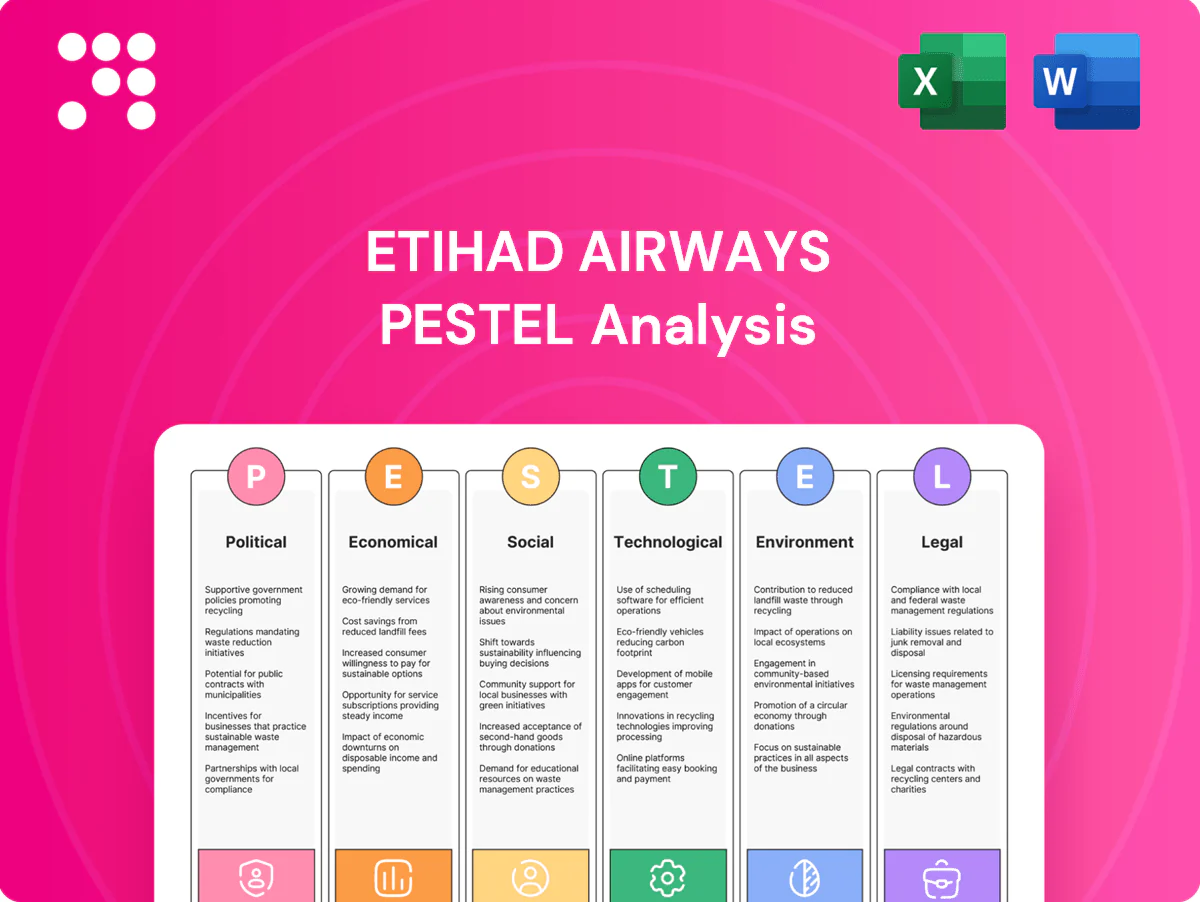

Etihad Airways PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic cycles, and technological change are reshaping Etihad Airways’ prospects in our concise PESTLE snapshot—insightful for investors and strategists alike. Purchase the full PESTLE for the complete, actionable analysis and ready-to-use templates.

