E.Sun Financial PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are reshaping E.Sun Financial’s strategic landscape in our concise PESTLE snapshot. This preview highlights key risks and opportunities—perfect for quick briefs or investor notes. Purchase the full PESTLE for a complete, actionable analysis you can use immediately.

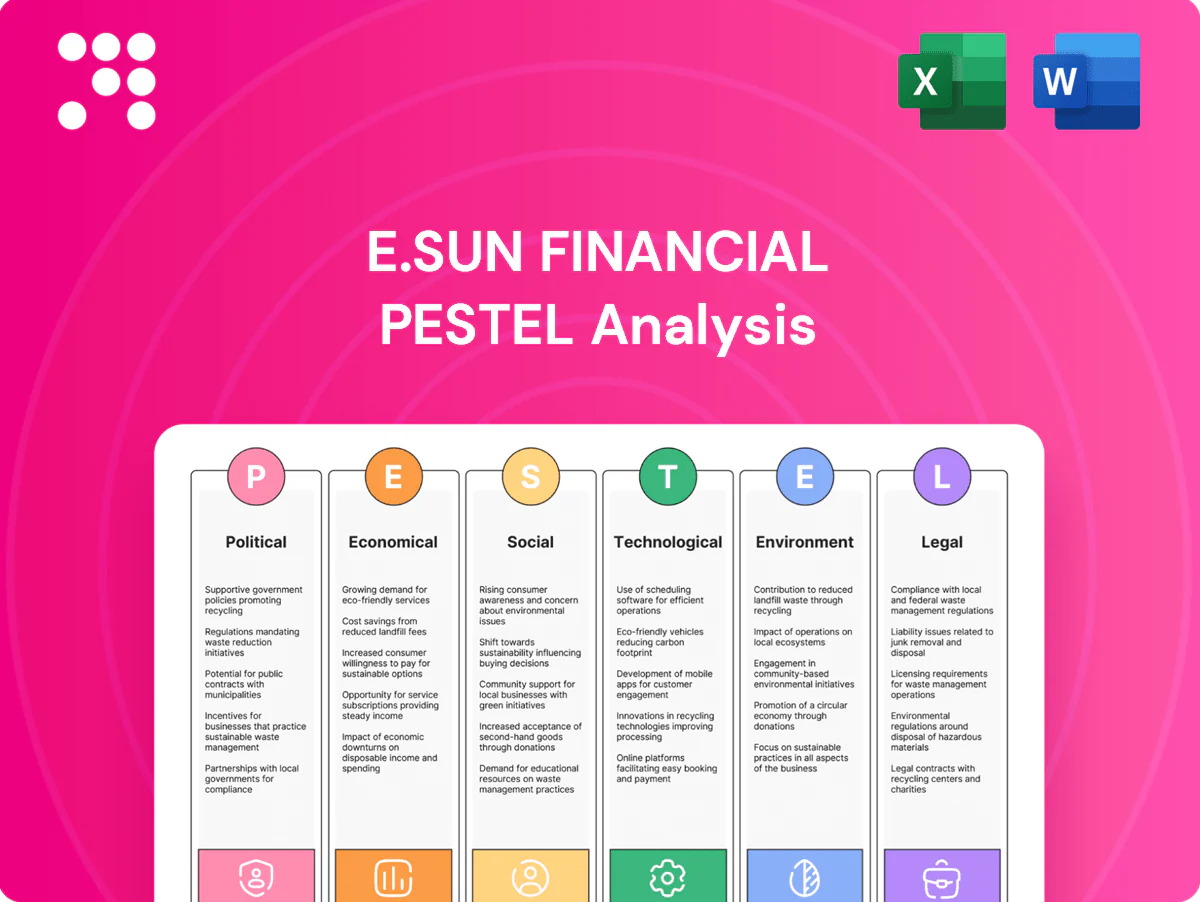

Political factors

Cross-strait geopolitical risk

Heightened China–Taiwan tensions push sovereign and market risk premia higher, undermining investor confidence and prompting intermittent FX volatility and capital flow swings; Taiwan’s defense spending has risen to over 3% of GDP, reinforcing geopolitical risk pricing. E.SUN must prioritize scenario planning and contingency liquidity buffers to meet Basel III liquidity coverage ratio rules (100% minimum). Insurance and hedging costs for cross‑border clients have trended up, lifting counterparty and operational expense pressures.

