ExxonMobil PESTLE Analysis

Skip the Research. Get the Strategy.

Get decisive insight into how political regulation, energy markets, and sustainability trends are reshaping ExxonMobil's strategy and risk profile—our PESTLE distills the external forces you need to know. Ideal for investors and strategists, the full, ready-to-use report is available for instant download.

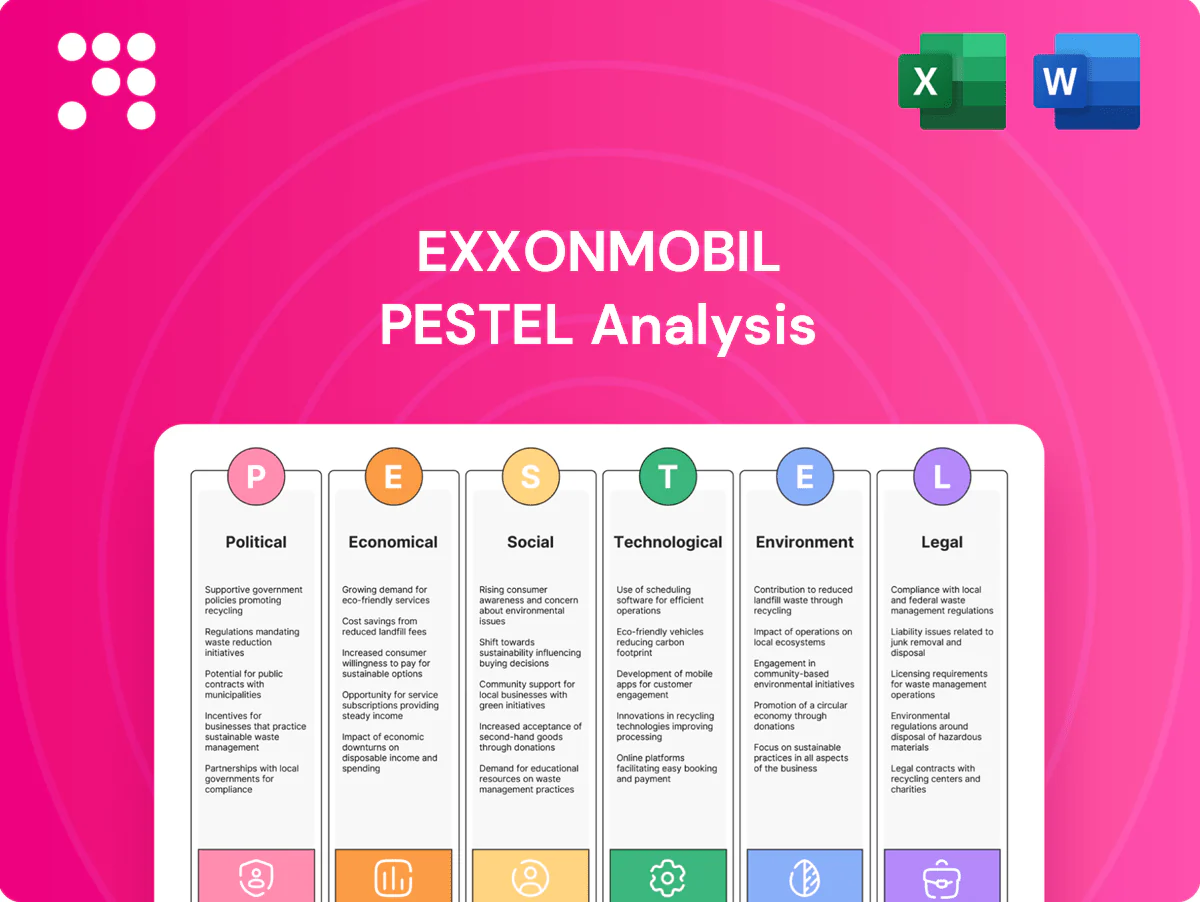

Political factors

Resource nationalism and sanctions

ExxonMobil’s upstream access is shaped by host-country politics, from licensing preferences to expropriation risk across operations in over 50 countries. Sanctions on Russia and Iran since 2022 have curtailed partner options and constrained projects, removing roughly 3–4 million b/d of seaborne crude capacity. OPEC+ moves and geopolitical tensions swing supply expectations by about 1–2 million b/d, affecting project timing and roughly $25–30 billion in annual upstream investment plans. Diversifying jurisdictions and strong compliance are central to resilience.

