Farmer Brothers Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Farmer Brothers faces moderate buyer power, concentrated retail channels, rising private-label substitutes, and manageable supplier influence—factors shaping margin pressure and growth. This snapshot highlights competitive risks across entry barriers, rivalry, and substitute threats. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategies tailored to Farmer Brothers.

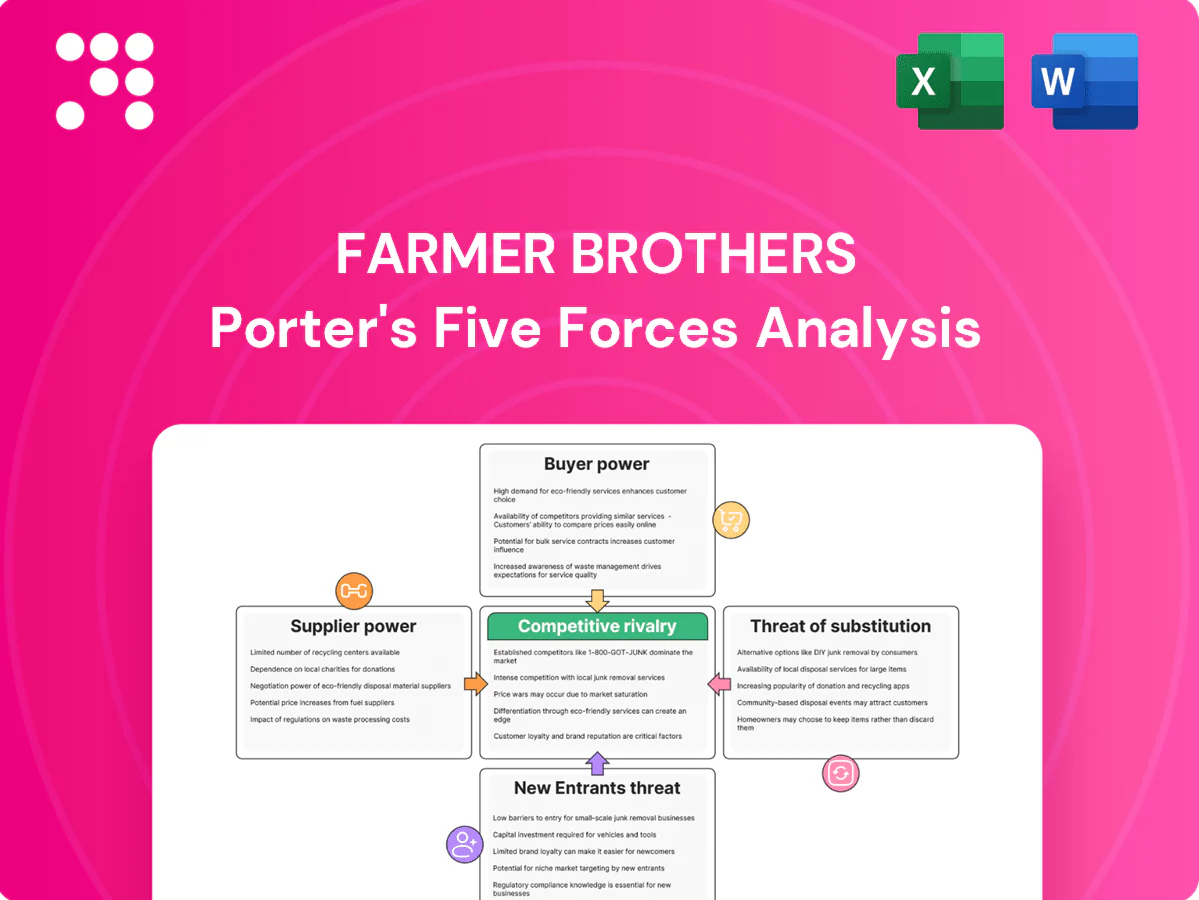

Suppliers Bargaining Power

Green bean origins

Global coffee is concentrated: Arabica accounts for about 60% of production, with Brazil ~37% of world output and Vietnam ~17% (mostly Robusta), exposing Farmer Brothers to weather, political risk, and crop disease shocks.

