EssilorLuxottica Boston Consulting Group Matrix

Download Your Competitive Advantage

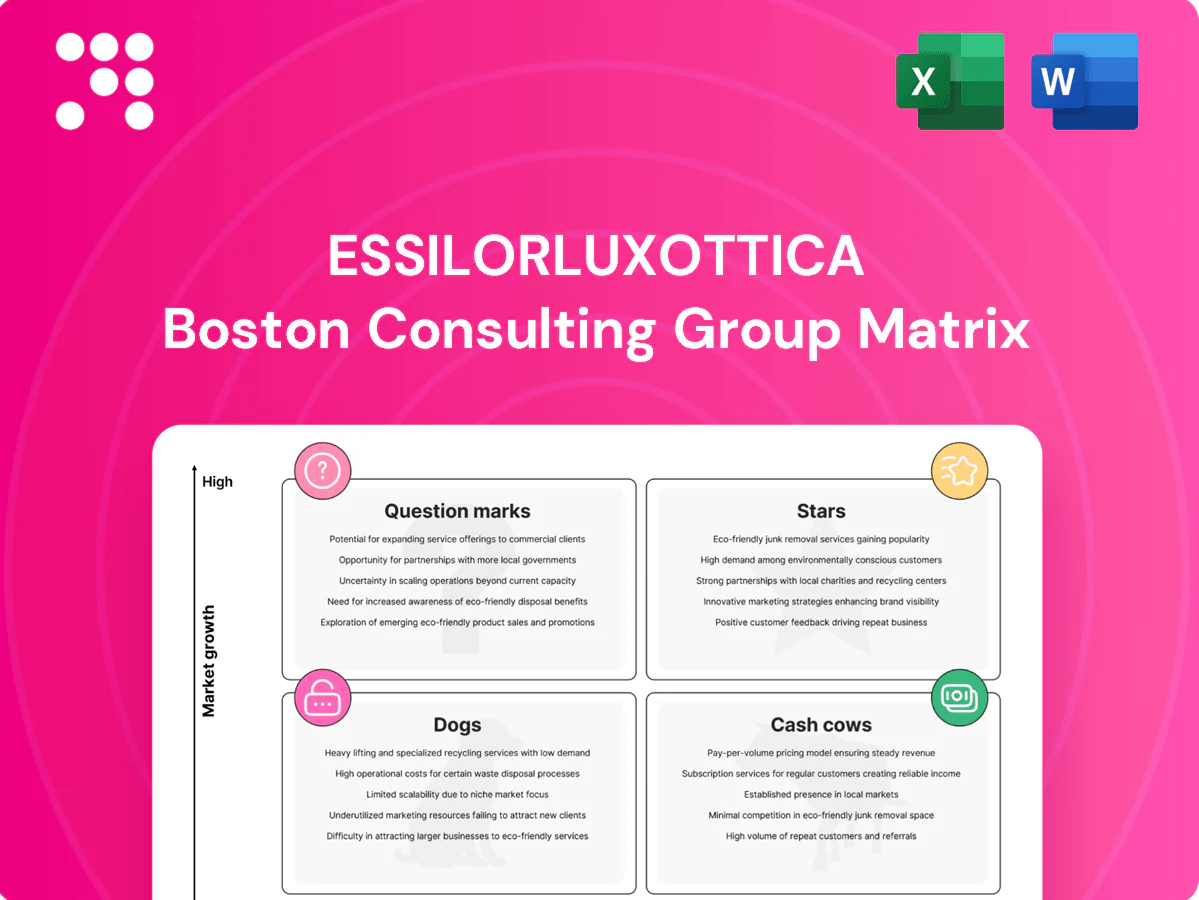

EssilorLuxottica sits at the crossroads of optics and fashion—some product lines are clear Stars, others look like Cash Cows, and a few categories raise real Question Marks if market trends shift. This snapshot teases where value is created and where resources might be leaking, but the full BCG Matrix puts every brand and segment into crisp quadrants with data-backed recommendations. Purchase the complete report for detailed placements, strategic moves, and Word + Excel files you can use to reallocate capital and drive growth.

