Evraz Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

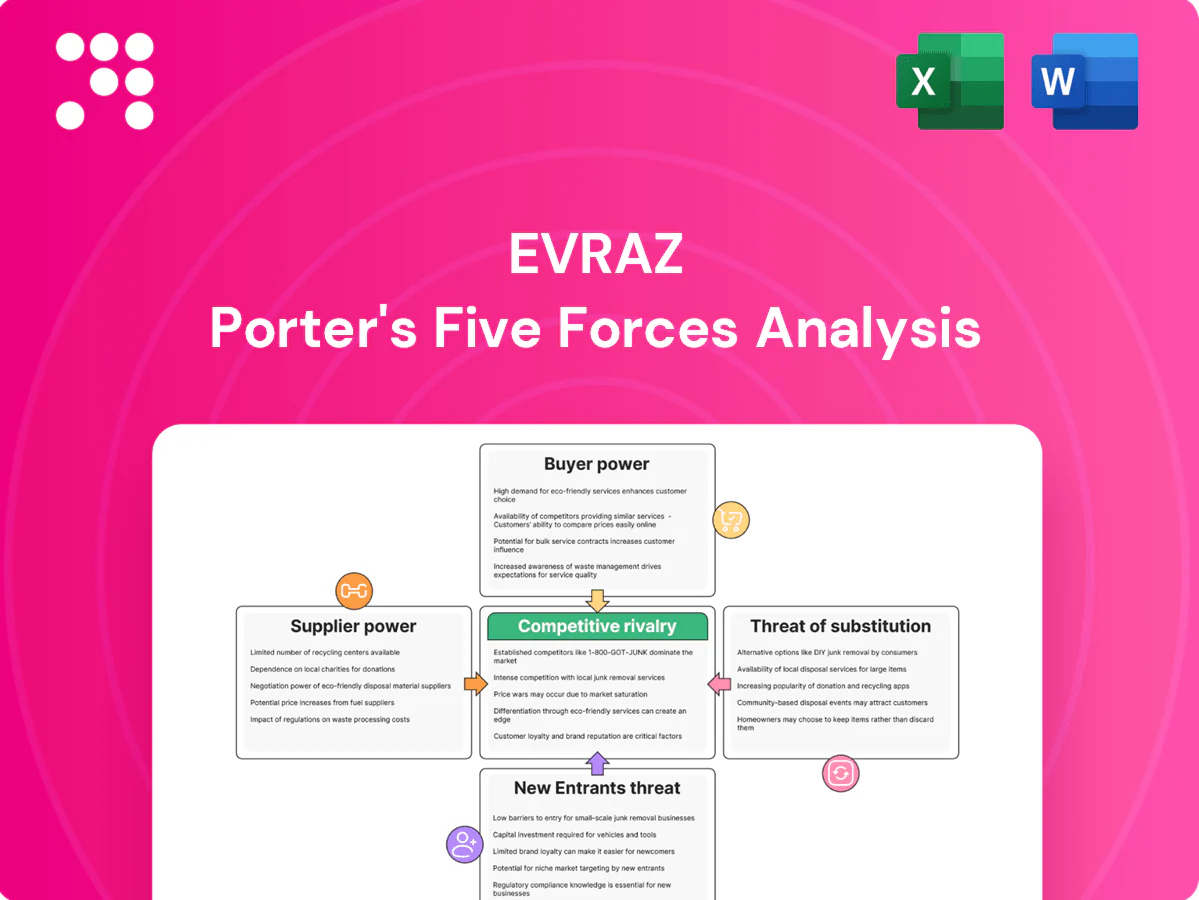

Evraz faces intense competitive rivalry in steel and mining, moderated by scale advantages, vertical integration and exposure to commodity cycles; supplier bargaining and downstream buyer power shape margins, while substitute materials and regulatory shifts create strategic risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Evraz’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical integration dampens input leverage

EVRAZ vertically integrates upstream by owning major iron ore and coking coal assets in Russia and Kazakhstan, which reduces reliance on third-party raw materials and lowers exposure to input price volatility. This integration materially weakens external suppliers’ bargaining power for bulk inputs. Outsourced specialty items — alloys, refractories, electrodes, critical spares and equipment — remain significant cost drivers. Disruptions or concentration among those suppliers can create localized pockets of supplier leverage.