Producers and exporters can wield leverage during poor harvests; Farmer Brothers reports multi-origin sourcing and use of price hedging to mitigate, but input volatility still passes through to margins.

Certification demands such as Fair Trade and organic further constrict eligible supply and raise procurement costs.

Price volatility

Coffee futures and FX swings rapidly alter COGS, disrupting price lists and margin planning for Farmer Brothers. Suppliers tighten terms when markets spike, reducing leeway on lead times, payment and premiums. Long-dated contracts blunt spot shocks but create basis risk versus current prices. Frequent, systematic repricing with customers is required to preserve spread.

Specialty inputs

Premium microlots, flavors, and sustainable lines often come from niche vendors with limited capacity, giving suppliers stronger bargaining power as scarcity and brand halo allow price premiums; in 2024 specialty premiums averaged roughly 25% above commodity green-bean prices. Substituting beans risks diluting established blend profiles customers expect, eroding brand equity. Seasonal allocations during peak demand further tighten Farmer Brothers negotiating room.

Packaging and equipment

Packaging and equipment suppliers for bag films, valves, cans and OEM brewers/grinders are concentrated, giving suppliers elevated bargaining power; strict technical specs and food-safety certifications raise switching costs and validation time. Extended lead times and minimum order quantities force Farmer Brothers to carry inventory, while vendor consolidation tightens pricing leverage and service terms.

- Supplier concentration: smaller qualified pool

- Switching costs: certification and specs

- Inventory impact: long lead times, MOQs

- Pricing pressure: vendor consolidation

Logistics constraints

Logistics constraints raise supplier power as 2024 container rates (~$1,500 per FEU) and port congestion (multi-day berth delays) increase landed cost; domestic freight often adds 10–20% to finished coffee cost and tight markets let carriers push 2–8% surcharges, while coffee’s bulk volume and limited shelf-life reduce modal flexibility and delays directly degrade foodservice fill rates.

- Port congestion: multi-day delays

- Container rates: ≈ $1,500/FEU (2024)

- Domestic freight: +10–20% landed cost

- Surcharges: carriers add 2–8% in tight markets

Coffee supply: Brazil 37%, Vietnam 17% - freight squeezes margins

Farmer Brothers faces elevated supplier power: supply concentrated (Brazil ~37% of world coffee, Vietnam ~17%), specialty premiums ~25% above commodities (2024), and certification/shelf-life constraints raise switching costs. Packaging, equipment and carriers are consolidated; 2024 container rates ≈ $1,500/FEU and domestic freight adds 10–20% to landed cost, squeezing margins.

| Metric | Value (2024) |

|---|---|

| Brazil share | ~37% |

| Vietnam share | ~17% |

| Specialty premium | ~25% above commodity |

| Container rate | ≈ $1,500/FEU |

| Domestic freight impact | +10–20% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and market entry risks tailored to Farmer Brothers’ coffee and foodservice position, identifying disruptive substitutes and strategic levers that influence pricing and profitability.

One-sheet Porter’s Five Forces for Farmer Brothers—instantly visualize competitive pressure with a customizable radar chart and editable ratings to relieve analysis bottlenecks for decks, reports, or scenario comparisons.

Customers Bargaining Power

Large institutional buyers

Chains, hospitality groups and distributors buy at scale from Farmer Brothers, demanding sharp pricing and negotiating rebates, private-label programs and service SLAs; in 2024 large accounts accounted for an estimated majority of commercial volumes.

Their ability to dual-source raises switching risk and price pressure, with major customers leveraging national contracts to secure 5–10% lower unit costs.

Losing a single national account can materially dent route density and plant utilization, often reducing utilization by roughly 10–20% in comparable foodservice roaster scenarios.

Fragmented independents

Independent restaurants—part of roughly 1 million U.S. restaurant locations in 2024—are numerous and highly price sensitive, giving buyers bargaining leverage. Switching roasters is relatively easy when equipment tie-ins are weak, increasing churn risk for national suppliers. Reliable service, staff training and consistent delivery can mitigate price pressure by raising perceived switching costs. The rise of local craft roasters expands high-end alternatives, intensifying competition.

