Evercore PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

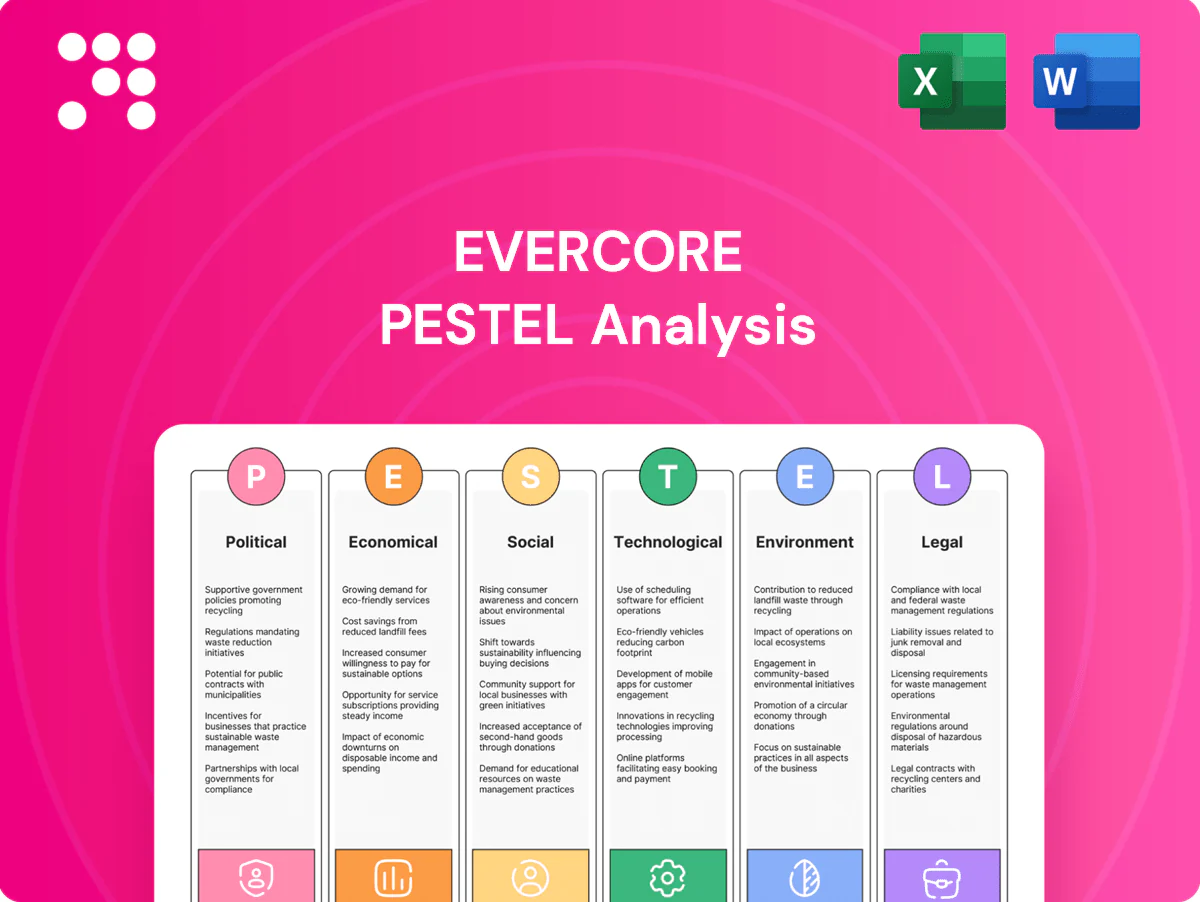

Gain a competitive edge with our Evercore PESTLE Analysis—concise, research-backed insight into political, economic, social, technological, legal, and environmental forces shaping Evercore's future. Ideal for investors and strategists; purchase the full report to access actionable, ready-to-use intelligence.

