Exel Composites PESTLE Analysis

Your Shortcut to Market Insight Starts Here

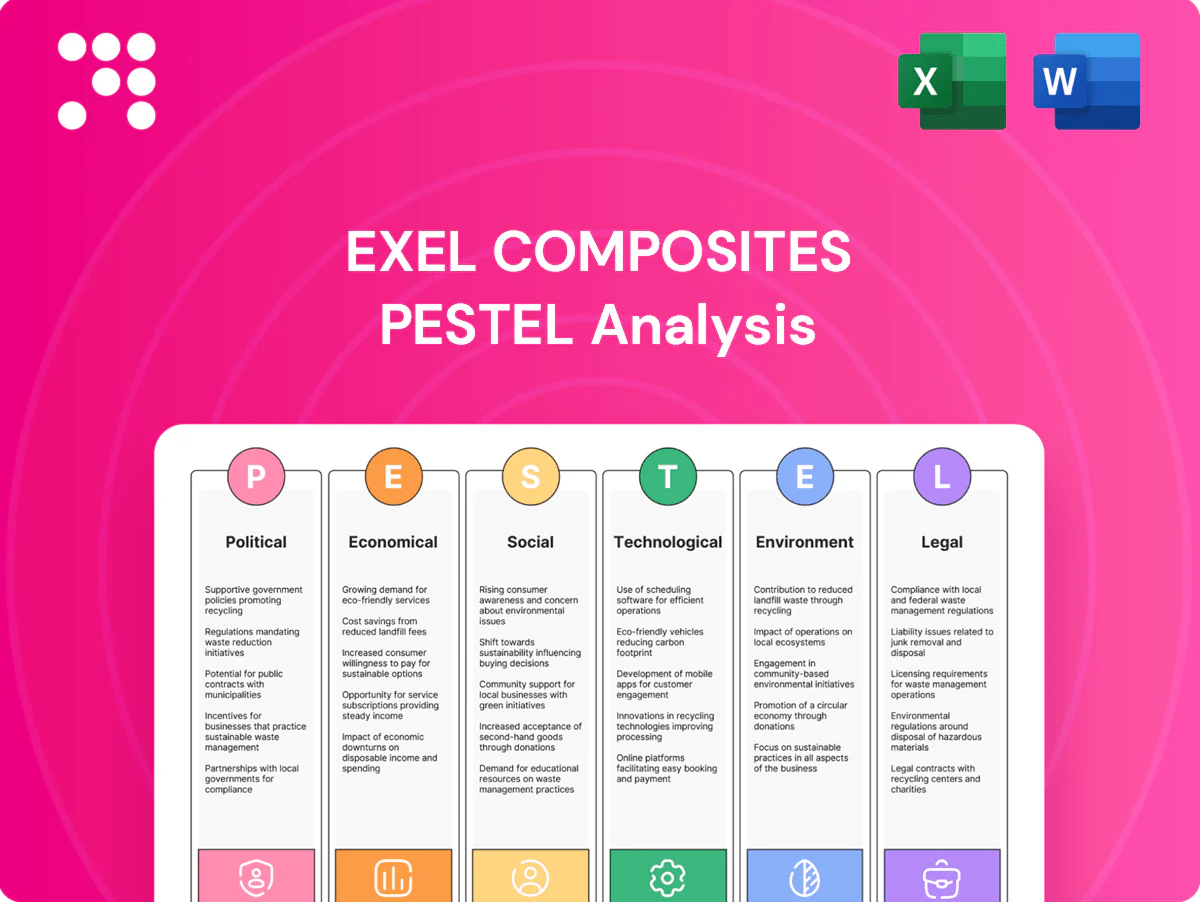

Our PESTLE Analysis for Exel Composites reveals how political regulation, economic cycles, and advancing composite technologies shape its strategic outlook, while social and environmental trends create both risks and opportunities; buy the full report to access detailed, actionable insights and downloadable templates.

