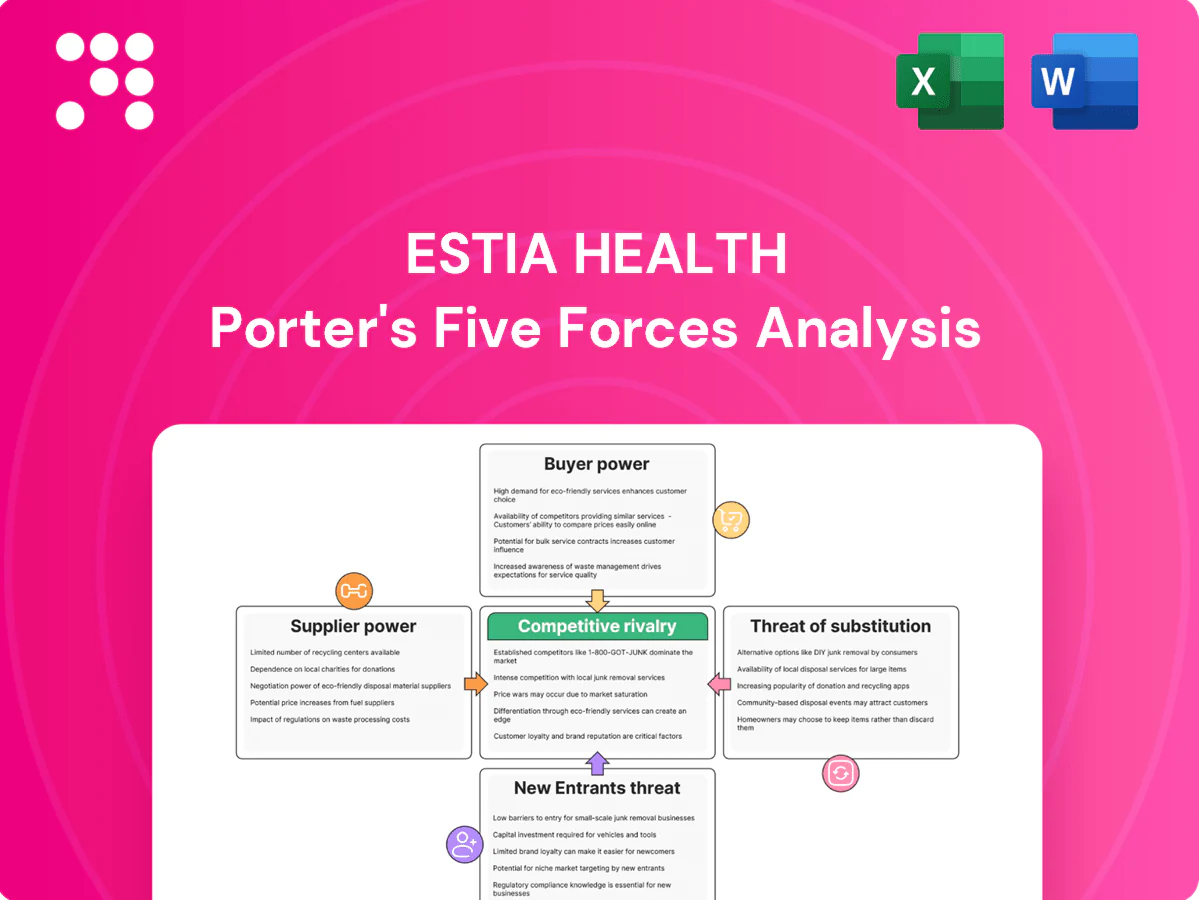

Estia Health Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Estia Health operates in a highly regulated Australian aged-care market where regulatory change, rising staffing costs and fragmented demand intensify rivalry and supplier (labor) power, while barriers to entry and brand scale limit new entrants; substitutes like home care exert moderate pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Estia Health’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Skilled labor scarcity

Registered nurses, carers and allied health staff remain scarce, pushing wage costs higher after Fair Work Commission-awarded wage increases of roughly 15–19% across 2023–24; mandatory 24/7 RN coverage and increased staffing minutes under recent aged‑care reforms further strengthen supplier leverage. Overtime, agency staffing reliance and retention bonuses have raised cost volatility and operating cashflow pressure. Union-negotiated awards set wage floors that limit Estia Health’s bargaining latitude.