U.S. energy policy and election cycles

Federal permitting, leasing on public lands and pipeline approvals have swung with administrations, forcing ExxonMobil to adjust capital plans as regulatory windows open or close. The Inflation Reduction Act's roughly $369 billion for clean energy and tax credits can accelerate lower-emission investments, while budget shifts can stall them. Election outcomes materially affect EPA enforcement intensity and DOE program support, so ExxonMobil must scenario-plan for policy whiplash.

Trade policy and tariffs

Petrochemical exports face tariff exposure to Asia and Europe, pressuring margins on merchant sales and JV supply contracts. Changes in LNG export licensing and maritime rules—with the US the world s top LNG exporter since 2022—reshape market access and freight costs. EU carbon border adjustment measures move to full reporting by 2026, potentially altering competitiveness for refined products and chemicals. Supply-chain localization drives higher capex but strengthens security.

Global climate diplomacy and targets

Global climate diplomacy (Paris: 193 parties) drives national rules on methane (Global Methane Pledge: 30% cut by 2030), flaring and carbon pricing, pressuring ExxonMobil asset economics. COP decisions steer subsidy design for CCS and low-carbon fuels (US 45Q up to $85/t CO2; hydrogen tax credit up to $3/kg under IRA). Stricter NDCs can curb future oil demand growth while opening CCS, hydrogen and biofuel revenue streams; policy pace varies widely by region.

- 193 parties

- Methane −30% by 2030

- 45Q ≈ $85/t CO2

- H2 credit ≤ $3/kg

Local content and community politics

Host governments often mandate local content, training and procurement; as of 2024 more than 70 countries maintain formal local-content rules, forcing ExxonMobil to adapt sourcing and workforce plans. Municipal and state politics regularly delay pipelines and terminals through zoning and public consultations, while strong community engagement reduces opposition and schedule risk. Benefit-sharing frameworks are increasingly expected by regulators and communities.

- Local-content laws: >70 countries (2024)

- Community engagement: lowers protest-related delays

- Zoning/public consultation: common cause of 12+ month delays

- Benefit-sharing: growing regulatory expectation

Geopolitics, sanctions & OPEC+ swings slash seaborne supply, force $25-30bn/yr upstream reallocation

Host-country politics, sanctions (Russia/Iran) and OPEC+ swings (±1–2 m b/d) reshape upstream access and timing, cutting ~3–4 m b/d of seaborne capacity and altering ~$25–30bn p.a. upstream plans. US policy shifts (IRA $369bn, 45Q ≈ $85/t, H2 credit ≤ $3/kg) and permitting volatility force capital reallocation. Local-content rules (>70 countries, 2024), CBAM reporting by 2026 and methane −30% by 2030 raise compliance and capex needs.

| Metric | Value |

|---|---|

| Countries active | >50 |

| Seaborne capacity removed | 3–4 m b/d |

| Upstream capex impact | $25–30bn p.a. |

| Local-content laws (2024) | >70 countries |

What is included in the product

Explores how macro-environmental factors uniquely affect ExxonMobil across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities; designed for executives and investors to support scenario planning, strategy design and funding-ready reporting.

A concise, visually segmented ExxonMobil PESTLE summary that distills external risks and opportunities for quick reference in meetings, easily dropped into presentations or shared across teams for faster alignment.

