EVERTEC Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

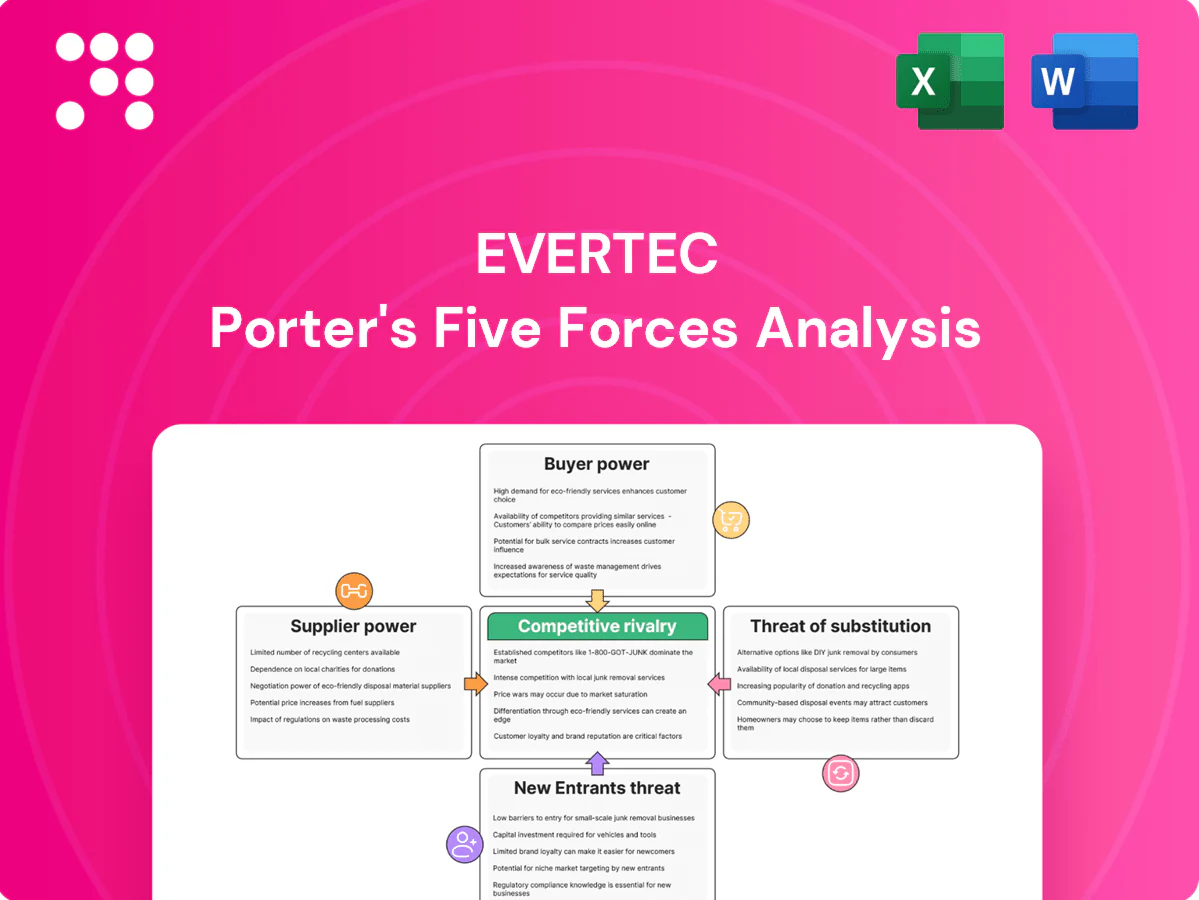

EVERTEC operates in a fast-evolving payments and fintech ecosystem where supplier leverage, buyer bargaining, and intense rivalry shape margins and growth prospects. Threats from entrants and substitutes—especially digital disruptors—add pressure to innovation and pricing. Strategic positioning, scale, and regulatory navigation are key to sustaining advantage. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis for detailed, actionable insights.

Suppliers Bargaining Power

Card networks set rails

EVOTEC depends on Visa, Mastercard and regional schemes like ATH, with Visa+Mastercard controlling roughly 80% of global card volume, so scheme rules, fees and certifications directly affect processing costs. Fee increases typically flow through costs and can compress margins if not fully passed to merchants. Network mandates force roadmap priorities and incremental compliance spend, while few viable alternative rails heighten supplier leverage.

