Extreme Networks PESTLE Analysis

Skip the Research. Get the Strategy.

Our PESTLE Analysis for Extreme Networks reveals how political shifts, economic cycles, social trends, technological innovation, legal changes, and environmental pressures jointly shape its strategic outlook. It’s concise, evidence-based, and tailored for investors and strategists. Purchase the full report to access the complete, actionable breakdown and ready-to-use templates.

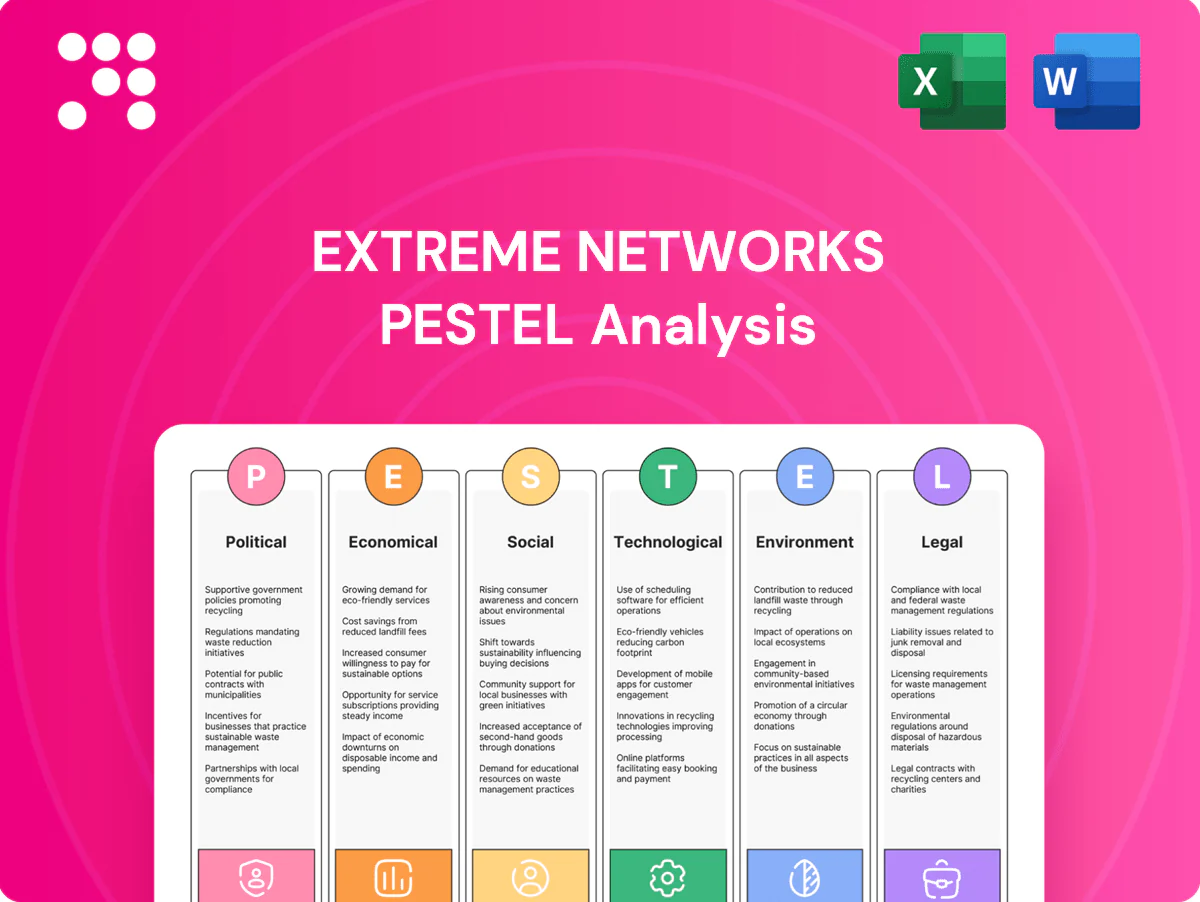

Political factors

Government IT spending and procurement

Public sector modernization and the IIJA broadband package (65 billion USD total, including the 42.45 billion USD BEAD program) drive demand for campus, K‑12 and municipal networks, shaping project pipelines. Extreme must navigate multi‑year budgeting and RFP‑driven procurement cycles while meeting Build America, Buy America and local content rules that can accelerate or block wins. Stable federal and state funding supports recurring cloud subscriptions via long‑term contracts tied to awarded grants.