Political factors

Geopolitical tensions and regional instability

Shifts in global power dynamics are reshaping cross-border M&A appetite and raising regulatory scrutiny, contributing to volatility in deal pipelines; UNCTAD reported global FDI fell to about $1.11 trillion in 2023. Conflicts, tariffs and diplomatic rifts can delay approvals and widen valuation gaps, increasing hold-period risk. Evercore must embed political-risk assessment into transaction structures and timelines, using scenario planning and country-risk analytics to protect deal certainty.

Trade policy and investment screening

Trade restrictions and tightened FDI screening (CFIUS, EU FSR) are reshaping inbound/outbound deals, with over 60 jurisdictions operating screening regimes and higher scrutiny in semiconductors, defense and data infrastructure. Evercore must embed regulatory pathways in deal design early, using strategic positioning and binding mitigation commitments to preserve viability and speed approvals.

Government fiscal and industrial policy

Government fiscal and industrial policy, via subsidies and reshoring incentives, is driving consolidation in targeted sectors; US IIJA totals $1.2 trillion (about $550 billion new spending) and the CHIPS Act provides $52 billion for domestic semiconductor capacity.

Policy-driven capital allocation—notably the US Inflation Reduction Act and EU NextGenerationEU (about €800 billion)—fuels deal pipelines in energy transition, infrastructure and healthcare.

Evercore can align coverage to policy-backed growth arenas and win advisory mandates by mastering grants, tax-credit mechanics and public–private frameworks.

Election cycles and policy uncertainty

Elections, notably the 2024 US cycle, shift antitrust enforcement intensity, tax regime debate and fiscal spending priorities, prompting clients to accelerate or defer deals around key milestones; Evercore times processes and uses earnouts to hedge post-election policy shifts and valuation risk. Targeted outreach to policy-sensitive sectors such as healthcare, defense and energy sustains deal momentum.

- Antitrust focus: timing advisory to anticipate enforcement swings

- Tax/spend: structure earnouts to bridge pre/post-election valuations

- Client behavior: accelerate/hold transactions around electoral milestones

- Outreach: prioritize healthcare, defense, energy for continuity

Sanctions regimes and national security priorities

Expanding sanctions regimes complicate diligence, counterparty screening, and financing, increasing Evercore's compliance workload and transaction risk; national security reviews for critical technologies and infrastructure routinely extend deal timelines and may require mitigation agreements. Evercore must maintain robust sanctions compliance, map alternative buyer universes, and embed adaptive covenants in deal documentation to address evolving lists and review outcomes.

- Sanctions compliance: continuous monitoring

- Counterparty screening: enhanced KYC and AML

- Alternative buyers: proactive mapping

- Deal docs: adaptive covenants and exit clauses

Geopolitics and 60+ FDI screens reshape M&A: policy cash flows, longer regulatory timelines

Geopolitical shifts and 60+ FDI screening regimes are raising transaction scrutiny and delaying M&A; UNCTAD FDI fell to $1.11T in 2023. Policy drives deal flow—IIJA $1.2T (≈$550B new), CHIPS $52B, EU NextGenerationEU ≈€800B—while sanctions and national-security reviews extend timelines. Evercore must embed political-risk analytics, adaptive covenants and regulatory pathways into deal design.

| Metric | Value |

|---|---|

| Global FDI (2023) | $1.11T |

| Screening regimes | 60+ jurisdictions |

| CHIPS | $52B |

What is included in the product

Explores how macro-environmental factors uniquely affect Evercore across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific regulatory context. Designed to support executives and investors with forward-looking insights, clean formatting, and actionable scenarios.

A concise, visually segmented PESTLE summary of Evercore that’s easily editable and shareable—ideal for dropping into presentations, aligning teams, and supporting strategic discussions on external risks and market positioning.

Economic factors

Interest rate trajectory and credit availability

With policy rates near 5.25–5.50% in mid-2025, discount rates are higher, compressing debt capacity and squeezing LBO returns. Tighter credit in 2023–24 curtailed sponsor-backed deal volume while partial easing in 2024–25 has begun to reopen activity. Evercore’s restructuring and liability-management practices hedge this cyclicality. Active lender mapping and bespoke financing structures sustain deal execution.