Tech vendors are sticky

Core processing, fraud engines and POS firmware come from specialized vendors, and enterprise core replacements routinely take 12–24 months and can cost tens of millions, giving suppliers clear pricing power. Evergreen licensing and deep integrations create strong lock-in—vendor retention rates in payments tech often exceed 90%. Volume discounts mitigate costs but dependency and migration risk keep bargaining power with suppliers.

Telecom and data center reliance

Resilient payments require carrier diversity and Tier III data centers to ensure redundancy and uptime; in island markets where carriers are concentrated, limited options can push wholesale prices higher and restrict failover paths. Carrier outages or SLA breaches directly harm EVERTEC’s service levels and trigger contractual penalties and customer churn. Multi-homing and multiple data-center contracts reduce supplier power but do not fully eliminate it due to last-mile and optical-fiber bottlenecks.

Bank sponsorship and BINs

Issuer sponsorship, BIN sponsorship and settlement banking are critical supplier levers for EVERTEC; bank sponsors can negotiate economics, impose reserves and compliance requirements, and slow replacements due to licensing and risk reviews, giving financial institution partners meaningful bargaining power.

- Issuer sponsorship: bank controls go-to-market

- BIN sponsorship: access and fee leverage

- Settlement banking: reserve/compliance demands

- Switching: lengthy licensing and risk checks

Regulatory and compliance suppliers

Compliance stacks for EVERTEC hinge on KYC/AML data, sanctions screening and PCI services, making vendor reliability critical; regulatory updates in 2024 drove recurring vendor spend and external audits that squeeze margins. Few credible providers in smaller Latin American and Caribbean markets raise supplier dependency, and compliance timing often dictates EVERTEC’s product launch cadence.

- Dependency: KYC/AML, sanctions, PCI

- Risk: vendor concentration in smaller markets

- Impact: regulatory updates → vendor spend/audits

- Timing: compliance schedules set product cadence

Card-scheme concentration and vendor lock-in drive supplier bargaining power; compliance spend up

EVERTEC relies on Visa/Mastercard (~80% card volume) and a few specialized vendors, so scheme fees, certifications and processing suppliers exert high bargaining power. Vendor lock-in (vendor retention >90%) and 12–24 month core replacements raise switching costs. Carrier/datacenter concentration in island markets and bank sponsors (BIN/settlement) add leverage; 2024 regulatory updates lifted compliance vendor spend.

| Metric | Value |

|---|---|

| Visa+Mastercard share | ~80% |

| Vendor retention | >90% |

| Core replacement | 12–24 months |

| 2024 effect | Compliance vendor spend ↑ |

What is included in the product

Tailored Porter’s Five Forces analysis for EVERTEC that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats with strategic insights for investors and managers.

A clear, one-sheet summary of EVERTEC's Five Forces—perfect for rapid strategic decisions in payments and merchant services. Customize pressure levels and swap in your own data to reflect evolving regulation, fintech entrants, or shifting merchant dynamics.

Customers Bargaining Power

Concentrated anchor clients

Banks, large retailers and government agencies exert strong leverage over EVERTEC, with anchor customers in Puerto Rico and select LATAM niches often representing over 40% of processed TPV, allowing aggressive negotiation on fees. Competitive RFP cycles (annual or multi‑year) compress pricing and tighten SLA demands, forcing margin tradeoffs. Losing a single anchor can cut utilization rates sharply and erode operating margins.

High switching costs, but not absolute

Deep integrations, certifications, and custom reporting make switching from EVERTEC painful for customers, preserving bargaining power despite cost sensitivity. Modern RESTful APIs and vendor migration playbooks in 2024 materially lower friction versus legacy eras, shortening onboarding timelines. Buyers weigh disruption risk against potential fee savings and features, while multi-processor routing options amplify buyer leverage.

Price sensitivity in acquiring

Merchant acquiring is commoditizing on MDR and fixed fees, with large retailers in 2024 pushing for 10–25% blended-rate cuts and interchange++ transparency to shave costs. Faster settlement terms (T+0 to T+1) are increasingly requested, forcing acquirers to trade cash float for lower fees. Value-added services must demonstrably raise ROI to command premiums; volume rebates and bundling concessions of up to 20% are now common.

Service reliability demands

Buyers enforce strict SLAs—commonly 99.99% uptime and sub-100ms authorization latency in 2024—tying penalties and chargeback KPIs to financial remedies; outages shift bargaining power to buyers due to reputational loss and lost transactions. Custom SLAs and dedicated support teams raise EVERTEC’s operating cost, so differentiating on demonstrable reliability metrics is essential to mitigate price pressure.

