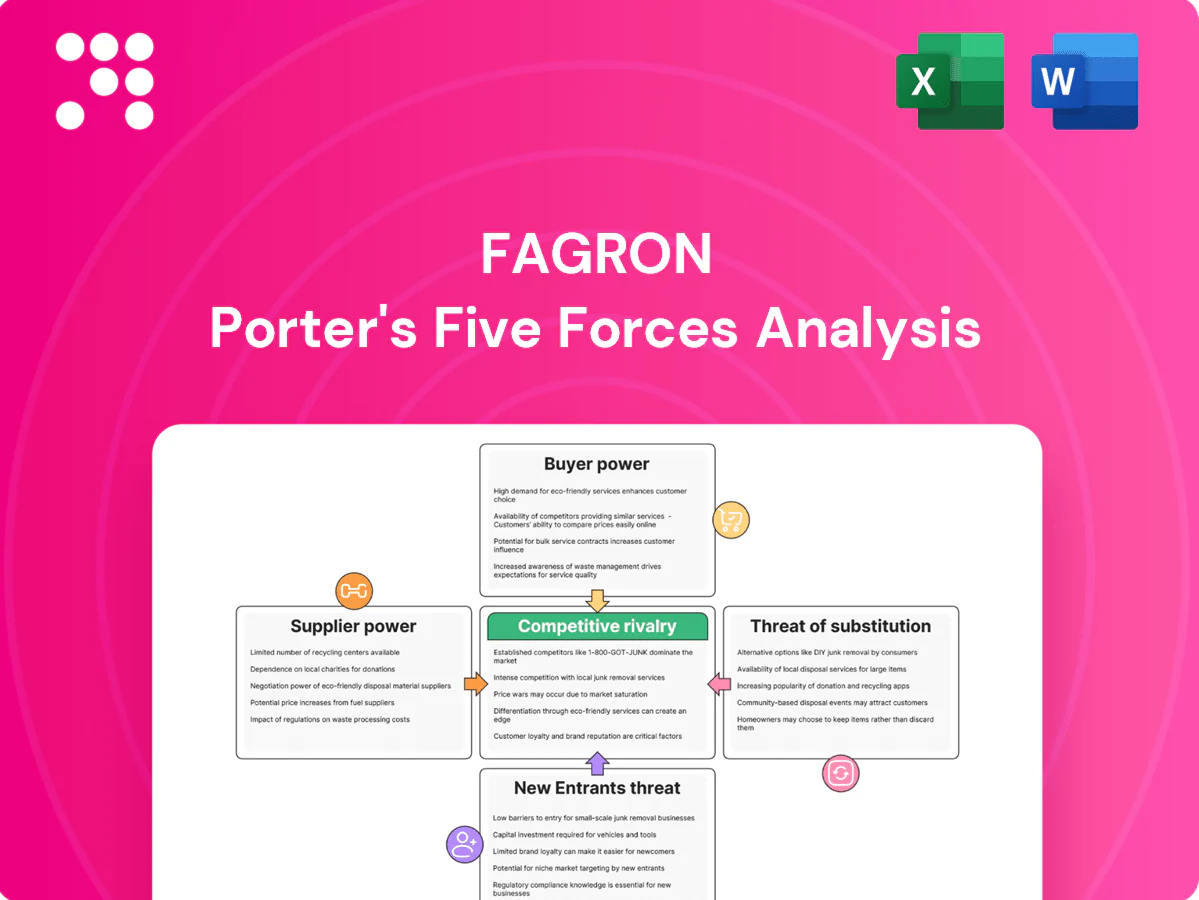

Fagron Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Fagron operates in specialized pharmaceutical compounding where supplier leverage, buyer sophistication, niche substitutes and regulatory barriers combine to shape intense competitive rivalry. This snapshot highlights key pressures but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a consultant-grade, data-driven breakdown to guide investment and strategy.