Economic factors

Commodity price volatility

Earnings remain highly sensitive to Brent/WTI spreads (about $6/b in mid‑2025), Henry Hub near $3/MMBtu and USGC 3‑2‑1 crack spreads ≈ $13/b; OPEC+ voluntary cuts (~2.2 mb/d in recent rounds) plus geopolitical risk and shale’s quick quarterly response drive cycles. Hedging is more limited than pure E&Ps, raising cash‑flow variability, while capital discipline and diversified upstream, downstream and chemicals mix help buffer downturns.

Global demand and GDP cycles

Oil and chemicals volumes track industrial production, freight and mobility, with global GDP growth ~3.0% in 2024 and IMF projecting ~3.1% in 2025; China grew ~5.2% in 2024, supporting petrochemical demand. EM industrialization and aviation recovery (RPKs ~95–98% of 2019) lift volumes, while EVs (global new‑car EV share ~14% in 2024) and efficiency temper long‑run demand. ExxonMobil’s elastic capex (~$22–26B range in 2024 guidance) and phased projects align supply with these macro signals.

LNG and gas market dynamics

European re-gas demand climbed to about 130 bcm in 2023, while Asia (led by China and India) drove over half of 2024 LNG demand growth; long‑term SPAs still underpin roughly 70% of contracted volumes, stabilising economics. Seasonal volatility and Henry Hub vs TTF/JKM spreads (2024 averages ~HH $2.9/MMBtu, TTF $21, JKM $18) materially influence margins. U.S. export permitting and shipping capacity remain pivotal constraints, and gas’s role as a transition fuel supports medium‑term growth.

Capital markets and interest rates

Higher rates (US fed funds ~5.25–5.50% and 10y Treasury ~4.2% mid‑2025) lift WACC and hurdle rates, disadvantaging mega long‑cycle projects; shareholder pressure after ExxonMobil returned roughly $57bn in 2023 favors buybacks/dividends and high‑return brownfield over greenfield; green finance is easing for CCS/hydrogen; strong investment‑grade credit supports countercyclical spend.

- Higher rates → higher WACC/hurdles

- Shareholders → buybacks/dividends, brownfield

- Green finance improving for CCS/hydrogen

- Credit strength → enables countercyclical investment

Input costs and supply chains

Steel, labor and specialized-equipment inflation raised project costs ~10–15% in 2024 and extended timelines; logistics bottlenecks and limited vessel availability kept freight rates elevated (container rates up ~20% y/y in 2024), constraining exports. U.S. NGL feedstock advantaged chemicals margins versus naphtha in 2024, while supplier diversification and long-term contracts reduced input-price volatility.

- steel:+10–15% 2024

- freight:+20% y/y 2024

- U.S. NGLs:chemicals margin edge 2024

- hedges:long-term contracts diversify suppliers

Geopolitics, sanctions & OPEC+ swings slash seaborne supply, force $25-30bn/yr upstream reallocation

Earnings sensitive to Brent/WTI (~$6/b mid‑2025), Henry Hub ~$3/MMBtu and USGC crack ≈$13/b; capex ~$22–26B (2024 guidance) and diversified mix buffer cycles. Global GDP ~3.1% (IMF 2025), China growth ~5.2% (2024) support petrochemicals; higher rates (10y ~4.2% mid‑2025) raise WACC, favoring buybacks/brownfield.

| Metric | Value |

|---|---|

| Brent/WTI spread | $6/b |

| Henry Hub | $3/MMBtu |

| Capex (2024) | $22–26B |

| 10y Treasury | ~4.2% |

Full Version Awaits

ExxonMobil PESTLE Analysis

This ExxonMobil PESTLE analysis delivers a concise review of political, economic, social, technological, legal, and environmental factors affecting the company and industry, helping inform strategic and investment decisions. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; what you see is the final, downloadable file.

Skip the Research. Get the Strategy.

Get decisive insight into how political regulation, energy markets, and sustainability trends are reshaping ExxonMobil's strategy and risk profile—our PESTLE distills the external forces you need to know. Ideal for investors and strategists, the full, ready-to-use report is available for instant download.