Geopolitical trade and export controls

Tariffs, sanctions and export licensing raise hardware costs, constrain component sourcing and limit market access—U.S. tariffs on targeted ICT goods have reached up to 25% and the U.S. Entity List expanded to about 1,600 entries by 2024. Restrictions on advanced networking and encryption force product variants and can block sales in China and allied markets. Shifts in U.S.‑China relations are accelerating supply‑chain localization to ASEAN/onshore hubs; scenario planning and multi‑source BOMs mitigate disruption risk.

Domestic infrastructure and digital sovereignty

Rising digital sovereignty—with data localization rules now in 65+ countries—pushes demand for in-region cloud hosting, directly affecting Extreme’s cloud-managed platforms. Participation in national cloud marketplaces (public cloud market >$600B in 2024 per Gartner) can unlock enterprise and government contracts. Compliance often requires regional PoPs or partners; policy momentum favors vendors offering flexible onshore deployment models.

CERT, NIST, and critical infrastructure directives

CERT, NIST SP 800-207 (Zero Trust, 2020) and Executive Order 14028 (May 12, 2021) plus CISA directives push network segmentation, zero trust and continuous monitoring as federal baseline; DHS defines 16 critical infrastructure sectors that drive sectoral mandates in health, energy and transport. Extreme can map roadmaps to hardened configs and pursue certifications to capture regulated upgrade cycles and tender advantages.

- NIST SP 800-207 (2020) — zero trust baseline

- EO 14028 (May 12, 2021) — federal modernization driver

- 16 critical infrastructure sectors — sectoral mandates

- Cert wins → competitive edge in regulated tenders

Standards and spectrum policy

Decisions on 6 GHz and emerging 7 GHz allocations directly shape Extreme Networks wireless product roadmaps, since the FCC opened 1,200 MHz of 6 GHz for unlicensed use in 2020 and regulators differ by country. IEEE/IETF engagement matters: IEEE 802.11be (Wi‑Fi 7) was ratified in 2024, enabling theoretical PHY rates up to 46 Gbps, which drives interoperability and future-proofing.

- 6 GHz: 1,200 MHz opened in US (FCC, 2020)

- Wi‑Fi 7: 802.11be ratified 2024, up to 46 Gbps

- National spectrum variance → multiple SKUs and staggered launches

- Clear policy → faster enterprise adoption of high‑throughput WLAN

IIJA/BEAD and data localization push campus networks; 6 GHz/Wi-Fi7 timing critical

Federal IIJA funding ($65B, BEAD $42.45B) and stable grant cycles boost campus/municipal network demand while Build America, Buy America rules and tariffs (up to 25%) shape procurement and supply costs. Data localization (65+ countries) and cloud market scale (> $600B in 2024) force regional deployments. Spectrum (6 GHz 1,200 MHz) and Wi‑Fi7 (802.11be, 2024) drive product timing.

| Policy | Key figure |

|---|---|

| IIJA/BEAD | $65B / $42.45B |

| Tariffs/Entity List | Up to 25% / ~1,600 entries (2024) |

| Data localization | 65+ countries |

| Cloud market (2024) | >$600B |

| 6 GHz / Wi‑Fi7 | 1,200 MHz / 46 Gbps |

What is included in the product

Explores how macro-environmental factors across Political, Economic, Social, Technological, Environmental and Legal dimensions uniquely affect Extreme Networks; each section is backed by data and current trends, offers forward-looking insights and practical examples to support executives, investors and strategists in risk and opportunity planning.