Political factors

Trade policies and tariffs on composite materials

Changes in tariffs on glass/carbon fibers, resins and finished profiles—sometimes reaching up to 25% on imports—can materially shift Exel Composites’ cost base and cross‑border pricing; the global composites market exceeded USD 100 billion in 2023. Regional content rules in the EU, US and Asia reframe sourcing and favor local production. Monitoring anti‑dumping cases and adjusting supply chains preserves margins, while proactive engagement with trade bodies mitigates disruptions.

Industrial policy and infrastructure investment

EU recovery and cohesion funds (NextGenerationEU €806.9bn, cohesion €392bn for 2021–2027) and national spending on rail, grids and broadband favor lightweight, corrosion‑resistant composites that can cut component weight by up to 60% versus steel. Public procurement increasingly uses lifecycle costing, advantaging pultruded, low‑maintenance solutions; shifts in fiscal priorities can swing multi‑year project pipelines, so early vendor qualification secures share in long‑cycle programs.

Geopolitical supply risk management

Geopolitical tensions since Russia’s invasion of Ukraine on 24 February 2022 have disrupted resin and fiber-precursor flows, raising lead times for composites buyers. Diversified plants and multi-sourcing reduce exposure to regional shocks and are common mitigation. Currency controls or sanctions (eg EU/US measures since 2022) can complicate sales in select markets. Scenario planning helps balance nearshore and offshore capacity.

Sustainability-driven subsidies and incentives

Policy incentives favor low-carbon materials, enabling composites to substitute steel/aluminum as EU ETS carbon prices rose above €100/t in 2024 and US clean-energy tax credits under the Inflation Reduction Act total about $369bn over a decade, lowering project payback hurdles. Grants and tax credits for energy-efficient manufacturing reduce capex for process upgrades, but eligibility increasingly requires robust ESG reporting and traceability; alignment with green public taxonomies improves access to procurement and funding.

- EU ETS > €100/t (2024)

- IRA ~ $369bn clean-energy tax credits

- ESG reporting and traceability required

- Taxonomy alignment eases public procurement access

Standards harmonization and public safety requirements

Government-backed rail, building and wind standards (eg EN 45545, CPR, IEC 61400 series) guide approvals for Exel Composites materials, with the global composites market ~USD 90–95bn in 2024 and ~6–7% CAGR, increasing demand for certified profiles and tubes.

Harmonized norms ease multi-country sales of standard profiles and custom tubes, while new fire, smoke and toxicity thresholds (stricter in EU/UK since 2023–24) can force resin reformulation; active participation in standards committees shortens market entry and cuts compliance lag.

Trade shocks, green funds and regulation reshape composites: nearshoring, low-carbon demand rise

Tariffs, anti‑dumping and sanctions (post‑2022) materially affect Exel Composites’ costs and market access; diversified sourcing and nearshoring mitigate risk. EU funds (NextGenerationEU €806.9bn) and high carbon prices (EU ETS >€100/t in 2024) boost demand for low‑carbon composites; IRA ~ $369bn supports US projects. Stricter EU/UK fire/toxicity rules force resin reformulation and certification.

| Indicator | Value |

|---|---|

| Composites market 2024 | USD 90–95bn |

| EU ETS | >€100/t (2024) |

| IRA | ~$369bn |

What is included in the product

Explores how macro-environmental factors uniquely affect Exel Composites across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section is data-backed, region- and industry-specific, and provides forward-looking insights to inform strategy, risk mitigation and investment decisions.

Clean, summarized PESTLE insights for Exel Composites that are visually segmented by category, easily dropped into presentations or shared across teams to speed planning, support external risk discussions, and allow quick annotation for region- or product-specific context.

Economic factors

Cyclicality across end-markets

Demand for Exel Composites’ products closely follows investment cycles in construction, transportation and energy, making revenues cyclical across these end-markets. Diversification across sectors smooths revenue streams but cannot fully offset industry-wide downturns. Backlogs in long-cycle verticals provide a buffer against short-term volatility. Close forecasting with key accounts improves capacity utilization and order visibility.

Raw material price volatility

Resin, fiber and energy price volatility in 2024 continues to pressure Exel Composites gross margins, with feedstock-driven swings transmitted directly to unit costs. Index-linked contracts and hedging strategies are used to stabilise selling prices and protect margin visibility. Ongoing value engineering and yield improvements tighten unit economics, while strategic inventory management and closer supplier partnerships reduce exposure to sudden input shocks.