- 99.99% uptime

- sub-100ms latency

- penalty-backed chargeback KPIs

- custom SLA cost impact

Alternative channels available

Anchors >40% TPV squeeze fees; merchants push 10–25% MDR cuts

Banks, large retailers and government clients exert high leverage over EVERTEC—anchors can represent >40% TPV, driving fee pressure and tight SLAs. Switching costs from integrations preserve some pricing power, but 2024 APIs and PSPs cut friction and increase buyer bargaining. Merchants push 10–25% MDR cuts; buyers demand 99.99% uptime and sub-100ms auth latency.

| Buyer | Leverage | 2024 Metric |

|---|---|---|

| Anchors | High | >40% TPV |

| Merchants | Growing | 10–25% MDR cuts |

| Card Schemes | Dominant | Visa/MC >80% |

Full Version Awaits

EVERTEC Porter's Five Forces Analysis

This preview shows the exact EVERTEC Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical file.

A Must-Have Tool for Decision-Makers

EVERTEC operates in a fast-evolving payments and fintech ecosystem where supplier leverage, buyer bargaining, and intense rivalry shape margins and growth prospects. Threats from entrants and substitutes—especially digital disruptors—add pressure to innovation and pricing. Strategic positioning, scale, and regulatory navigation are key to sustaining advantage. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis for detailed, actionable insights.

Suppliers Bargaining Power

Card networks set rails

EVOTEC depends on Visa, Mastercard and regional schemes like ATH, with Visa+Mastercard controlling roughly 80% of global card volume, so scheme rules, fees and certifications directly affect processing costs. Fee increases typically flow through costs and can compress margins if not fully passed to merchants. Network mandates force roadmap priorities and incremental compliance spend, while few viable alternative rails heighten supplier leverage.

Tech vendors are sticky

Core processing, fraud engines and POS firmware come from specialized vendors, and enterprise core replacements routinely take 12–24 months and can cost tens of millions, giving suppliers clear pricing power. Evergreen licensing and deep integrations create strong lock-in—vendor retention rates in payments tech often exceed 90%. Volume discounts mitigate costs but dependency and migration risk keep bargaining power with suppliers.

Telecom and data center reliance

Resilient payments require carrier diversity and Tier III data centers to ensure redundancy and uptime; in island markets where carriers are concentrated, limited options can push wholesale prices higher and restrict failover paths. Carrier outages or SLA breaches directly harm EVERTEC’s service levels and trigger contractual penalties and customer churn. Multi-homing and multiple data-center contracts reduce supplier power but do not fully eliminate it due to last-mile and optical-fiber bottlenecks.

Bank sponsorship and BINs

Issuer sponsorship, BIN sponsorship and settlement banking are critical supplier levers for EVERTEC; bank sponsors can negotiate economics, impose reserves and compliance requirements, and slow replacements due to licensing and risk reviews, giving financial institution partners meaningful bargaining power.

- Issuer sponsorship: bank controls go-to-market

- BIN sponsorship: access and fee leverage

- Settlement banking: reserve/compliance demands

- Switching: lengthy licensing and risk checks

Regulatory and compliance suppliers

Compliance stacks for EVERTEC hinge on KYC/AML data, sanctions screening and PCI services, making vendor reliability critical; regulatory updates in 2024 drove recurring vendor spend and external audits that squeeze margins. Few credible providers in smaller Latin American and Caribbean markets raise supplier dependency, and compliance timing often dictates EVERTEC’s product launch cadence.

- Dependency: KYC/AML, sanctions, PCI

- Risk: vendor concentration in smaller markets

- Impact: regulatory updates → vendor spend/audits

- Timing: compliance schedules set product cadence

Card-scheme concentration and vendor lock-in drive supplier bargaining power; compliance spend up

EVERTEC relies on Visa/Mastercard (~80% card volume) and a few specialized vendors, so scheme fees, certifications and processing suppliers exert high bargaining power. Vendor lock-in (vendor retention >90%) and 12–24 month core replacements raise switching costs. Carrier/datacenter concentration in island markets and bank sponsors (BIN/settlement) add leverage; 2024 regulatory updates lifted compliance vendor spend.

| Metric | Value |

|---|---|

| Visa+Mastercard share | ~80% |

| Vendor retention | >90% |

| Core replacement | 12–24 months |

| 2024 effect | Compliance vendor spend ↑ |

What is included in the product

Tailored Porter’s Five Forces analysis for EVERTEC that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats with strategic insights for investors and managers.