Visually segmented by PESTEL categories, allowing for quick interpretation at a glance and effortless insertion into presentations or planning sessions to align teams rapidly.

Economic factors

Enterprise IT spending cycles

Macro growth and CIO budget sentiment drive campus and data-center refresh timing, with 2024 surveys showing more than half of CIOs signaling stable or rising networking budgets, accelerating refresh cycles. Cloud-managed OPEX models have proved more resilient during CAPEX freezes, supporting steady subscription growth for vendors like Extreme. Vertical exposure to education, healthcare and hospitality creates mixed cyclicality tied to public and travel spend patterns. Subscription attach and multi-year agreements have measurably improved pipeline visibility and revenue predictability for networking vendors.

Interest rates and capital costs

Higher policy rates—federal funds near 5.25–5.50% in H1 2025—raise customer CAPEX hurdles and vendor financing costs, lengthening sales cycles for large hardware deals. Extreme's growing as-a-service and leasing options reduce upfront barriers and expand deal sizes. Rate declines historically prompt deferred refresh waves that can boost demand. Treasury hedging and disciplined pricing help protect gross margins and cash flow.

FX volatility and global revenue mix

FX volatility can swing reported revenue for Extreme Networks—which posted about $1.2 billion revenue in FY2024—altering competitiveness versus local vendors when the dollar moves. Sourcing and manufacturing footprints in APAC and EMEA provide natural hedges by matching cost and sales currencies. Pricing localization and FX pass-through clauses reduce deal slippage. Financial planning must model multi-currency subscription streams and hedging costs.

Component supply and logistics costs

Semiconductor lead times averaged about 20 weeks in 2024 and Drewry's World Container Index averaged near USD 1,600 per 40ft, pressuring delivery timelines and gross margins; design-to-cost and alternate-component qualification are essential for continuity. Buffer inventory and supplier diversification reduce stockout risk, and customers favor vendors that provide reliable ETAs for critical rollouts.

- Lead times ~20 weeks (2024)

- Freight ~USD 1,600/40ft (Drewry WCI 2024)

- Buffer inventory + supplier diversification

- Reliable ETAs win critical-rollout business

Consolidation and competitive pricing

Networking remains intensely competitive with hyperscaler adjacency and large incumbents; Extreme Networks reported fiscal 2024 revenue of $1.06 billion, forcing price-to-value positioning and TCO/cloud ops savings to drive win rates. M&A among partners or rivals can rapidly shift channel power, while differentiated services and SLAs help defend margins.

- Price-to-value: TCO/cloud ops drive wins

- M&A: channel power shifts

- Services/SLAs: margin defense

IIJA/BEAD and data localization push campus networks; 6 GHz/Wi-Fi7 timing critical

Macro growth and CIO budget sentiment drive refresh timing; >50% of CIOs signaled stable/rising networking budgets in 2024, aiding subscription growth. Fed funds ~5.25–5.50% in H1 2025 raise CAPEX hurdles while as-a-service options shorten cycles. FX and supply-chain (semiconductors ~20 weeks; Drewry WCI ~USD 1,600/40ft) affect revenue and margins; Extreme FY2024 revenue ~USD 1.06B.

| Metric | Value |

|---|---|

| FY2024 Revenue | USD 1.06B |

| Fed funds (H1 2025) | 5.25–5.50% |

| Semiconductor lead time (2024) | ~20 weeks |

| Drewry WCI (2024) | ~USD 1,600/40ft |

Preview Before You Purchase

Extreme Networks PESTLE Analysis

The preview shown here is the exact Extreme Networks PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed, with no placeholders or teasers. After checkout you’ll instantly download this exact file.

Skip the Research. Get the Strategy.