Exchange rate fluctuations

Multi-region sales expose Exel Composites, listed on Nasdaq Helsinki, to currency risk across EMEA, APAC and North America, affecting both revenue and imported inputs. Local sourcing and production in key markets create natural hedges that reduce transactional exposure. Financial hedging programs are used to smooth earnings visibility. Regional price lists and contractual pricing clauses help mitigate FX pass-through lags.

Labor availability and productivity

Skilled operators and engineers remain critical for pultrusion quality and throughput, with Exel Composites relying on specialist roles for precision processes; tight Nordic labor markets pushed manufacturing wage growth to about 3.5% in 2024 (Statistics Finland), raising operating costs and training needs. Automation and digitized QA can boost productivity per head by up to 30% (McKinsey), while apprenticeships and retention programs cut turnover risk and recruitment costs.

- Skilled staff: quality-dependent

- Wage pressure: ~3.5% rise in 2024

- Automation: up to 30% productivity gain

- Apprenticeships: lower turnover risk

Capital intensity and ROI discipline

Pultrusion lines require targeted capex justified by utilization and product mix; modular line upgrades let Exel Composites scale capacity to high-margin segments without large sunk costs. OEE and lean programs lift asset returns and shorten payback, while disciplined project selection preserves free cash flow and limits balance sheet strain.

- Capex tied to utilization and mix; modular upgrades; OEE/lean improve ROI; disciplined projects protect FCF

Trade shocks, green funds and regulation reshape composites: nearshoring, low-carbon demand rise

Exel Composites revenues track construction, transport and energy cycles, creating cyclical sales; backlogs in long-cycle projects smooth short-term volatility. 2024 resin and fiber price swings compressed gross margins; index-linked contracts and hedges improve visibility. Nordic wage growth ~3.5% in 2024 raised operating costs; automation can boost productivity up to 30%.

| Metric | 2024/2025 |

|---|---|

| Nordic wage growth | ~3.5% (2024) |

| Automation upside | Up to 30% productivity |

| Input volatility | Resin/fiber high in 2024 |

| Listing | Nasdaq Helsinki |

Same Document Delivered

Exel Composites PESTLE Analysis

The preview shown here is the exact Exel Composites PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains the complete political, economic, social, technological, legal and environmental review as displayed. No placeholders or teasers—what you see is the final downloadable file.

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis for Exel Composites reveals how political regulation, economic cycles, and advancing composite technologies shape its strategic outlook, while social and environmental trends create both risks and opportunities; buy the full report to access detailed, actionable insights and downloadable templates.

Political factors

Trade policies and tariffs on composite materials

Changes in tariffs on glass/carbon fibers, resins and finished profiles—sometimes reaching up to 25% on imports—can materially shift Exel Composites’ cost base and cross‑border pricing; the global composites market exceeded USD 100 billion in 2023. Regional content rules in the EU, US and Asia reframe sourcing and favor local production. Monitoring anti‑dumping cases and adjusting supply chains preserves margins, while proactive engagement with trade bodies mitigates disruptions.

Industrial policy and infrastructure investment

EU recovery and cohesion funds (NextGenerationEU €806.9bn, cohesion €392bn for 2021–2027) and national spending on rail, grids and broadband favor lightweight, corrosion‑resistant composites that can cut component weight by up to 60% versus steel. Public procurement increasingly uses lifecycle costing, advantaging pultruded, low‑maintenance solutions; shifts in fiscal priorities can swing multi‑year project pipelines, so early vendor qualification secures share in long‑cycle programs.

Geopolitical supply risk management

Geopolitical tensions since Russia’s invasion of Ukraine on 24 February 2022 have disrupted resin and fiber-precursor flows, raising lead times for composites buyers. Diversified plants and multi-sourcing reduce exposure to regional shocks and are common mitigation. Currency controls or sanctions (eg EU/US measures since 2022) can complicate sales in select markets. Scenario planning helps balance nearshore and offshore capacity.