Suppliers Bargaining Power

Concentrated API and excipient sources

Many critical actives and specialty excipients originate from a concentrated base of GMP-certified producers—around 70–80% of key APIs are sourced from China and India as of 2024—elevating supplier leverage. Regulatory qualification further narrows usable suppliers, so any disruption can cascade into shortages. Fagron mitigates via multisourcing and stringent audits, but dependency remains nontrivial.

Regulatory-grade compliance requirements

Suppliers must meet FDA/EMA/ICH standards, raising switching costs and strengthening their bargaining position. Qualification, audits and validation cycles typically run 6–18 months with regulatory audits every 12–24 months, making rapid replacement during shortages difficult. This fosters reliance on a small pool of compliant suppliers. Long-term partnerships can temper price pressure but lock Fagron into lower flexibility and higher exit costs.

Supply chain volatility and geopolitics

Global shocks — pandemics, the Ukraine war and export controls — have periodically tightened API markets and logistics, pushing typical lead times to around 10–14 weeks in 2024 and driving scarcity premiums up to about 20%. Such volatility elevates supplier power as buyers face higher prices and longer waits. Buffer stocks and nearshoring mitigate risk but raised industry inventory days by roughly 15–25 days, increasing working-capital needs. Contract terms increasingly include escalation clauses to share price and supply risks.

Specialized equipment and packaging vendors

Specialized OEMs supply sterile packaging, analytical kits and compounding equipment for Fagron, creating few practical substitutes and strong supplier leverage. Certification and validation requirements deepen lock-in by raising switching costs and regulatory barriers. Service/maintenance contracts often include price escalators, while volume commitments can recover concessions but need significant scale.

- Few substitutes — high supplier power

- Certification raises switching costs

- Service contracts embed price escalators

- Volume commitments restore leverage if scale

Countervailing scale and reputation of Fagron

Fagron’s global scale, forecasting accuracy and quality reputation give it notable purchasing leverage: aggregated demand across 30+ countries (as of 2024) secures better pricing and priority allocation from suppliers, while data-sharing and vendor-managed inventory align incentives and reduce stock-outs.

- Global footprint: 30+ countries (2024)

- Leverage: aggregated regional demand improves terms

- Operational: VMI and data-sharing reduce supply friction

- Risk: scarce APIs can still give suppliers the edge

Supplier power high: 70–80% APIs China/India; lead times 10–14 weeks; scarcity premium ~20%

Supplier power is high: 70–80% of key APIs sourced from China/India (2024), regulatory qualification raises switching costs and lead times (10–14 weeks), and scarcity premiums reached ~20%. Fagron’s 30+ country scale, VMI and forecasting lower risk but cannot fully offset constrained supplier pools and certification-driven lock‑in.

| Metric | 2024 Value |

|---|---|

| API concentration (China/India) | 70–80% |

| Typical lead time | 10–14 weeks |

| Scarcity premium | ~20% |

| Inventory days increase | +15–25 days |

| Geographic footprint | 30+ countries |

What is included in the product

Concise Porter's Five Forces assessment for Fagron, detailing competitive rivalry, supplier and buyer bargaining power, threat of substitutes and new entrants, and highlighting disruptive trends and regulatory or scale barriers shaping its pricing power and profitability.

A concise one-sheet Porter's Five Forces summary for Fagron—instantly highlights competitive, supplier and regulatory pressures to simplify strategic decisions and investor briefings.

Customers Bargaining Power

Professional buyers and GPO dynamics

Hospital pharmacies, compounding centers and chains often buy via tenders or GPOs, increasing price sensitivity. In the US GPOs represent roughly 90% of hospital procurement, so volume concentration enables steep discount demands and transparent benchmarking intensifies negotiations. Fagron counters with bundled offerings and service differentiation to protect margins.

