Etisalat Porter's Five Forces Analysis

From Overview to Strategy Blueprint

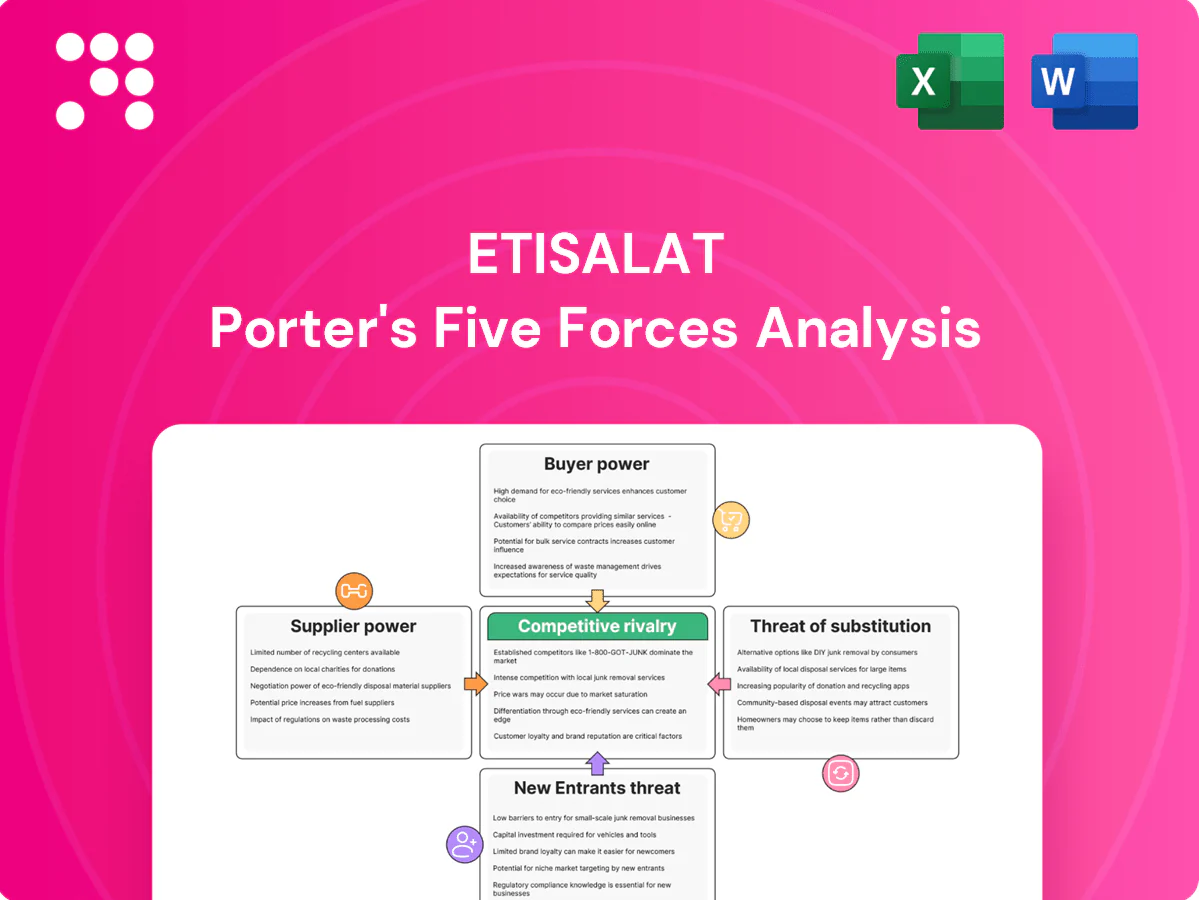

Etisalat faces intense rivalry, moderate buyer power, regulated supplier dynamics, high barriers to entry but rising tech-based substitutes; this snapshot highlights key pressures shaping margins and growth. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated network vendors

Core RAN/5G gear for Etisalat is sourced from a concentrated group of vendors—about 70% of the global RAN market in 2024—raising switching costs and integration risk. Limited alternatives boost vendor leverage on pricing and contract terms. Multi-vendor strategies mitigate single-supplier risk but add interoperability and performance-assurance complexity and OpEx. Long lifecycle assets (typically 7–10 years) further deepen dependence.