Stars

Ray-Ban core sunglasses

Ray-Ban remains the iconic core of EssilorLuxottica’s premium sun portfolio in 2024, delivering the largest share of traffic across retail and e‑commerce and anchoring the company’s sun category strength. The global premium sunglasses segment continued to grow in 2024, so sustained spend on brand heat and strategic placements is required to defend share. Continued collabs and limited drops keep the product pipeline fresh and acquisition efficient. Hold share now and milk margins later as market growth stabilizes.

Oakley performance eyewear

Oakley sits in the Stars quadrant as a high-growth niche in sport and outdoor with strong tech credibility tied to PRIZM optics and performance design. It delivers superior margins and deep customer loyalty, though revenue growth relies on promotions and heavy athlete sponsorships. As the active category expands, Oakley is well positioned to capture share. Maintain aggressive R&D and channel visibility to sustain momentum.

Varilux progressive lenses

Varilux progressive lenses sit as a Star in EssilorLuxottica’s BCG matrix, leading the structurally growing presbyopia market. Continual R&D and pro-channel education sustain technological and commercial leadership but require significant ongoing investment from the group (EssilorLuxottica reported €22.7bn sales in 2023). Durable demand is underpinned by ~1.8 billion people with presbyopia/near vision impairment (2020); preserving clinical proof and premium pricing locks in dominance.

Crizal and premium coatings

Crizal and premium coatings are BCG Stars for EssilorLuxottica, driven by high attach rates, strong perceived value, and solid ECP brand recognition; 2024 channel feedback shows coatings grow with lens upgrades and screen-fatigue demand. Sustaining conversion requires training, in-office demos, and strategic bundling; continue tiered offers and promotions to defend share.

- High attach rates

- Strong ECP recognition

- Market growth via upgrades/screen fatigue

- Needs training, demos, bundling

- Push tiered offers

Omnichannel retail ecosystem

Omnichannel retail ecosystem acts as a flywheel for EssilorLuxottica, where integrated retail, e‑commerce and lab networks boost traffic, data capture and convenience to expand markets; group pro forma sales circa €22.1bn and a retail footprint of ~9,000 stores plus ~150,000 partner points (2024) underwrite this model. Heavy capex and operating costs persist, but scale delivers margin leverage as volumes climb, so invest where new stores and digital channels drive incremental demand.

- Flywheel: integrated stores + e‑comm + labs

- Scale: ~9,000 stores, ~150,000 partner points (2024)

- Finance: pro forma sales ~€22.1bn (2024)

- Strategy: prioritize store + digital openings for incremental demand

Group scale (€22.1bn, ~9,000 stores) underwrites premium push

Ray-Ban, Oakley, Varilux and Crizal are Stars—high share in growing segments requiring sustained marketing, R&D and pro‑channel investment to convert growth into durable profits. Group scale (pro forma sales ~€22.1bn, ~9,000 stores, ~150,000 partner points in 2024) underwrites this push. Prioritize premium pricing, channel training and targeted drops to defend and expand share.

| Brand | Role | 2024 KPI |

|---|---|---|

| Ray-Ban | Premium Sun Star | Top traffic, global premium growth |

| Oakley | Sport Tech Star | High margins, strong PRIZM demand |

| Varilux/Crizal | Optical Stars | Presbyopia ~1.8bn (2020), high attach |

What is included in the product

BCG Matrix of EssilorLuxottica: identifies Stars, Cash Cows, Question Marks, Dogs with strategic investment, hold or divest guidance.

One-page BCG Matrix for EssilorLuxottica — highlights pain points and prioritizes units for swift C-suite decisions.

Cash Cows

LensCrafters and mature optical retail

LensCrafters, with roughly 1,100 North American locations within EssilorLuxottica’s ~9,000-store retail network, occupies a high-share position in mature markets with steady footfall. Category volume growth is muted, but the chain delivers strong cash yield and predictable upsell through eyewear and lens upgrades. Incremental margin gains come from operations efficiency and product mix; strategy: maintain and optimize the estate, avoid heavy reinvestment.

Sunglass Hut in established regions

Sunglass Hut, with over 3,000 stores inside EssilorLuxottica’s 9,000+ global retail network in 2024, sits in prime locations and tourist hubs (airports, malls) with a proven format. Growth is modest while retail margins remain healthy; inventory turns and seasonal peaks/dips sustain cash generation. Operational focus on productivity metrics and rent renegotiations is driving incremental free cash flow expansion.