Healthcare inputs

Essential medical supplies, pharmaceuticals and infection-control products have limited alternate sources; with about 243,000 Australians in residential aged care (AIHW 2023), demand is steady and compliance-grade products narrow substitution, keeping prices firm. Bulk contracts mitigate volatility but shocks such as the COVID-19 PPE shortages strained availability, and suppliers can pass through cost increases tied to higher regulatory standards.

Food and utilities

Catering quality standards and resident expectations sharply limit switching of food vendors, raising supplier leverage for specialised menus and dietary requirements. Energy and utilities remain essential with limited regional competition, and Australian CPI-driven input price inflation of about 5.9% in 2024 strained margins under government-indexed revenue models. Long-term supply agreements reduce volatility but do not eliminate exposure to commodity and wage-driven cost shocks.

Property and maintenance

- Specialized fit-outs favor certified builders

- Capex-led refurb consolidates contractor power

- Compliance limits vendor switching

- Long lead times (often 6–18 months) boost supplier leverage

Tech and compliance systems

- High integration and training raise switching costs

- Accreditation and cybersecurity requirements entrench vendors

- Contracts often include multi-year terms and recurring support fees

Margins hit by 15–19% wages, 5.9% CPI, 6–18m delays

Supplier power is high: nursing workforce shortages and 15–19% Fair Work wage rises in 2023–24 squeeze margins and raise operating costs. Compliance-driven capital works and 6–18 month lead times limit vendor switching; multi-year IT contracts (3–5 years) embed suppliers. Essential consumables and utilities face firm pricing with 2024 CPI ~5.9% increasing pass-through risk.

| Supplier | Impact | 2024 metric |

|---|---|---|

| Labor | High | 15–19% wage rise |

| Consumables | Medium-High | CPI 5.9% |

| Builders/IT | High | Lead times 6–18m; contracts 3–5y |

What is included in the product

Tailored Porter’s Five Forces analysis for Estia Health uncovering competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and rivalry dynamics. Provides strategic commentary on regulatory, operational, and demographic factors shaping pricing, margins, and market positioning.

A clear, one-sheet Porter's Five Forces for Estia Health—quickly highlights competitive pressures, regulatory risk and supplier dynamics to guide boardroom decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Government price-setter

Commonwealth subsidies and AN-ACC funding, introduced on 1 October 2022, constitute the primary revenue base for Estia Health, making government policy the de facto price-setter. Indexation and AN-ACC recalibrations directly impact margins since providers have little scope to negotiate higher care rates with the payer. Operational compliance and quality outcomes routinely determine funding levels and expose providers to sanctions or funding adjustments.

Residents and families

Choice among local homes gives families leverage over accommodation preferences, enabling moves for location, room type or contract terms. Reputation and Aged Care Quality star ratings strongly drive switching decisions. Negative publicity can quickly dent occupancy in a sector where national residential aged care occupancy averaged about 88% in 2023–24 (AIHW). Service differentiation on amenities and clinical programs can reduce price sensitivity for extras.

Not-for-profit competition

Not-for-profit rivals can accept lower margins, raising buyer expectations for value and pressuring Estia on pricing and service mix. Community trust in NFPs often shifts resident preference away from for-profits, strengthening customers bargaining leverage. Buyers cite mission alignment to negotiate enhanced amenities and care levels. Donations and grants enable NFPs to bundle services that for-profits may struggle to match.

Transparency and ratings

Public quality indicators and 2024 complaints data published by the Aged Care Quality and Safety Commission increase buyer scrutiny of Estia Health, making performance highly visible to residents and families. Comparability across homes via public ratings heightens customer bargaining power as customers can easily switch or demand concessions. Poor metrics force Estia to offer discounts or additional services to retain residents. Continuous improvement in care and transparency is required to defend occupancy.

- Public 2024 complaints data raises scrutiny

- Ratings enable easy home comparison

- Poor metrics -> discounts/refunds pressure

- Ongoing quality improvements defend occupancy

Co-payments and extras

Co-payments and extras give residents leverage: in 2024 many negotiated refundable deposits and tailored service bundles, pressuring average per-resident revenue as price-sensitive buyers down-tier extras during cost-of-living strain. Mix shifts toward basic packages diluted ARPR, while targeted customization and bundled offerings supported sustained willingness to pay.