Sustainability-driven subsidies and incentives

Policy incentives favor low-carbon materials, enabling composites to substitute steel/aluminum as EU ETS carbon prices rose above €100/t in 2024 and US clean-energy tax credits under the Inflation Reduction Act total about $369bn over a decade, lowering project payback hurdles. Grants and tax credits for energy-efficient manufacturing reduce capex for process upgrades, but eligibility increasingly requires robust ESG reporting and traceability; alignment with green public taxonomies improves access to procurement and funding.

- EU ETS > €100/t (2024)

- IRA ~ $369bn clean-energy tax credits

- ESG reporting and traceability required

- Taxonomy alignment eases public procurement access

Standards harmonization and public safety requirements

Government-backed rail, building and wind standards (eg EN 45545, CPR, IEC 61400 series) guide approvals for Exel Composites materials, with the global composites market ~USD 90–95bn in 2024 and ~6–7% CAGR, increasing demand for certified profiles and tubes.

Harmonized norms ease multi-country sales of standard profiles and custom tubes, while new fire, smoke and toxicity thresholds (stricter in EU/UK since 2023–24) can force resin reformulation; active participation in standards committees shortens market entry and cuts compliance lag.

Trade shocks, green funds and regulation reshape composites: nearshoring, low-carbon demand rise

Tariffs, anti‑dumping and sanctions (post‑2022) materially affect Exel Composites’ costs and market access; diversified sourcing and nearshoring mitigate risk. EU funds (NextGenerationEU €806.9bn) and high carbon prices (EU ETS >€100/t in 2024) boost demand for low‑carbon composites; IRA ~ $369bn supports US projects. Stricter EU/UK fire/toxicity rules force resin reformulation and certification.

| Indicator | Value |

|---|---|

| Composites market 2024 | USD 90–95bn |

| EU ETS | >€100/t (2024) |

| IRA | ~$369bn |

What is included in the product

Explores how macro-environmental factors uniquely affect Exel Composites across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section is data-backed, region- and industry-specific, and provides forward-looking insights to inform strategy, risk mitigation and investment decisions.

Clean, summarized PESTLE insights for Exel Composites that are visually segmented by category, easily dropped into presentations or shared across teams to speed planning, support external risk discussions, and allow quick annotation for region- or product-specific context.

Economic factors

Cyclicality across end-markets

Demand for Exel Composites’ products closely follows investment cycles in construction, transportation and energy, making revenues cyclical across these end-markets. Diversification across sectors smooths revenue streams but cannot fully offset industry-wide downturns. Backlogs in long-cycle verticals provide a buffer against short-term volatility. Close forecasting with key accounts improves capacity utilization and order visibility.

Raw material price volatility

Resin, fiber and energy price volatility in 2024 continues to pressure Exel Composites gross margins, with feedstock-driven swings transmitted directly to unit costs. Index-linked contracts and hedging strategies are used to stabilise selling prices and protect margin visibility. Ongoing value engineering and yield improvements tighten unit economics, while strategic inventory management and closer supplier partnerships reduce exposure to sudden input shocks.

Exchange rate fluctuations

Multi-region sales expose Exel Composites, listed on Nasdaq Helsinki, to currency risk across EMEA, APAC and North America, affecting both revenue and imported inputs. Local sourcing and production in key markets create natural hedges that reduce transactional exposure. Financial hedging programs are used to smooth earnings visibility. Regional price lists and contractual pricing clauses help mitigate FX pass-through lags.

Labor availability and productivity

Skilled operators and engineers remain critical for pultrusion quality and throughput, with Exel Composites relying on specialist roles for precision processes; tight Nordic labor markets pushed manufacturing wage growth to about 3.5% in 2024 (Statistics Finland), raising operating costs and training needs. Automation and digitized QA can boost productivity per head by up to 30% (McKinsey), while apprenticeships and retention programs cut turnover risk and recruitment costs.

- Skilled staff: quality-dependent

- Wage pressure: ~3.5% rise in 2024

- Automation: up to 30% productivity gain

- Apprenticeships: lower turnover risk

Capital intensity and ROI discipline

Pultrusion lines require targeted capex justified by utilization and product mix; modular line upgrades let Exel Composites scale capacity to high-margin segments without large sunk costs. OEE and lean programs lift asset returns and shorten payback, while disciplined project selection preserves free cash flow and limits balance sheet strain.

