Exact Sciences Porter's Five Forces Analysis

Don't Miss the Bigger Picture

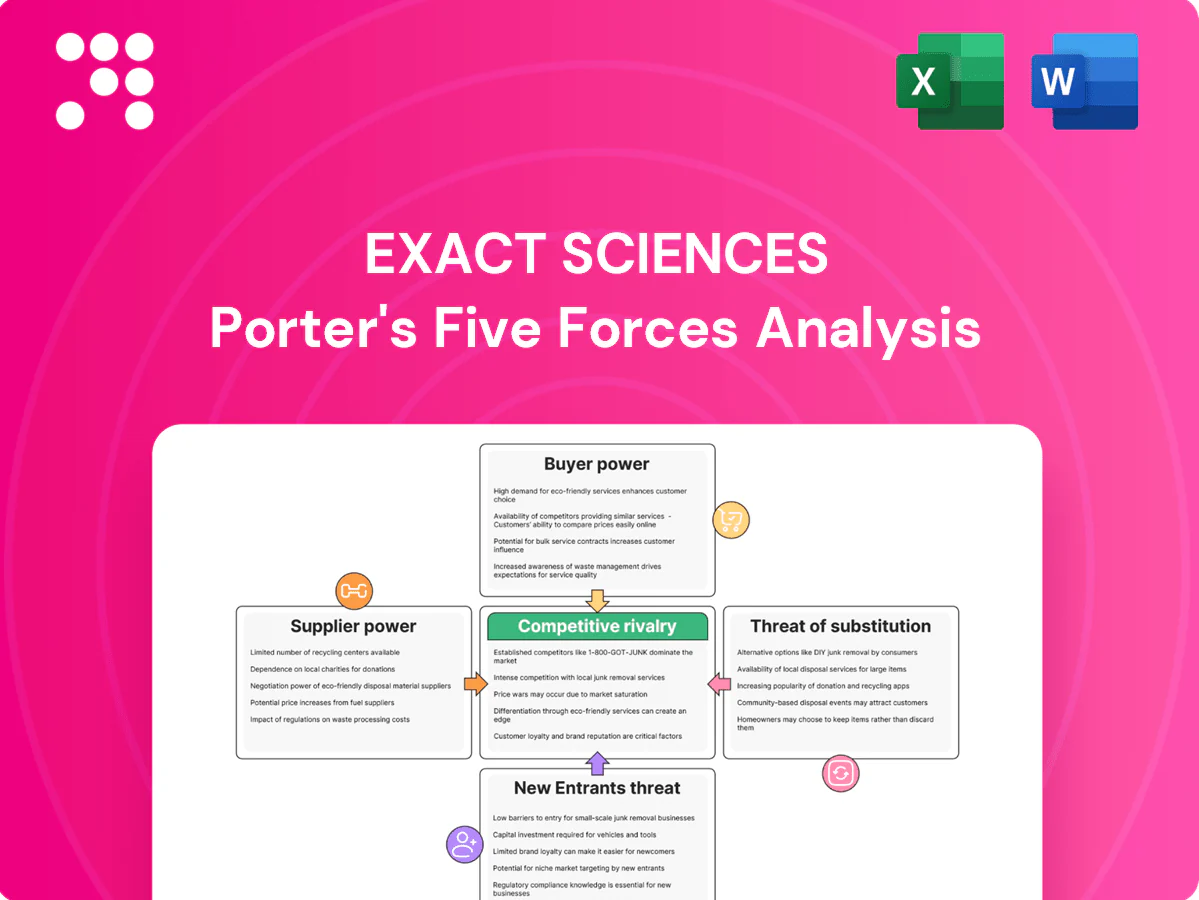

Exact Sciences faces moderating supplier power, intense rivalry in diagnostic screening, and growing threat from innovative substitutes and new entrants as it scales commercialization of liquid biopsy and CRC screening products. Regulatory and reimbursement pressures amplify buyer leverage and margin risks, while IP and clinical data remain key defenses. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Exact Sciences’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized reagents and consumables

Exact Sciences depends on specialized reagents, oligos, antibodies and collection kits validated for specific assays, and these inputs underpin its ~$3.3B 2024 revenue base, making supplier issues high-impact. Supplier switching is constrained by analytical validation and regulatory filings, giving suppliers moderate pricing and continuity leverage. Mitigants include dual-sourcing, long-term contracts and safety-stock policies to reduce disruption risk.