Licensed fashion frames portfolio

Licensed fashion frames from top houses drive volume with limited incremental R&D, functioning as core cash cows for EssilorLuxottica. Category growth remains slow while the roster reliably generates surplus cash, supporting margins and capex elsewhere. Management should prioritize renewing high-return licenses and pruning underperformers to protect royalty streams. A tight assortment ensures high sell-through and steady royalty inflows.

Lab network and supply chain services

Lab network and supply chain services are cash cows for EssilorLuxottica, with the company operating the world’s largest integrated lens and frame logistics system that processes hundreds of millions of lenses annually and supports global retail and wholesale channels. The mature network delivers cost advantages and reliability versus smaller players; targeted CAPEX in 2023–24 focuses on automation to raise throughput and improve gross margins. Continuous efficiency drives squeeze unit costs while protecting sub-72-hour service levels in priority markets.

Core single-vision Rx lenses

Core single-vision Rx lenses are a big, replacement-driven base business for EssilorLuxottica: predictable volume with modest margin expansion rather than high growth, delivering steady cash flow by winning on consistent supply, tiered pricing and broad distribution coverage.

~9,000-store eyewear network: steady retail cash flow, labs process hundreds of millions/yr

LensCrafters and Sunglass Hut (≈1,100 and >3,000 stores within EssilorLuxottica’s ~9,000-store network in 2024) are mature, high-share cash cows delivering steady margins and predictable upsell. The global lab/logistics network processes hundreds of millions of lenses/year, lowering unit costs after 2023–24 automation CAPEX. Core single-vision lenses are replacement-driven, stable cash generators.

| Metric | 2024 |

|---|---|

| Total retail stores | ~9,000+ |

| LensCrafters | ~1,100 NA |

| Sunglass Hut | >3,000 |

| Lab throughput | hundreds of millions lenses/yr |

Preview = Final Product

EssilorLuxottica BCG Matrix

The file you’re previewing is the exact EssilorLuxottica BCG Matrix report you’ll receive after purchase. No watermarks, no placeholders—just a fully formatted, ready-to-use strategic matrix built for clarity. It’s editable, printable, and tailored for presentations or boardroom review. Buy once and download instantly—no surprises, just professional analysis you can act on.

Download Your Competitive Advantage

EssilorLuxottica sits at the crossroads of optics and fashion—some product lines are clear Stars, others look like Cash Cows, and a few categories raise real Question Marks if market trends shift. This snapshot teases where value is created and where resources might be leaking, but the full BCG Matrix puts every brand and segment into crisp quadrants with data-backed recommendations. Purchase the complete report for detailed placements, strategic moves, and Word + Excel files you can use to reallocate capital and drive growth.

Stars

Ray-Ban core sunglasses

Ray-Ban remains the iconic core of EssilorLuxottica’s premium sun portfolio in 2024, delivering the largest share of traffic across retail and e‑commerce and anchoring the company’s sun category strength. The global premium sunglasses segment continued to grow in 2024, so sustained spend on brand heat and strategic placements is required to defend share. Continued collabs and limited drops keep the product pipeline fresh and acquisition efficient. Hold share now and milk margins later as market growth stabilizes.

Oakley performance eyewear

Oakley sits in the Stars quadrant as a high-growth niche in sport and outdoor with strong tech credibility tied to PRIZM optics and performance design. It delivers superior margins and deep customer loyalty, though revenue growth relies on promotions and heavy athlete sponsorships. As the active category expands, Oakley is well positioned to capture share. Maintain aggressive R&D and channel visibility to sustain momentum.

Varilux progressive lenses

Varilux progressive lenses sit as a Star in EssilorLuxottica’s BCG matrix, leading the structurally growing presbyopia market. Continual R&D and pro-channel education sustain technological and commercial leadership but require significant ongoing investment from the group (EssilorLuxottica reported €22.7bn sales in 2023). Durable demand is underpinned by ~1.8 billion people with presbyopia/near vision impairment (2020); preserving clinical proof and premium pricing locks in dominance.