Our PESTLE Analysis for Extreme Networks reveals how political shifts, economic cycles, social trends, technological innovation, legal changes, and environmental pressures jointly shape its strategic outlook. It’s concise, evidence-based, and tailored for investors and strategists. Purchase the full report to access the complete, actionable breakdown and ready-to-use templates.

Political factors

Government IT spending and procurement

Public sector modernization and the IIJA broadband package (65 billion USD total, including the 42.45 billion USD BEAD program) drive demand for campus, K‑12 and municipal networks, shaping project pipelines. Extreme must navigate multi‑year budgeting and RFP‑driven procurement cycles while meeting Build America, Buy America and local content rules that can accelerate or block wins. Stable federal and state funding supports recurring cloud subscriptions via long‑term contracts tied to awarded grants.

Geopolitical trade and export controls

Tariffs, sanctions and export licensing raise hardware costs, constrain component sourcing and limit market access—U.S. tariffs on targeted ICT goods have reached up to 25% and the U.S. Entity List expanded to about 1,600 entries by 2024. Restrictions on advanced networking and encryption force product variants and can block sales in China and allied markets. Shifts in U.S.‑China relations are accelerating supply‑chain localization to ASEAN/onshore hubs; scenario planning and multi‑source BOMs mitigate disruption risk.

Domestic infrastructure and digital sovereignty

Rising digital sovereignty—with data localization rules now in 65+ countries—pushes demand for in-region cloud hosting, directly affecting Extreme’s cloud-managed platforms. Participation in national cloud marketplaces (public cloud market >$600B in 2024 per Gartner) can unlock enterprise and government contracts. Compliance often requires regional PoPs or partners; policy momentum favors vendors offering flexible onshore deployment models.

CERT, NIST, and critical infrastructure directives

CERT, NIST SP 800-207 (Zero Trust, 2020) and Executive Order 14028 (May 12, 2021) plus CISA directives push network segmentation, zero trust and continuous monitoring as federal baseline; DHS defines 16 critical infrastructure sectors that drive sectoral mandates in health, energy and transport. Extreme can map roadmaps to hardened configs and pursue certifications to capture regulated upgrade cycles and tender advantages.

- NIST SP 800-207 (2020) — zero trust baseline

- EO 14028 (May 12, 2021) — federal modernization driver

- 16 critical infrastructure sectors — sectoral mandates

- Cert wins → competitive edge in regulated tenders

Standards and spectrum policy

Decisions on 6 GHz and emerging 7 GHz allocations directly shape Extreme Networks wireless product roadmaps, since the FCC opened 1,200 MHz of 6 GHz for unlicensed use in 2020 and regulators differ by country. IEEE/IETF engagement matters: IEEE 802.11be (Wi‑Fi 7) was ratified in 2024, enabling theoretical PHY rates up to 46 Gbps, which drives interoperability and future-proofing.

- 6 GHz: 1,200 MHz opened in US (FCC, 2020)

- Wi‑Fi 7: 802.11be ratified 2024, up to 46 Gbps

- National spectrum variance → multiple SKUs and staggered launches

- Clear policy → faster enterprise adoption of high‑throughput WLAN

IIJA/BEAD and data localization push campus networks; 6 GHz/Wi-Fi7 timing critical

Federal IIJA funding ($65B, BEAD $42.45B) and stable grant cycles boost campus/municipal network demand while Build America, Buy America rules and tariffs (up to 25%) shape procurement and supply costs. Data localization (65+ countries) and cloud market scale (> $600B in 2024) force regional deployments. Spectrum (6 GHz 1,200 MHz) and Wi‑Fi7 (802.11be, 2024) drive product timing.

| Policy | Key figure |

|---|---|

| IIJA/BEAD | $65B / $42.45B |

| Tariffs/Entity List | Up to 25% / ~1,600 entries (2024) |

| Data localization | 65+ countries |

| Cloud market (2024) | >$600B |

| 6 GHz / Wi‑Fi7 | 1,200 MHz / 46 Gbps |

What is included in the product

Explores how macro-environmental factors across Political, Economic, Social, Technological, Environmental and Legal dimensions uniquely affect Extreme Networks; each section is backed by data and current trends, offers forward-looking insights and practical examples to support executives, investors and strategists in risk and opportunity planning.