- Capex tied to utilization and mix; modular upgrades; OEE/lean improve ROI; disciplined projects protect FCF

Trade shocks, green funds and regulation reshape composites: nearshoring, low-carbon demand rise

Exel Composites revenues track construction, transport and energy cycles, creating cyclical sales; backlogs in long-cycle projects smooth short-term volatility. 2024 resin and fiber price swings compressed gross margins; index-linked contracts and hedges improve visibility. Nordic wage growth ~3.5% in 2024 raised operating costs; automation can boost productivity up to 30%.

| Metric | 2024/2025 |

|---|---|

| Nordic wage growth | ~3.5% (2024) |

| Automation upside | Up to 30% productivity |

| Input volatility | Resin/fiber high in 2024 |

| Listing | Nasdaq Helsinki |

Same Document Delivered

Exel Composites PESTLE Analysis

The preview shown here is the exact Exel Composites PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains the complete political, economic, social, technological, legal and environmental review as displayed. No placeholders or teasers—what you see is the final downloadable file.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis for Exel Composites reveals how political regulation, economic cycles, and advancing composite technologies shape its strategic outlook, while social and environmental trends create both risks and opportunities; buy the full report to access detailed, actionable insights and downloadable templates.

Political factors

Trade policies and tariffs on composite materials

Changes in tariffs on glass/carbon fibers, resins and finished profiles—sometimes reaching up to 25% on imports—can materially shift Exel Composites’ cost base and cross‑border pricing; the global composites market exceeded USD 100 billion in 2023. Regional content rules in the EU, US and Asia reframe sourcing and favor local production. Monitoring anti‑dumping cases and adjusting supply chains preserves margins, while proactive engagement with trade bodies mitigates disruptions.

Industrial policy and infrastructure investment

EU recovery and cohesion funds (NextGenerationEU €806.9bn, cohesion €392bn for 2021–2027) and national spending on rail, grids and broadband favor lightweight, corrosion‑resistant composites that can cut component weight by up to 60% versus steel. Public procurement increasingly uses lifecycle costing, advantaging pultruded, low‑maintenance solutions; shifts in fiscal priorities can swing multi‑year project pipelines, so early vendor qualification secures share in long‑cycle programs.

Geopolitical supply risk management

Geopolitical tensions since Russia’s invasion of Ukraine on 24 February 2022 have disrupted resin and fiber-precursor flows, raising lead times for composites buyers. Diversified plants and multi-sourcing reduce exposure to regional shocks and are common mitigation. Currency controls or sanctions (eg EU/US measures since 2022) can complicate sales in select markets. Scenario planning helps balance nearshore and offshore capacity.

Sustainability-driven subsidies and incentives

Policy incentives favor low-carbon materials, enabling composites to substitute steel/aluminum as EU ETS carbon prices rose above €100/t in 2024 and US clean-energy tax credits under the Inflation Reduction Act total about $369bn over a decade, lowering project payback hurdles. Grants and tax credits for energy-efficient manufacturing reduce capex for process upgrades, but eligibility increasingly requires robust ESG reporting and traceability; alignment with green public taxonomies improves access to procurement and funding.

- EU ETS > €100/t (2024)

- IRA ~ $369bn clean-energy tax credits

- ESG reporting and traceability required

- Taxonomy alignment eases public procurement access

Standards harmonization and public safety requirements

Government-backed rail, building and wind standards (eg EN 45545, CPR, IEC 61400 series) guide approvals for Exel Composites materials, with the global composites market ~USD 90–95bn in 2024 and ~6–7% CAGR, increasing demand for certified profiles and tubes.

Harmonized norms ease multi-country sales of standard profiles and custom tubes, while new fire, smoke and toxicity thresholds (stricter in EU/UK since 2023–24) can force resin reformulation; active participation in standards committees shortens market entry and cuts compliance lag.