Proprietary biomarkers and IP licensing

Proprietary biomarkers, algorithms, and method patents, including licensed know-how from partners, give Exact Sciences concentrated supplier-like power over key assay inputs in 2024. Royalties and exclusivity terms in licensing deals can raise costs and limit operational flexibility. As patents expire or internal discovery expands, dependence on external IP can decline. Strategic partnerships secure rights and share development and commercialization risk.

Laboratory equipment and platform vendors

Automated extraction, PCR and NGS platforms and robotics vendors exert leverage through multi-year service contracts and periodic upgrade cycles; NGS sequencers range from about $100,000 to over $1 million, with service agreements commonly 10–15% of equipment cost annually. Qualification and validation often take 3–9 months, raising switching costs and delaying deployment. Volume commitments and cross-site standardization can secure 10–30% unit-cost reductions and lower downtime risk. Diversifying vendors mitigates single-supplier disruption and preserves operational continuity.

Logistics and cold-chain carriers

Logistics and cold-chain carriers for Exact Sciences are concentrated among national carriers (UPS, FedEx, USPS) as of 2024, creating leverage where service disruptions or fuel surcharges can delay time-sensitive biological samples and compress margins.

Negotiated SLAs, redundant routing and regional cold-chain partnerships reduce single-carrier exposure, and Exact Sciences scale in at-home collection provides counter-leverage in pricing and service terms.

- Carrier concentration: national carriers dominate sample transport

- Risk: service disruptions or fuel surcharges affect TAT and margins

- Mitigants: SLAs + redundant routing + regional partners

- Leverage: large at-home collection scale strengthens negotiation

Data infrastructure and software tools

Cloud, LIMS and bioinformatics vendors are critical to Exact Sciences operations and quality control; 92% of enterprises used multi-cloud in 2024 (Flexera), raising dependency and switching costs especially given average data breach costs of ~$4.45M (IBM 2024). Strong compliance needs elevate lock-in, but multi-cloud strategies and in-house tooling plus volume discounts (cloud commitment savings up to ~40%) and co-development deals reduce supplier power.

- 92% multi-cloud adoption (2024)

- Average breach cost ~$4.45M (2024)

- Cloud commitment discounts up to ~40%

- In-house tooling and co-dev lower lock-in

Supply Risk: $3.3B, High Switching Costs, 92% Multi-cloud

Exact depends on specialized reagents, kits and platforms; supplier disruption is high-impact given ~\$3.3B 2024 revenue. Switching costs are high from validation, patents and multi-year service contracts; NGS sequencers \$100k–\$1M with service ~10–15% annually. Mitigants include dual-sourcing, long-term contracts, SLAs, multi-cloud and scale in at-home collection reducing supplier leverage.

| Category | 2024 metric | Impact |

|---|---|---|

| Revenue exposure | \$3.3B | High |

| NGS equipment | \$100k–\$1M; service 10–15% | High |

| Cloud adoption | 92% multi-cloud | Moderate |

What is included in the product

Tailored Porter's Five Forces analysis for Exact Sciences uncovering competitive drivers, buyer and supplier power, substitutes, and new‑entry risks; evaluates how these forces shape pricing, profitability, and strategic positioning in oncology and diagnostics. Includes identification of disruptive threats, regulatory and technology barriers, and actionable implications for defense and growth.

Clear one-sheet Porter's Five Forces for Exact Sciences—quickly pinpoint competitive pressures in diagnostics and relieve strategic uncertainty for faster, data-driven decisions.

Customers Bargaining Power

Payers and reimbursement gatekeepers

CMS (including Medicare) and large commercial insurers set effective price points through coverage decisions and reimbursement rates, with stool DNA testing billed under CPT 81528 and national Medicare coverage in place as of 2024. Prior authorization and insurer medical policies materially shape test volume and mix by gating access. Inclusion in USPSTF-supported screening programs and published health-economic analyses strengthen Exact Sciences’ negotiating posture. Value-based arrangements can align access with price, offsetting payer leverage.

Health systems and large provider groups

Integrated delivery networks and GPOs aggregate demand across roughly 6,100 US hospitals (AHA, 2024) to negotiate volume discounts and tighter service terms, pressuring Exact Sciences on price and contracts. They favor formulary-like test menus, which can limit standalone test pricing. Demonstrated clinical utility and streamlined workflows boost stickiness, while embedded EHR ordering and reliable turnaround materially reduce switching risk.