Spectrum and regulatory dependence

Governments act as unique suppliers by controlling spectrum licensing and fees, with license terms, renewal risk and coverage obligations directly shaping Etisalat’s cost structure. Policy shifts can rapidly change economics, constraining pricing and investment timing. Regulatory compliance reduces negotiation flexibility and raises switching costs, increasing supplier bargaining power over the operator.

Subsea, backhaul, and tower inputs

Capacity on submarine cables, fiber backhaul and tower access remains essential and regionally concentrated, with consortium-led builds and anchor tenants shaping capacity allocation in 2024. Consortium dynamics and anchor tenants frequently set commercial terms, squeezing smaller operators' margins. Where towercos dominate, rental escalators and multi-year lock-ins raise operating costs; owning assets mitigates exposure but is not feasible across all markets.

Handset OEMs and device ecosystems

Flagship OEMs such as Apple and Samsung shape device financing, promotions and 5G rollout timing; Gulf market concentrations give them leverage over subsidies when popular models are scarce. Broad Android diversity (dozens of OEMs) reduces single-vendor dependence, while US-China trade shifts and chipset cycle timing (annual flagship SoC releases) create periodic volatility for Etisalat.

- OEM leverage: influences financing and promo terms

- Scarcity: pressures subsidy budgets

- Android breadth: dilutes single-OEM power

- Volatility: trade policy and chipset cycles

Cloud, IT, and platform partners

Dependence on hyperscalers and enterprise software vendors intensifies as Etisalat expands digital, fintech, IoT and AI services; global cloud market shares in 2024 are roughly AWS 32%, Azure 23%, GCP 10%, concentrating supplier leverage. Data residency and integration constraints in UAE and regional regimes limit switching and raise migration costs. Usage-based pricing often grows with scale, creating variable OPEX that can outpace revenue without optimization; joint go-to-market deals can rebalance commercial terms but embed co-dependencies.

- Hyperscaler concentration: AWS 32%, Azure 23%, GCP 10% (2024)

- Data residency/integration: raises lock-in and migration costs

- Usage-based pricing: variable OPEX rises with scale

- JGTM: can secure better terms but increases supplier interdependence

Suppliers wield outsized power: RAN/5G OEMs ~70%, AWS 32%

Suppliers hold high leverage: core RAN/5G vendors control ~70% of the market in 2024, raising switching costs and pricing power. Spectrum/licensing by governments and long 7–10 year RAN lifecycles constrain Etisalat’s negotiation flexibility. Hyperscaler concentration (AWS 32%, Azure 23%, GCP 10% in 2024) and tower/submarine consortiums further elevate supplier bargaining power.

| Supplier | Key 2024 Metric |

|---|---|

| RAN/5G OEMs | ~70% global share |

| Hyperscalers | AWS 32% / Azure 23% / GCP 10% |

| RAN lifecycle | 7–10 years |

What is included in the product

Concise Porter's Five Forces analysis of Etisalat, identifying competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, plus regulatory and technological disruptors shaping pricing, margins, and strategic defenses.

A clear, one-sheet summary of Etisalat's Five Forces—instantly spot regulatory, competitive, supplier and buyer pressure points to guide swift strategic decisions. Clean layout ready to drop into decks or dashboards for boardroom-ready analysis.

Customers Bargaining Power

Price-sensitive mass market

Price-sensitive mass-market customers routinely compare tariffs, data allowances and promos, driving tariff pressure in a UAE market with mobile subscriptions exceeding 200% of population in 2024 and smartphone penetration above 80%. Number portability and prepaid flexibility make churn easier, while bundles can lock customers but must match market promos to retain value. Digital channels and comparison apps amplify transparency and accelerate switching.

Large enterprise and government accounts

In 2024 large enterprise and government accounts continued to demand bespoke SLAs and steep discounts, leveraging mission-critical connectivity and ICT projects to extract concessions. Their volume and strategic importance give them strong bargaining power, while multi-year contracts (commonly 3–5 years) reduce churn but compress margins. Aggressive cross-selling of IoT, cloud and security helps Etisalat offset pricing pressure.