Trade shocks, green funds and regulation reshape composites: nearshoring, low-carbon demand rise

Tariffs, anti‑dumping and sanctions (post‑2022) materially affect Exel Composites’ costs and market access; diversified sourcing and nearshoring mitigate risk. EU funds (NextGenerationEU €806.9bn) and high carbon prices (EU ETS >€100/t in 2024) boost demand for low‑carbon composites; IRA ~ $369bn supports US projects. Stricter EU/UK fire/toxicity rules force resin reformulation and certification.

| Indicator | Value |

|---|---|

| Composites market 2024 | USD 90–95bn |

| EU ETS | >€100/t (2024) |

| IRA | ~$369bn |

What is included in the product

Explores how macro-environmental factors uniquely affect Exel Composites across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section is data-backed, region- and industry-specific, and provides forward-looking insights to inform strategy, risk mitigation and investment decisions.

Clean, summarized PESTLE insights for Exel Composites that are visually segmented by category, easily dropped into presentations or shared across teams to speed planning, support external risk discussions, and allow quick annotation for region- or product-specific context.

Economic factors

Cyclicality across end-markets

Demand for Exel Composites’ products closely follows investment cycles in construction, transportation and energy, making revenues cyclical across these end-markets. Diversification across sectors smooths revenue streams but cannot fully offset industry-wide downturns. Backlogs in long-cycle verticals provide a buffer against short-term volatility. Close forecasting with key accounts improves capacity utilization and order visibility.

Raw material price volatility

Resin, fiber and energy price volatility in 2024 continues to pressure Exel Composites gross margins, with feedstock-driven swings transmitted directly to unit costs. Index-linked contracts and hedging strategies are used to stabilise selling prices and protect margin visibility. Ongoing value engineering and yield improvements tighten unit economics, while strategic inventory management and closer supplier partnerships reduce exposure to sudden input shocks.

Exchange rate fluctuations

Multi-region sales expose Exel Composites, listed on Nasdaq Helsinki, to currency risk across EMEA, APAC and North America, affecting both revenue and imported inputs. Local sourcing and production in key markets create natural hedges that reduce transactional exposure. Financial hedging programs are used to smooth earnings visibility. Regional price lists and contractual pricing clauses help mitigate FX pass-through lags.

Labor availability and productivity

Skilled operators and engineers remain critical for pultrusion quality and throughput, with Exel Composites relying on specialist roles for precision processes; tight Nordic labor markets pushed manufacturing wage growth to about 3.5% in 2024 (Statistics Finland), raising operating costs and training needs. Automation and digitized QA can boost productivity per head by up to 30% (McKinsey), while apprenticeships and retention programs cut turnover risk and recruitment costs.

- Skilled staff: quality-dependent

- Wage pressure: ~3.5% rise in 2024

- Automation: up to 30% productivity gain

- Apprenticeships: lower turnover risk

Capital intensity and ROI discipline

Pultrusion lines require targeted capex justified by utilization and product mix; modular line upgrades let Exel Composites scale capacity to high-margin segments without large sunk costs. OEE and lean programs lift asset returns and shorten payback, while disciplined project selection preserves free cash flow and limits balance sheet strain.

- Capex tied to utilization and mix; modular upgrades; OEE/lean improve ROI; disciplined projects protect FCF

Trade shocks, green funds and regulation reshape composites: nearshoring, low-carbon demand rise

Exel Composites revenues track construction, transport and energy cycles, creating cyclical sales; backlogs in long-cycle projects smooth short-term volatility. 2024 resin and fiber price swings compressed gross margins; index-linked contracts and hedges improve visibility. Nordic wage growth ~3.5% in 2024 raised operating costs; automation can boost productivity up to 30%.

| Metric | 2024/2025 |

|---|---|

| Nordic wage growth | ~3.5% (2024) |

| Automation upside | Up to 30% productivity |

| Input volatility | Resin/fiber high in 2024 |

| Listing | Nasdaq Helsinki |

Same Document Delivered

Exel Composites PESTLE Analysis

The preview shown here is the exact Exel Composites PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains the complete political, economic, social, technological, legal and environmental review as displayed. No placeholders or teasers—what you see is the final downloadable file.