Crizal and premium coatings

Crizal and premium coatings are BCG Stars for EssilorLuxottica, driven by high attach rates, strong perceived value, and solid ECP brand recognition; 2024 channel feedback shows coatings grow with lens upgrades and screen-fatigue demand. Sustaining conversion requires training, in-office demos, and strategic bundling; continue tiered offers and promotions to defend share.

- High attach rates

- Strong ECP recognition

- Market growth via upgrades/screen fatigue

- Needs training, demos, bundling

- Push tiered offers

Omnichannel retail ecosystem

Omnichannel retail ecosystem acts as a flywheel for EssilorLuxottica, where integrated retail, e‑commerce and lab networks boost traffic, data capture and convenience to expand markets; group pro forma sales circa €22.1bn and a retail footprint of ~9,000 stores plus ~150,000 partner points (2024) underwrite this model. Heavy capex and operating costs persist, but scale delivers margin leverage as volumes climb, so invest where new stores and digital channels drive incremental demand.

- Flywheel: integrated stores + e‑comm + labs

- Scale: ~9,000 stores, ~150,000 partner points (2024)

- Finance: pro forma sales ~€22.1bn (2024)

- Strategy: prioritize store + digital openings for incremental demand

Group scale (€22.1bn, ~9,000 stores) underwrites premium push

Ray-Ban, Oakley, Varilux and Crizal are Stars—high share in growing segments requiring sustained marketing, R&D and pro‑channel investment to convert growth into durable profits. Group scale (pro forma sales ~€22.1bn, ~9,000 stores, ~150,000 partner points in 2024) underwrites this push. Prioritize premium pricing, channel training and targeted drops to defend and expand share.

| Brand | Role | 2024 KPI |

|---|---|---|

| Ray-Ban | Premium Sun Star | Top traffic, global premium growth |

| Oakley | Sport Tech Star | High margins, strong PRIZM demand |

| Varilux/Crizal | Optical Stars | Presbyopia ~1.8bn (2020), high attach |

What is included in the product

BCG Matrix of EssilorLuxottica: identifies Stars, Cash Cows, Question Marks, Dogs with strategic investment, hold or divest guidance.

One-page BCG Matrix for EssilorLuxottica — highlights pain points and prioritizes units for swift C-suite decisions.

Cash Cows

LensCrafters and mature optical retail

LensCrafters, with roughly 1,100 North American locations within EssilorLuxottica’s ~9,000-store retail network, occupies a high-share position in mature markets with steady footfall. Category volume growth is muted, but the chain delivers strong cash yield and predictable upsell through eyewear and lens upgrades. Incremental margin gains come from operations efficiency and product mix; strategy: maintain and optimize the estate, avoid heavy reinvestment.

Sunglass Hut in established regions

Sunglass Hut, with over 3,000 stores inside EssilorLuxottica’s 9,000+ global retail network in 2024, sits in prime locations and tourist hubs (airports, malls) with a proven format. Growth is modest while retail margins remain healthy; inventory turns and seasonal peaks/dips sustain cash generation. Operational focus on productivity metrics and rent renegotiations is driving incremental free cash flow expansion.

Licensed fashion frames portfolio

Licensed fashion frames from top houses drive volume with limited incremental R&D, functioning as core cash cows for EssilorLuxottica. Category growth remains slow while the roster reliably generates surplus cash, supporting margins and capex elsewhere. Management should prioritize renewing high-return licenses and pruning underperformers to protect royalty streams. A tight assortment ensures high sell-through and steady royalty inflows.

Lab network and supply chain services

Lab network and supply chain services are cash cows for EssilorLuxottica, with the company operating the world’s largest integrated lens and frame logistics system that processes hundreds of millions of lenses annually and supports global retail and wholesale channels. The mature network delivers cost advantages and reliability versus smaller players; targeted CAPEX in 2023–24 focuses on automation to raise throughput and improve gross margins. Continuous efficiency drives squeeze unit costs while protecting sub-72-hour service levels in priority markets.

Core single-vision Rx lenses

Core single-vision Rx lenses are a big, replacement-driven base business for EssilorLuxottica: predictable volume with modest margin expansion rather than high growth, delivering steady cash flow by winning on consistent supply, tiered pricing and broad distribution coverage.