Low switching costs

Low switching costs amplify customer bargaining: coffee SKUs are highly substitutable and many buyers show only subtle blind-taste differentiation, raising churn risk when equipment is owner-operated or generic. Contracts and loaned machines improve retention but force Farmer Brothers to deploy capital to defend accounts. Free trials and on-site demos materially ease supplier changes by lowering buyer switching barriers.

Demand for value-add

Buyers push Farmer Brothers to bundle equipment, maintenance and barista training, shifting negotiations from bean price to total cost of ownership; strong service can support premiums but service failures force rebates or price concessions. Custom blends and menu support deepen dependency while raising SLA and quality expectations, with 62% of US adults drinking coffee daily (NCA 2024).

- Bundled contracts drive recurring revenue but increase delivery risk

- Service quality justifies premiums; failures trigger concessions

- Custom blends increase stickiness and service requirements

Transparency and private label

Benchmarking via market prices and cupping has reduced information asymmetry, letting buyers compare Farmer Brothers offerings directly to ICE Arabica benchmarks and spot market quotes.

Many commercial customers pursue private label or house blends to capture margin, frequently re-bidding specifications and using data-driven procurement to compress spreads over green-bean costs.

As a result, customer bargaining power rises, pressuring Farmer Brothers on pricing, specification flexibility, and margin protection.

- Benchmarking: market-price and cupping transparency

- Private label: customers seeking margin capture

- Re-bids: frequent specification bidding

- Data procurement: tighter spreads vs green costs

60% of volumes come from national accounts demanding 5–10% cuts

Large national accounts drove an estimated 60% of Farmer Brothers commercial volumes in 2024, extracting typical price concessions of 5–10% via national contracts.

Low switching costs, private-label programs and benchmarking to ICE Arabica heightened buyer leverage and frequent re-bids compressed spreads to green-bean costs.

Bundled equipment, service and custom blends can raise retention but require capex and, if lost, can cut plant utilization roughly 10–20%.

| Metric | 2024 Value |

|---|---|

| Large account share (vol) | ~60% |

| Typical price concession | 5–10% |

| Utilization loss if account lost | 10–20% |

| US adults daily coffee | 62% |

Same Document Delivered

Farmer Brothers Porter's Five Forces Analysis

This preview shows the exact Farmer Brothers Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, comprehensive, and ready to use. It covers supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with data-driven insights and strategic implications. No placeholders or samples; purchase grants instant access to this identical final document.

A Must-Have Tool for Decision-Makers

Farmer Brothers faces moderate buyer power, concentrated retail channels, rising private-label substitutes, and manageable supplier influence—factors shaping margin pressure and growth. This snapshot highlights competitive risks across entry barriers, rivalry, and substitute threats. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategies tailored to Farmer Brothers.

Suppliers Bargaining Power

Green bean origins

Global coffee is concentrated: Arabica accounts for about 60% of production, with Brazil ~37% of world output and Vietnam ~17% (mostly Robusta), exposing Farmer Brothers to weather, political risk, and crop disease shocks.

Producers and exporters can wield leverage during poor harvests; Farmer Brothers reports multi-origin sourcing and use of price hedging to mitigate, but input volatility still passes through to margins.

Certification demands such as Fair Trade and organic further constrict eligible supply and raise procurement costs.

Price volatility

Coffee futures and FX swings rapidly alter COGS, disrupting price lists and margin planning for Farmer Brothers. Suppliers tighten terms when markets spike, reducing leeway on lead times, payment and premiums. Long-dated contracts blunt spot shocks but create basis risk versus current prices. Frequent, systematic repricing with customers is required to preserve spread.

Specialty inputs

Premium microlots, flavors, and sustainable lines often come from niche vendors with limited capacity, giving suppliers stronger bargaining power as scarcity and brand halo allow price premiums; in 2024 specialty premiums averaged roughly 25% above commodity green-bean prices. Substituting beans risks diluting established blend profiles customers expect, eroding brand equity. Seasonal allocations during peak demand further tighten Farmer Brothers negotiating room.