Concentrated specialty input vendors

Graphite electrodes, ferroalloys and advanced refractories are often sourced from a limited supplier pool, with the top five graphite electrode producers supplying roughly 65% of global capacity in 2024. High technical specs and multi-month qualification cycles restrict switching, while concentration lifts prices and lead times—graphite electrode lead times were commonly 6–9 months in 2024. Long-term contracts mitigate but do not eliminate supply, price or timing risk.

Capital equipment and maintenance OEM power

Blast furnace, EAF, rolling mill and mining equipment OEMs exert strong leverage over Evraz via proprietary parts and service, with the global crude steel industry producing ~1.88 billion tonnes in 2023 (World Steel Association) amplifying uptime value. Switching costs are high because of compatibility and performance risks. Scheduled overhauls become bottlenecks if OEM slots are scarce. Framework agreements can trade lower unit cost for guaranteed availability.

Logistics and energy dependencies

Logistics and energy suppliers significantly influence EVRAZ’s delivered costs and uptime: rail and port access, often controlled by regional monopolies like Russian Railways, create pricing and capacity bottlenecks that raise freight costs and delay shipments.

Energy price volatility — notably gas and electricity swings since 2022— directly alters smelting and rolling margins, increasing operating cost sensitivity in primary steelmaking.

EVRAZ’s operations across Russia, North America and Kazakhstan provide geographic hedging against localized logistics or energy shocks but do not fully insulate group margins from coordinated supply or price disruptions.

- rail concentration: regional monopolies limit alternatives

- port constraints: terminal capacity tightens delivery windows

- energy swings: fuel/electricity volatility compresses smelting margins

- multi-region: partial hedging, not full protection

Geopolitical and sanctions-driven frictions

Geopolitical and sanctions-driven frictions restrict Evrazs access to Western technology, spare parts, and international financing, forcing reliance on a narrower set of non-Western suppliers and raising procurement costs and capital expenses.

Parallel supply chains create longer lead times and logistical complexity, while limited regulatory alternatives amplify supplier bargaining power, enabling higher prices and stricter terms.

- Supply concentration: increased dependence on fewer vendors

- Cost pressure: higher CAPEX and OPEX from restricted access

- Delay risk: parallel chains extend lead times

- Regulatory lock-in: scarce alternatives boost supplier leverage

Upstream integration trims bulk-supplier power; electrodes, sanctions tighten CAPEX and lead times

EVRAZ’s upstream integration (iron ore, coking coal) sharply reduces bulk-input supplier power, but specialty inputs, OEM parts, logistics and energy retain leverage. Graphite electrodes/top‑5 ~65% global capacity (2024) with 6–9 month lead times; global crude steel ~1.88bn t (2023) raises OEM service value. Sanctions concentrate non‑Western suppliers, raising CAPEX/OPEX and lead times.

| Category | Key 2023/24 figure |

|---|---|

| Graphite electrodes share | ~65% (top 5, 2024) |

| Electrode lead times | 6–9 months (2024) |

| Global crude steel | ~1.88bn t (2023) |

What is included in the product

Tailored Porter's Five Forces analysis for Evraz that uncovers competitive intensity, supplier and buyer bargaining power, threat of new entrants and substitutes, and identifies disruptive forces and market barriers shaping its profitability and strategic positioning.

Concise one-sheet Porter's Five Forces for Evraz—instantly reveal supplier, buyer, entrant, substitute and rivalry pressures to prioritize tactical responses and de-risk capital, pricing and expansion decisions.

Customers Bargaining Power

Diverse end-markets with price sensitivity

Construction, rail, oil and gas and industrial users show cyclical 2024 demand and strong price sensitivity, driving bargaining power. Commodity-grade steel buyers can readily switch across producers, compressing margins. EVRAZ’s rails and tubular products provide some differentiation and higher conversion pricing. Spot buyers nonetheless negotiated aggressively in 2024 downturns, pressuring volumes and realized prices.

Large contract customers wield scale

Pipeline operators, railways and OEMs buy in high volumes on multi-year terms (typically 3–5 years), giving them leverage to demand tougher pricing, quality and delivery clauses; performance penalties and competitive bidding further compress supplier margins. Approved-vendor status creates customer stickiness, but suppliers like Evraz face tight margins and frequent rebids that erode pricing power.