~9,000-store eyewear network: steady retail cash flow, labs process hundreds of millions/yr

LensCrafters and Sunglass Hut (≈1,100 and >3,000 stores within EssilorLuxottica’s ~9,000-store network in 2024) are mature, high-share cash cows delivering steady margins and predictable upsell. The global lab/logistics network processes hundreds of millions of lenses/year, lowering unit costs after 2023–24 automation CAPEX. Core single-vision lenses are replacement-driven, stable cash generators.

| Metric | 2024 |

|---|---|

| Total retail stores | ~9,000+ |

| LensCrafters | ~1,100 NA |

| Sunglass Hut | >3,000 |

| Lab throughput | hundreds of millions lenses/yr |

Preview = Final Product

EssilorLuxottica BCG Matrix

The file you’re previewing is the exact EssilorLuxottica BCG Matrix report you’ll receive after purchase. No watermarks, no placeholders—just a fully formatted, ready-to-use strategic matrix built for clarity. It’s editable, printable, and tailored for presentations or boardroom review. Buy once and download instantly—no surprises, just professional analysis you can act on.

Original: $10.00

-65%$10.00

$3.50Description

Download Your Competitive Advantage

EssilorLuxottica sits at the crossroads of optics and fashion—some product lines are clear Stars, others look like Cash Cows, and a few categories raise real Question Marks if market trends shift. This snapshot teases where value is created and where resources might be leaking, but the full BCG Matrix puts every brand and segment into crisp quadrants with data-backed recommendations. Purchase the complete report for detailed placements, strategic moves, and Word + Excel files you can use to reallocate capital and drive growth.

Stars

Ray-Ban core sunglasses

Ray-Ban remains the iconic core of EssilorLuxottica’s premium sun portfolio in 2024, delivering the largest share of traffic across retail and e‑commerce and anchoring the company’s sun category strength. The global premium sunglasses segment continued to grow in 2024, so sustained spend on brand heat and strategic placements is required to defend share. Continued collabs and limited drops keep the product pipeline fresh and acquisition efficient. Hold share now and milk margins later as market growth stabilizes.

Oakley performance eyewear

Oakley sits in the Stars quadrant as a high-growth niche in sport and outdoor with strong tech credibility tied to PRIZM optics and performance design. It delivers superior margins and deep customer loyalty, though revenue growth relies on promotions and heavy athlete sponsorships. As the active category expands, Oakley is well positioned to capture share. Maintain aggressive R&D and channel visibility to sustain momentum.

Varilux progressive lenses

Varilux progressive lenses sit as a Star in EssilorLuxottica’s BCG matrix, leading the structurally growing presbyopia market. Continual R&D and pro-channel education sustain technological and commercial leadership but require significant ongoing investment from the group (EssilorLuxottica reported €22.7bn sales in 2023). Durable demand is underpinned by ~1.8 billion people with presbyopia/near vision impairment (2020); preserving clinical proof and premium pricing locks in dominance.

Crizal and premium coatings

Crizal and premium coatings are BCG Stars for EssilorLuxottica, driven by high attach rates, strong perceived value, and solid ECP brand recognition; 2024 channel feedback shows coatings grow with lens upgrades and screen-fatigue demand. Sustaining conversion requires training, in-office demos, and strategic bundling; continue tiered offers and promotions to defend share.

- High attach rates

- Strong ECP recognition

- Market growth via upgrades/screen fatigue

- Needs training, demos, bundling

- Push tiered offers

Omnichannel retail ecosystem

Omnichannel retail ecosystem acts as a flywheel for EssilorLuxottica, where integrated retail, e‑commerce and lab networks boost traffic, data capture and convenience to expand markets; group pro forma sales circa €22.1bn and a retail footprint of ~9,000 stores plus ~150,000 partner points (2024) underwrite this model. Heavy capex and operating costs persist, but scale delivers margin leverage as volumes climb, so invest where new stores and digital channels drive incremental demand.