A clear, one-sheet summary of EVERTEC's Five Forces—perfect for rapid strategic decisions in payments and merchant services. Customize pressure levels and swap in your own data to reflect evolving regulation, fintech entrants, or shifting merchant dynamics.

Customers Bargaining Power

Concentrated anchor clients

Banks, large retailers and government agencies exert strong leverage over EVERTEC, with anchor customers in Puerto Rico and select LATAM niches often representing over 40% of processed TPV, allowing aggressive negotiation on fees. Competitive RFP cycles (annual or multi‑year) compress pricing and tighten SLA demands, forcing margin tradeoffs. Losing a single anchor can cut utilization rates sharply and erode operating margins.

High switching costs, but not absolute

Deep integrations, certifications, and custom reporting make switching from EVERTEC painful for customers, preserving bargaining power despite cost sensitivity. Modern RESTful APIs and vendor migration playbooks in 2024 materially lower friction versus legacy eras, shortening onboarding timelines. Buyers weigh disruption risk against potential fee savings and features, while multi-processor routing options amplify buyer leverage.

Price sensitivity in acquiring

Merchant acquiring is commoditizing on MDR and fixed fees, with large retailers in 2024 pushing for 10–25% blended-rate cuts and interchange++ transparency to shave costs. Faster settlement terms (T+0 to T+1) are increasingly requested, forcing acquirers to trade cash float for lower fees. Value-added services must demonstrably raise ROI to command premiums; volume rebates and bundling concessions of up to 20% are now common.

Service reliability demands

Buyers enforce strict SLAs—commonly 99.99% uptime and sub-100ms authorization latency in 2024—tying penalties and chargeback KPIs to financial remedies; outages shift bargaining power to buyers due to reputational loss and lost transactions. Custom SLAs and dedicated support teams raise EVERTEC’s operating cost, so differentiating on demonstrable reliability metrics is essential to mitigate price pressure.

- 99.99% uptime

- sub-100ms latency

- penalty-backed chargeback KPIs

- custom SLA cost impact

Alternative channels available

Anchors >40% TPV squeeze fees; merchants push 10–25% MDR cuts

Banks, large retailers and government clients exert high leverage over EVERTEC—anchors can represent >40% TPV, driving fee pressure and tight SLAs. Switching costs from integrations preserve some pricing power, but 2024 APIs and PSPs cut friction and increase buyer bargaining. Merchants push 10–25% MDR cuts; buyers demand 99.99% uptime and sub-100ms auth latency.

| Buyer | Leverage | 2024 Metric |

|---|---|---|

| Anchors | High | >40% TPV |

| Merchants | Growing | 10–25% MDR cuts |

| Card Schemes | Dominant | Visa/MC >80% |

Full Version Awaits

EVERTEC Porter's Five Forces Analysis

This preview shows the exact EVERTEC Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical file.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

EVERTEC operates in a fast-evolving payments and fintech ecosystem where supplier leverage, buyer bargaining, and intense rivalry shape margins and growth prospects. Threats from entrants and substitutes—especially digital disruptors—add pressure to innovation and pricing. Strategic positioning, scale, and regulatory navigation are key to sustaining advantage. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis for detailed, actionable insights.

Suppliers Bargaining Power

Card networks set rails

EVOTEC depends on Visa, Mastercard and regional schemes like ATH, with Visa+Mastercard controlling roughly 80% of global card volume, so scheme rules, fees and certifications directly affect processing costs. Fee increases typically flow through costs and can compress margins if not fully passed to merchants. Network mandates force roadmap priorities and incremental compliance spend, while few viable alternative rails heighten supplier leverage.

Tech vendors are sticky

Core processing, fraud engines and POS firmware come from specialized vendors, and enterprise core replacements routinely take 12–24 months and can cost tens of millions, giving suppliers clear pricing power. Evergreen licensing and deep integrations create strong lock-in—vendor retention rates in payments tech often exceed 90%. Volume discounts mitigate costs but dependency and migration risk keep bargaining power with suppliers.

Telecom and data center reliance

Resilient payments require carrier diversity and Tier III data centers to ensure redundancy and uptime; in island markets where carriers are concentrated, limited options can push wholesale prices higher and restrict failover paths. Carrier outages or SLA breaches directly harm EVERTEC’s service levels and trigger contractual penalties and customer churn. Multi-homing and multiple data-center contracts reduce supplier power but do not fully eliminate it due to last-mile and optical-fiber bottlenecks.

Bank sponsorship and BINs

Issuer sponsorship, BIN sponsorship and settlement banking are critical supplier levers for EVERTEC; bank sponsors can negotiate economics, impose reserves and compliance requirements, and slow replacements due to licensing and risk reviews, giving financial institution partners meaningful bargaining power.