Domestic policy stability and fiscal stance

Taiwan’s mature democratic institutions support policy continuity for financial services, with general government gross debt around 34% of GDP (2023) and a fiscal deficit near 2.5% of GDP (2024 est.), shaping public investment and credit demand. Fiscal priorities drive infrastructure financing and can boost corporate borrowing when capex rises. Changes in subsidies or taxes directly affect household disposable income and retail loan growth—bank lending rose about 3.7% in 2024. Coordination with state-led industrial policies, notably in semiconductors and green tech, opens targeted lending opportunities.

Regulatory supervision by FSC and CBC

Regulatory supervision by the FSC sets prudential rules and conduct standards, including Basel III minimum CET1 of 4.5% and global countercyclical buffer up to 2.5%, while the CBC shapes liquidity and macroprudential settings such as reserve requirements and systemic risk tools. Policy shifts on capital buffers, dividend limits and consumer protection directly affect E.Sun Financials profitability and capital planning. Active engagement with regulators supports compliant product innovation and faster approval cycles.

International alignment and sanctions regimes

Taiwan aligns with global AML/CFT and sanctions frameworks and Taiwan financial institutions, including E.SUN Financial, have upgraded controls after recent rule changes; global AML fines have exceeded $30 billion since 2009 and correspondent banking relations have fallen roughly 15% since 2011, increasing trade finance screening complexity under expanding extraterritorial rules. Robust KYC and sanctions filtering reduce risks of fines and constrained correspondent access.

- AML fines: > $30 billion since 2009

- Correspondent banking: ~15% decline since 2011

- Risk: fines, frozen assets, reduced corridors

- Mitigation: enhanced KYC, sanctions filtering, screened trade finance

Public ESG and inclusive finance priorities

Government emphasis on green finance and inclusive digital/SME policies—aligned with Taiwan's net-zero by 2050 pledge and SMEs comprising over 97% of firms—steers E.Sun toward sustainability-linked lending and digital-credit products. Incentives and targets channel capital into green and social assets, while policy-backed guarantee schemes lower credit risk and improve funding terms, boosting reputation and investor access.

- net-zero 2050

- SMEs >97% of firms

- policy guarantees reduce credit risk

- enhanced funding/access

Taiwan risks: China tensions, FX volatility, defense >3% GDP, AML >$30bn

China–Taiwan tensions raise sovereign risk and FX volatility; Taiwan defense spending >3% of GDP and E.SUN must maintain Basel III LCR contingencies. Democratic stability with general government debt ~34% of GDP (2023) and a ~2.5% fiscal deficit (2024 est.) supports steady credit demand; bank lending +3.7% in 2024. AML fines >$30bn since 2009 and correspondent banking -15% since 2011 elevate compliance costs; SMEs >97% of firms and net-zero 2050 drive green/SME lending.

| Metric | Value |

|---|---|

| Defense spending | >3% GDP |

| Govt debt (2023) | ~34% GDP |

| Fiscal deficit (2024 est.) | ~2.5% GDP |

| Bank lending (2024) | +3.7% |

| AML fines | >$30bn (since 2009) |

| Correspondent banking | -15% (since 2011) |

| SMEs | >97% firms |

| Climate target | Net-zero 2050 |

What is included in the product

Examines how Political, Economic, Social, Technological, Environmental, and Legal forces specifically impact E.Sun Financial, combining data-driven trends and regional regulatory context to identify risks, opportunities, and strategic implications for executives and investors.