Physicians as ordering influencers

Primary care, GI, and oncology physicians are the primary drivers of Cologuard adoption and repeat use, with USPSTF colorectal screening recommendations for ages 45–75 (2021) anchoring guideline sensitivity. Physicians prioritize guideline status, ease of use, and patient adherence; education, field support, and clear reports increase loyalty. Competing reps and convenient sample pick-up materially affect share-of-mind and ordering behavior.

Patients and adherence dynamics

Cologuard’s at-home convenience drives higher completion (real-world completion ≈65%), but the $649 list price and variable out-of-pocket exposure limit uptake among cost-sensitive patients. Ongoing DTC awareness creates pull that moderates buyer power by increasing demand and provider acceptance. Financial assistance programs and simple collection kits reduce friction, and strong patient experience boosts advocacy and word-of-mouth.

- Completion ≈65%

- List price $649

- DTC increases pull

- Assistance lowers friction

International payers and HTA bodies

Outside the U.S., HTA assessments and national tenders intensify price pressure; NICE’s 2024 cost‑effectiveness range remains ~£20,000–30,000 per QALY, shaping UK negotiations. Country‑specific evidence and dossier requirements increase rollout complexity, while local partnerships and real‑world data raise chances of favorable coverage. Currency swings and 3–5 year procurement cycles materially influence realized pricing.

- HTA thresholds affect list vs realized price

- Country evidence heterogeneity raises launch cost

- RWD/partners improve reimbursement odds

- FX and procurement timing drive revenue volatility

Payer controls, hospital discounting and NICE pressure constrain access: 65% completion, $649 price

Payers (Medicare national coverage 2024) and large insurers control reimbursement and prior authorization, constraining price and access. IDNs/GPOs (≈6,100 US hospitals, AHA 2024) pressure discounts; NICE HTA ranges (£20–30k/QALY, 2024) tighten international pricing. Physicians drive adoption; patient completion ≈65% and $649 list price shape demand and out‑of‑pocket sensitivity.

| Metric | Value (2024) |

|---|---|

| Medicare coverage | National (2024) |

| Hospital aggregation | ≈6,100 (AHA) |

| Patient completion | ≈65% |

| List price | $649 |

| NICE QALY range | £20k–30k |

Preview Before You Purchase

Exact Sciences Porter's Five Forces Analysis

This preview shows the Exact Sciences Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples. The document is professionally formatted, complete, and ready for download; upon payment you get instant access to this exact file for immediate use.

Don't Miss the Bigger Picture

Exact Sciences faces moderating supplier power, intense rivalry in diagnostic screening, and growing threat from innovative substitutes and new entrants as it scales commercialization of liquid biopsy and CRC screening products. Regulatory and reimbursement pressures amplify buyer leverage and margin risks, while IP and clinical data remain key defenses. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Exact Sciences’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized reagents and consumables

Exact Sciences depends on specialized reagents, oligos, antibodies and collection kits validated for specific assays, and these inputs underpin its ~$3.3B 2024 revenue base, making supplier issues high-impact. Supplier switching is constrained by analytical validation and regulatory filings, giving suppliers moderate pricing and continuity leverage. Mitigants include dual-sourcing, long-term contracts and safety-stock policies to reduce disruption risk.

Proprietary biomarkers and IP licensing

Proprietary biomarkers, algorithms, and method patents, including licensed know-how from partners, give Exact Sciences concentrated supplier-like power over key assay inputs in 2024. Royalties and exclusivity terms in licensing deals can raise costs and limit operational flexibility. As patents expire or internal discovery expands, dependence on external IP can decline. Strategic partnerships secure rights and share development and commercialization risk.

Laboratory equipment and platform vendors

Automated extraction, PCR and NGS platforms and robotics vendors exert leverage through multi-year service contracts and periodic upgrade cycles; NGS sequencers range from about $100,000 to over $1 million, with service agreements commonly 10–15% of equipment cost annually. Qualification and validation often take 3–9 months, raising switching costs and delaying deployment. Volume commitments and cross-site standardization can secure 10–30% unit-cost reductions and lower downtime risk. Diversifying vendors mitigates single-supplier disruption and preserves operational continuity.

Logistics and cold-chain carriers

Logistics and cold-chain carriers for Exact Sciences are concentrated among national carriers (UPS, FedEx, USPS) as of 2024, creating leverage where service disruptions or fuel surcharges can delay time-sensitive biological samples and compress margins.