International wholesale buyers

International wholesale buyers, including 700+ roaming partners, press Etisalat on interconnect and capacity rates, using global price benchmarks that cap upside. Superior route quality and low latency allow Etisalat to command premiums, especially for premium data/voice routes. Large volume commitments commonly secure substantial rate relief, shifting bargaining power toward high-volume buyers.

OTT-influenced expectations

Customers now benchmark telco services against app-like experiences; expectations for zero-friction onboarding, robust self-care and instant support raise the service bar and directly influence retention. Poor CX rapidly accelerates switching, while Etisalat (e&) H1 2024 revenues of AED 27.9bn underline the commercial stakes of churn and ARPU preservation. Value-added digital services can shift focus away from pure price competition.

- Benchmarking: app-like UX

- Onboarding: zero-friction required

- Support: instant, self-care driven

- Risk: poor CX → faster churn

- Strategy: digital services to protect ARPU

MVNO and channel options

Availability of MVNOs in the UAE gives consumers lower-cost alternatives and increases price sensitivity against Etisalat; UAE mobile penetration is roughly 200% in 2024, intensifying churn pressure. Retailers and online aggregators simplify comparison shopping and can drive promotional pricing. Distribution partners can demand commissions that squeeze margins, while Etisalat’s differentiated network quality and bundled services (fixed-mobile convergence) help retain higher-value customers.

- MVNOs: lower-cost alternatives

- Aggregators: easier comparison

- Partners: commission pressure

- Network/bundles: retention lever

UAE telcos face churn as 200%+ mobile subs and 80%+ smartphone pen. squeeze ARPU

Customers exert strong price and service pressure: UAE mobile subscriptions >200% and smartphone penetration >80% in 2024 drive high churn risk; Etisalat H1 2024 revenues AED 27.9bn. Enterprises leverage 3–5 year SLAs for discounts; 700+ roaming partners push wholesale rate negotiation. MVNOs and aggregators increase price transparency, while network quality and bundles remain key retention levers.

| Metric | 2024 | Impact |

|---|---|---|

| Mobile subs | >200% pop | High churn |

| Smartphone pen. | >80% | Data demand |

| H1 revenues | AED 27.9bn | ARPU focus |

Full Version Awaits

Etisalat Porter's Five Forces Analysis

This preview shows the exact Etisalat Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The analysis evaluates competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications with data-backed insights. Fully formatted and ready for instant download and use upon payment.

From Overview to Strategy Blueprint

Etisalat faces intense rivalry, moderate buyer power, regulated supplier dynamics, high barriers to entry but rising tech-based substitutes; this snapshot highlights key pressures shaping margins and growth. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated network vendors

Core RAN/5G gear for Etisalat is sourced from a concentrated group of vendors—about 70% of the global RAN market in 2024—raising switching costs and integration risk. Limited alternatives boost vendor leverage on pricing and contract terms. Multi-vendor strategies mitigate single-supplier risk but add interoperability and performance-assurance complexity and OpEx. Long lifecycle assets (typically 7–10 years) further deepen dependence.

Spectrum and regulatory dependence

Governments act as unique suppliers by controlling spectrum licensing and fees, with license terms, renewal risk and coverage obligations directly shaping Etisalat’s cost structure. Policy shifts can rapidly change economics, constraining pricing and investment timing. Regulatory compliance reduces negotiation flexibility and raises switching costs, increasing supplier bargaining power over the operator.

Subsea, backhaul, and tower inputs

Capacity on submarine cables, fiber backhaul and tower access remains essential and regionally concentrated, with consortium-led builds and anchor tenants shaping capacity allocation in 2024. Consortium dynamics and anchor tenants frequently set commercial terms, squeezing smaller operators' margins. Where towercos dominate, rental escalators and multi-year lock-ins raise operating costs; owning assets mitigates exposure but is not feasible across all markets.

Handset OEMs and device ecosystems

Flagship OEMs such as Apple and Samsung shape device financing, promotions and 5G rollout timing; Gulf market concentrations give them leverage over subsidies when popular models are scarce. Broad Android diversity (dozens of OEMs) reduces single-vendor dependence, while US-China trade shifts and chipset cycle timing (annual flagship SoC releases) create periodic volatility for Etisalat.