A compact, visually segmented PESTLE summary of E.Sun Financial that can be dropped into presentations or shared across teams, enabling quick alignment, editable notes for region or business-line specifics, and focused discussions on external risks and market positioning during planning sessions.

Economic factors

Interest rate cycle and NIM sensitivity

Net interest margin at E.SUN is tightly linked to CBC policy moves and global cycles; with major central banks like the Fed at 5.25–5.50% (mid‑2025), rapid shifts can compress spreads and force deposit repricing. Duration mismatches in asset‑liability management amplify NIM sensitivity, making active duration hedging critical. Diversified fee income — increasingly targeted in 2024–25 — helps buffer earnings volatility from rate swings.

TWD exchange rate and external trade exposure

Taiwan’s export-led economy—exports ≈ two-thirds of GDP in 2024—drives strong FX flows and corporate demand for hedging, raising bank treasury volumes. TWD volatility materially affects corporate clients and investment portfolios, increasing market and credit risk for lenders. Effective FX risk management supports capital ratios and liquidity buffers under Basel frameworks. Cross-selling FX and treasury solutions can deepen client relationships and fee income.

Semiconductor-led business cycles

Electronics down/up-cycles drive corporate credit demand and risk for E.Sun as semiconductors account for about 30% of Taiwan exports and TSMC held roughly 56% of global foundry share in 2024, amplifying credit exposure swings. Supply chain finance volumes track inventory and capex trends, rising with chip capex and falling in downturns. Concentration risk mandates sectoral limits and stress tests; IFRS 9-aligned countercyclical provisioning bolsters resilience.

Household leverage and real estate dynamics

Property prices and mortgage policy remain primary determinants of E.Sun Financials retail loan growth, where macroprudential tightening can reduce origination volumes while improving asset quality through higher loan-to-value and debt-service ratio scrutiny. Monitoring LTV and DSR trends is essential for credit risk management and pricing. Cross-selling wealth management and protection products helps offset slower credit growth by boosting fee income and deepening customer relationships.

- Retail loan growth tied to property market and mortgage policy

- Macroprudential tightening cuts volumes but raises quality (LTV, DSR focus)

- Cross-selling wealth/protection offsets weaker lending

Global growth and capital market conditions

Equity and bond market health directly affects brokerage and wealth management fees; risk-off episodes compress trading volumes and AUM inflows, while diversified product shelves (mutual funds, ETFs, derivatives, advisory) help stabilize fee revenue. Robust liquidity management preserves market-making continuity. IMF projects global growth at 3.1% in 2025.

- Market impact: lower volumes → lower fees

- Risk-off: reduces AUM inflows

- Diversification: stabilizes fee streams

- Liquidity mgmt: ensures market-making

Taiwan risks: China tensions, FX volatility, defense >3% GDP, AML >$30bn

Higher global rates (Fed 5.25–5.50% mid‑2025) squeeze NIMs; duration mismatches require active hedging. Taiwan exports ≈66% of GDP (2024) and semiconductors ~30% of exports, amplifying corporate credit cyclicality. Property policy drives retail loan growth and LTV/DSR risk; fee diversification cushions earnings.

| Metric | Value |

|---|---|

| Fed policy rate (mid‑2025) | 5.25–5.50% |

| Taiwan exports/GDP (2024) | ≈66% |

| Semiconductor share of exports | ≈30% |

| Global growth (IMF 2025) | 3.1% |

Preview Before You Purchase

E.Sun Financial PESTLE Analysis

The E.Sun Financial PESTLE Analysis preview shown here is the exact, fully formatted document you’ll receive after purchase—professionally structured and ready to use. The content, layout, and insights visible are identical to the final file available for immediate download upon payment.

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are reshaping E.Sun Financial’s strategic landscape in our concise PESTLE snapshot. This preview highlights key risks and opportunities—perfect for quick briefs or investor notes. Purchase the full PESTLE for a complete, actionable analysis you can use immediately.