Moderate switching costs, high quality stakes

Switching suppliers is feasible but typically requires requalification, stability checks and documentation that can take weeks to months, raising transaction costs. Patient safety and audit-trail requirements increase perceived regulatory and clinical risk, so buyers hesitate to churn. Reliable QA/QC and traceability at Fagron-grade suppliers lower churn propensity and shift negotiations away from price-only decisions.

Breadth of portfolio and services

Fagron’s integrated offering of raw materials, formulations, equipment, QC support and education creates a one-stop value proposition that, as of 2024, supports operations in over 65 countries and strengthens customer reliance. Bundled services reduce buyer power by increasing switching costs and lowering procurement fragmentation. On-site technical support during inspections and tailored formulation solutions further lock in clients and raise customer stickiness.

Regulatory and compliance pressures on buyers

Buyers face stringent inspections and demand validated supply chains, tilting procurement toward suppliers with impeccable compliance records to minimize audit risk; this elevates total risk-adjusted value over lowest price and reduces pure cost-focused bargaining leverage.

- Compliance-first sourcing

- Validated supply chains

- Audit-risk reduction

- Weakened price-only leverage

Price sensitivity varies by reimbursement

Where compounded medicines lack robust reimbursement, buyers push harder on price, reducing margins; in 2024 markets with limited reimbursement saw ordering volatility for compounding suppliers. In reimbursed or critical-care niches, reliability and continuity outweigh minor cost differences, supporting premium pricing and contract wins. Urgent formulations (e.g., ICU parenterals) cut haggling latitude and favor suppliers with guaranteed lead times. Fagron can segment pricing by reimbursement status and urgency to protect margins and win tenders.

US GPOs (~90%) pressure prices; global QA, bundled services and urgency pricing protect margins

Customers wield moderate bargaining power: US hospital GPOs drive ~90% of procurement, forcing steep discounts, while switching is costly due to requalification and audit risk. Fagron’s 65+ country footprint (2024), bundled services and QA reduce price-only leverage and raise switching costs. In non-reimbursed markets 2024 ordering volatility reached ~20%, so targeted discounts and urgency pricing preserve margins.

| Metric | 2024 value |

|---|---|

| US hospital GPO procurement | ~90% |

| Fagron operations | 65+ countries |

| Ordering volatility (weak reimbursement) | ~20% |

Same Document Delivered

Fagron Porter's Five Forces Analysis

This preview shows the exact Fagron Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted and ready for download the moment you buy. It contains the complete, professional strategic assessment you can use right away.

Don't Miss the Bigger Picture

Fagron operates in specialized pharmaceutical compounding where supplier leverage, buyer sophistication, niche substitutes and regulatory barriers combine to shape intense competitive rivalry. This snapshot highlights key pressures but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a consultant-grade, data-driven breakdown to guide investment and strategy.

Suppliers Bargaining Power

Concentrated API and excipient sources

Many critical actives and specialty excipients originate from a concentrated base of GMP-certified producers—around 70–80% of key APIs are sourced from China and India as of 2024—elevating supplier leverage. Regulatory qualification further narrows usable suppliers, so any disruption can cascade into shortages. Fagron mitigates via multisourcing and stringent audits, but dependency remains nontrivial.

Regulatory-grade compliance requirements

Suppliers must meet FDA/EMA/ICH standards, raising switching costs and strengthening their bargaining position. Qualification, audits and validation cycles typically run 6–18 months with regulatory audits every 12–24 months, making rapid replacement during shortages difficult. This fosters reliance on a small pool of compliant suppliers. Long-term partnerships can temper price pressure but lock Fagron into lower flexibility and higher exit costs.

Supply chain volatility and geopolitics

Global shocks — pandemics, the Ukraine war and export controls — have periodically tightened API markets and logistics, pushing typical lead times to around 10–14 weeks in 2024 and driving scarcity premiums up to about 20%. Such volatility elevates supplier power as buyers face higher prices and longer waits. Buffer stocks and nearshoring mitigate risk but raised industry inventory days by roughly 15–25 days, increasing working-capital needs. Contract terms increasingly include escalation clauses to share price and supply risks.