Visually segmented by PESTEL categories, allowing for quick interpretation at a glance and effortless insertion into presentations or planning sessions to align teams rapidly.

Economic factors

Enterprise IT spending cycles

Macro growth and CIO budget sentiment drive campus and data-center refresh timing, with 2024 surveys showing more than half of CIOs signaling stable or rising networking budgets, accelerating refresh cycles. Cloud-managed OPEX models have proved more resilient during CAPEX freezes, supporting steady subscription growth for vendors like Extreme. Vertical exposure to education, healthcare and hospitality creates mixed cyclicality tied to public and travel spend patterns. Subscription attach and multi-year agreements have measurably improved pipeline visibility and revenue predictability for networking vendors.

Interest rates and capital costs

Higher policy rates—federal funds near 5.25–5.50% in H1 2025—raise customer CAPEX hurdles and vendor financing costs, lengthening sales cycles for large hardware deals. Extreme's growing as-a-service and leasing options reduce upfront barriers and expand deal sizes. Rate declines historically prompt deferred refresh waves that can boost demand. Treasury hedging and disciplined pricing help protect gross margins and cash flow.

FX volatility and global revenue mix

FX volatility can swing reported revenue for Extreme Networks—which posted about $1.2 billion revenue in FY2024—altering competitiveness versus local vendors when the dollar moves. Sourcing and manufacturing footprints in APAC and EMEA provide natural hedges by matching cost and sales currencies. Pricing localization and FX pass-through clauses reduce deal slippage. Financial planning must model multi-currency subscription streams and hedging costs.

Component supply and logistics costs

Semiconductor lead times averaged about 20 weeks in 2024 and Drewry's World Container Index averaged near USD 1,600 per 40ft, pressuring delivery timelines and gross margins; design-to-cost and alternate-component qualification are essential for continuity. Buffer inventory and supplier diversification reduce stockout risk, and customers favor vendors that provide reliable ETAs for critical rollouts.

- Lead times ~20 weeks (2024)

- Freight ~USD 1,600/40ft (Drewry WCI 2024)

- Buffer inventory + supplier diversification

- Reliable ETAs win critical-rollout business

Consolidation and competitive pricing

Networking remains intensely competitive with hyperscaler adjacency and large incumbents; Extreme Networks reported fiscal 2024 revenue of $1.06 billion, forcing price-to-value positioning and TCO/cloud ops savings to drive win rates. M&A among partners or rivals can rapidly shift channel power, while differentiated services and SLAs help defend margins.

- Price-to-value: TCO/cloud ops drive wins

- M&A: channel power shifts

- Services/SLAs: margin defense

IIJA/BEAD and data localization push campus networks; 6 GHz/Wi-Fi7 timing critical

Macro growth and CIO budget sentiment drive refresh timing; >50% of CIOs signaled stable/rising networking budgets in 2024, aiding subscription growth. Fed funds ~5.25–5.50% in H1 2025 raise CAPEX hurdles while as-a-service options shorten cycles. FX and supply-chain (semiconductors ~20 weeks; Drewry WCI ~USD 1,600/40ft) affect revenue and margins; Extreme FY2024 revenue ~USD 1.06B.

| Metric | Value |

|---|---|

| FY2024 Revenue | USD 1.06B |

| Fed funds (H1 2025) | 5.25–5.50% |

| Semiconductor lead time (2024) | ~20 weeks |

| Drewry WCI (2024) | ~USD 1,600/40ft |

Preview Before You Purchase

Extreme Networks PESTLE Analysis

The preview shown here is the exact Extreme Networks PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed, with no placeholders or teasers. After checkout you’ll instantly download this exact file.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Our PESTLE Analysis for Extreme Networks reveals how political shifts, economic cycles, social trends, technological innovation, legal changes, and environmental pressures jointly shape its strategic outlook. It’s concise, evidence-based, and tailored for investors and strategists. Purchase the full report to access the complete, actionable breakdown and ready-to-use templates.