Political factors

Cross-strait geopolitical risk

Heightened China–Taiwan tensions push sovereign and market risk premia higher, undermining investor confidence and prompting intermittent FX volatility and capital flow swings; Taiwan’s defense spending has risen to over 3% of GDP, reinforcing geopolitical risk pricing. E.SUN must prioritize scenario planning and contingency liquidity buffers to meet Basel III liquidity coverage ratio rules (100% minimum). Insurance and hedging costs for cross‑border clients have trended up, lifting counterparty and operational expense pressures.

Domestic policy stability and fiscal stance

Taiwan’s mature democratic institutions support policy continuity for financial services, with general government gross debt around 34% of GDP (2023) and a fiscal deficit near 2.5% of GDP (2024 est.), shaping public investment and credit demand. Fiscal priorities drive infrastructure financing and can boost corporate borrowing when capex rises. Changes in subsidies or taxes directly affect household disposable income and retail loan growth—bank lending rose about 3.7% in 2024. Coordination with state-led industrial policies, notably in semiconductors and green tech, opens targeted lending opportunities.

Regulatory supervision by FSC and CBC

Regulatory supervision by the FSC sets prudential rules and conduct standards, including Basel III minimum CET1 of 4.5% and global countercyclical buffer up to 2.5%, while the CBC shapes liquidity and macroprudential settings such as reserve requirements and systemic risk tools. Policy shifts on capital buffers, dividend limits and consumer protection directly affect E.Sun Financials profitability and capital planning. Active engagement with regulators supports compliant product innovation and faster approval cycles.

International alignment and sanctions regimes

Taiwan aligns with global AML/CFT and sanctions frameworks and Taiwan financial institutions, including E.SUN Financial, have upgraded controls after recent rule changes; global AML fines have exceeded $30 billion since 2009 and correspondent banking relations have fallen roughly 15% since 2011, increasing trade finance screening complexity under expanding extraterritorial rules. Robust KYC and sanctions filtering reduce risks of fines and constrained correspondent access.

- AML fines: > $30 billion since 2009

- Correspondent banking: ~15% decline since 2011

- Risk: fines, frozen assets, reduced corridors

- Mitigation: enhanced KYC, sanctions filtering, screened trade finance

Public ESG and inclusive finance priorities

Government emphasis on green finance and inclusive digital/SME policies—aligned with Taiwan's net-zero by 2050 pledge and SMEs comprising over 97% of firms—steers E.Sun toward sustainability-linked lending and digital-credit products. Incentives and targets channel capital into green and social assets, while policy-backed guarantee schemes lower credit risk and improve funding terms, boosting reputation and investor access.

- net-zero 2050

- SMEs >97% of firms

- policy guarantees reduce credit risk

- enhanced funding/access

Taiwan risks: China tensions, FX volatility, defense >3% GDP, AML >$30bn

China–Taiwan tensions raise sovereign risk and FX volatility; Taiwan defense spending >3% of GDP and E.SUN must maintain Basel III LCR contingencies. Democratic stability with general government debt ~34% of GDP (2023) and a ~2.5% fiscal deficit (2024 est.) supports steady credit demand; bank lending +3.7% in 2024. AML fines >$30bn since 2009 and correspondent banking -15% since 2011 elevate compliance costs; SMEs >97% of firms and net-zero 2050 drive green/SME lending.

| Metric | Value |

|---|---|

| Defense spending | >3% GDP |

| Govt debt (2023) | ~34% GDP |

| Fiscal deficit (2024 est.) | ~2.5% GDP |

| Bank lending (2024) | +3.7% |

| AML fines | >$30bn (since 2009) |

| Correspondent banking | -15% (since 2011) |

| SMEs | >97% firms |

| Climate target | Net-zero 2050 |

What is included in the product

Examines how Political, Economic, Social, Technological, Environmental, and Legal forces specifically impact E.Sun Financial, combining data-driven trends and regional regulatory context to identify risks, opportunities, and strategic implications for executives and investors.