Political factors

UAE aviation policy and state backing

Etihad is 100% government-owned and its strategy closely follows Abu Dhabi’s national aviation and economic visions, including diversification toward tourism and growth through 2030. State backing has enabled rapid fleet renewal and route launches in prior recapitalisations and partnerships. Policy emphasis on long-haul connectivity supports hub development and tourism targets. Any recalibration of subsidies or capital allocation would materially change Etihad’s competitive posture.

Bilateral air service agreements and traffic rights

Access to key markets for Etihad hinges on negotiated bilaterals and Open Skies regimes, which have enabled the airline to expand its Abu Dhabi network to about 67 passenger destinations as of 2024.

Expanded freedoms such as fifth freedom rights and extra frequencies materially drive connectivity and network growth via Abu Dhabi, while restrictions in specific jurisdictions can cap capacity and suppress yield.

Lobbying and diplomacy remain active levers—Etihad and the UAE government continuously negotiate traffic rights to unlock new routes and additional frequencies.

Regional geopolitics and airspace stability

Middle East tensions (eg. FAA and EASA Red Sea advisories in Nov 2023) force Etihad to reroute flights, lengthening stage lengths and occasionally suspending sectors, raising fuel and crew costs. Airspace closures disrupt schedules and increase operational costs and delays. Stable regional geopolitics improves Abu Dhabi hub reliability and passenger confidence. Insurance premiums and security protocols are routinely adjusted upward in higher-risk periods.

Global alliances and government relations

Etihad, 100% owned by the Abu Dhabi government via ADQ, relies on political goodwill for regulatory clearances on partnerships and codeshares; government-to-government ties both enable and can restrict joint ventures depending on diplomatic relations. Alignment with UAE tourism and economic agencies underpinned capacity growth strategies in 2024. Heightened foreign-investment scrutiny in many markets constrains deeper equity integrations.

- Ownership: ADQ (Abu Dhabi) — facilitates state-backed deals

- Regulatory: clearances required for codeshares/JVs

- Policy: aligned with national tourism strategy (2024 focus)

- Risk: rising FDI/foreign-influence scrutiny limits equity depth

Subsidy scrutiny and protectionism abroad

Subsidy scrutiny and protectionism abroad threaten Etihad as competitors in mature markets lobby for curbs on Gulf carriers; investigations or hearings can delay route approvals and slow expansion. Protectionist slot policies at constrained airports like London Heathrow (capacity cap ~480,000 annual movements) restrict entry. Transparent governance and compliance reduce political backlash and ease regulatory approvals.

- Competitor lobbying

- Investigations delay approvals

- Slot limits (Heathrow ~480,000 movements)

- Governance mitigates backlash

State-owned, aligned to Abu Dhabi 2030; 67 destinations, slots capped

Etihad is 100% government-owned, aligning strategy with Abu Dhabi’s 2030 tourism and connectivity goals and benefiting from state recapitalisations. Access to markets depends on bilaterals/Open Skies; network reached about 67 passenger destinations in 2024. Regional tensions (eg. Red Sea advisories Nov 2023) and foreign-investment scrutiny raise costs and constrain JVs. Protectionist slots (Heathrow ~480,000 movements) limit expansion.

| Metric | Value |

|---|---|

| Ownership | 100% ADQ |

| Destinations (2024) | ~67 |

| Heathrow cap | ~480,000 movements |

| Notable advisory | Red Sea Nov 2023 |

What is included in the product

Explores how macro-environmental factors uniquely affect Etihad Airways across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific regulatory context. Designed for executives and investors, it highlights risks, opportunities and forward-looking insights ready for inclusion in reports or decks.

A concise, visually segmented PESTLE summary of Etihad Airways that clarifies external risks and market positioning for quick alignment across teams, easily dropped into presentations or planning sessions and editable for regional or business-line notes.

Economic factors

Fuel price volatility and hedging

Jet fuel is the dominant cost driver for Etihad, representing a large single-variable input for the carrier and industry-wide typically 20–30% of operating costs; global jet fuel averaged about $95/barrel in 2024 (IATA), linking costs tightly to crude and refining spreads.