Packaging and equipment

Packaging and equipment suppliers for bag films, valves, cans and OEM brewers/grinders are concentrated, giving suppliers elevated bargaining power; strict technical specs and food-safety certifications raise switching costs and validation time. Extended lead times and minimum order quantities force Farmer Brothers to carry inventory, while vendor consolidation tightens pricing leverage and service terms.

- Supplier concentration: smaller qualified pool

- Switching costs: certification and specs

- Inventory impact: long lead times, MOQs

- Pricing pressure: vendor consolidation

Logistics constraints

Logistics constraints raise supplier power as 2024 container rates (~$1,500 per FEU) and port congestion (multi-day berth delays) increase landed cost; domestic freight often adds 10–20% to finished coffee cost and tight markets let carriers push 2–8% surcharges, while coffee’s bulk volume and limited shelf-life reduce modal flexibility and delays directly degrade foodservice fill rates.

- Port congestion: multi-day delays

- Container rates: ≈ $1,500/FEU (2024)

- Domestic freight: +10–20% landed cost

- Surcharges: carriers add 2–8% in tight markets

Coffee supply: Brazil 37%, Vietnam 17% - freight squeezes margins

Farmer Brothers faces elevated supplier power: supply concentrated (Brazil ~37% of world coffee, Vietnam ~17%), specialty premiums ~25% above commodities (2024), and certification/shelf-life constraints raise switching costs. Packaging, equipment and carriers are consolidated; 2024 container rates ≈ $1,500/FEU and domestic freight adds 10–20% to landed cost, squeezing margins.

| Metric | Value (2024) |

|---|---|

| Brazil share | ~37% |

| Vietnam share | ~17% |

| Specialty premium | ~25% above commodity |

| Container rate | ≈ $1,500/FEU |

| Domestic freight impact | +10–20% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and market entry risks tailored to Farmer Brothers’ coffee and foodservice position, identifying disruptive substitutes and strategic levers that influence pricing and profitability.

One-sheet Porter’s Five Forces for Farmer Brothers—instantly visualize competitive pressure with a customizable radar chart and editable ratings to relieve analysis bottlenecks for decks, reports, or scenario comparisons.

Customers Bargaining Power

Large institutional buyers

Chains, hospitality groups and distributors buy at scale from Farmer Brothers, demanding sharp pricing and negotiating rebates, private-label programs and service SLAs; in 2024 large accounts accounted for an estimated majority of commercial volumes.

Their ability to dual-source raises switching risk and price pressure, with major customers leveraging national contracts to secure 5–10% lower unit costs.

Losing a single national account can materially dent route density and plant utilization, often reducing utilization by roughly 10–20% in comparable foodservice roaster scenarios.

Fragmented independents

Independent restaurants—part of roughly 1 million U.S. restaurant locations in 2024—are numerous and highly price sensitive, giving buyers bargaining leverage. Switching roasters is relatively easy when equipment tie-ins are weak, increasing churn risk for national suppliers. Reliable service, staff training and consistent delivery can mitigate price pressure by raising perceived switching costs. The rise of local craft roasters expands high-end alternatives, intensifying competition.

Low switching costs

Low switching costs amplify customer bargaining: coffee SKUs are highly substitutable and many buyers show only subtle blind-taste differentiation, raising churn risk when equipment is owner-operated or generic. Contracts and loaned machines improve retention but force Farmer Brothers to deploy capital to defend accounts. Free trials and on-site demos materially ease supplier changes by lowering buyer switching barriers.

Demand for value-add

Buyers push Farmer Brothers to bundle equipment, maintenance and barista training, shifting negotiations from bean price to total cost of ownership; strong service can support premiums but service failures force rebates or price concessions. Custom blends and menu support deepen dependency while raising SLA and quality expectations, with 62% of US adults drinking coffee daily (NCA 2024).

- Bundled contracts drive recurring revenue but increase delivery risk

- Service quality justifies premiums; failures trigger concessions

- Custom blends increase stickiness and service requirements

Transparency and private label

Benchmarking via market prices and cupping has reduced information asymmetry, letting buyers compare Farmer Brothers offerings directly to ICE Arabica benchmarks and spot market quotes.

Many commercial customers pursue private label or house blends to capture margin, frequently re-bidding specifications and using data-driven procurement to compress spreads over green-bean costs.