A compact, visually segmented PESTLE summary of E.Sun Financial that can be dropped into presentations or shared across teams, enabling quick alignment, editable notes for region or business-line specifics, and focused discussions on external risks and market positioning during planning sessions.

Economic factors

Interest rate cycle and NIM sensitivity

Net interest margin at E.SUN is tightly linked to CBC policy moves and global cycles; with major central banks like the Fed at 5.25–5.50% (mid‑2025), rapid shifts can compress spreads and force deposit repricing. Duration mismatches in asset‑liability management amplify NIM sensitivity, making active duration hedging critical. Diversified fee income — increasingly targeted in 2024–25 — helps buffer earnings volatility from rate swings.

TWD exchange rate and external trade exposure

Taiwan’s export-led economy—exports ≈ two-thirds of GDP in 2024—drives strong FX flows and corporate demand for hedging, raising bank treasury volumes. TWD volatility materially affects corporate clients and investment portfolios, increasing market and credit risk for lenders. Effective FX risk management supports capital ratios and liquidity buffers under Basel frameworks. Cross-selling FX and treasury solutions can deepen client relationships and fee income.

Semiconductor-led business cycles

Electronics down/up-cycles drive corporate credit demand and risk for E.Sun as semiconductors account for about 30% of Taiwan exports and TSMC held roughly 56% of global foundry share in 2024, amplifying credit exposure swings. Supply chain finance volumes track inventory and capex trends, rising with chip capex and falling in downturns. Concentration risk mandates sectoral limits and stress tests; IFRS 9-aligned countercyclical provisioning bolsters resilience.

Household leverage and real estate dynamics

Property prices and mortgage policy remain primary determinants of E.Sun Financials retail loan growth, where macroprudential tightening can reduce origination volumes while improving asset quality through higher loan-to-value and debt-service ratio scrutiny. Monitoring LTV and DSR trends is essential for credit risk management and pricing. Cross-selling wealth management and protection products helps offset slower credit growth by boosting fee income and deepening customer relationships.

- Retail loan growth tied to property market and mortgage policy

- Macroprudential tightening cuts volumes but raises quality (LTV, DSR focus)

- Cross-selling wealth/protection offsets weaker lending

Global growth and capital market conditions

Equity and bond market health directly affects brokerage and wealth management fees; risk-off episodes compress trading volumes and AUM inflows, while diversified product shelves (mutual funds, ETFs, derivatives, advisory) help stabilize fee revenue. Robust liquidity management preserves market-making continuity. IMF projects global growth at 3.1% in 2025.

- Market impact: lower volumes → lower fees

- Risk-off: reduces AUM inflows

- Diversification: stabilizes fee streams

- Liquidity mgmt: ensures market-making

Taiwan risks: China tensions, FX volatility, defense >3% GDP, AML >$30bn

Higher global rates (Fed 5.25–5.50% mid‑2025) squeeze NIMs; duration mismatches require active hedging. Taiwan exports ≈66% of GDP (2024) and semiconductors ~30% of exports, amplifying corporate credit cyclicality. Property policy drives retail loan growth and LTV/DSR risk; fee diversification cushions earnings.

| Metric | Value |

|---|---|

| Fed policy rate (mid‑2025) | 5.25–5.50% |

| Taiwan exports/GDP (2024) | ≈66% |

| Semiconductor share of exports | ≈30% |

| Global growth (IMF 2025) | 3.1% |

Preview Before You Purchase

E.Sun Financial PESTLE Analysis

The E.Sun Financial PESTLE Analysis preview shown here is the exact, fully formatted document you’ll receive after purchase—professionally structured and ready to use. The content, layout, and insights visible are identical to the final file available for immediate download upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are reshaping E.Sun Financial’s strategic landscape in our concise PESTLE snapshot. This preview highlights key risks and opportunities—perfect for quick briefs or investor notes. Purchase the full PESTLE for a complete, actionable analysis you can use immediately.