- Negotiable refundable deposits

- Down‑tiering of extras under cost pressure

- Mix shifts dilute ARPR

- Customization preserves willingness to pay

AN-ACC funding caps pricing; 88% occupancy and 2024 complaints raise switching risk

Government-set AN-ACC funding (effective 1 Oct 2022) is the primary revenue driver, limiting Estia’s price flexibility; sector occupancy averaged 88% in 2023–24 (AIHW), intensifying competition for residents. Public 2024 ACQSC complaints and star ratings raise switching risk and force concessions on extras and deposits; NFP competitors’ subsidy-differentials further press margins.

| Metric | Value | Source |

|---|---|---|

| AN-ACC start | 1 Oct 2022 | Commonwealth |

| Occupancy | 88% (2023–24) | AIHW |

| Visibility | High (2024 ACQSC complaints) | ACQSC |

Preview the Actual Deliverable

Estia Health Porter's Five Forces Analysis

This preview shows the exact Estia Health Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed here is the full, professionally formatted analysis ready for download and use the moment you buy. You're viewing the final deliverable and will get instant access to this same file after payment. No surprises, no setup required.

Don't Miss the Bigger Picture

Estia Health operates in a highly regulated Australian aged-care market where regulatory change, rising staffing costs and fragmented demand intensify rivalry and supplier (labor) power, while barriers to entry and brand scale limit new entrants; substitutes like home care exert moderate pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Estia Health’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Skilled labor scarcity

Registered nurses, carers and allied health staff remain scarce, pushing wage costs higher after Fair Work Commission-awarded wage increases of roughly 15–19% across 2023–24; mandatory 24/7 RN coverage and increased staffing minutes under recent aged‑care reforms further strengthen supplier leverage. Overtime, agency staffing reliance and retention bonuses have raised cost volatility and operating cashflow pressure. Union-negotiated awards set wage floors that limit Estia Health’s bargaining latitude.

Healthcare inputs

Essential medical supplies, pharmaceuticals and infection-control products have limited alternate sources; with about 243,000 Australians in residential aged care (AIHW 2023), demand is steady and compliance-grade products narrow substitution, keeping prices firm. Bulk contracts mitigate volatility but shocks such as the COVID-19 PPE shortages strained availability, and suppliers can pass through cost increases tied to higher regulatory standards.

Food and utilities

Catering quality standards and resident expectations sharply limit switching of food vendors, raising supplier leverage for specialised menus and dietary requirements. Energy and utilities remain essential with limited regional competition, and Australian CPI-driven input price inflation of about 5.9% in 2024 strained margins under government-indexed revenue models. Long-term supply agreements reduce volatility but do not eliminate exposure to commodity and wage-driven cost shocks.

Property and maintenance

- Specialized fit-outs favor certified builders

- Capex-led refurb consolidates contractor power

- Compliance limits vendor switching

- Long lead times (often 6–18 months) boost supplier leverage

Tech and compliance systems

- High integration and training raise switching costs

- Accreditation and cybersecurity requirements entrench vendors

- Contracts often include multi-year terms and recurring support fees

Margins hit by 15–19% wages, 5.9% CPI, 6–18m delays

Supplier power is high: nursing workforce shortages and 15–19% Fair Work wage rises in 2023–24 squeeze margins and raise operating costs. Compliance-driven capital works and 6–18 month lead times limit vendor switching; multi-year IT contracts (3–5 years) embed suppliers. Essential consumables and utilities face firm pricing with 2024 CPI ~5.9% increasing pass-through risk.

| Supplier | Impact | 2024 metric |

|---|---|---|

| Labor | High | 15–19% wage rise |

| Consumables | Medium-High | CPI 5.9% |

| Builders/IT | High | Lead times 6–18m; contracts 3–5y |

What is included in the product

Tailored Porter’s Five Forces analysis for Estia Health uncovering competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and rivalry dynamics. Provides strategic commentary on regulatory, operational, and demographic factors shaping pricing, margins, and market positioning.

A clear, one-sheet Porter's Five Forces for Estia Health—quickly highlights competitive pressures, regulatory risk and supplier dynamics to guide boardroom decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Government price-setter

Commonwealth subsidies and AN-ACC funding, introduced on 1 October 2022, constitute the primary revenue base for Estia Health, making government policy the de facto price-setter. Indexation and AN-ACC recalibrations directly impact margins since providers have little scope to negotiate higher care rates with the payer. Operational compliance and quality outcomes routinely determine funding levels and expose providers to sanctions or funding adjustments.