Etihad uses hedging to smooth expense volatility, but hedges expose the carrier to basis risk when jet fuel and crude move differently.

Fleet renewal and operational measures (route optimization, weight reduction) lower fuel burn and partially offset spikes, while USD-denominated fuel purchases add currency exposure when AED or partner currencies fluctuate against the dollar.

Global GDP, tourism flows, and trade

Passenger and cargo demand for Etihad closely follows global GDP growth, which the IMF projected at about 3.1% for 2024 and ~3.0% for 2025, driving RPK and freight volumes. Abu Dhabi’s tourism agenda and events calendar (e.g., major cultural and sporting events) bolster inbound leisure traffic and seasonally lift load factors. Slower global trade weakens cargo yields and belly capacity utilization, pressuring cargo revenue per kg. Premium cabin demand mirrors corporate travel budgets and oil-sector activity, sensitive to oil prices near the mid-70s to mid-80s USD/bbl range.

Exchange rates and revenue mix

Multi-currency revenues expose Etihad to translation and transaction risks across ticket sales and cargo; the UAE dirham has been pegged to the US dollar since 1997, anchoring many costs to USD. USD strength in 2024 pressured non-USD demand while easing USD-priced inputs like fuel and aircraft leases. Pricing, surcharges and natural hedges (route-level currency matching) are used to balance exposures. Network diversification across more than 70 destinations reduces regional concentration risk.

Capital intensity and financing costs

Widebody acquisitions, leases and engine maintenance drive Etihad’s high capex and cash needs, forcing reliance on operating leases and maintenance reserves to preserve liquidity. Interest rate cycles directly shape lease rates and refinancing costs, affecting unit cost and RASK sensitivity. Access to export credit agencies and Islamic finance structures can lower funding costs and extend maturities. Capacity discipline is essential to protect load factors and RASK.

- Capex drivers: widebodies, engines, MRO

- Financing: leases, export credit, sukuk

- Rates impact: lease/refinance sensitivity

- Network: capacity discipline → load factor/RASK

Airport capacity and slot economics

Hub infrastructure and terminal efficiency at Abu Dhabi reduce Etihad turnaround times and improve connectivity; Abu Dhabi Airport aims to expand capacity to ~45 million passengers to 2030, underpinning long‑term growth. Scarcity at full gateways such as Heathrow (~99% runway utilization) pushes slot acquisition and lease costs sharply higher. Wave scheduling preserves banked connections and can boost yields on peak banks.

- Abu Dhabi expansion: ~45M p.a. target to 2030

- Heathrow utilization: ~99%, elevating slot costs

- Wave scheduling: higher yields on banked banks

State-owned, aligned to Abu Dhabi 2030; 67 destinations, slots capped

Jet fuel (~$95/barrel in 2024) is Etihad’s largest cost driver, hedged but exposing basis risk; fleet renewal and ops cuts reduce burn. Global GDP ~3.1% (IMF 2024) guides pax/cargo demand while UAE dirham peg to USD ties costs to dollar moves. High capex (widebodies, engines) and rising lease rates increase funding needs; Abu Dhabi airport capacity target ~45M by 2030 supports growth.

| Metric | Value |

|---|---|

| Jet fuel (2024) | $95/bbl |

| Global GDP (2024) | 3.1% |

| Abu Dhabi capacity target | ~45M by 2030 |

| Heathrow utilization | ~99% |

Preview Before You Purchase

Etihad Airways PESTLE Analysis

The preview shown here is the exact Etihad Airways PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with professional structure and no placeholders. After checkout you’ll instantly download this identical file, ready for analysis and presentation.

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic cycles, and technological change are reshaping Etihad Airways’ prospects in our concise PESTLE snapshot—insightful for investors and strategists alike. Purchase the full PESTLE for the complete, actionable analysis and ready-to-use templates.