- Issuer sponsorship: bank controls go-to-market

- BIN sponsorship: access and fee leverage

- Settlement banking: reserve/compliance demands

- Switching: lengthy licensing and risk checks

Regulatory and compliance suppliers

Compliance stacks for EVERTEC hinge on KYC/AML data, sanctions screening and PCI services, making vendor reliability critical; regulatory updates in 2024 drove recurring vendor spend and external audits that squeeze margins. Few credible providers in smaller Latin American and Caribbean markets raise supplier dependency, and compliance timing often dictates EVERTEC’s product launch cadence.

- Dependency: KYC/AML, sanctions, PCI

- Risk: vendor concentration in smaller markets

- Impact: regulatory updates → vendor spend/audits

- Timing: compliance schedules set product cadence

Card-scheme concentration and vendor lock-in drive supplier bargaining power; compliance spend up

EVERTEC relies on Visa/Mastercard (~80% card volume) and a few specialized vendors, so scheme fees, certifications and processing suppliers exert high bargaining power. Vendor lock-in (vendor retention >90%) and 12–24 month core replacements raise switching costs. Carrier/datacenter concentration in island markets and bank sponsors (BIN/settlement) add leverage; 2024 regulatory updates lifted compliance vendor spend.

| Metric | Value |

|---|---|

| Visa+Mastercard share | ~80% |

| Vendor retention | >90% |

| Core replacement | 12–24 months |

| 2024 effect | Compliance vendor spend ↑ |

What is included in the product

Tailored Porter’s Five Forces analysis for EVERTEC that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats with strategic insights for investors and managers.

A clear, one-sheet summary of EVERTEC's Five Forces—perfect for rapid strategic decisions in payments and merchant services. Customize pressure levels and swap in your own data to reflect evolving regulation, fintech entrants, or shifting merchant dynamics.

Customers Bargaining Power

Concentrated anchor clients

Banks, large retailers and government agencies exert strong leverage over EVERTEC, with anchor customers in Puerto Rico and select LATAM niches often representing over 40% of processed TPV, allowing aggressive negotiation on fees. Competitive RFP cycles (annual or multi‑year) compress pricing and tighten SLA demands, forcing margin tradeoffs. Losing a single anchor can cut utilization rates sharply and erode operating margins.

High switching costs, but not absolute

Deep integrations, certifications, and custom reporting make switching from EVERTEC painful for customers, preserving bargaining power despite cost sensitivity. Modern RESTful APIs and vendor migration playbooks in 2024 materially lower friction versus legacy eras, shortening onboarding timelines. Buyers weigh disruption risk against potential fee savings and features, while multi-processor routing options amplify buyer leverage.

Price sensitivity in acquiring

Merchant acquiring is commoditizing on MDR and fixed fees, with large retailers in 2024 pushing for 10–25% blended-rate cuts and interchange++ transparency to shave costs. Faster settlement terms (T+0 to T+1) are increasingly requested, forcing acquirers to trade cash float for lower fees. Value-added services must demonstrably raise ROI to command premiums; volume rebates and bundling concessions of up to 20% are now common.

Service reliability demands

Buyers enforce strict SLAs—commonly 99.99% uptime and sub-100ms authorization latency in 2024—tying penalties and chargeback KPIs to financial remedies; outages shift bargaining power to buyers due to reputational loss and lost transactions. Custom SLAs and dedicated support teams raise EVERTEC’s operating cost, so differentiating on demonstrable reliability metrics is essential to mitigate price pressure.

- 99.99% uptime

- sub-100ms latency

- penalty-backed chargeback KPIs

- custom SLA cost impact

Alternative channels available

Anchors >40% TPV squeeze fees; merchants push 10–25% MDR cuts

Banks, large retailers and government clients exert high leverage over EVERTEC—anchors can represent >40% TPV, driving fee pressure and tight SLAs. Switching costs from integrations preserve some pricing power, but 2024 APIs and PSPs cut friction and increase buyer bargaining. Merchants push 10–25% MDR cuts; buyers demand 99.99% uptime and sub-100ms auth latency.

| Buyer | Leverage | 2024 Metric |

|---|---|---|

| Anchors | High | >40% TPV |

| Merchants | Growing | 10–25% MDR cuts |

| Card Schemes | Dominant | Visa/MC >80% |

Full Version Awaits

EVERTEC Porter's Five Forces Analysis

This preview shows the exact EVERTEC Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical file.