Political factors

Resource nationalism and sanctions

ExxonMobil’s upstream access is shaped by host-country politics, from licensing preferences to expropriation risk across operations in over 50 countries. Sanctions on Russia and Iran since 2022 have curtailed partner options and constrained projects, removing roughly 3–4 million b/d of seaborne crude capacity. OPEC+ moves and geopolitical tensions swing supply expectations by about 1–2 million b/d, affecting project timing and roughly $25–30 billion in annual upstream investment plans. Diversifying jurisdictions and strong compliance are central to resilience.

U.S. energy policy and election cycles

Federal permitting, leasing on public lands and pipeline approvals have swung with administrations, forcing ExxonMobil to adjust capital plans as regulatory windows open or close. The Inflation Reduction Act's roughly $369 billion for clean energy and tax credits can accelerate lower-emission investments, while budget shifts can stall them. Election outcomes materially affect EPA enforcement intensity and DOE program support, so ExxonMobil must scenario-plan for policy whiplash.

Trade policy and tariffs

Petrochemical exports face tariff exposure to Asia and Europe, pressuring margins on merchant sales and JV supply contracts. Changes in LNG export licensing and maritime rules—with the US the world s top LNG exporter since 2022—reshape market access and freight costs. EU carbon border adjustment measures move to full reporting by 2026, potentially altering competitiveness for refined products and chemicals. Supply-chain localization drives higher capex but strengthens security.

Global climate diplomacy and targets

Global climate diplomacy (Paris: 193 parties) drives national rules on methane (Global Methane Pledge: 30% cut by 2030), flaring and carbon pricing, pressuring ExxonMobil asset economics. COP decisions steer subsidy design for CCS and low-carbon fuels (US 45Q up to $85/t CO2; hydrogen tax credit up to $3/kg under IRA). Stricter NDCs can curb future oil demand growth while opening CCS, hydrogen and biofuel revenue streams; policy pace varies widely by region.

- 193 parties

- Methane −30% by 2030

- 45Q ≈ $85/t CO2

- H2 credit ≤ $3/kg

Local content and community politics

Host governments often mandate local content, training and procurement; as of 2024 more than 70 countries maintain formal local-content rules, forcing ExxonMobil to adapt sourcing and workforce plans. Municipal and state politics regularly delay pipelines and terminals through zoning and public consultations, while strong community engagement reduces opposition and schedule risk. Benefit-sharing frameworks are increasingly expected by regulators and communities.

- Local-content laws: >70 countries (2024)

- Community engagement: lowers protest-related delays

- Zoning/public consultation: common cause of 12+ month delays

- Benefit-sharing: growing regulatory expectation

Geopolitics, sanctions & OPEC+ swings slash seaborne supply, force $25-30bn/yr upstream reallocation

Host-country politics, sanctions (Russia/Iran) and OPEC+ swings (±1–2 m b/d) reshape upstream access and timing, cutting ~3–4 m b/d of seaborne capacity and altering ~$25–30bn p.a. upstream plans. US policy shifts (IRA $369bn, 45Q ≈ $85/t, H2 credit ≤ $3/kg) and permitting volatility force capital reallocation. Local-content rules (>70 countries, 2024), CBAM reporting by 2026 and methane −30% by 2030 raise compliance and capex needs.

| Metric | Value |

|---|---|

| Countries active | >50 |

| Seaborne capacity removed | 3–4 m b/d |

| Upstream capex impact | $25–30bn p.a. |

| Local-content laws (2024) | >70 countries |

What is included in the product

Explores how macro-environmental factors uniquely affect ExxonMobil across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities; designed for executives and investors to support scenario planning, strategy design and funding-ready reporting.

A concise, visually segmented ExxonMobil PESTLE summary that distills external risks and opportunities for quick reference in meetings, easily dropped into presentations or shared across teams for faster alignment.