Equity market valuations and IPO window

Public market multiples, e.g., S&P 500 forward P/E ~17.0 as of July 2025 (Bloomberg), set reference prices for M&A and carve-outs. A recovering IPO window in H1 2025 after the 2022–23 slump enables dual-track processes and valuation tension. Evercore can optimize timing between public and private routes, using volatility hedges and go-to-market readiness to accelerate captures when windows open.

Private capital dry powder and fundraising cycles

Global private capital dry powder stood near $3.2 trillion as of mid-2024, with PE and infrastructure funds’ undeployed capital underwriting elevated buy-side demand. Slower exits—exit value down roughly 40% in 2023 versus prior peaks—have pressured DPI and pacing, changing sponsor behavior toward liquidity solutions. Evercore can structure continuation vehicles and GP-led deals, offering tailored capital to bridge valuation gaps and meet sponsor liquidity needs.

Macroeconomic growth and sector rotation

Currency movements and cross-border arbitrage

FX swings create relative value that drives cross-border bids; the US dollar's ~4% trade-weighted rise in 2024 heightened arbitrage opportunities and raised hedging costs, while translation risk alters pro formas and financing structures. Evercore can embed FX strategies in acquisition finance to reduce forward-cost exposure and use currency-aware comparables to sharpen negotiation leverage.

- FX volatility: +4% DXY (2024)

- Hedging impact: higher forward spreads

- Deal strategy: embedded FX in financing

- Valuation: currency-aware comps

Geopolitics and 60+ FDI screens reshape M&A: policy cash flows, longer regulatory timelines

With policy rates ~5.25–5.50% in mid-2025, higher discount rates compress debt capacity and LBO returns. S&P 500 forward P/E ~17.0 (Jul 2025) and a recovering IPO window shape exit timing. Global private capital dry powder ~$3.2T (mid-2024) sustains buy-side demand while GDP 2024 ~3.1% (US ~2.6%) shifts sector focus; DXY +4% (2024) raises hedging costs.

| Metric | Value |

|---|---|

| Policy rate | 5.25–5.50% (mid-2025) |

| S&P 500 fwd P/E | ~17.0 (Jul 2025) |

| Dry powder | ~$3.2T (mid-2024) |

| GDP 2024 | ~3.1% (US ~2.6%) |

| DXY | +4% (2024) |

Preview Before You Purchase

Evercore PESTLE Analysis

The Evercore PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This snapshot reflects the final content, layout, and depth of analysis without placeholders or edits. After checkout you’ll instantly download this same complete file.

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our Evercore PESTLE Analysis—concise, research-backed insight into political, economic, social, technological, legal, and environmental forces shaping Evercore's future. Ideal for investors and strategists; purchase the full report to access actionable, ready-to-use intelligence.

Political factors

Geopolitical tensions and regional instability

Shifts in global power dynamics are reshaping cross-border M&A appetite and raising regulatory scrutiny, contributing to volatility in deal pipelines; UNCTAD reported global FDI fell to about $1.11 trillion in 2023. Conflicts, tariffs and diplomatic rifts can delay approvals and widen valuation gaps, increasing hold-period risk. Evercore must embed political-risk assessment into transaction structures and timelines, using scenario planning and country-risk analytics to protect deal certainty.

Trade policy and investment screening

Trade restrictions and tightened FDI screening (CFIUS, EU FSR) are reshaping inbound/outbound deals, with over 60 jurisdictions operating screening regimes and higher scrutiny in semiconductors, defense and data infrastructure. Evercore must embed regulatory pathways in deal design early, using strategic positioning and binding mitigation commitments to preserve viability and speed approvals.

Government fiscal and industrial policy

Government fiscal and industrial policy, via subsidies and reshoring incentives, is driving consolidation in targeted sectors; US IIJA totals $1.2 trillion (about $550 billion new spending) and the CHIPS Act provides $52 billion for domestic semiconductor capacity.

Policy-driven capital allocation—notably the US Inflation Reduction Act and EU NextGenerationEU (about €800 billion)—fuels deal pipelines in energy transition, infrastructure and healthcare.

Evercore can align coverage to policy-backed growth arenas and win advisory mandates by mastering grants, tax-credit mechanics and public–private frameworks.