- OEM leverage: influences financing and promo terms

- Scarcity: pressures subsidy budgets

- Android breadth: dilutes single-OEM power

- Volatility: trade policy and chipset cycles

Cloud, IT, and platform partners

Dependence on hyperscalers and enterprise software vendors intensifies as Etisalat expands digital, fintech, IoT and AI services; global cloud market shares in 2024 are roughly AWS 32%, Azure 23%, GCP 10%, concentrating supplier leverage. Data residency and integration constraints in UAE and regional regimes limit switching and raise migration costs. Usage-based pricing often grows with scale, creating variable OPEX that can outpace revenue without optimization; joint go-to-market deals can rebalance commercial terms but embed co-dependencies.

- Hyperscaler concentration: AWS 32%, Azure 23%, GCP 10% (2024)

- Data residency/integration: raises lock-in and migration costs

- Usage-based pricing: variable OPEX rises with scale

- JGTM: can secure better terms but increases supplier interdependence

Suppliers wield outsized power: RAN/5G OEMs ~70%, AWS 32%

Suppliers hold high leverage: core RAN/5G vendors control ~70% of the market in 2024, raising switching costs and pricing power. Spectrum/licensing by governments and long 7–10 year RAN lifecycles constrain Etisalat’s negotiation flexibility. Hyperscaler concentration (AWS 32%, Azure 23%, GCP 10% in 2024) and tower/submarine consortiums further elevate supplier bargaining power.

| Supplier | Key 2024 Metric |

|---|---|

| RAN/5G OEMs | ~70% global share |

| Hyperscalers | AWS 32% / Azure 23% / GCP 10% |

| RAN lifecycle | 7–10 years |

What is included in the product

Concise Porter's Five Forces analysis of Etisalat, identifying competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, plus regulatory and technological disruptors shaping pricing, margins, and strategic defenses.

A clear, one-sheet summary of Etisalat's Five Forces—instantly spot regulatory, competitive, supplier and buyer pressure points to guide swift strategic decisions. Clean layout ready to drop into decks or dashboards for boardroom-ready analysis.

Customers Bargaining Power

Price-sensitive mass market

Price-sensitive mass-market customers routinely compare tariffs, data allowances and promos, driving tariff pressure in a UAE market with mobile subscriptions exceeding 200% of population in 2024 and smartphone penetration above 80%. Number portability and prepaid flexibility make churn easier, while bundles can lock customers but must match market promos to retain value. Digital channels and comparison apps amplify transparency and accelerate switching.

Large enterprise and government accounts

In 2024 large enterprise and government accounts continued to demand bespoke SLAs and steep discounts, leveraging mission-critical connectivity and ICT projects to extract concessions. Their volume and strategic importance give them strong bargaining power, while multi-year contracts (commonly 3–5 years) reduce churn but compress margins. Aggressive cross-selling of IoT, cloud and security helps Etisalat offset pricing pressure.

International wholesale buyers

International wholesale buyers, including 700+ roaming partners, press Etisalat on interconnect and capacity rates, using global price benchmarks that cap upside. Superior route quality and low latency allow Etisalat to command premiums, especially for premium data/voice routes. Large volume commitments commonly secure substantial rate relief, shifting bargaining power toward high-volume buyers.

OTT-influenced expectations

Customers now benchmark telco services against app-like experiences; expectations for zero-friction onboarding, robust self-care and instant support raise the service bar and directly influence retention. Poor CX rapidly accelerates switching, while Etisalat (e&) H1 2024 revenues of AED 27.9bn underline the commercial stakes of churn and ARPU preservation. Value-added digital services can shift focus away from pure price competition.

- Benchmarking: app-like UX

- Onboarding: zero-friction required

- Support: instant, self-care driven

- Risk: poor CX → faster churn

- Strategy: digital services to protect ARPU

MVNO and channel options

Availability of MVNOs in the UAE gives consumers lower-cost alternatives and increases price sensitivity against Etisalat; UAE mobile penetration is roughly 200% in 2024, intensifying churn pressure. Retailers and online aggregators simplify comparison shopping and can drive promotional pricing. Distribution partners can demand commissions that squeeze margins, while Etisalat’s differentiated network quality and bundled services (fixed-mobile convergence) help retain higher-value customers.