Substitution and import options for buyers

Buyers can pivot among domestic and international mills, but tariffs, route closures and higher freight costs constrain options and raise effective switching costs for Evraz clients. When trade routes reopen, competition broadens and buyer power rises as import alternatives appear. Certifications and standards (approval cycles commonly 6–12 months) limit instant switching but not over time. Currency swings frequently tilt sourcing preferences.

Service, lead-time, and reliability expectations

Service, short lead-times, consistent specs, and technical support drive customer leverage in Evraz's markets; missed deliveries or quality issues typically trigger retendering and contract reviews, while value-added services like processing and just-in-time logistics shift negotiations away from price alone.

- Short lead times

- Consistent specs

- Technical support

- On-time performance reduces leverage

- Value-added services temper price pressure

Regional segmentation moderates leverage

Regional segmentation moderates customer leverage: in Russia and Kazakhstan EVRAZ benefits from proximity to the 85,500 km Russian and ~16,000 km Kazakh rail networks, where rail products and logistics anchor long-term relationships and reduce buyer bargaining power. In North America Buy America rules (55% domestic content) and higher transport costs increase local sourcing, shifting leverage to regional suppliers. These dynamics split bargaining profiles and let EVRAZ balance contract mix across cycles.

- Russia/Kazakhstan: proximity + rail network scale reduces buyer power

- North America: 55% Buy America domestic-content rule increases local preference

- Result: differentiated bargaining power by region enables portfolio balancing

Buyers squeeze margins spot pricing, 3-5 yrs, 55% local

Customers show high price sensitivity in 2024 with spot-driven negotiations and cyclical demand, compressing margins despite EVRAZ’s differentiated rail and tubular products. Large buyers use 3–5 year contracts and competitive bidding to extract tougher terms; approvals (6–12 months) limit instant switching but not over time. Regional factors—Russia/Kazakhstan proximity vs North America Buy America 55%—create asymmetric buyer power.

| Metric | Impact | Value |

|---|---|---|

| Contract length | Buyer leverage | 3–5 years |

| Approval cycle | Switching delay | 6–12 months |

| Buy America | Local preference | 55% |

| Rail network | Proximity advantage | Russia 85,500 km; KZ ~16,000 km |

Same Document Delivered

Evraz Porter's Five Forces Analysis

This preview shows the exact Evraz Porter’s Five Forces analysis you’ll receive after purchase—fully written, formatted, and ready to download. It’s not a sample or excerpt; this is the final deliverable. Instant access is provided upon payment with no placeholders or further setup required.

A Must-Have Tool for Decision-Makers

Evraz faces intense competitive rivalry in steel and mining, moderated by scale advantages, vertical integration and exposure to commodity cycles; supplier bargaining and downstream buyer power shape margins, while substitute materials and regulatory shifts create strategic risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Evraz’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical integration dampens input leverage

EVRAZ vertically integrates upstream by owning major iron ore and coking coal assets in Russia and Kazakhstan, which reduces reliance on third-party raw materials and lowers exposure to input price volatility. This integration materially weakens external suppliers’ bargaining power for bulk inputs. Outsourced specialty items — alloys, refractories, electrodes, critical spares and equipment — remain significant cost drivers. Disruptions or concentration among those suppliers can create localized pockets of supplier leverage.

Concentrated specialty input vendors

Graphite electrodes, ferroalloys and advanced refractories are often sourced from a limited supplier pool, with the top five graphite electrode producers supplying roughly 65% of global capacity in 2024. High technical specs and multi-month qualification cycles restrict switching, while concentration lifts prices and lead times—graphite electrode lead times were commonly 6–9 months in 2024. Long-term contracts mitigate but do not eliminate supply, price or timing risk.

Capital equipment and maintenance OEM power

Blast furnace, EAF, rolling mill and mining equipment OEMs exert strong leverage over Evraz via proprietary parts and service, with the global crude steel industry producing ~1.88 billion tonnes in 2023 (World Steel Association) amplifying uptime value. Switching costs are high because of compatibility and performance risks. Scheduled overhauls become bottlenecks if OEM slots are scarce. Framework agreements can trade lower unit cost for guaranteed availability.

Logistics and energy dependencies

Logistics and energy suppliers significantly influence EVRAZ’s delivered costs and uptime: rail and port access, often controlled by regional monopolies like Russian Railways, create pricing and capacity bottlenecks that raise freight costs and delay shipments.

Energy price volatility — notably gas and electricity swings since 2022— directly alters smelting and rolling margins, increasing operating cost sensitivity in primary steelmaking.