Election cycles and policy uncertainty

Elections, notably the 2024 US cycle, shift antitrust enforcement intensity, tax regime debate and fiscal spending priorities, prompting clients to accelerate or defer deals around key milestones; Evercore times processes and uses earnouts to hedge post-election policy shifts and valuation risk. Targeted outreach to policy-sensitive sectors such as healthcare, defense and energy sustains deal momentum.

- Antitrust focus: timing advisory to anticipate enforcement swings

- Tax/spend: structure earnouts to bridge pre/post-election valuations

- Client behavior: accelerate/hold transactions around electoral milestones

- Outreach: prioritize healthcare, defense, energy for continuity

Sanctions regimes and national security priorities

Expanding sanctions regimes complicate diligence, counterparty screening, and financing, increasing Evercore's compliance workload and transaction risk; national security reviews for critical technologies and infrastructure routinely extend deal timelines and may require mitigation agreements. Evercore must maintain robust sanctions compliance, map alternative buyer universes, and embed adaptive covenants in deal documentation to address evolving lists and review outcomes.

- Sanctions compliance: continuous monitoring

- Counterparty screening: enhanced KYC and AML

- Alternative buyers: proactive mapping

- Deal docs: adaptive covenants and exit clauses

Geopolitics and 60+ FDI screens reshape M&A: policy cash flows, longer regulatory timelines

Geopolitical shifts and 60+ FDI screening regimes are raising transaction scrutiny and delaying M&A; UNCTAD FDI fell to $1.11T in 2023. Policy drives deal flow—IIJA $1.2T (≈$550B new), CHIPS $52B, EU NextGenerationEU ≈€800B—while sanctions and national-security reviews extend timelines. Evercore must embed political-risk analytics, adaptive covenants and regulatory pathways into deal design.

| Metric | Value |

|---|---|

| Global FDI (2023) | $1.11T |

| Screening regimes | 60+ jurisdictions |

| CHIPS | $52B |

What is included in the product

Explores how macro-environmental factors uniquely affect Evercore across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific regulatory context. Designed to support executives and investors with forward-looking insights, clean formatting, and actionable scenarios.

A concise, visually segmented PESTLE summary of Evercore that’s easily editable and shareable—ideal for dropping into presentations, aligning teams, and supporting strategic discussions on external risks and market positioning.

Economic factors

Interest rate trajectory and credit availability

With policy rates near 5.25–5.50% in mid-2025, discount rates are higher, compressing debt capacity and squeezing LBO returns. Tighter credit in 2023–24 curtailed sponsor-backed deal volume while partial easing in 2024–25 has begun to reopen activity. Evercore’s restructuring and liability-management practices hedge this cyclicality. Active lender mapping and bespoke financing structures sustain deal execution.

Equity market valuations and IPO window

Public market multiples, e.g., S&P 500 forward P/E ~17.0 as of July 2025 (Bloomberg), set reference prices for M&A and carve-outs. A recovering IPO window in H1 2025 after the 2022–23 slump enables dual-track processes and valuation tension. Evercore can optimize timing between public and private routes, using volatility hedges and go-to-market readiness to accelerate captures when windows open.

Private capital dry powder and fundraising cycles

Global private capital dry powder stood near $3.2 trillion as of mid-2024, with PE and infrastructure funds’ undeployed capital underwriting elevated buy-side demand. Slower exits—exit value down roughly 40% in 2023 versus prior peaks—have pressured DPI and pacing, changing sponsor behavior toward liquidity solutions. Evercore can structure continuation vehicles and GP-led deals, offering tailored capital to bridge valuation gaps and meet sponsor liquidity needs.

Macroeconomic growth and sector rotation

Currency movements and cross-border arbitrage

FX swings create relative value that drives cross-border bids; the US dollar's ~4% trade-weighted rise in 2024 heightened arbitrage opportunities and raised hedging costs, while translation risk alters pro formas and financing structures. Evercore can embed FX strategies in acquisition finance to reduce forward-cost exposure and use currency-aware comparables to sharpen negotiation leverage.