Specialized equipment and packaging vendors

Specialized OEMs supply sterile packaging, analytical kits and compounding equipment for Fagron, creating few practical substitutes and strong supplier leverage. Certification and validation requirements deepen lock-in by raising switching costs and regulatory barriers. Service/maintenance contracts often include price escalators, while volume commitments can recover concessions but need significant scale.

- Few substitutes — high supplier power

- Certification raises switching costs

- Service contracts embed price escalators

- Volume commitments restore leverage if scale

Countervailing scale and reputation of Fagron

Fagron’s global scale, forecasting accuracy and quality reputation give it notable purchasing leverage: aggregated demand across 30+ countries (as of 2024) secures better pricing and priority allocation from suppliers, while data-sharing and vendor-managed inventory align incentives and reduce stock-outs.

- Global footprint: 30+ countries (2024)

- Leverage: aggregated regional demand improves terms

- Operational: VMI and data-sharing reduce supply friction

- Risk: scarce APIs can still give suppliers the edge

Supplier power high: 70–80% APIs China/India; lead times 10–14 weeks; scarcity premium ~20%

Supplier power is high: 70–80% of key APIs sourced from China/India (2024), regulatory qualification raises switching costs and lead times (10–14 weeks), and scarcity premiums reached ~20%. Fagron’s 30+ country scale, VMI and forecasting lower risk but cannot fully offset constrained supplier pools and certification-driven lock‑in.

| Metric | 2024 Value |

|---|---|

| API concentration (China/India) | 70–80% |

| Typical lead time | 10–14 weeks |

| Scarcity premium | ~20% |

| Inventory days increase | +15–25 days |

| Geographic footprint | 30+ countries |

What is included in the product

Concise Porter's Five Forces assessment for Fagron, detailing competitive rivalry, supplier and buyer bargaining power, threat of substitutes and new entrants, and highlighting disruptive trends and regulatory or scale barriers shaping its pricing power and profitability.

A concise one-sheet Porter's Five Forces summary for Fagron—instantly highlights competitive, supplier and regulatory pressures to simplify strategic decisions and investor briefings.

Customers Bargaining Power

Professional buyers and GPO dynamics

Hospital pharmacies, compounding centers and chains often buy via tenders or GPOs, increasing price sensitivity. In the US GPOs represent roughly 90% of hospital procurement, so volume concentration enables steep discount demands and transparent benchmarking intensifies negotiations. Fagron counters with bundled offerings and service differentiation to protect margins.

Moderate switching costs, high quality stakes

Switching suppliers is feasible but typically requires requalification, stability checks and documentation that can take weeks to months, raising transaction costs. Patient safety and audit-trail requirements increase perceived regulatory and clinical risk, so buyers hesitate to churn. Reliable QA/QC and traceability at Fagron-grade suppliers lower churn propensity and shift negotiations away from price-only decisions.

Breadth of portfolio and services

Fagron’s integrated offering of raw materials, formulations, equipment, QC support and education creates a one-stop value proposition that, as of 2024, supports operations in over 65 countries and strengthens customer reliance. Bundled services reduce buyer power by increasing switching costs and lowering procurement fragmentation. On-site technical support during inspections and tailored formulation solutions further lock in clients and raise customer stickiness.

Regulatory and compliance pressures on buyers

Buyers face stringent inspections and demand validated supply chains, tilting procurement toward suppliers with impeccable compliance records to minimize audit risk; this elevates total risk-adjusted value over lowest price and reduces pure cost-focused bargaining leverage.