Economic factors

Commodity price volatility

Earnings remain highly sensitive to Brent/WTI spreads (about $6/b in mid‑2025), Henry Hub near $3/MMBtu and USGC 3‑2‑1 crack spreads ≈ $13/b; OPEC+ voluntary cuts (~2.2 mb/d in recent rounds) plus geopolitical risk and shale’s quick quarterly response drive cycles. Hedging is more limited than pure E&Ps, raising cash‑flow variability, while capital discipline and diversified upstream, downstream and chemicals mix help buffer downturns.

Global demand and GDP cycles

Oil and chemicals volumes track industrial production, freight and mobility, with global GDP growth ~3.0% in 2024 and IMF projecting ~3.1% in 2025; China grew ~5.2% in 2024, supporting petrochemical demand. EM industrialization and aviation recovery (RPKs ~95–98% of 2019) lift volumes, while EVs (global new‑car EV share ~14% in 2024) and efficiency temper long‑run demand. ExxonMobil’s elastic capex (~$22–26B range in 2024 guidance) and phased projects align supply with these macro signals.

LNG and gas market dynamics

European re-gas demand climbed to about 130 bcm in 2023, while Asia (led by China and India) drove over half of 2024 LNG demand growth; long‑term SPAs still underpin roughly 70% of contracted volumes, stabilising economics. Seasonal volatility and Henry Hub vs TTF/JKM spreads (2024 averages ~HH $2.9/MMBtu, TTF $21, JKM $18) materially influence margins. U.S. export permitting and shipping capacity remain pivotal constraints, and gas’s role as a transition fuel supports medium‑term growth.

Capital markets and interest rates

Higher rates (US fed funds ~5.25–5.50% and 10y Treasury ~4.2% mid‑2025) lift WACC and hurdle rates, disadvantaging mega long‑cycle projects; shareholder pressure after ExxonMobil returned roughly $57bn in 2023 favors buybacks/dividends and high‑return brownfield over greenfield; green finance is easing for CCS/hydrogen; strong investment‑grade credit supports countercyclical spend.

- Higher rates → higher WACC/hurdles

- Shareholders → buybacks/dividends, brownfield

- Green finance improving for CCS/hydrogen

- Credit strength → enables countercyclical investment

Input costs and supply chains

Steel, labor and specialized-equipment inflation raised project costs ~10–15% in 2024 and extended timelines; logistics bottlenecks and limited vessel availability kept freight rates elevated (container rates up ~20% y/y in 2024), constraining exports. U.S. NGL feedstock advantaged chemicals margins versus naphtha in 2024, while supplier diversification and long-term contracts reduced input-price volatility.

- steel:+10–15% 2024

- freight:+20% y/y 2024

- U.S. NGLs:chemicals margin edge 2024

- hedges:long-term contracts diversify suppliers

Geopolitics, sanctions & OPEC+ swings slash seaborne supply, force $25-30bn/yr upstream reallocation

Earnings sensitive to Brent/WTI (~$6/b mid‑2025), Henry Hub ~$3/MMBtu and USGC crack ≈$13/b; capex ~$22–26B (2024 guidance) and diversified mix buffer cycles. Global GDP ~3.1% (IMF 2025), China growth ~5.2% (2024) support petrochemicals; higher rates (10y ~4.2% mid‑2025) raise WACC, favoring buybacks/brownfield.

| Metric | Value |

|---|---|

| Brent/WTI spread | $6/b |

| Henry Hub | $3/MMBtu |

| Capex (2024) | $22–26B |

| 10y Treasury | ~4.2% |

Full Version Awaits

ExxonMobil PESTLE Analysis

This ExxonMobil PESTLE analysis delivers a concise review of political, economic, social, technological, legal, and environmental factors affecting the company and industry, helping inform strategic and investment decisions. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; what you see is the final, downloadable file.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Get decisive insight into how political regulation, energy markets, and sustainability trends are reshaping ExxonMobil's strategy and risk profile—our PESTLE distills the external forces you need to know. Ideal for investors and strategists, the full, ready-to-use report is available for instant download.