- FX volatility: +4% DXY (2024)

- Hedging impact: higher forward spreads

- Deal strategy: embedded FX in financing

- Valuation: currency-aware comps

Geopolitics and 60+ FDI screens reshape M&A: policy cash flows, longer regulatory timelines

With policy rates ~5.25–5.50% in mid-2025, higher discount rates compress debt capacity and LBO returns. S&P 500 forward P/E ~17.0 (Jul 2025) and a recovering IPO window shape exit timing. Global private capital dry powder ~$3.2T (mid-2024) sustains buy-side demand while GDP 2024 ~3.1% (US ~2.6%) shifts sector focus; DXY +4% (2024) raises hedging costs.

| Metric | Value |

|---|---|

| Policy rate | 5.25–5.50% (mid-2025) |

| S&P 500 fwd P/E | ~17.0 (Jul 2025) |

| Dry powder | ~$3.2T (mid-2024) |

| GDP 2024 | ~3.1% (US ~2.6%) |

| DXY | +4% (2024) |

Preview Before You Purchase

Evercore PESTLE Analysis

The Evercore PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This snapshot reflects the final content, layout, and depth of analysis without placeholders or edits. After checkout you’ll instantly download this same complete file.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our Evercore PESTLE Analysis—concise, research-backed insight into political, economic, social, technological, legal, and environmental forces shaping Evercore's future. Ideal for investors and strategists; purchase the full report to access actionable, ready-to-use intelligence.

Political factors

Geopolitical tensions and regional instability

Shifts in global power dynamics are reshaping cross-border M&A appetite and raising regulatory scrutiny, contributing to volatility in deal pipelines; UNCTAD reported global FDI fell to about $1.11 trillion in 2023. Conflicts, tariffs and diplomatic rifts can delay approvals and widen valuation gaps, increasing hold-period risk. Evercore must embed political-risk assessment into transaction structures and timelines, using scenario planning and country-risk analytics to protect deal certainty.

Trade policy and investment screening

Trade restrictions and tightened FDI screening (CFIUS, EU FSR) are reshaping inbound/outbound deals, with over 60 jurisdictions operating screening regimes and higher scrutiny in semiconductors, defense and data infrastructure. Evercore must embed regulatory pathways in deal design early, using strategic positioning and binding mitigation commitments to preserve viability and speed approvals.

Government fiscal and industrial policy

Government fiscal and industrial policy, via subsidies and reshoring incentives, is driving consolidation in targeted sectors; US IIJA totals $1.2 trillion (about $550 billion new spending) and the CHIPS Act provides $52 billion for domestic semiconductor capacity.

Policy-driven capital allocation—notably the US Inflation Reduction Act and EU NextGenerationEU (about €800 billion)—fuels deal pipelines in energy transition, infrastructure and healthcare.

Evercore can align coverage to policy-backed growth arenas and win advisory mandates by mastering grants, tax-credit mechanics and public–private frameworks.

Election cycles and policy uncertainty

Elections, notably the 2024 US cycle, shift antitrust enforcement intensity, tax regime debate and fiscal spending priorities, prompting clients to accelerate or defer deals around key milestones; Evercore times processes and uses earnouts to hedge post-election policy shifts and valuation risk. Targeted outreach to policy-sensitive sectors such as healthcare, defense and energy sustains deal momentum.

- Antitrust focus: timing advisory to anticipate enforcement swings

- Tax/spend: structure earnouts to bridge pre/post-election valuations

- Client behavior: accelerate/hold transactions around electoral milestones

- Outreach: prioritize healthcare, defense, energy for continuity

Sanctions regimes and national security priorities

Expanding sanctions regimes complicate diligence, counterparty screening, and financing, increasing Evercore's compliance workload and transaction risk; national security reviews for critical technologies and infrastructure routinely extend deal timelines and may require mitigation agreements. Evercore must maintain robust sanctions compliance, map alternative buyer universes, and embed adaptive covenants in deal documentation to address evolving lists and review outcomes.