Political factors

UAE aviation policy and state backing

Etihad is 100% government-owned and its strategy closely follows Abu Dhabi’s national aviation and economic visions, including diversification toward tourism and growth through 2030. State backing has enabled rapid fleet renewal and route launches in prior recapitalisations and partnerships. Policy emphasis on long-haul connectivity supports hub development and tourism targets. Any recalibration of subsidies or capital allocation would materially change Etihad’s competitive posture.

Bilateral air service agreements and traffic rights

Access to key markets for Etihad hinges on negotiated bilaterals and Open Skies regimes, which have enabled the airline to expand its Abu Dhabi network to about 67 passenger destinations as of 2024.

Expanded freedoms such as fifth freedom rights and extra frequencies materially drive connectivity and network growth via Abu Dhabi, while restrictions in specific jurisdictions can cap capacity and suppress yield.

Lobbying and diplomacy remain active levers—Etihad and the UAE government continuously negotiate traffic rights to unlock new routes and additional frequencies.

Regional geopolitics and airspace stability

Middle East tensions (eg. FAA and EASA Red Sea advisories in Nov 2023) force Etihad to reroute flights, lengthening stage lengths and occasionally suspending sectors, raising fuel and crew costs. Airspace closures disrupt schedules and increase operational costs and delays. Stable regional geopolitics improves Abu Dhabi hub reliability and passenger confidence. Insurance premiums and security protocols are routinely adjusted upward in higher-risk periods.

Global alliances and government relations

Etihad, 100% owned by the Abu Dhabi government via ADQ, relies on political goodwill for regulatory clearances on partnerships and codeshares; government-to-government ties both enable and can restrict joint ventures depending on diplomatic relations. Alignment with UAE tourism and economic agencies underpinned capacity growth strategies in 2024. Heightened foreign-investment scrutiny in many markets constrains deeper equity integrations.

- Ownership: ADQ (Abu Dhabi) — facilitates state-backed deals

- Regulatory: clearances required for codeshares/JVs

- Policy: aligned with national tourism strategy (2024 focus)

- Risk: rising FDI/foreign-influence scrutiny limits equity depth

Subsidy scrutiny and protectionism abroad

Subsidy scrutiny and protectionism abroad threaten Etihad as competitors in mature markets lobby for curbs on Gulf carriers; investigations or hearings can delay route approvals and slow expansion. Protectionist slot policies at constrained airports like London Heathrow (capacity cap ~480,000 annual movements) restrict entry. Transparent governance and compliance reduce political backlash and ease regulatory approvals.

- Competitor lobbying

- Investigations delay approvals

- Slot limits (Heathrow ~480,000 movements)

- Governance mitigates backlash

State-owned, aligned to Abu Dhabi 2030; 67 destinations, slots capped

Etihad is 100% government-owned, aligning strategy with Abu Dhabi’s 2030 tourism and connectivity goals and benefiting from state recapitalisations. Access to markets depends on bilaterals/Open Skies; network reached about 67 passenger destinations in 2024. Regional tensions (eg. Red Sea advisories Nov 2023) and foreign-investment scrutiny raise costs and constrain JVs. Protectionist slots (Heathrow ~480,000 movements) limit expansion.

| Metric | Value |

|---|---|

| Ownership | 100% ADQ |

| Destinations (2024) | ~67 |

| Heathrow cap | ~480,000 movements |

| Notable advisory | Red Sea Nov 2023 |

What is included in the product

Explores how macro-environmental factors uniquely affect Etihad Airways across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific regulatory context. Designed for executives and investors, it highlights risks, opportunities and forward-looking insights ready for inclusion in reports or decks.

A concise, visually segmented PESTLE summary of Etihad Airways that clarifies external risks and market positioning for quick alignment across teams, easily dropped into presentations or planning sessions and editable for regional or business-line notes.