EVRAZ’s operations across Russia, North America and Kazakhstan provide geographic hedging against localized logistics or energy shocks but do not fully insulate group margins from coordinated supply or price disruptions.

- rail concentration: regional monopolies limit alternatives

- port constraints: terminal capacity tightens delivery windows

- energy swings: fuel/electricity volatility compresses smelting margins

- multi-region: partial hedging, not full protection

Geopolitical and sanctions-driven frictions

Geopolitical and sanctions-driven frictions restrict Evrazs access to Western technology, spare parts, and international financing, forcing reliance on a narrower set of non-Western suppliers and raising procurement costs and capital expenses.

Parallel supply chains create longer lead times and logistical complexity, while limited regulatory alternatives amplify supplier bargaining power, enabling higher prices and stricter terms.

- Supply concentration: increased dependence on fewer vendors

- Cost pressure: higher CAPEX and OPEX from restricted access

- Delay risk: parallel chains extend lead times

- Regulatory lock-in: scarce alternatives boost supplier leverage

Upstream integration trims bulk-supplier power; electrodes, sanctions tighten CAPEX and lead times

EVRAZ’s upstream integration (iron ore, coking coal) sharply reduces bulk-input supplier power, but specialty inputs, OEM parts, logistics and energy retain leverage. Graphite electrodes/top‑5 ~65% global capacity (2024) with 6–9 month lead times; global crude steel ~1.88bn t (2023) raises OEM service value. Sanctions concentrate non‑Western suppliers, raising CAPEX/OPEX and lead times.

| Category | Key 2023/24 figure |

|---|---|

| Graphite electrodes share | ~65% (top 5, 2024) |

| Electrode lead times | 6–9 months (2024) |

| Global crude steel | ~1.88bn t (2023) |

What is included in the product

Tailored Porter's Five Forces analysis for Evraz that uncovers competitive intensity, supplier and buyer bargaining power, threat of new entrants and substitutes, and identifies disruptive forces and market barriers shaping its profitability and strategic positioning.

Concise one-sheet Porter's Five Forces for Evraz—instantly reveal supplier, buyer, entrant, substitute and rivalry pressures to prioritize tactical responses and de-risk capital, pricing and expansion decisions.

Customers Bargaining Power

Diverse end-markets with price sensitivity

Construction, rail, oil and gas and industrial users show cyclical 2024 demand and strong price sensitivity, driving bargaining power. Commodity-grade steel buyers can readily switch across producers, compressing margins. EVRAZ’s rails and tubular products provide some differentiation and higher conversion pricing. Spot buyers nonetheless negotiated aggressively in 2024 downturns, pressuring volumes and realized prices.

Large contract customers wield scale

Pipeline operators, railways and OEMs buy in high volumes on multi-year terms (typically 3–5 years), giving them leverage to demand tougher pricing, quality and delivery clauses; performance penalties and competitive bidding further compress supplier margins. Approved-vendor status creates customer stickiness, but suppliers like Evraz face tight margins and frequent rebids that erode pricing power.

Substitution and import options for buyers

Buyers can pivot among domestic and international mills, but tariffs, route closures and higher freight costs constrain options and raise effective switching costs for Evraz clients. When trade routes reopen, competition broadens and buyer power rises as import alternatives appear. Certifications and standards (approval cycles commonly 6–12 months) limit instant switching but not over time. Currency swings frequently tilt sourcing preferences.

Service, lead-time, and reliability expectations

Service, short lead-times, consistent specs, and technical support drive customer leverage in Evraz's markets; missed deliveries or quality issues typically trigger retendering and contract reviews, while value-added services like processing and just-in-time logistics shift negotiations away from price alone.

- Short lead times

- Consistent specs

- Technical support

- On-time performance reduces leverage

- Value-added services temper price pressure

Regional segmentation moderates leverage

Regional segmentation moderates customer leverage: in Russia and Kazakhstan EVRAZ benefits from proximity to the 85,500 km Russian and ~16,000 km Kazakh rail networks, where rail products and logistics anchor long-term relationships and reduce buyer bargaining power. In North America Buy America rules (55% domestic content) and higher transport costs increase local sourcing, shifting leverage to regional suppliers. These dynamics split bargaining profiles and let EVRAZ balance contract mix across cycles.