Negotiated SLAs, redundant routing and regional cold-chain partnerships reduce single-carrier exposure, and Exact Sciences scale in at-home collection provides counter-leverage in pricing and service terms.

- Carrier concentration: national carriers dominate sample transport

- Risk: service disruptions or fuel surcharges affect TAT and margins

- Mitigants: SLAs + redundant routing + regional partners

- Leverage: large at-home collection scale strengthens negotiation

Data infrastructure and software tools

Cloud, LIMS and bioinformatics vendors are critical to Exact Sciences operations and quality control; 92% of enterprises used multi-cloud in 2024 (Flexera), raising dependency and switching costs especially given average data breach costs of ~$4.45M (IBM 2024). Strong compliance needs elevate lock-in, but multi-cloud strategies and in-house tooling plus volume discounts (cloud commitment savings up to ~40%) and co-development deals reduce supplier power.

- 92% multi-cloud adoption (2024)

- Average breach cost ~$4.45M (2024)

- Cloud commitment discounts up to ~40%

- In-house tooling and co-dev lower lock-in

Supply Risk: $3.3B, High Switching Costs, 92% Multi-cloud

Exact depends on specialized reagents, kits and platforms; supplier disruption is high-impact given ~\$3.3B 2024 revenue. Switching costs are high from validation, patents and multi-year service contracts; NGS sequencers \$100k–\$1M with service ~10–15% annually. Mitigants include dual-sourcing, long-term contracts, SLAs, multi-cloud and scale in at-home collection reducing supplier leverage.

| Category | 2024 metric | Impact |

|---|---|---|

| Revenue exposure | \$3.3B | High |

| NGS equipment | \$100k–\$1M; service 10–15% | High |

| Cloud adoption | 92% multi-cloud | Moderate |

What is included in the product

Tailored Porter's Five Forces analysis for Exact Sciences uncovering competitive drivers, buyer and supplier power, substitutes, and new‑entry risks; evaluates how these forces shape pricing, profitability, and strategic positioning in oncology and diagnostics. Includes identification of disruptive threats, regulatory and technology barriers, and actionable implications for defense and growth.

Clear one-sheet Porter's Five Forces for Exact Sciences—quickly pinpoint competitive pressures in diagnostics and relieve strategic uncertainty for faster, data-driven decisions.

Customers Bargaining Power

Payers and reimbursement gatekeepers

CMS (including Medicare) and large commercial insurers set effective price points through coverage decisions and reimbursement rates, with stool DNA testing billed under CPT 81528 and national Medicare coverage in place as of 2024. Prior authorization and insurer medical policies materially shape test volume and mix by gating access. Inclusion in USPSTF-supported screening programs and published health-economic analyses strengthen Exact Sciences’ negotiating posture. Value-based arrangements can align access with price, offsetting payer leverage.

Health systems and large provider groups

Integrated delivery networks and GPOs aggregate demand across roughly 6,100 US hospitals (AHA, 2024) to negotiate volume discounts and tighter service terms, pressuring Exact Sciences on price and contracts. They favor formulary-like test menus, which can limit standalone test pricing. Demonstrated clinical utility and streamlined workflows boost stickiness, while embedded EHR ordering and reliable turnaround materially reduce switching risk.

Physicians as ordering influencers

Primary care, GI, and oncology physicians are the primary drivers of Cologuard adoption and repeat use, with USPSTF colorectal screening recommendations for ages 45–75 (2021) anchoring guideline sensitivity. Physicians prioritize guideline status, ease of use, and patient adherence; education, field support, and clear reports increase loyalty. Competing reps and convenient sample pick-up materially affect share-of-mind and ordering behavior.

Patients and adherence dynamics

Cologuard’s at-home convenience drives higher completion (real-world completion ≈65%), but the $649 list price and variable out-of-pocket exposure limit uptake among cost-sensitive patients. Ongoing DTC awareness creates pull that moderates buyer power by increasing demand and provider acceptance. Financial assistance programs and simple collection kits reduce friction, and strong patient experience boosts advocacy and word-of-mouth.

- Completion ≈65%

- List price $649

- DTC increases pull

- Assistance lowers friction

International payers and HTA bodies

Outside the U.S., HTA assessments and national tenders intensify price pressure; NICE’s 2024 cost‑effectiveness range remains ~£20,000–30,000 per QALY, shaping UK negotiations. Country‑specific evidence and dossier requirements increase rollout complexity, while local partnerships and real‑world data raise chances of favorable coverage. Currency swings and 3–5 year procurement cycles materially influence realized pricing.