Political factors

Government IT spending and procurement

Public sector modernization and the IIJA broadband package (65 billion USD total, including the 42.45 billion USD BEAD program) drive demand for campus, K‑12 and municipal networks, shaping project pipelines. Extreme must navigate multi‑year budgeting and RFP‑driven procurement cycles while meeting Build America, Buy America and local content rules that can accelerate or block wins. Stable federal and state funding supports recurring cloud subscriptions via long‑term contracts tied to awarded grants.

Geopolitical trade and export controls

Tariffs, sanctions and export licensing raise hardware costs, constrain component sourcing and limit market access—U.S. tariffs on targeted ICT goods have reached up to 25% and the U.S. Entity List expanded to about 1,600 entries by 2024. Restrictions on advanced networking and encryption force product variants and can block sales in China and allied markets. Shifts in U.S.‑China relations are accelerating supply‑chain localization to ASEAN/onshore hubs; scenario planning and multi‑source BOMs mitigate disruption risk.

Domestic infrastructure and digital sovereignty

Rising digital sovereignty—with data localization rules now in 65+ countries—pushes demand for in-region cloud hosting, directly affecting Extreme’s cloud-managed platforms. Participation in national cloud marketplaces (public cloud market >$600B in 2024 per Gartner) can unlock enterprise and government contracts. Compliance often requires regional PoPs or partners; policy momentum favors vendors offering flexible onshore deployment models.

CERT, NIST, and critical infrastructure directives

CERT, NIST SP 800-207 (Zero Trust, 2020) and Executive Order 14028 (May 12, 2021) plus CISA directives push network segmentation, zero trust and continuous monitoring as federal baseline; DHS defines 16 critical infrastructure sectors that drive sectoral mandates in health, energy and transport. Extreme can map roadmaps to hardened configs and pursue certifications to capture regulated upgrade cycles and tender advantages.

- NIST SP 800-207 (2020) — zero trust baseline

- EO 14028 (May 12, 2021) — federal modernization driver

- 16 critical infrastructure sectors — sectoral mandates

- Cert wins → competitive edge in regulated tenders

Standards and spectrum policy

Decisions on 6 GHz and emerging 7 GHz allocations directly shape Extreme Networks wireless product roadmaps, since the FCC opened 1,200 MHz of 6 GHz for unlicensed use in 2020 and regulators differ by country. IEEE/IETF engagement matters: IEEE 802.11be (Wi‑Fi 7) was ratified in 2024, enabling theoretical PHY rates up to 46 Gbps, which drives interoperability and future-proofing.

- 6 GHz: 1,200 MHz opened in US (FCC, 2020)

- Wi‑Fi 7: 802.11be ratified 2024, up to 46 Gbps

- National spectrum variance → multiple SKUs and staggered launches

- Clear policy → faster enterprise adoption of high‑throughput WLAN

IIJA/BEAD and data localization push campus networks; 6 GHz/Wi-Fi7 timing critical

Federal IIJA funding ($65B, BEAD $42.45B) and stable grant cycles boost campus/municipal network demand while Build America, Buy America rules and tariffs (up to 25%) shape procurement and supply costs. Data localization (65+ countries) and cloud market scale (> $600B in 2024) force regional deployments. Spectrum (6 GHz 1,200 MHz) and Wi‑Fi7 (802.11be, 2024) drive product timing.

| Policy | Key figure |

|---|---|

| IIJA/BEAD | $65B / $42.45B |

| Tariffs/Entity List | Up to 25% / ~1,600 entries (2024) |

| Data localization | 65+ countries |

| Cloud market (2024) | >$600B |

| 6 GHz / Wi‑Fi7 | 1,200 MHz / 46 Gbps |

What is included in the product

Explores how macro-environmental factors across Political, Economic, Social, Technological, Environmental and Legal dimensions uniquely affect Extreme Networks; each section is backed by data and current trends, offers forward-looking insights and practical examples to support executives, investors and strategists in risk and opportunity planning.