- MVNOs: lower-cost alternatives

- Aggregators: easier comparison

- Partners: commission pressure

- Network/bundles: retention lever

UAE telcos face churn as 200%+ mobile subs and 80%+ smartphone pen. squeeze ARPU

Customers exert strong price and service pressure: UAE mobile subscriptions >200% and smartphone penetration >80% in 2024 drive high churn risk; Etisalat H1 2024 revenues AED 27.9bn. Enterprises leverage 3–5 year SLAs for discounts; 700+ roaming partners push wholesale rate negotiation. MVNOs and aggregators increase price transparency, while network quality and bundles remain key retention levers.

| Metric | 2024 | Impact |

|---|---|---|

| Mobile subs | >200% pop | High churn |

| Smartphone pen. | >80% | Data demand |

| H1 revenues | AED 27.9bn | ARPU focus |

Full Version Awaits

Etisalat Porter's Five Forces Analysis

This preview shows the exact Etisalat Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The analysis evaluates competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications with data-backed insights. Fully formatted and ready for instant download and use upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Etisalat faces intense rivalry, moderate buyer power, regulated supplier dynamics, high barriers to entry but rising tech-based substitutes; this snapshot highlights key pressures shaping margins and growth. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated network vendors

Core RAN/5G gear for Etisalat is sourced from a concentrated group of vendors—about 70% of the global RAN market in 2024—raising switching costs and integration risk. Limited alternatives boost vendor leverage on pricing and contract terms. Multi-vendor strategies mitigate single-supplier risk but add interoperability and performance-assurance complexity and OpEx. Long lifecycle assets (typically 7–10 years) further deepen dependence.

Spectrum and regulatory dependence

Governments act as unique suppliers by controlling spectrum licensing and fees, with license terms, renewal risk and coverage obligations directly shaping Etisalat’s cost structure. Policy shifts can rapidly change economics, constraining pricing and investment timing. Regulatory compliance reduces negotiation flexibility and raises switching costs, increasing supplier bargaining power over the operator.

Subsea, backhaul, and tower inputs

Capacity on submarine cables, fiber backhaul and tower access remains essential and regionally concentrated, with consortium-led builds and anchor tenants shaping capacity allocation in 2024. Consortium dynamics and anchor tenants frequently set commercial terms, squeezing smaller operators' margins. Where towercos dominate, rental escalators and multi-year lock-ins raise operating costs; owning assets mitigates exposure but is not feasible across all markets.

Handset OEMs and device ecosystems

Flagship OEMs such as Apple and Samsung shape device financing, promotions and 5G rollout timing; Gulf market concentrations give them leverage over subsidies when popular models are scarce. Broad Android diversity (dozens of OEMs) reduces single-vendor dependence, while US-China trade shifts and chipset cycle timing (annual flagship SoC releases) create periodic volatility for Etisalat.

- OEM leverage: influences financing and promo terms

- Scarcity: pressures subsidy budgets

- Android breadth: dilutes single-OEM power

- Volatility: trade policy and chipset cycles

Cloud, IT, and platform partners

Dependence on hyperscalers and enterprise software vendors intensifies as Etisalat expands digital, fintech, IoT and AI services; global cloud market shares in 2024 are roughly AWS 32%, Azure 23%, GCP 10%, concentrating supplier leverage. Data residency and integration constraints in UAE and regional regimes limit switching and raise migration costs. Usage-based pricing often grows with scale, creating variable OPEX that can outpace revenue without optimization; joint go-to-market deals can rebalance commercial terms but embed co-dependencies.