Residents and families

Choice among local homes gives families leverage over accommodation preferences, enabling moves for location, room type or contract terms. Reputation and Aged Care Quality star ratings strongly drive switching decisions. Negative publicity can quickly dent occupancy in a sector where national residential aged care occupancy averaged about 88% in 2023–24 (AIHW). Service differentiation on amenities and clinical programs can reduce price sensitivity for extras.

Not-for-profit competition

Not-for-profit rivals can accept lower margins, raising buyer expectations for value and pressuring Estia on pricing and service mix. Community trust in NFPs often shifts resident preference away from for-profits, strengthening customers bargaining leverage. Buyers cite mission alignment to negotiate enhanced amenities and care levels. Donations and grants enable NFPs to bundle services that for-profits may struggle to match.

Transparency and ratings

Public quality indicators and 2024 complaints data published by the Aged Care Quality and Safety Commission increase buyer scrutiny of Estia Health, making performance highly visible to residents and families. Comparability across homes via public ratings heightens customer bargaining power as customers can easily switch or demand concessions. Poor metrics force Estia to offer discounts or additional services to retain residents. Continuous improvement in care and transparency is required to defend occupancy.

- Public 2024 complaints data raises scrutiny

- Ratings enable easy home comparison

- Poor metrics -> discounts/refunds pressure

- Ongoing quality improvements defend occupancy

Co-payments and extras

Co-payments and extras give residents leverage: in 2024 many negotiated refundable deposits and tailored service bundles, pressuring average per-resident revenue as price-sensitive buyers down-tier extras during cost-of-living strain. Mix shifts toward basic packages diluted ARPR, while targeted customization and bundled offerings supported sustained willingness to pay.

- Negotiable refundable deposits

- Down‑tiering of extras under cost pressure

- Mix shifts dilute ARPR

- Customization preserves willingness to pay

AN-ACC funding caps pricing; 88% occupancy and 2024 complaints raise switching risk

Government-set AN-ACC funding (effective 1 Oct 2022) is the primary revenue driver, limiting Estia’s price flexibility; sector occupancy averaged 88% in 2023–24 (AIHW), intensifying competition for residents. Public 2024 ACQSC complaints and star ratings raise switching risk and force concessions on extras and deposits; NFP competitors’ subsidy-differentials further press margins.

| Metric | Value | Source |

|---|---|---|

| AN-ACC start | 1 Oct 2022 | Commonwealth |

| Occupancy | 88% (2023–24) | AIHW |

| Visibility | High (2024 ACQSC complaints) | ACQSC |

Preview the Actual Deliverable

Estia Health Porter's Five Forces Analysis

This preview shows the exact Estia Health Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed here is the full, professionally formatted analysis ready for download and use the moment you buy. You're viewing the final deliverable and will get instant access to this same file after payment. No surprises, no setup required.

Description

Don't Miss the Bigger Picture

Estia Health operates in a highly regulated Australian aged-care market where regulatory change, rising staffing costs and fragmented demand intensify rivalry and supplier (labor) power, while barriers to entry and brand scale limit new entrants; substitutes like home care exert moderate pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Estia Health’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Skilled labor scarcity

Registered nurses, carers and allied health staff remain scarce, pushing wage costs higher after Fair Work Commission-awarded wage increases of roughly 15–19% across 2023–24; mandatory 24/7 RN coverage and increased staffing minutes under recent aged‑care reforms further strengthen supplier leverage. Overtime, agency staffing reliance and retention bonuses have raised cost volatility and operating cashflow pressure. Union-negotiated awards set wage floors that limit Estia Health’s bargaining latitude.

Healthcare inputs

Essential medical supplies, pharmaceuticals and infection-control products have limited alternate sources; with about 243,000 Australians in residential aged care (AIHW 2023), demand is steady and compliance-grade products narrow substitution, keeping prices firm. Bulk contracts mitigate volatility but shocks such as the COVID-19 PPE shortages strained availability, and suppliers can pass through cost increases tied to higher regulatory standards.

Food and utilities

Catering quality standards and resident expectations sharply limit switching of food vendors, raising supplier leverage for specialised menus and dietary requirements. Energy and utilities remain essential with limited regional competition, and Australian CPI-driven input price inflation of about 5.9% in 2024 strained margins under government-indexed revenue models. Long-term supply agreements reduce volatility but do not eliminate exposure to commodity and wage-driven cost shocks.