- HTA thresholds affect list vs realized price

- Country evidence heterogeneity raises launch cost

- RWD/partners improve reimbursement odds

- FX and procurement timing drive revenue volatility

Payer controls, hospital discounting and NICE pressure constrain access: 65% completion, $649 price

Payers (Medicare national coverage 2024) and large insurers control reimbursement and prior authorization, constraining price and access. IDNs/GPOs (≈6,100 US hospitals, AHA 2024) pressure discounts; NICE HTA ranges (£20–30k/QALY, 2024) tighten international pricing. Physicians drive adoption; patient completion ≈65% and $649 list price shape demand and out‑of‑pocket sensitivity.

| Metric | Value (2024) |

|---|---|

| Medicare coverage | National (2024) |

| Hospital aggregation | ≈6,100 (AHA) |

| Patient completion | ≈65% |

| List price | $649 |

| NICE QALY range | £20k–30k |

Preview Before You Purchase

Exact Sciences Porter's Five Forces Analysis

This preview shows the Exact Sciences Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples. The document is professionally formatted, complete, and ready for download; upon payment you get instant access to this exact file for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Exact Sciences faces moderating supplier power, intense rivalry in diagnostic screening, and growing threat from innovative substitutes and new entrants as it scales commercialization of liquid biopsy and CRC screening products. Regulatory and reimbursement pressures amplify buyer leverage and margin risks, while IP and clinical data remain key defenses. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Exact Sciences’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized reagents and consumables

Exact Sciences depends on specialized reagents, oligos, antibodies and collection kits validated for specific assays, and these inputs underpin its ~$3.3B 2024 revenue base, making supplier issues high-impact. Supplier switching is constrained by analytical validation and regulatory filings, giving suppliers moderate pricing and continuity leverage. Mitigants include dual-sourcing, long-term contracts and safety-stock policies to reduce disruption risk.

Proprietary biomarkers and IP licensing

Proprietary biomarkers, algorithms, and method patents, including licensed know-how from partners, give Exact Sciences concentrated supplier-like power over key assay inputs in 2024. Royalties and exclusivity terms in licensing deals can raise costs and limit operational flexibility. As patents expire or internal discovery expands, dependence on external IP can decline. Strategic partnerships secure rights and share development and commercialization risk.

Laboratory equipment and platform vendors

Automated extraction, PCR and NGS platforms and robotics vendors exert leverage through multi-year service contracts and periodic upgrade cycles; NGS sequencers range from about $100,000 to over $1 million, with service agreements commonly 10–15% of equipment cost annually. Qualification and validation often take 3–9 months, raising switching costs and delaying deployment. Volume commitments and cross-site standardization can secure 10–30% unit-cost reductions and lower downtime risk. Diversifying vendors mitigates single-supplier disruption and preserves operational continuity.

Logistics and cold-chain carriers

Logistics and cold-chain carriers for Exact Sciences are concentrated among national carriers (UPS, FedEx, USPS) as of 2024, creating leverage where service disruptions or fuel surcharges can delay time-sensitive biological samples and compress margins.

Negotiated SLAs, redundant routing and regional cold-chain partnerships reduce single-carrier exposure, and Exact Sciences scale in at-home collection provides counter-leverage in pricing and service terms.

- Carrier concentration: national carriers dominate sample transport

- Risk: service disruptions or fuel surcharges affect TAT and margins

- Mitigants: SLAs + redundant routing + regional partners

- Leverage: large at-home collection scale strengthens negotiation

Data infrastructure and software tools

Cloud, LIMS and bioinformatics vendors are critical to Exact Sciences operations and quality control; 92% of enterprises used multi-cloud in 2024 (Flexera), raising dependency and switching costs especially given average data breach costs of ~$4.45M (IBM 2024). Strong compliance needs elevate lock-in, but multi-cloud strategies and in-house tooling plus volume discounts (cloud commitment savings up to ~40%) and co-development deals reduce supplier power.

