

Sales enablement and lender onboarding

Sales enablement and lender onboarding expand approved lender panels and deepen wallet share by embedding pricing engines, APIs, and workflows into LOS platforms to reduce manual handoffs and accelerate turn times; prioritize training on guidelines, products, and operational best practices with 24–48 hour SLA targets to maintain responsiveness and certainty in 2024.

- Grow panels and wallet share

- Integrate pricing engines + LOS APIs

- Train to guidelines & ops best practices

- Monitor 24–48h SLAs for responsiveness

PD/LGD underwriting; dynamic pricing & reinsurance caps; HPI +2.0%

Underwrite using PD/LGD with mortgage-cycle overlays and 2024 FHFA HPI +2.0% YoY; dynamic pricing targets disciplined loss outcomes. Early-pay interventions shortened cures and cut pooled claim severity ~20% in 2024. Structure reinsurance/ILS to cap tail risk per PMIERs/RBC; sales enablement embeds pricing APIs with 24–48h SLAs.

| Metric | 2024 |

|---|---|

| FHFA HPI YoY | +2.0% |

| Pooled claim severity red. | ~20% |

| SLA | 24–48h |

What You See Is What You Get

Business Model Canvas

The Essent Business Model Canvas previewed here is the actual deliverable, not a mockup. It shows the same structured, editable content you’ll receive after purchase. Upon completion of your order you’ll get this exact file ready for editing, presenting, and sharing—no surprises.

Description

Unlock the strategic Business Model Canvas: value props, segments, revenue & costs

Unlock Essent's strategic blueprint with our full Business Model Canvas. This in-depth, editable document reveals value propositions, customer segments, revenue streams and cost drivers—perfect for investors, consultants, and founders. Download the complete Canvas in Word and Excel to benchmark and act.

Partnerships

Mortgage lenders and banks

Mortgage lenders and banks are core distribution partners that originate loans requiring PMI and designate Essent as insurer of record; in 2024 these deep relationships provided enhanced pipeline visibility and early engagement, supporting preferred placement. Collaboration spans underwriting guidelines, pricing, and operational workflows to streamline closings. Scale lenders anchor premium volume and drive product refinement.

Government-sponsored enterprises (GSEs)

Alignment with Fannie Mae and Freddie Mac eligibility and master policy standards is essential, given GSEs guarantee over $6 trillion of U.S. single-family mortgage credit exposures as of 2024. Coordination ensures MI meets credit policy, loan delivery and capital frameworks, reducing buybacks and preserving capital ratios. Joint initiatives streamline rescission relief, QC and loan seasoning rules, enabling insured loans to remain saleable into the secondary market.

Reinsurers and capital markets

In 2024 Essent relied on quota share and excess-of-loss reinsurance to optimize capital efficiency and stabilize earnings. Insurance-linked notes and capital-relief structures broadened risk transfer and investor diversification. Global counterparties provided capacity across cycles, supporting origination growth. Reinsurance terms were calibrated to portfolio mix, macro risk and rating-agency expectations.

Servicers, fintechs, and data providers

Servicers enable payment processing, delinquency reporting, and loss mitigation; U.S. mortgage debt outstanding was about $12 trillion in 2024, underscoring servicing scale. Fintech integrations automate verifications, LOS/POS connectivity, and API flows. Data partners supply credit, property, and fraud insights to tighten underwriting and reduce loss.

- Servicers: payment, reporting, mitigation

- Fintechs: automated verifications, API LOS/POS

- Data: credit, property, fraud signals

- Impact: lower friction, higher decision quality

Regulators and rating agencies

Regulatory alignment sustains Essent’s license to operate and capital adequacy, while rating agencies assess financial strength and claims-paying ability, directly shaping lender confidence. Ongoing dialogue with regulators and agencies promotes methodology transparency and performance benchmarking. Strong regulatory and rating standing reduces funding costs and widens market access.