- Russia/Kazakhstan: proximity + rail network scale reduces buyer power

- North America: 55% Buy America domestic-content rule increases local preference

- Result: differentiated bargaining power by region enables portfolio balancing

Buyers squeeze margins spot pricing, 3-5 yrs, 55% local

Customers show high price sensitivity in 2024 with spot-driven negotiations and cyclical demand, compressing margins despite EVRAZ’s differentiated rail and tubular products. Large buyers use 3–5 year contracts and competitive bidding to extract tougher terms; approvals (6–12 months) limit instant switching but not over time. Regional factors—Russia/Kazakhstan proximity vs North America Buy America 55%—create asymmetric buyer power.

| Metric | Impact | Value |

|---|---|---|

| Contract length | Buyer leverage | 3–5 years |

| Approval cycle | Switching delay | 6–12 months |

| Buy America | Local preference | 55% |

| Rail network | Proximity advantage | Russia 85,500 km; KZ ~16,000 km |

Same Document Delivered

Evraz Porter's Five Forces Analysis

This preview shows the exact Evraz Porter’s Five Forces analysis you’ll receive after purchase—fully written, formatted, and ready to download. It’s not a sample or excerpt; this is the final deliverable. Instant access is provided upon payment with no placeholders or further setup required.

Description

A Must-Have Tool for Decision-Makers

Evraz faces intense competitive rivalry in steel and mining, moderated by scale advantages, vertical integration and exposure to commodity cycles; supplier bargaining and downstream buyer power shape margins, while substitute materials and regulatory shifts create strategic risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Evraz’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical integration dampens input leverage

EVRAZ vertically integrates upstream by owning major iron ore and coking coal assets in Russia and Kazakhstan, which reduces reliance on third-party raw materials and lowers exposure to input price volatility. This integration materially weakens external suppliers’ bargaining power for bulk inputs. Outsourced specialty items — alloys, refractories, electrodes, critical spares and equipment — remain significant cost drivers. Disruptions or concentration among those suppliers can create localized pockets of supplier leverage.

Concentrated specialty input vendors

Graphite electrodes, ferroalloys and advanced refractories are often sourced from a limited supplier pool, with the top five graphite electrode producers supplying roughly 65% of global capacity in 2024. High technical specs and multi-month qualification cycles restrict switching, while concentration lifts prices and lead times—graphite electrode lead times were commonly 6–9 months in 2024. Long-term contracts mitigate but do not eliminate supply, price or timing risk.

Capital equipment and maintenance OEM power

Blast furnace, EAF, rolling mill and mining equipment OEMs exert strong leverage over Evraz via proprietary parts and service, with the global crude steel industry producing ~1.88 billion tonnes in 2023 (World Steel Association) amplifying uptime value. Switching costs are high because of compatibility and performance risks. Scheduled overhauls become bottlenecks if OEM slots are scarce. Framework agreements can trade lower unit cost for guaranteed availability.

Logistics and energy dependencies

Logistics and energy suppliers significantly influence EVRAZ’s delivered costs and uptime: rail and port access, often controlled by regional monopolies like Russian Railways, create pricing and capacity bottlenecks that raise freight costs and delay shipments.

Energy price volatility — notably gas and electricity swings since 2022— directly alters smelting and rolling margins, increasing operating cost sensitivity in primary steelmaking.

EVRAZ’s operations across Russia, North America and Kazakhstan provide geographic hedging against localized logistics or energy shocks but do not fully insulate group margins from coordinated supply or price disruptions.

- rail concentration: regional monopolies limit alternatives

- port constraints: terminal capacity tightens delivery windows

- energy swings: fuel/electricity volatility compresses smelting margins

- multi-region: partial hedging, not full protection

Geopolitical and sanctions-driven frictions

Geopolitical and sanctions-driven frictions restrict Evrazs access to Western technology, spare parts, and international financing, forcing reliance on a narrower set of non-Western suppliers and raising procurement costs and capital expenses.

Parallel supply chains create longer lead times and logistical complexity, while limited regulatory alternatives amplify supplier bargaining power, enabling higher prices and stricter terms.