- Sanctions compliance: continuous monitoring

- Counterparty screening: enhanced KYC and AML

- Alternative buyers: proactive mapping

- Deal docs: adaptive covenants and exit clauses

Geopolitics and 60+ FDI screens reshape M&A: policy cash flows, longer regulatory timelines

Geopolitical shifts and 60+ FDI screening regimes are raising transaction scrutiny and delaying M&A; UNCTAD FDI fell to $1.11T in 2023. Policy drives deal flow—IIJA $1.2T (≈$550B new), CHIPS $52B, EU NextGenerationEU ≈€800B—while sanctions and national-security reviews extend timelines. Evercore must embed political-risk analytics, adaptive covenants and regulatory pathways into deal design.

| Metric | Value |

|---|---|

| Global FDI (2023) | $1.11T |

| Screening regimes | 60+ jurisdictions |

| CHIPS | $52B |

What is included in the product

Explores how macro-environmental factors uniquely affect Evercore across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific regulatory context. Designed to support executives and investors with forward-looking insights, clean formatting, and actionable scenarios.

A concise, visually segmented PESTLE summary of Evercore that’s easily editable and shareable—ideal for dropping into presentations, aligning teams, and supporting strategic discussions on external risks and market positioning.

Economic factors

Interest rate trajectory and credit availability

With policy rates near 5.25–5.50% in mid-2025, discount rates are higher, compressing debt capacity and squeezing LBO returns. Tighter credit in 2023–24 curtailed sponsor-backed deal volume while partial easing in 2024–25 has begun to reopen activity. Evercore’s restructuring and liability-management practices hedge this cyclicality. Active lender mapping and bespoke financing structures sustain deal execution.

Equity market valuations and IPO window

Public market multiples, e.g., S&P 500 forward P/E ~17.0 as of July 2025 (Bloomberg), set reference prices for M&A and carve-outs. A recovering IPO window in H1 2025 after the 2022–23 slump enables dual-track processes and valuation tension. Evercore can optimize timing between public and private routes, using volatility hedges and go-to-market readiness to accelerate captures when windows open.

Private capital dry powder and fundraising cycles

Global private capital dry powder stood near $3.2 trillion as of mid-2024, with PE and infrastructure funds’ undeployed capital underwriting elevated buy-side demand. Slower exits—exit value down roughly 40% in 2023 versus prior peaks—have pressured DPI and pacing, changing sponsor behavior toward liquidity solutions. Evercore can structure continuation vehicles and GP-led deals, offering tailored capital to bridge valuation gaps and meet sponsor liquidity needs.

Macroeconomic growth and sector rotation

Currency movements and cross-border arbitrage

FX swings create relative value that drives cross-border bids; the US dollar's ~4% trade-weighted rise in 2024 heightened arbitrage opportunities and raised hedging costs, while translation risk alters pro formas and financing structures. Evercore can embed FX strategies in acquisition finance to reduce forward-cost exposure and use currency-aware comparables to sharpen negotiation leverage.

- FX volatility: +4% DXY (2024)

- Hedging impact: higher forward spreads

- Deal strategy: embedded FX in financing

- Valuation: currency-aware comps

Geopolitics and 60+ FDI screens reshape M&A: policy cash flows, longer regulatory timelines

With policy rates ~5.25–5.50% in mid-2025, higher discount rates compress debt capacity and LBO returns. S&P 500 forward P/E ~17.0 (Jul 2025) and a recovering IPO window shape exit timing. Global private capital dry powder ~$3.2T (mid-2024) sustains buy-side demand while GDP 2024 ~3.1% (US ~2.6%) shifts sector focus; DXY +4% (2024) raises hedging costs.

| Metric | Value |

|---|---|

| Policy rate | 5.25–5.50% (mid-2025) |

| S&P 500 fwd P/E | ~17.0 (Jul 2025) |

| Dry powder | ~$3.2T (mid-2024) |

| GDP 2024 | ~3.1% (US ~2.6%) |

| DXY | +4% (2024) |

Preview Before You Purchase

Evercore PESTLE Analysis

The Evercore PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This snapshot reflects the final content, layout, and depth of analysis without placeholders or edits. After checkout you’ll instantly download this same complete file.