- 92% multi-cloud adoption (2024)

- Average breach cost ~$4.45M (2024)

- Cloud commitment discounts up to ~40%

- In-house tooling and co-dev lower lock-in

Supply Risk: $3.3B, High Switching Costs, 92% Multi-cloud

Exact depends on specialized reagents, kits and platforms; supplier disruption is high-impact given ~\$3.3B 2024 revenue. Switching costs are high from validation, patents and multi-year service contracts; NGS sequencers \$100k–\$1M with service ~10–15% annually. Mitigants include dual-sourcing, long-term contracts, SLAs, multi-cloud and scale in at-home collection reducing supplier leverage.

| Category | 2024 metric | Impact |

|---|---|---|

| Revenue exposure | \$3.3B | High |

| NGS equipment | \$100k–\$1M; service 10–15% | High |

| Cloud adoption | 92% multi-cloud | Moderate |

What is included in the product

Tailored Porter's Five Forces analysis for Exact Sciences uncovering competitive drivers, buyer and supplier power, substitutes, and new‑entry risks; evaluates how these forces shape pricing, profitability, and strategic positioning in oncology and diagnostics. Includes identification of disruptive threats, regulatory and technology barriers, and actionable implications for defense and growth.

Clear one-sheet Porter's Five Forces for Exact Sciences—quickly pinpoint competitive pressures in diagnostics and relieve strategic uncertainty for faster, data-driven decisions.

Customers Bargaining Power

Payers and reimbursement gatekeepers

CMS (including Medicare) and large commercial insurers set effective price points through coverage decisions and reimbursement rates, with stool DNA testing billed under CPT 81528 and national Medicare coverage in place as of 2024. Prior authorization and insurer medical policies materially shape test volume and mix by gating access. Inclusion in USPSTF-supported screening programs and published health-economic analyses strengthen Exact Sciences’ negotiating posture. Value-based arrangements can align access with price, offsetting payer leverage.

Health systems and large provider groups

Integrated delivery networks and GPOs aggregate demand across roughly 6,100 US hospitals (AHA, 2024) to negotiate volume discounts and tighter service terms, pressuring Exact Sciences on price and contracts. They favor formulary-like test menus, which can limit standalone test pricing. Demonstrated clinical utility and streamlined workflows boost stickiness, while embedded EHR ordering and reliable turnaround materially reduce switching risk.

Physicians as ordering influencers

Primary care, GI, and oncology physicians are the primary drivers of Cologuard adoption and repeat use, with USPSTF colorectal screening recommendations for ages 45–75 (2021) anchoring guideline sensitivity. Physicians prioritize guideline status, ease of use, and patient adherence; education, field support, and clear reports increase loyalty. Competing reps and convenient sample pick-up materially affect share-of-mind and ordering behavior.

Patients and adherence dynamics

Cologuard’s at-home convenience drives higher completion (real-world completion ≈65%), but the $649 list price and variable out-of-pocket exposure limit uptake among cost-sensitive patients. Ongoing DTC awareness creates pull that moderates buyer power by increasing demand and provider acceptance. Financial assistance programs and simple collection kits reduce friction, and strong patient experience boosts advocacy and word-of-mouth.

- Completion ≈65%

- List price $649

- DTC increases pull

- Assistance lowers friction

International payers and HTA bodies

Outside the U.S., HTA assessments and national tenders intensify price pressure; NICE’s 2024 cost‑effectiveness range remains ~£20,000–30,000 per QALY, shaping UK negotiations. Country‑specific evidence and dossier requirements increase rollout complexity, while local partnerships and real‑world data raise chances of favorable coverage. Currency swings and 3–5 year procurement cycles materially influence realized pricing.

- HTA thresholds affect list vs realized price

- Country evidence heterogeneity raises launch cost

- RWD/partners improve reimbursement odds

- FX and procurement timing drive revenue volatility

Payer controls, hospital discounting and NICE pressure constrain access: 65% completion, $649 price

Payers (Medicare national coverage 2024) and large insurers control reimbursement and prior authorization, constraining price and access. IDNs/GPOs (≈6,100 US hospitals, AHA 2024) pressure discounts; NICE HTA ranges (£20–30k/QALY, 2024) tighten international pricing. Physicians drive adoption; patient completion ≈65% and $649 list price shape demand and out‑of‑pocket sensitivity.

| Metric | Value (2024) |

|---|---|

| Medicare coverage | National (2024) |

| Hospital aggregation | ≈6,100 (AHA) |

| Patient completion | ≈65% |

| List price | $649 |

| NICE QALY range | £20k–30k |

Preview Before You Purchase

Exact Sciences Porter's Five Forces Analysis

This preview shows the Exact Sciences Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples. The document is professionally formatted, complete, and ready for download; upon payment you get instant access to this exact file for immediate use.