- Flywheel: integrated stores + e‑comm + labs

- Scale: ~9,000 stores, ~150,000 partner points (2024)

- Finance: pro forma sales ~€22.1bn (2024)

- Strategy: prioritize store + digital openings for incremental demand

Group scale (€22.1bn, ~9,000 stores) underwrites premium push

Ray-Ban, Oakley, Varilux and Crizal are Stars—high share in growing segments requiring sustained marketing, R&D and pro‑channel investment to convert growth into durable profits. Group scale (pro forma sales ~€22.1bn, ~9,000 stores, ~150,000 partner points in 2024) underwrites this push. Prioritize premium pricing, channel training and targeted drops to defend and expand share.

| Brand | Role | 2024 KPI |

|---|---|---|

| Ray-Ban | Premium Sun Star | Top traffic, global premium growth |

| Oakley | Sport Tech Star | High margins, strong PRIZM demand |

| Varilux/Crizal | Optical Stars | Presbyopia ~1.8bn (2020), high attach |

What is included in the product

BCG Matrix of EssilorLuxottica: identifies Stars, Cash Cows, Question Marks, Dogs with strategic investment, hold or divest guidance.

One-page BCG Matrix for EssilorLuxottica — highlights pain points and prioritizes units for swift C-suite decisions.

Cash Cows

LensCrafters and mature optical retail

LensCrafters, with roughly 1,100 North American locations within EssilorLuxottica’s ~9,000-store retail network, occupies a high-share position in mature markets with steady footfall. Category volume growth is muted, but the chain delivers strong cash yield and predictable upsell through eyewear and lens upgrades. Incremental margin gains come from operations efficiency and product mix; strategy: maintain and optimize the estate, avoid heavy reinvestment.

Sunglass Hut in established regions

Sunglass Hut, with over 3,000 stores inside EssilorLuxottica’s 9,000+ global retail network in 2024, sits in prime locations and tourist hubs (airports, malls) with a proven format. Growth is modest while retail margins remain healthy; inventory turns and seasonal peaks/dips sustain cash generation. Operational focus on productivity metrics and rent renegotiations is driving incremental free cash flow expansion.

Licensed fashion frames portfolio

Licensed fashion frames from top houses drive volume with limited incremental R&D, functioning as core cash cows for EssilorLuxottica. Category growth remains slow while the roster reliably generates surplus cash, supporting margins and capex elsewhere. Management should prioritize renewing high-return licenses and pruning underperformers to protect royalty streams. A tight assortment ensures high sell-through and steady royalty inflows.

Lab network and supply chain services

Lab network and supply chain services are cash cows for EssilorLuxottica, with the company operating the world’s largest integrated lens and frame logistics system that processes hundreds of millions of lenses annually and supports global retail and wholesale channels. The mature network delivers cost advantages and reliability versus smaller players; targeted CAPEX in 2023–24 focuses on automation to raise throughput and improve gross margins. Continuous efficiency drives squeeze unit costs while protecting sub-72-hour service levels in priority markets.

Core single-vision Rx lenses

Core single-vision Rx lenses are a big, replacement-driven base business for EssilorLuxottica: predictable volume with modest margin expansion rather than high growth, delivering steady cash flow by winning on consistent supply, tiered pricing and broad distribution coverage.

~9,000-store eyewear network: steady retail cash flow, labs process hundreds of millions/yr

LensCrafters and Sunglass Hut (≈1,100 and >3,000 stores within EssilorLuxottica’s ~9,000-store network in 2024) are mature, high-share cash cows delivering steady margins and predictable upsell. The global lab/logistics network processes hundreds of millions of lenses/year, lowering unit costs after 2023–24 automation CAPEX. Core single-vision lenses are replacement-driven, stable cash generators.

| Metric | 2024 |

|---|---|

| Total retail stores | ~9,000+ |

| LensCrafters | ~1,100 NA |

| Sunglass Hut | >3,000 |

| Lab throughput | hundreds of millions lenses/yr |

Preview = Final Product

EssilorLuxottica BCG Matrix

The file you’re previewing is the exact EssilorLuxottica BCG Matrix report you’ll receive after purchase. No watermarks, no placeholders—just a fully formatted, ready-to-use strategic matrix built for clarity. It’s editable, printable, and tailored for presentations or boardroom review. Buy once and download instantly—no surprises, just professional analysis you can act on.