As a result, customer bargaining power rises, pressuring Farmer Brothers on pricing, specification flexibility, and margin protection.

- Benchmarking: market-price and cupping transparency

- Private label: customers seeking margin capture

- Re-bids: frequent specification bidding

- Data procurement: tighter spreads vs green costs

60% of volumes come from national accounts demanding 5–10% cuts

Large national accounts drove an estimated 60% of Farmer Brothers commercial volumes in 2024, extracting typical price concessions of 5–10% via national contracts.

Low switching costs, private-label programs and benchmarking to ICE Arabica heightened buyer leverage and frequent re-bids compressed spreads to green-bean costs.

Bundled equipment, service and custom blends can raise retention but require capex and, if lost, can cut plant utilization roughly 10–20%.

| Metric | 2024 Value |

|---|---|

| Large account share (vol) | ~60% |

| Typical price concession | 5–10% |

| Utilization loss if account lost | 10–20% |

| US adults daily coffee | 62% |

Same Document Delivered

Farmer Brothers Porter's Five Forces Analysis

This preview shows the exact Farmer Brothers Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, comprehensive, and ready to use. It covers supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with data-driven insights and strategic implications. No placeholders or samples; purchase grants instant access to this identical final document.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Farmer Brothers faces moderate buyer power, concentrated retail channels, rising private-label substitutes, and manageable supplier influence—factors shaping margin pressure and growth. This snapshot highlights competitive risks across entry barriers, rivalry, and substitute threats. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategies tailored to Farmer Brothers.

Suppliers Bargaining Power

Green bean origins

Global coffee is concentrated: Arabica accounts for about 60% of production, with Brazil ~37% of world output and Vietnam ~17% (mostly Robusta), exposing Farmer Brothers to weather, political risk, and crop disease shocks.

Producers and exporters can wield leverage during poor harvests; Farmer Brothers reports multi-origin sourcing and use of price hedging to mitigate, but input volatility still passes through to margins.

Certification demands such as Fair Trade and organic further constrict eligible supply and raise procurement costs.

Price volatility

Coffee futures and FX swings rapidly alter COGS, disrupting price lists and margin planning for Farmer Brothers. Suppliers tighten terms when markets spike, reducing leeway on lead times, payment and premiums. Long-dated contracts blunt spot shocks but create basis risk versus current prices. Frequent, systematic repricing with customers is required to preserve spread.

Specialty inputs

Premium microlots, flavors, and sustainable lines often come from niche vendors with limited capacity, giving suppliers stronger bargaining power as scarcity and brand halo allow price premiums; in 2024 specialty premiums averaged roughly 25% above commodity green-bean prices. Substituting beans risks diluting established blend profiles customers expect, eroding brand equity. Seasonal allocations during peak demand further tighten Farmer Brothers negotiating room.

Packaging and equipment

Packaging and equipment suppliers for bag films, valves, cans and OEM brewers/grinders are concentrated, giving suppliers elevated bargaining power; strict technical specs and food-safety certifications raise switching costs and validation time. Extended lead times and minimum order quantities force Farmer Brothers to carry inventory, while vendor consolidation tightens pricing leverage and service terms.

- Supplier concentration: smaller qualified pool

- Switching costs: certification and specs

- Inventory impact: long lead times, MOQs

- Pricing pressure: vendor consolidation

Logistics constraints

Logistics constraints raise supplier power as 2024 container rates (~$1,500 per FEU) and port congestion (multi-day berth delays) increase landed cost; domestic freight often adds 10–20% to finished coffee cost and tight markets let carriers push 2–8% surcharges, while coffee’s bulk volume and limited shelf-life reduce modal flexibility and delays directly degrade foodservice fill rates.