Political factors

Resource nationalism and sanctions

ExxonMobil’s upstream access is shaped by host-country politics, from licensing preferences to expropriation risk across operations in over 50 countries. Sanctions on Russia and Iran since 2022 have curtailed partner options and constrained projects, removing roughly 3–4 million b/d of seaborne crude capacity. OPEC+ moves and geopolitical tensions swing supply expectations by about 1–2 million b/d, affecting project timing and roughly $25–30 billion in annual upstream investment plans. Diversifying jurisdictions and strong compliance are central to resilience.

U.S. energy policy and election cycles

Federal permitting, leasing on public lands and pipeline approvals have swung with administrations, forcing ExxonMobil to adjust capital plans as regulatory windows open or close. The Inflation Reduction Act's roughly $369 billion for clean energy and tax credits can accelerate lower-emission investments, while budget shifts can stall them. Election outcomes materially affect EPA enforcement intensity and DOE program support, so ExxonMobil must scenario-plan for policy whiplash.

Trade policy and tariffs

Petrochemical exports face tariff exposure to Asia and Europe, pressuring margins on merchant sales and JV supply contracts. Changes in LNG export licensing and maritime rules—with the US the world s top LNG exporter since 2022—reshape market access and freight costs. EU carbon border adjustment measures move to full reporting by 2026, potentially altering competitiveness for refined products and chemicals. Supply-chain localization drives higher capex but strengthens security.

Global climate diplomacy and targets

Global climate diplomacy (Paris: 193 parties) drives national rules on methane (Global Methane Pledge: 30% cut by 2030), flaring and carbon pricing, pressuring ExxonMobil asset economics. COP decisions steer subsidy design for CCS and low-carbon fuels (US 45Q up to $85/t CO2; hydrogen tax credit up to $3/kg under IRA). Stricter NDCs can curb future oil demand growth while opening CCS, hydrogen and biofuel revenue streams; policy pace varies widely by region.

- 193 parties

- Methane −30% by 2030

- 45Q ≈ $85/t CO2

- H2 credit ≤ $3/kg

Local content and community politics

Host governments often mandate local content, training and procurement; as of 2024 more than 70 countries maintain formal local-content rules, forcing ExxonMobil to adapt sourcing and workforce plans. Municipal and state politics regularly delay pipelines and terminals through zoning and public consultations, while strong community engagement reduces opposition and schedule risk. Benefit-sharing frameworks are increasingly expected by regulators and communities.

- Local-content laws: >70 countries (2024)

- Community engagement: lowers protest-related delays

- Zoning/public consultation: common cause of 12+ month delays

- Benefit-sharing: growing regulatory expectation

Geopolitics, sanctions & OPEC+ swings slash seaborne supply, force $25-30bn/yr upstream reallocation

Host-country politics, sanctions (Russia/Iran) and OPEC+ swings (±1–2 m b/d) reshape upstream access and timing, cutting ~3–4 m b/d of seaborne capacity and altering ~$25–30bn p.a. upstream plans. US policy shifts (IRA $369bn, 45Q ≈ $85/t, H2 credit ≤ $3/kg) and permitting volatility force capital reallocation. Local-content rules (>70 countries, 2024), CBAM reporting by 2026 and methane −30% by 2030 raise compliance and capex needs.

| Metric | Value |

|---|---|

| Countries active | >50 |

| Seaborne capacity removed | 3–4 m b/d |

| Upstream capex impact | $25–30bn p.a. |

| Local-content laws (2024) | >70 countries |

What is included in the product

Explores how macro-environmental factors uniquely affect ExxonMobil across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities; designed for executives and investors to support scenario planning, strategy design and funding-ready reporting.