Political factors

Cross-strait geopolitical risk

Heightened China–Taiwan tensions push sovereign and market risk premia higher, undermining investor confidence and prompting intermittent FX volatility and capital flow swings; Taiwan’s defense spending has risen to over 3% of GDP, reinforcing geopolitical risk pricing. E.SUN must prioritize scenario planning and contingency liquidity buffers to meet Basel III liquidity coverage ratio rules (100% minimum). Insurance and hedging costs for cross‑border clients have trended up, lifting counterparty and operational expense pressures.

Domestic policy stability and fiscal stance

Taiwan’s mature democratic institutions support policy continuity for financial services, with general government gross debt around 34% of GDP (2023) and a fiscal deficit near 2.5% of GDP (2024 est.), shaping public investment and credit demand. Fiscal priorities drive infrastructure financing and can boost corporate borrowing when capex rises. Changes in subsidies or taxes directly affect household disposable income and retail loan growth—bank lending rose about 3.7% in 2024. Coordination with state-led industrial policies, notably in semiconductors and green tech, opens targeted lending opportunities.

Regulatory supervision by FSC and CBC

Regulatory supervision by the FSC sets prudential rules and conduct standards, including Basel III minimum CET1 of 4.5% and global countercyclical buffer up to 2.5%, while the CBC shapes liquidity and macroprudential settings such as reserve requirements and systemic risk tools. Policy shifts on capital buffers, dividend limits and consumer protection directly affect E.Sun Financials profitability and capital planning. Active engagement with regulators supports compliant product innovation and faster approval cycles.

International alignment and sanctions regimes

Taiwan aligns with global AML/CFT and sanctions frameworks and Taiwan financial institutions, including E.SUN Financial, have upgraded controls after recent rule changes; global AML fines have exceeded $30 billion since 2009 and correspondent banking relations have fallen roughly 15% since 2011, increasing trade finance screening complexity under expanding extraterritorial rules. Robust KYC and sanctions filtering reduce risks of fines and constrained correspondent access.

- AML fines: > $30 billion since 2009

- Correspondent banking: ~15% decline since 2011

- Risk: fines, frozen assets, reduced corridors

- Mitigation: enhanced KYC, sanctions filtering, screened trade finance

Public ESG and inclusive finance priorities

Government emphasis on green finance and inclusive digital/SME policies—aligned with Taiwan's net-zero by 2050 pledge and SMEs comprising over 97% of firms—steers E.Sun toward sustainability-linked lending and digital-credit products. Incentives and targets channel capital into green and social assets, while policy-backed guarantee schemes lower credit risk and improve funding terms, boosting reputation and investor access.

- net-zero 2050

- SMEs >97% of firms

- policy guarantees reduce credit risk

- enhanced funding/access

Taiwan risks: China tensions, FX volatility, defense >3% GDP, AML >$30bn

China–Taiwan tensions raise sovereign risk and FX volatility; Taiwan defense spending >3% of GDP and E.SUN must maintain Basel III LCR contingencies. Democratic stability with general government debt ~34% of GDP (2023) and a ~2.5% fiscal deficit (2024 est.) supports steady credit demand; bank lending +3.7% in 2024. AML fines >$30bn since 2009 and correspondent banking -15% since 2011 elevate compliance costs; SMEs >97% of firms and net-zero 2050 drive green/SME lending.

| Metric | Value |

|---|---|

| Defense spending | >3% GDP |

| Govt debt (2023) | ~34% GDP |

| Fiscal deficit (2024 est.) | ~2.5% GDP |

| Bank lending (2024) | +3.7% |

| AML fines | >$30bn (since 2009) |

| Correspondent banking | -15% (since 2011) |

| SMEs | >97% firms |

| Climate target | Net-zero 2050 |

What is included in the product

Examines how Political, Economic, Social, Technological, Environmental, and Legal forces specifically impact E.Sun Financial, combining data-driven trends and regional regulatory context to identify risks, opportunities, and strategic implications for executives and investors.