- Regulatory alignment: capital adequacy

- Ratings: claims-paying ability

- Dialogue: transparency & benchmarking

- Outcome: lower funding costs, broader access

Mortgage lenders drive premium flow; GSEs guarantee 6T USD

Mortgage lenders drive premium flow and preferred placement via deep origination ties; GSE alignment matters as Fannie/Freddie guarantee >6 trillion USD of single-family credit in 2024. Reinsurance (quota-share, excess-of-loss) stabilized earnings and provided capacity for origination growth. Servicers, fintech and data partners lower friction and improve underwriting outcomes; regulatory and rating standing reduces funding costs.

| Partner | Role | 2024 metric |

|---|---|---|

| Lenders | Distribution | Primary premium source |

| GSEs | Eligibility | >6T USD guarantee |

| Reinsurers | Capital relief | Quota/excess structures |

| Servicers/Data | Ops & insights | Supports $12T mortgage market |

What is included in the product

A comprehensive Essent Business Model Canvas mapping all nine BMC blocks with detailed value propositions, customer segments, channels and revenue streams, reflecting real-world operations and strategic plans; ideal for presentations, investor discussions, and includes SWOT and competitive-advantage insights to support decision-making.

High-level one-page Business Model Canvas that consolidates Essent’s strategy into editable cells, saving hours of formatting while helping teams quickly identify core components for boardroom-ready presentations and collaborative adaptation.

Activities

Risk-based underwriting and pricing

Assess borrower, collateral, and loan structure to set eligibility and rate, using PD/LGD models and overlays that incorporate mortgage-cycle signals and the 2024 FHFA HPI change of about +2.0% YoY. Dynamic pricing balances origination growth against expected losses, targeting disciplined loss outcomes. Guardrails monitor fraud, layered risk, and exceptions with strict escalation thresholds.

Portfolio monitoring and loss mitigation

Track early payment performance, delinquencies, and cures by cohort and trigger tailored interventions—workouts, forbearance coordination, and modifications—to shorten time-to-cure; in 2024 such targeted interventions reduced pooled claim severity by about 20% at leading private mortgage insurers. Optimize outcomes to minimize claim severity and borrower disruption while feeding cohort learnings back into underwriting rules to lower future default risk.

Capital and reinsurance management

Structure and renew quota share and excess-of-loss programs to cap tail exposure and preserve statutory capital. Align capital planning with PMIERs, RBC frameworks and Essent’s internal risk appetite to sustain underwriting capacity. Execute insurance-linked notes to transfer catastrophe layers and smooth earnings volatility. Scenario-test macro and housing stress to inform capacity limits and reinsurance purchase decisions.

Claims adjudication and servicing support

Claims adjudication verifies coverage, documentation, and timelines to ensure fair, timely payouts while coordinating with servicers on property preservation and liquidation to protect collateral value. Teamwork with servicers accelerates recoveries and enforces rescission relief frameworks to limit loss severity. All actions are logged with immutable audit trails to satisfy GSE and regulatory requirements.

- Validate coverage, docs, timelines

- Coordinate preservation & liquidation

- Accelerate recoveries & rescission relief

- Maintain GSE-compliant audit trails

Sales enablement and lender onboarding

Sales enablement and lender onboarding expand approved lender panels and deepen wallet share by embedding pricing engines, APIs, and workflows into LOS platforms to reduce manual handoffs and accelerate turn times; prioritize training on guidelines, products, and operational best practices with 24–48 hour SLA targets to maintain responsiveness and certainty in 2024.

- Grow panels and wallet share

- Integrate pricing engines + LOS APIs

- Train to guidelines & ops best practices

- Monitor 24–48h SLAs for responsiveness

PD/LGD underwriting; dynamic pricing & reinsurance caps; HPI +2.0%

Underwrite using PD/LGD with mortgage-cycle overlays and 2024 FHFA HPI +2.0% YoY; dynamic pricing targets disciplined loss outcomes. Early-pay interventions shortened cures and cut pooled claim severity ~20% in 2024. Structure reinsurance/ILS to cap tail risk per PMIERs/RBC; sales enablement embeds pricing APIs with 24–48h SLAs.

| Metric | 2024 |

|---|---|

| FHFA HPI YoY | +2.0% |

| Pooled claim severity red. | ~20% |

| SLA | 24–48h |

What You See Is What You Get

Business Model Canvas

The Essent Business Model Canvas previewed here is the actual deliverable, not a mockup. It shows the same structured, editable content you’ll receive after purchase. Upon completion of your order you’ll get this exact file ready for editing, presenting, and sharing—no surprises.