- Port congestion: multi-day delays

- Container rates: ≈ $1,500/FEU (2024)

- Domestic freight: +10–20% landed cost

- Surcharges: carriers add 2–8% in tight markets

Coffee supply: Brazil 37%, Vietnam 17% - freight squeezes margins

Farmer Brothers faces elevated supplier power: supply concentrated (Brazil ~37% of world coffee, Vietnam ~17%), specialty premiums ~25% above commodities (2024), and certification/shelf-life constraints raise switching costs. Packaging, equipment and carriers are consolidated; 2024 container rates ≈ $1,500/FEU and domestic freight adds 10–20% to landed cost, squeezing margins.

| Metric | Value (2024) |

|---|---|

| Brazil share | ~37% |

| Vietnam share | ~17% |

| Specialty premium | ~25% above commodity |

| Container rate | ≈ $1,500/FEU |

| Domestic freight impact | +10–20% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and market entry risks tailored to Farmer Brothers’ coffee and foodservice position, identifying disruptive substitutes and strategic levers that influence pricing and profitability.

One-sheet Porter’s Five Forces for Farmer Brothers—instantly visualize competitive pressure with a customizable radar chart and editable ratings to relieve analysis bottlenecks for decks, reports, or scenario comparisons.

Customers Bargaining Power

Large institutional buyers

Chains, hospitality groups and distributors buy at scale from Farmer Brothers, demanding sharp pricing and negotiating rebates, private-label programs and service SLAs; in 2024 large accounts accounted for an estimated majority of commercial volumes.

Their ability to dual-source raises switching risk and price pressure, with major customers leveraging national contracts to secure 5–10% lower unit costs.

Losing a single national account can materially dent route density and plant utilization, often reducing utilization by roughly 10–20% in comparable foodservice roaster scenarios.

Fragmented independents

Independent restaurants—part of roughly 1 million U.S. restaurant locations in 2024—are numerous and highly price sensitive, giving buyers bargaining leverage. Switching roasters is relatively easy when equipment tie-ins are weak, increasing churn risk for national suppliers. Reliable service, staff training and consistent delivery can mitigate price pressure by raising perceived switching costs. The rise of local craft roasters expands high-end alternatives, intensifying competition.

Low switching costs

Low switching costs amplify customer bargaining: coffee SKUs are highly substitutable and many buyers show only subtle blind-taste differentiation, raising churn risk when equipment is owner-operated or generic. Contracts and loaned machines improve retention but force Farmer Brothers to deploy capital to defend accounts. Free trials and on-site demos materially ease supplier changes by lowering buyer switching barriers.

Demand for value-add

Buyers push Farmer Brothers to bundle equipment, maintenance and barista training, shifting negotiations from bean price to total cost of ownership; strong service can support premiums but service failures force rebates or price concessions. Custom blends and menu support deepen dependency while raising SLA and quality expectations, with 62% of US adults drinking coffee daily (NCA 2024).

- Bundled contracts drive recurring revenue but increase delivery risk

- Service quality justifies premiums; failures trigger concessions

- Custom blends increase stickiness and service requirements

Transparency and private label

Benchmarking via market prices and cupping has reduced information asymmetry, letting buyers compare Farmer Brothers offerings directly to ICE Arabica benchmarks and spot market quotes.

Many commercial customers pursue private label or house blends to capture margin, frequently re-bidding specifications and using data-driven procurement to compress spreads over green-bean costs.

As a result, customer bargaining power rises, pressuring Farmer Brothers on pricing, specification flexibility, and margin protection.

- Benchmarking: market-price and cupping transparency

- Private label: customers seeking margin capture

- Re-bids: frequent specification bidding

- Data procurement: tighter spreads vs green costs

60% of volumes come from national accounts demanding 5–10% cuts

Large national accounts drove an estimated 60% of Farmer Brothers commercial volumes in 2024, extracting typical price concessions of 5–10% via national contracts.

Low switching costs, private-label programs and benchmarking to ICE Arabica heightened buyer leverage and frequent re-bids compressed spreads to green-bean costs.

Bundled equipment, service and custom blends can raise retention but require capex and, if lost, can cut plant utilization roughly 10–20%.

| Metric | 2024 Value |

|---|---|

| Large account share (vol) | ~60% |

| Typical price concession | 5–10% |

| Utilization loss if account lost | 10–20% |

| US adults daily coffee | 62% |

Same Document Delivered

Farmer Brothers Porter's Five Forces Analysis

This preview shows the exact Farmer Brothers Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, comprehensive, and ready to use. It covers supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with data-driven insights and strategic implications. No placeholders or samples; purchase grants instant access to this identical final document.