Economic factors

Fuel price volatility and hedging

Jet fuel is the dominant cost driver for Etihad, representing a large single-variable input for the carrier and industry-wide typically 20–30% of operating costs; global jet fuel averaged about $95/barrel in 2024 (IATA), linking costs tightly to crude and refining spreads.

Etihad uses hedging to smooth expense volatility, but hedges expose the carrier to basis risk when jet fuel and crude move differently.

Fleet renewal and operational measures (route optimization, weight reduction) lower fuel burn and partially offset spikes, while USD-denominated fuel purchases add currency exposure when AED or partner currencies fluctuate against the dollar.

Global GDP, tourism flows, and trade

Passenger and cargo demand for Etihad closely follows global GDP growth, which the IMF projected at about 3.1% for 2024 and ~3.0% for 2025, driving RPK and freight volumes. Abu Dhabi’s tourism agenda and events calendar (e.g., major cultural and sporting events) bolster inbound leisure traffic and seasonally lift load factors. Slower global trade weakens cargo yields and belly capacity utilization, pressuring cargo revenue per kg. Premium cabin demand mirrors corporate travel budgets and oil-sector activity, sensitive to oil prices near the mid-70s to mid-80s USD/bbl range.

Exchange rates and revenue mix

Multi-currency revenues expose Etihad to translation and transaction risks across ticket sales and cargo; the UAE dirham has been pegged to the US dollar since 1997, anchoring many costs to USD. USD strength in 2024 pressured non-USD demand while easing USD-priced inputs like fuel and aircraft leases. Pricing, surcharges and natural hedges (route-level currency matching) are used to balance exposures. Network diversification across more than 70 destinations reduces regional concentration risk.

Capital intensity and financing costs

Widebody acquisitions, leases and engine maintenance drive Etihad’s high capex and cash needs, forcing reliance on operating leases and maintenance reserves to preserve liquidity. Interest rate cycles directly shape lease rates and refinancing costs, affecting unit cost and RASK sensitivity. Access to export credit agencies and Islamic finance structures can lower funding costs and extend maturities. Capacity discipline is essential to protect load factors and RASK.

- Capex drivers: widebodies, engines, MRO

- Financing: leases, export credit, sukuk

- Rates impact: lease/refinance sensitivity

- Network: capacity discipline → load factor/RASK

Airport capacity and slot economics

Hub infrastructure and terminal efficiency at Abu Dhabi reduce Etihad turnaround times and improve connectivity; Abu Dhabi Airport aims to expand capacity to ~45 million passengers to 2030, underpinning long‑term growth. Scarcity at full gateways such as Heathrow (~99% runway utilization) pushes slot acquisition and lease costs sharply higher. Wave scheduling preserves banked connections and can boost yields on peak banks.

- Abu Dhabi expansion: ~45M p.a. target to 2030

- Heathrow utilization: ~99%, elevating slot costs

- Wave scheduling: higher yields on banked banks

State-owned, aligned to Abu Dhabi 2030; 67 destinations, slots capped

Jet fuel (~$95/barrel in 2024) is Etihad’s largest cost driver, hedged but exposing basis risk; fleet renewal and ops cuts reduce burn. Global GDP ~3.1% (IMF 2024) guides pax/cargo demand while UAE dirham peg to USD ties costs to dollar moves. High capex (widebodies, engines) and rising lease rates increase funding needs; Abu Dhabi airport capacity target ~45M by 2030 supports growth.

| Metric | Value |

|---|---|

| Jet fuel (2024) | $95/bbl |

| Global GDP (2024) | 3.1% |

| Abu Dhabi capacity target | ~45M by 2030 |

| Heathrow utilization | ~99% |

Preview Before You Purchase

Etihad Airways PESTLE Analysis

The preview shown here is the exact Etihad Airways PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with professional structure and no placeholders. After checkout you’ll instantly download this identical file, ready for analysis and presentation.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic cycles, and technological change are reshaping Etihad Airways’ prospects in our concise PESTLE snapshot—insightful for investors and strategists alike. Purchase the full PESTLE for the complete, actionable analysis and ready-to-use templates.