- Compliance-first sourcing

- Validated supply chains

- Audit-risk reduction

- Weakened price-only leverage

Price sensitivity varies by reimbursement

Where compounded medicines lack robust reimbursement, buyers push harder on price, reducing margins; in 2024 markets with limited reimbursement saw ordering volatility for compounding suppliers. In reimbursed or critical-care niches, reliability and continuity outweigh minor cost differences, supporting premium pricing and contract wins. Urgent formulations (e.g., ICU parenterals) cut haggling latitude and favor suppliers with guaranteed lead times. Fagron can segment pricing by reimbursement status and urgency to protect margins and win tenders.

US GPOs (~90%) pressure prices; global QA, bundled services and urgency pricing protect margins

Customers wield moderate bargaining power: US hospital GPOs drive ~90% of procurement, forcing steep discounts, while switching is costly due to requalification and audit risk. Fagron’s 65+ country footprint (2024), bundled services and QA reduce price-only leverage and raise switching costs. In non-reimbursed markets 2024 ordering volatility reached ~20%, so targeted discounts and urgency pricing preserve margins.

| Metric | 2024 value |

|---|---|

| US hospital GPO procurement | ~90% |

| Fagron operations | 65+ countries |

| Ordering volatility (weak reimbursement) | ~20% |

Same Document Delivered

Fagron Porter's Five Forces Analysis

This preview shows the exact Fagron Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted and ready for download the moment you buy. It contains the complete, professional strategic assessment you can use right away.

Description

Don't Miss the Bigger Picture

Fagron operates in specialized pharmaceutical compounding where supplier leverage, buyer sophistication, niche substitutes and regulatory barriers combine to shape intense competitive rivalry. This snapshot highlights key pressures but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a consultant-grade, data-driven breakdown to guide investment and strategy.

Suppliers Bargaining Power

Concentrated API and excipient sources

Many critical actives and specialty excipients originate from a concentrated base of GMP-certified producers—around 70–80% of key APIs are sourced from China and India as of 2024—elevating supplier leverage. Regulatory qualification further narrows usable suppliers, so any disruption can cascade into shortages. Fagron mitigates via multisourcing and stringent audits, but dependency remains nontrivial.

Regulatory-grade compliance requirements

Suppliers must meet FDA/EMA/ICH standards, raising switching costs and strengthening their bargaining position. Qualification, audits and validation cycles typically run 6–18 months with regulatory audits every 12–24 months, making rapid replacement during shortages difficult. This fosters reliance on a small pool of compliant suppliers. Long-term partnerships can temper price pressure but lock Fagron into lower flexibility and higher exit costs.

Supply chain volatility and geopolitics

Global shocks — pandemics, the Ukraine war and export controls — have periodically tightened API markets and logistics, pushing typical lead times to around 10–14 weeks in 2024 and driving scarcity premiums up to about 20%. Such volatility elevates supplier power as buyers face higher prices and longer waits. Buffer stocks and nearshoring mitigate risk but raised industry inventory days by roughly 15–25 days, increasing working-capital needs. Contract terms increasingly include escalation clauses to share price and supply risks.

Specialized equipment and packaging vendors

Specialized OEMs supply sterile packaging, analytical kits and compounding equipment for Fagron, creating few practical substitutes and strong supplier leverage. Certification and validation requirements deepen lock-in by raising switching costs and regulatory barriers. Service/maintenance contracts often include price escalators, while volume commitments can recover concessions but need significant scale.

- Few substitutes — high supplier power

- Certification raises switching costs

- Service contracts embed price escalators

- Volume commitments restore leverage if scale

Countervailing scale and reputation of Fagron

Fagron’s global scale, forecasting accuracy and quality reputation give it notable purchasing leverage: aggregated demand across 30+ countries (as of 2024) secures better pricing and priority allocation from suppliers, while data-sharing and vendor-managed inventory align incentives and reduce stock-outs.