- Hyperscaler concentration: AWS 32%, Azure 23%, GCP 10% (2024)

- Data residency/integration: raises lock-in and migration costs

- Usage-based pricing: variable OPEX rises with scale

- JGTM: can secure better terms but increases supplier interdependence

Suppliers wield outsized power: RAN/5G OEMs ~70%, AWS 32%

Suppliers hold high leverage: core RAN/5G vendors control ~70% of the market in 2024, raising switching costs and pricing power. Spectrum/licensing by governments and long 7–10 year RAN lifecycles constrain Etisalat’s negotiation flexibility. Hyperscaler concentration (AWS 32%, Azure 23%, GCP 10% in 2024) and tower/submarine consortiums further elevate supplier bargaining power.

| Supplier | Key 2024 Metric |

|---|---|

| RAN/5G OEMs | ~70% global share |

| Hyperscalers | AWS 32% / Azure 23% / GCP 10% |

| RAN lifecycle | 7–10 years |

What is included in the product

Concise Porter's Five Forces analysis of Etisalat, identifying competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, plus regulatory and technological disruptors shaping pricing, margins, and strategic defenses.

A clear, one-sheet summary of Etisalat's Five Forces—instantly spot regulatory, competitive, supplier and buyer pressure points to guide swift strategic decisions. Clean layout ready to drop into decks or dashboards for boardroom-ready analysis.

Customers Bargaining Power

Price-sensitive mass market

Price-sensitive mass-market customers routinely compare tariffs, data allowances and promos, driving tariff pressure in a UAE market with mobile subscriptions exceeding 200% of population in 2024 and smartphone penetration above 80%. Number portability and prepaid flexibility make churn easier, while bundles can lock customers but must match market promos to retain value. Digital channels and comparison apps amplify transparency and accelerate switching.

Large enterprise and government accounts

In 2024 large enterprise and government accounts continued to demand bespoke SLAs and steep discounts, leveraging mission-critical connectivity and ICT projects to extract concessions. Their volume and strategic importance give them strong bargaining power, while multi-year contracts (commonly 3–5 years) reduce churn but compress margins. Aggressive cross-selling of IoT, cloud and security helps Etisalat offset pricing pressure.

International wholesale buyers

International wholesale buyers, including 700+ roaming partners, press Etisalat on interconnect and capacity rates, using global price benchmarks that cap upside. Superior route quality and low latency allow Etisalat to command premiums, especially for premium data/voice routes. Large volume commitments commonly secure substantial rate relief, shifting bargaining power toward high-volume buyers.

OTT-influenced expectations

Customers now benchmark telco services against app-like experiences; expectations for zero-friction onboarding, robust self-care and instant support raise the service bar and directly influence retention. Poor CX rapidly accelerates switching, while Etisalat (e&) H1 2024 revenues of AED 27.9bn underline the commercial stakes of churn and ARPU preservation. Value-added digital services can shift focus away from pure price competition.

- Benchmarking: app-like UX

- Onboarding: zero-friction required

- Support: instant, self-care driven

- Risk: poor CX → faster churn

- Strategy: digital services to protect ARPU

MVNO and channel options

Availability of MVNOs in the UAE gives consumers lower-cost alternatives and increases price sensitivity against Etisalat; UAE mobile penetration is roughly 200% in 2024, intensifying churn pressure. Retailers and online aggregators simplify comparison shopping and can drive promotional pricing. Distribution partners can demand commissions that squeeze margins, while Etisalat’s differentiated network quality and bundled services (fixed-mobile convergence) help retain higher-value customers.

- MVNOs: lower-cost alternatives

- Aggregators: easier comparison

- Partners: commission pressure

- Network/bundles: retention lever

UAE telcos face churn as 200%+ mobile subs and 80%+ smartphone pen. squeeze ARPU

Customers exert strong price and service pressure: UAE mobile subscriptions >200% and smartphone penetration >80% in 2024 drive high churn risk; Etisalat H1 2024 revenues AED 27.9bn. Enterprises leverage 3–5 year SLAs for discounts; 700+ roaming partners push wholesale rate negotiation. MVNOs and aggregators increase price transparency, while network quality and bundles remain key retention levers.

| Metric | 2024 | Impact |

|---|---|---|

| Mobile subs | >200% pop | High churn |

| Smartphone pen. | >80% | Data demand |

| H1 revenues | AED 27.9bn | ARPU focus |

Full Version Awaits

Etisalat Porter's Five Forces Analysis

This preview shows the exact Etisalat Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The analysis evaluates competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications with data-backed insights. Fully formatted and ready for instant download and use upon payment.