Political factors

UAE aviation policy and state backing

Etihad is 100% government-owned and its strategy closely follows Abu Dhabi’s national aviation and economic visions, including diversification toward tourism and growth through 2030. State backing has enabled rapid fleet renewal and route launches in prior recapitalisations and partnerships. Policy emphasis on long-haul connectivity supports hub development and tourism targets. Any recalibration of subsidies or capital allocation would materially change Etihad’s competitive posture.

Bilateral air service agreements and traffic rights

Access to key markets for Etihad hinges on negotiated bilaterals and Open Skies regimes, which have enabled the airline to expand its Abu Dhabi network to about 67 passenger destinations as of 2024.

Expanded freedoms such as fifth freedom rights and extra frequencies materially drive connectivity and network growth via Abu Dhabi, while restrictions in specific jurisdictions can cap capacity and suppress yield.

Lobbying and diplomacy remain active levers—Etihad and the UAE government continuously negotiate traffic rights to unlock new routes and additional frequencies.

Regional geopolitics and airspace stability

Middle East tensions (eg. FAA and EASA Red Sea advisories in Nov 2023) force Etihad to reroute flights, lengthening stage lengths and occasionally suspending sectors, raising fuel and crew costs. Airspace closures disrupt schedules and increase operational costs and delays. Stable regional geopolitics improves Abu Dhabi hub reliability and passenger confidence. Insurance premiums and security protocols are routinely adjusted upward in higher-risk periods.

Global alliances and government relations

Etihad, 100% owned by the Abu Dhabi government via ADQ, relies on political goodwill for regulatory clearances on partnerships and codeshares; government-to-government ties both enable and can restrict joint ventures depending on diplomatic relations. Alignment with UAE tourism and economic agencies underpinned capacity growth strategies in 2024. Heightened foreign-investment scrutiny in many markets constrains deeper equity integrations.

- Ownership: ADQ (Abu Dhabi) — facilitates state-backed deals

- Regulatory: clearances required for codeshares/JVs

- Policy: aligned with national tourism strategy (2024 focus)

- Risk: rising FDI/foreign-influence scrutiny limits equity depth

Subsidy scrutiny and protectionism abroad

Subsidy scrutiny and protectionism abroad threaten Etihad as competitors in mature markets lobby for curbs on Gulf carriers; investigations or hearings can delay route approvals and slow expansion. Protectionist slot policies at constrained airports like London Heathrow (capacity cap ~480,000 annual movements) restrict entry. Transparent governance and compliance reduce political backlash and ease regulatory approvals.

- Competitor lobbying

- Investigations delay approvals

- Slot limits (Heathrow ~480,000 movements)

- Governance mitigates backlash

State-owned, aligned to Abu Dhabi 2030; 67 destinations, slots capped

Etihad is 100% government-owned, aligning strategy with Abu Dhabi’s 2030 tourism and connectivity goals and benefiting from state recapitalisations. Access to markets depends on bilaterals/Open Skies; network reached about 67 passenger destinations in 2024. Regional tensions (eg. Red Sea advisories Nov 2023) and foreign-investment scrutiny raise costs and constrain JVs. Protectionist slots (Heathrow ~480,000 movements) limit expansion.

| Metric | Value |

|---|---|

| Ownership | 100% ADQ |

| Destinations (2024) | ~67 |

| Heathrow cap | ~480,000 movements |

| Notable advisory | Red Sea Nov 2023 |

What is included in the product

Explores how macro-environmental factors uniquely affect Etihad Airways across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific regulatory context. Designed for executives and investors, it highlights risks, opportunities and forward-looking insights ready for inclusion in reports or decks.

A concise, visually segmented PESTLE summary of Etihad Airways that clarifies external risks and market positioning for quick alignment across teams, easily dropped into presentations or planning sessions and editable for regional or business-line notes.