- Supply concentration: increased dependence on fewer vendors

- Cost pressure: higher CAPEX and OPEX from restricted access

- Delay risk: parallel chains extend lead times

- Regulatory lock-in: scarce alternatives boost supplier leverage

Upstream integration trims bulk-supplier power; electrodes, sanctions tighten CAPEX and lead times

EVRAZ’s upstream integration (iron ore, coking coal) sharply reduces bulk-input supplier power, but specialty inputs, OEM parts, logistics and energy retain leverage. Graphite electrodes/top‑5 ~65% global capacity (2024) with 6–9 month lead times; global crude steel ~1.88bn t (2023) raises OEM service value. Sanctions concentrate non‑Western suppliers, raising CAPEX/OPEX and lead times.

| Category | Key 2023/24 figure |

|---|---|

| Graphite electrodes share | ~65% (top 5, 2024) |

| Electrode lead times | 6–9 months (2024) |

| Global crude steel | ~1.88bn t (2023) |

What is included in the product

Tailored Porter's Five Forces analysis for Evraz that uncovers competitive intensity, supplier and buyer bargaining power, threat of new entrants and substitutes, and identifies disruptive forces and market barriers shaping its profitability and strategic positioning.

Concise one-sheet Porter's Five Forces for Evraz—instantly reveal supplier, buyer, entrant, substitute and rivalry pressures to prioritize tactical responses and de-risk capital, pricing and expansion decisions.

Customers Bargaining Power

Diverse end-markets with price sensitivity

Construction, rail, oil and gas and industrial users show cyclical 2024 demand and strong price sensitivity, driving bargaining power. Commodity-grade steel buyers can readily switch across producers, compressing margins. EVRAZ’s rails and tubular products provide some differentiation and higher conversion pricing. Spot buyers nonetheless negotiated aggressively in 2024 downturns, pressuring volumes and realized prices.

Large contract customers wield scale

Pipeline operators, railways and OEMs buy in high volumes on multi-year terms (typically 3–5 years), giving them leverage to demand tougher pricing, quality and delivery clauses; performance penalties and competitive bidding further compress supplier margins. Approved-vendor status creates customer stickiness, but suppliers like Evraz face tight margins and frequent rebids that erode pricing power.

Substitution and import options for buyers

Buyers can pivot among domestic and international mills, but tariffs, route closures and higher freight costs constrain options and raise effective switching costs for Evraz clients. When trade routes reopen, competition broadens and buyer power rises as import alternatives appear. Certifications and standards (approval cycles commonly 6–12 months) limit instant switching but not over time. Currency swings frequently tilt sourcing preferences.

Service, lead-time, and reliability expectations

Service, short lead-times, consistent specs, and technical support drive customer leverage in Evraz's markets; missed deliveries or quality issues typically trigger retendering and contract reviews, while value-added services like processing and just-in-time logistics shift negotiations away from price alone.

- Short lead times

- Consistent specs

- Technical support

- On-time performance reduces leverage

- Value-added services temper price pressure

Regional segmentation moderates leverage

Regional segmentation moderates customer leverage: in Russia and Kazakhstan EVRAZ benefits from proximity to the 85,500 km Russian and ~16,000 km Kazakh rail networks, where rail products and logistics anchor long-term relationships and reduce buyer bargaining power. In North America Buy America rules (55% domestic content) and higher transport costs increase local sourcing, shifting leverage to regional suppliers. These dynamics split bargaining profiles and let EVRAZ balance contract mix across cycles.

- Russia/Kazakhstan: proximity + rail network scale reduces buyer power

- North America: 55% Buy America domestic-content rule increases local preference

- Result: differentiated bargaining power by region enables portfolio balancing

Buyers squeeze margins spot pricing, 3-5 yrs, 55% local

Customers show high price sensitivity in 2024 with spot-driven negotiations and cyclical demand, compressing margins despite EVRAZ’s differentiated rail and tubular products. Large buyers use 3–5 year contracts and competitive bidding to extract tougher terms; approvals (6–12 months) limit instant switching but not over time. Regional factors—Russia/Kazakhstan proximity vs North America Buy America 55%—create asymmetric buyer power.

| Metric | Impact | Value |

|---|---|---|

| Contract length | Buyer leverage | 3–5 years |

| Approval cycle | Switching delay | 6–12 months |

| Buy America | Local preference | 55% |

| Rail network | Proximity advantage | Russia 85,500 km; KZ ~16,000 km |

Same Document Delivered

Evraz Porter's Five Forces Analysis

This preview shows the exact Evraz Porter’s Five Forces analysis you’ll receive after purchase—fully written, formatted, and ready to download. It’s not a sample or excerpt; this is the final deliverable. Instant access is provided upon payment with no placeholders or further setup required.