Visually segmented by PESTEL categories, allowing for quick interpretation at a glance and effortless insertion into presentations or planning sessions to align teams rapidly.

Economic factors

Enterprise IT spending cycles

Macro growth and CIO budget sentiment drive campus and data-center refresh timing, with 2024 surveys showing more than half of CIOs signaling stable or rising networking budgets, accelerating refresh cycles. Cloud-managed OPEX models have proved more resilient during CAPEX freezes, supporting steady subscription growth for vendors like Extreme. Vertical exposure to education, healthcare and hospitality creates mixed cyclicality tied to public and travel spend patterns. Subscription attach and multi-year agreements have measurably improved pipeline visibility and revenue predictability for networking vendors.

Interest rates and capital costs

Higher policy rates—federal funds near 5.25–5.50% in H1 2025—raise customer CAPEX hurdles and vendor financing costs, lengthening sales cycles for large hardware deals. Extreme's growing as-a-service and leasing options reduce upfront barriers and expand deal sizes. Rate declines historically prompt deferred refresh waves that can boost demand. Treasury hedging and disciplined pricing help protect gross margins and cash flow.

FX volatility and global revenue mix

FX volatility can swing reported revenue for Extreme Networks—which posted about $1.2 billion revenue in FY2024—altering competitiveness versus local vendors when the dollar moves. Sourcing and manufacturing footprints in APAC and EMEA provide natural hedges by matching cost and sales currencies. Pricing localization and FX pass-through clauses reduce deal slippage. Financial planning must model multi-currency subscription streams and hedging costs.

Component supply and logistics costs

Semiconductor lead times averaged about 20 weeks in 2024 and Drewry's World Container Index averaged near USD 1,600 per 40ft, pressuring delivery timelines and gross margins; design-to-cost and alternate-component qualification are essential for continuity. Buffer inventory and supplier diversification reduce stockout risk, and customers favor vendors that provide reliable ETAs for critical rollouts.

- Lead times ~20 weeks (2024)

- Freight ~USD 1,600/40ft (Drewry WCI 2024)

- Buffer inventory + supplier diversification

- Reliable ETAs win critical-rollout business

Consolidation and competitive pricing

Networking remains intensely competitive with hyperscaler adjacency and large incumbents; Extreme Networks reported fiscal 2024 revenue of $1.06 billion, forcing price-to-value positioning and TCO/cloud ops savings to drive win rates. M&A among partners or rivals can rapidly shift channel power, while differentiated services and SLAs help defend margins.

- Price-to-value: TCO/cloud ops drive wins

- M&A: channel power shifts

- Services/SLAs: margin defense

IIJA/BEAD and data localization push campus networks; 6 GHz/Wi-Fi7 timing critical

Macro growth and CIO budget sentiment drive refresh timing; >50% of CIOs signaled stable/rising networking budgets in 2024, aiding subscription growth. Fed funds ~5.25–5.50% in H1 2025 raise CAPEX hurdles while as-a-service options shorten cycles. FX and supply-chain (semiconductors ~20 weeks; Drewry WCI ~USD 1,600/40ft) affect revenue and margins; Extreme FY2024 revenue ~USD 1.06B.

| Metric | Value |

|---|---|

| FY2024 Revenue | USD 1.06B |

| Fed funds (H1 2025) | 5.25–5.50% |

| Semiconductor lead time (2024) | ~20 weeks |

| Drewry WCI (2024) | ~USD 1,600/40ft |

Preview Before You Purchase

Extreme Networks PESTLE Analysis

The preview shown here is the exact Extreme Networks PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed, with no placeholders or teasers. After checkout you’ll instantly download this exact file.