Economic factors

Fuel price volatility and hedging

Jet fuel is the dominant cost driver for Etihad, representing a large single-variable input for the carrier and industry-wide typically 20–30% of operating costs; global jet fuel averaged about $95/barrel in 2024 (IATA), linking costs tightly to crude and refining spreads.

Etihad uses hedging to smooth expense volatility, but hedges expose the carrier to basis risk when jet fuel and crude move differently.

Fleet renewal and operational measures (route optimization, weight reduction) lower fuel burn and partially offset spikes, while USD-denominated fuel purchases add currency exposure when AED or partner currencies fluctuate against the dollar.

Global GDP, tourism flows, and trade

Passenger and cargo demand for Etihad closely follows global GDP growth, which the IMF projected at about 3.1% for 2024 and ~3.0% for 2025, driving RPK and freight volumes. Abu Dhabi’s tourism agenda and events calendar (e.g., major cultural and sporting events) bolster inbound leisure traffic and seasonally lift load factors. Slower global trade weakens cargo yields and belly capacity utilization, pressuring cargo revenue per kg. Premium cabin demand mirrors corporate travel budgets and oil-sector activity, sensitive to oil prices near the mid-70s to mid-80s USD/bbl range.

Exchange rates and revenue mix

Multi-currency revenues expose Etihad to translation and transaction risks across ticket sales and cargo; the UAE dirham has been pegged to the US dollar since 1997, anchoring many costs to USD. USD strength in 2024 pressured non-USD demand while easing USD-priced inputs like fuel and aircraft leases. Pricing, surcharges and natural hedges (route-level currency matching) are used to balance exposures. Network diversification across more than 70 destinations reduces regional concentration risk.

Capital intensity and financing costs

Widebody acquisitions, leases and engine maintenance drive Etihad’s high capex and cash needs, forcing reliance on operating leases and maintenance reserves to preserve liquidity. Interest rate cycles directly shape lease rates and refinancing costs, affecting unit cost and RASK sensitivity. Access to export credit agencies and Islamic finance structures can lower funding costs and extend maturities. Capacity discipline is essential to protect load factors and RASK.

- Capex drivers: widebodies, engines, MRO

- Financing: leases, export credit, sukuk

- Rates impact: lease/refinance sensitivity

- Network: capacity discipline → load factor/RASK

Airport capacity and slot economics

Hub infrastructure and terminal efficiency at Abu Dhabi reduce Etihad turnaround times and improve connectivity; Abu Dhabi Airport aims to expand capacity to ~45 million passengers to 2030, underpinning long‑term growth. Scarcity at full gateways such as Heathrow (~99% runway utilization) pushes slot acquisition and lease costs sharply higher. Wave scheduling preserves banked connections and can boost yields on peak banks.

- Abu Dhabi expansion: ~45M p.a. target to 2030

- Heathrow utilization: ~99%, elevating slot costs

- Wave scheduling: higher yields on banked banks

State-owned, aligned to Abu Dhabi 2030; 67 destinations, slots capped

Jet fuel (~$95/barrel in 2024) is Etihad’s largest cost driver, hedged but exposing basis risk; fleet renewal and ops cuts reduce burn. Global GDP ~3.1% (IMF 2024) guides pax/cargo demand while UAE dirham peg to USD ties costs to dollar moves. High capex (widebodies, engines) and rising lease rates increase funding needs; Abu Dhabi airport capacity target ~45M by 2030 supports growth.

| Metric | Value |

|---|---|

| Jet fuel (2024) | $95/bbl |

| Global GDP (2024) | 3.1% |

| Abu Dhabi capacity target | ~45M by 2030 |

| Heathrow utilization | ~99% |

Preview Before You Purchase

Etihad Airways PESTLE Analysis

The preview shown here is the exact Etihad Airways PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with professional structure and no placeholders. After checkout you’ll instantly download this identical file, ready for analysis and presentation.