Property and maintenance

- Specialized fit-outs favor certified builders

- Capex-led refurb consolidates contractor power

- Compliance limits vendor switching

- Long lead times (often 6–18 months) boost supplier leverage

Tech and compliance systems

- High integration and training raise switching costs

- Accreditation and cybersecurity requirements entrench vendors

- Contracts often include multi-year terms and recurring support fees

Margins hit by 15–19% wages, 5.9% CPI, 6–18m delays

Supplier power is high: nursing workforce shortages and 15–19% Fair Work wage rises in 2023–24 squeeze margins and raise operating costs. Compliance-driven capital works and 6–18 month lead times limit vendor switching; multi-year IT contracts (3–5 years) embed suppliers. Essential consumables and utilities face firm pricing with 2024 CPI ~5.9% increasing pass-through risk.

| Supplier | Impact | 2024 metric |

|---|---|---|

| Labor | High | 15–19% wage rise |

| Consumables | Medium-High | CPI 5.9% |

| Builders/IT | High | Lead times 6–18m; contracts 3–5y |

What is included in the product

Tailored Porter’s Five Forces analysis for Estia Health uncovering competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and rivalry dynamics. Provides strategic commentary on regulatory, operational, and demographic factors shaping pricing, margins, and market positioning.

A clear, one-sheet Porter's Five Forces for Estia Health—quickly highlights competitive pressures, regulatory risk and supplier dynamics to guide boardroom decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Government price-setter

Commonwealth subsidies and AN-ACC funding, introduced on 1 October 2022, constitute the primary revenue base for Estia Health, making government policy the de facto price-setter. Indexation and AN-ACC recalibrations directly impact margins since providers have little scope to negotiate higher care rates with the payer. Operational compliance and quality outcomes routinely determine funding levels and expose providers to sanctions or funding adjustments.

Residents and families

Choice among local homes gives families leverage over accommodation preferences, enabling moves for location, room type or contract terms. Reputation and Aged Care Quality star ratings strongly drive switching decisions. Negative publicity can quickly dent occupancy in a sector where national residential aged care occupancy averaged about 88% in 2023–24 (AIHW). Service differentiation on amenities and clinical programs can reduce price sensitivity for extras.

Not-for-profit competition

Not-for-profit rivals can accept lower margins, raising buyer expectations for value and pressuring Estia on pricing and service mix. Community trust in NFPs often shifts resident preference away from for-profits, strengthening customers bargaining leverage. Buyers cite mission alignment to negotiate enhanced amenities and care levels. Donations and grants enable NFPs to bundle services that for-profits may struggle to match.

Transparency and ratings

Public quality indicators and 2024 complaints data published by the Aged Care Quality and Safety Commission increase buyer scrutiny of Estia Health, making performance highly visible to residents and families. Comparability across homes via public ratings heightens customer bargaining power as customers can easily switch or demand concessions. Poor metrics force Estia to offer discounts or additional services to retain residents. Continuous improvement in care and transparency is required to defend occupancy.

- Public 2024 complaints data raises scrutiny

- Ratings enable easy home comparison

- Poor metrics -> discounts/refunds pressure

- Ongoing quality improvements defend occupancy

Co-payments and extras

Co-payments and extras give residents leverage: in 2024 many negotiated refundable deposits and tailored service bundles, pressuring average per-resident revenue as price-sensitive buyers down-tier extras during cost-of-living strain. Mix shifts toward basic packages diluted ARPR, while targeted customization and bundled offerings supported sustained willingness to pay.

- Negotiable refundable deposits

- Down‑tiering of extras under cost pressure

- Mix shifts dilute ARPR

- Customization preserves willingness to pay

AN-ACC funding caps pricing; 88% occupancy and 2024 complaints raise switching risk

Government-set AN-ACC funding (effective 1 Oct 2022) is the primary revenue driver, limiting Estia’s price flexibility; sector occupancy averaged 88% in 2023–24 (AIHW), intensifying competition for residents. Public 2024 ACQSC complaints and star ratings raise switching risk and force concessions on extras and deposits; NFP competitors’ subsidy-differentials further press margins.

| Metric | Value | Source |

|---|---|---|

| AN-ACC start | 1 Oct 2022 | Commonwealth |

| Occupancy | 88% (2023–24) | AIHW |

| Visibility | High (2024 ACQSC complaints) | ACQSC |

Preview the Actual Deliverable

Estia Health Porter's Five Forces Analysis

This preview shows the exact Estia Health Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed here is the full, professionally formatted analysis ready for download and use the moment you buy. You're viewing the final deliverable and will get instant access to this same file after payment. No surprises, no setup required.