- Global footprint: 30+ countries (2024)

- Leverage: aggregated regional demand improves terms

- Operational: VMI and data-sharing reduce supply friction

- Risk: scarce APIs can still give suppliers the edge

Supplier power high: 70–80% APIs China/India; lead times 10–14 weeks; scarcity premium ~20%

Supplier power is high: 70–80% of key APIs sourced from China/India (2024), regulatory qualification raises switching costs and lead times (10–14 weeks), and scarcity premiums reached ~20%. Fagron’s 30+ country scale, VMI and forecasting lower risk but cannot fully offset constrained supplier pools and certification-driven lock‑in.

| Metric | 2024 Value |

|---|---|

| API concentration (China/India) | 70–80% |

| Typical lead time | 10–14 weeks |

| Scarcity premium | ~20% |

| Inventory days increase | +15–25 days |

| Geographic footprint | 30+ countries |

What is included in the product

Concise Porter's Five Forces assessment for Fagron, detailing competitive rivalry, supplier and buyer bargaining power, threat of substitutes and new entrants, and highlighting disruptive trends and regulatory or scale barriers shaping its pricing power and profitability.

A concise one-sheet Porter's Five Forces summary for Fagron—instantly highlights competitive, supplier and regulatory pressures to simplify strategic decisions and investor briefings.

Customers Bargaining Power

Professional buyers and GPO dynamics

Hospital pharmacies, compounding centers and chains often buy via tenders or GPOs, increasing price sensitivity. In the US GPOs represent roughly 90% of hospital procurement, so volume concentration enables steep discount demands and transparent benchmarking intensifies negotiations. Fagron counters with bundled offerings and service differentiation to protect margins.

Moderate switching costs, high quality stakes

Switching suppliers is feasible but typically requires requalification, stability checks and documentation that can take weeks to months, raising transaction costs. Patient safety and audit-trail requirements increase perceived regulatory and clinical risk, so buyers hesitate to churn. Reliable QA/QC and traceability at Fagron-grade suppliers lower churn propensity and shift negotiations away from price-only decisions.

Breadth of portfolio and services

Fagron’s integrated offering of raw materials, formulations, equipment, QC support and education creates a one-stop value proposition that, as of 2024, supports operations in over 65 countries and strengthens customer reliance. Bundled services reduce buyer power by increasing switching costs and lowering procurement fragmentation. On-site technical support during inspections and tailored formulation solutions further lock in clients and raise customer stickiness.

Regulatory and compliance pressures on buyers

Buyers face stringent inspections and demand validated supply chains, tilting procurement toward suppliers with impeccable compliance records to minimize audit risk; this elevates total risk-adjusted value over lowest price and reduces pure cost-focused bargaining leverage.

- Compliance-first sourcing

- Validated supply chains

- Audit-risk reduction

- Weakened price-only leverage

Price sensitivity varies by reimbursement

Where compounded medicines lack robust reimbursement, buyers push harder on price, reducing margins; in 2024 markets with limited reimbursement saw ordering volatility for compounding suppliers. In reimbursed or critical-care niches, reliability and continuity outweigh minor cost differences, supporting premium pricing and contract wins. Urgent formulations (e.g., ICU parenterals) cut haggling latitude and favor suppliers with guaranteed lead times. Fagron can segment pricing by reimbursement status and urgency to protect margins and win tenders.

US GPOs (~90%) pressure prices; global QA, bundled services and urgency pricing protect margins

Customers wield moderate bargaining power: US hospital GPOs drive ~90% of procurement, forcing steep discounts, while switching is costly due to requalification and audit risk. Fagron’s 65+ country footprint (2024), bundled services and QA reduce price-only leverage and raise switching costs. In non-reimbursed markets 2024 ordering volatility reached ~20%, so targeted discounts and urgency pricing preserve margins.

| Metric | 2024 value |

|---|---|

| US hospital GPO procurement | ~90% |

| Fagron operations | 65+ countries |

| Ordering volatility (weak reimbursement) | ~20% |

Same Document Delivered

Fagron Porter's Five Forces Analysis

This preview shows the exact Fagron Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted and ready for download the moment you buy. It contains the complete, professional strategic assessment you can use right away.