A concise, visually segmented ExxonMobil PESTLE summary that distills external risks and opportunities for quick reference in meetings, easily dropped into presentations or shared across teams for faster alignment.

Economic factors

Commodity price volatility

Earnings remain highly sensitive to Brent/WTI spreads (about $6/b in mid‑2025), Henry Hub near $3/MMBtu and USGC 3‑2‑1 crack spreads ≈ $13/b; OPEC+ voluntary cuts (~2.2 mb/d in recent rounds) plus geopolitical risk and shale’s quick quarterly response drive cycles. Hedging is more limited than pure E&Ps, raising cash‑flow variability, while capital discipline and diversified upstream, downstream and chemicals mix help buffer downturns.

Global demand and GDP cycles

Oil and chemicals volumes track industrial production, freight and mobility, with global GDP growth ~3.0% in 2024 and IMF projecting ~3.1% in 2025; China grew ~5.2% in 2024, supporting petrochemical demand. EM industrialization and aviation recovery (RPKs ~95–98% of 2019) lift volumes, while EVs (global new‑car EV share ~14% in 2024) and efficiency temper long‑run demand. ExxonMobil’s elastic capex (~$22–26B range in 2024 guidance) and phased projects align supply with these macro signals.

LNG and gas market dynamics

European re-gas demand climbed to about 130 bcm in 2023, while Asia (led by China and India) drove over half of 2024 LNG demand growth; long‑term SPAs still underpin roughly 70% of contracted volumes, stabilising economics. Seasonal volatility and Henry Hub vs TTF/JKM spreads (2024 averages ~HH $2.9/MMBtu, TTF $21, JKM $18) materially influence margins. U.S. export permitting and shipping capacity remain pivotal constraints, and gas’s role as a transition fuel supports medium‑term growth.

Capital markets and interest rates

Higher rates (US fed funds ~5.25–5.50% and 10y Treasury ~4.2% mid‑2025) lift WACC and hurdle rates, disadvantaging mega long‑cycle projects; shareholder pressure after ExxonMobil returned roughly $57bn in 2023 favors buybacks/dividends and high‑return brownfield over greenfield; green finance is easing for CCS/hydrogen; strong investment‑grade credit supports countercyclical spend.

- Higher rates → higher WACC/hurdles

- Shareholders → buybacks/dividends, brownfield

- Green finance improving for CCS/hydrogen

- Credit strength → enables countercyclical investment

Input costs and supply chains

Steel, labor and specialized-equipment inflation raised project costs ~10–15% in 2024 and extended timelines; logistics bottlenecks and limited vessel availability kept freight rates elevated (container rates up ~20% y/y in 2024), constraining exports. U.S. NGL feedstock advantaged chemicals margins versus naphtha in 2024, while supplier diversification and long-term contracts reduced input-price volatility.

- steel:+10–15% 2024

- freight:+20% y/y 2024

- U.S. NGLs:chemicals margin edge 2024

- hedges:long-term contracts diversify suppliers

Geopolitics, sanctions & OPEC+ swings slash seaborne supply, force $25-30bn/yr upstream reallocation

Earnings sensitive to Brent/WTI (~$6/b mid‑2025), Henry Hub ~$3/MMBtu and USGC crack ≈$13/b; capex ~$22–26B (2024 guidance) and diversified mix buffer cycles. Global GDP ~3.1% (IMF 2025), China growth ~5.2% (2024) support petrochemicals; higher rates (10y ~4.2% mid‑2025) raise WACC, favoring buybacks/brownfield.

| Metric | Value |

|---|---|

| Brent/WTI spread | $6/b |

| Henry Hub | $3/MMBtu |

| Capex (2024) | $22–26B |

| 10y Treasury | ~4.2% |

Full Version Awaits

ExxonMobil PESTLE Analysis

This ExxonMobil PESTLE analysis delivers a concise review of political, economic, social, technological, legal, and environmental factors affecting the company and industry, helping inform strategic and investment decisions. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; what you see is the final, downloadable file.