A compact, visually segmented PESTLE summary of E.Sun Financial that can be dropped into presentations or shared across teams, enabling quick alignment, editable notes for region or business-line specifics, and focused discussions on external risks and market positioning during planning sessions.

Economic factors

Interest rate cycle and NIM sensitivity

Net interest margin at E.SUN is tightly linked to CBC policy moves and global cycles; with major central banks like the Fed at 5.25–5.50% (mid‑2025), rapid shifts can compress spreads and force deposit repricing. Duration mismatches in asset‑liability management amplify NIM sensitivity, making active duration hedging critical. Diversified fee income — increasingly targeted in 2024–25 — helps buffer earnings volatility from rate swings.

TWD exchange rate and external trade exposure

Taiwan’s export-led economy—exports ≈ two-thirds of GDP in 2024—drives strong FX flows and corporate demand for hedging, raising bank treasury volumes. TWD volatility materially affects corporate clients and investment portfolios, increasing market and credit risk for lenders. Effective FX risk management supports capital ratios and liquidity buffers under Basel frameworks. Cross-selling FX and treasury solutions can deepen client relationships and fee income.

Semiconductor-led business cycles

Electronics down/up-cycles drive corporate credit demand and risk for E.Sun as semiconductors account for about 30% of Taiwan exports and TSMC held roughly 56% of global foundry share in 2024, amplifying credit exposure swings. Supply chain finance volumes track inventory and capex trends, rising with chip capex and falling in downturns. Concentration risk mandates sectoral limits and stress tests; IFRS 9-aligned countercyclical provisioning bolsters resilience.

Household leverage and real estate dynamics

Property prices and mortgage policy remain primary determinants of E.Sun Financials retail loan growth, where macroprudential tightening can reduce origination volumes while improving asset quality through higher loan-to-value and debt-service ratio scrutiny. Monitoring LTV and DSR trends is essential for credit risk management and pricing. Cross-selling wealth management and protection products helps offset slower credit growth by boosting fee income and deepening customer relationships.

- Retail loan growth tied to property market and mortgage policy

- Macroprudential tightening cuts volumes but raises quality (LTV, DSR focus)

- Cross-selling wealth/protection offsets weaker lending

Global growth and capital market conditions

Equity and bond market health directly affects brokerage and wealth management fees; risk-off episodes compress trading volumes and AUM inflows, while diversified product shelves (mutual funds, ETFs, derivatives, advisory) help stabilize fee revenue. Robust liquidity management preserves market-making continuity. IMF projects global growth at 3.1% in 2025.

- Market impact: lower volumes → lower fees

- Risk-off: reduces AUM inflows

- Diversification: stabilizes fee streams

- Liquidity mgmt: ensures market-making

Taiwan risks: China tensions, FX volatility, defense >3% GDP, AML >$30bn

Higher global rates (Fed 5.25–5.50% mid‑2025) squeeze NIMs; duration mismatches require active hedging. Taiwan exports ≈66% of GDP (2024) and semiconductors ~30% of exports, amplifying corporate credit cyclicality. Property policy drives retail loan growth and LTV/DSR risk; fee diversification cushions earnings.

| Metric | Value |

|---|---|

| Fed policy rate (mid‑2025) | 5.25–5.50% |

| Taiwan exports/GDP (2024) | ≈66% |

| Semiconductor share of exports | ≈30% |

| Global growth (IMF 2025) | 3.1% |

Preview Before You Purchase

E.Sun Financial PESTLE Analysis

The E.Sun Financial PESTLE Analysis preview shown here is the exact, fully formatted document you’ll receive after purchase—professionally structured and ready to use. The content, layout, and insights visible are identical to the final file available for immediate download upon payment.