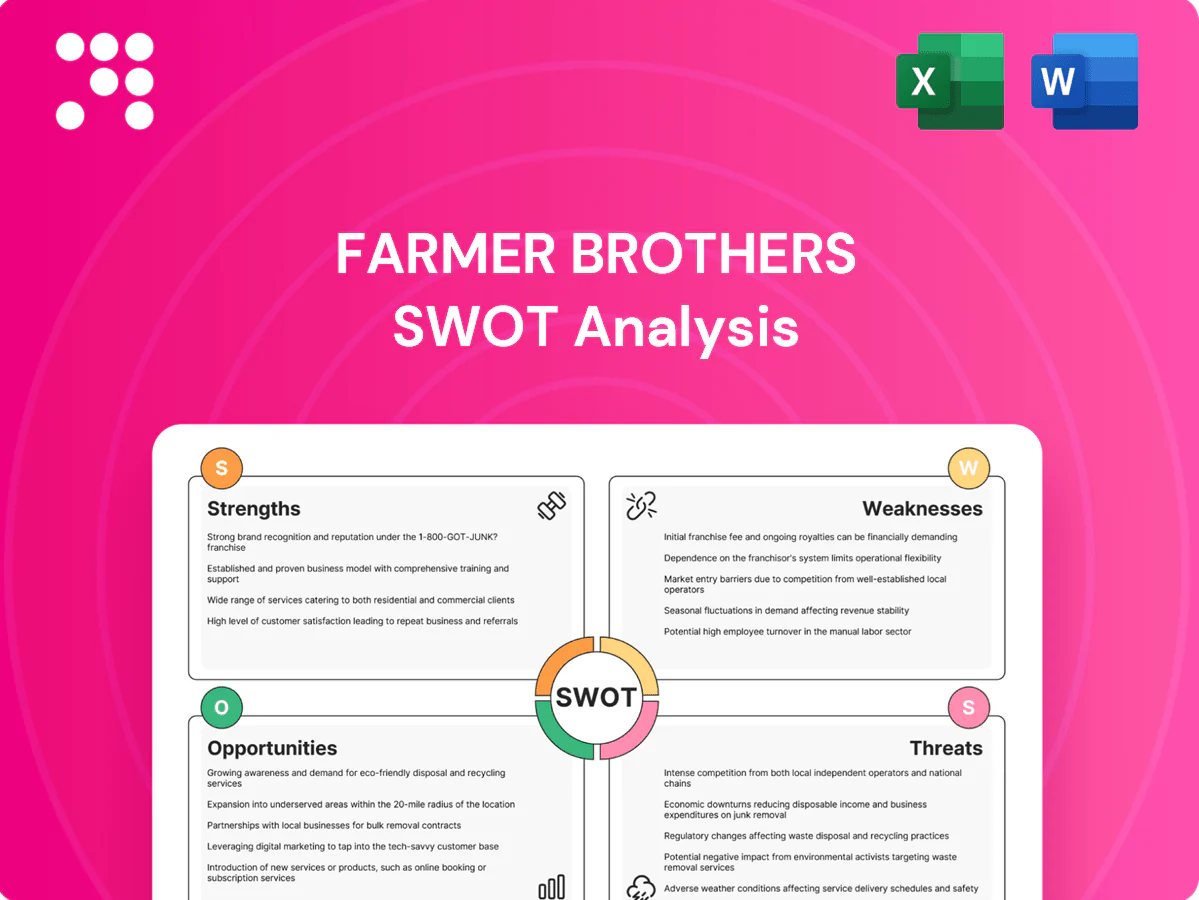

Farmer Brothers SWOT Analysis

Your Strategic Toolkit Starts Here

Explore Farmer Brothers' strategic standing with a concise SWOT snapshot highlighting brand strengths, supply-chain risks, market opportunities, and competitive pressures. Want deeper, actionable intelligence? Purchase the full SWOT analysis for a research-backed, editable report and Excel matrix—designed to inform strategy, investment decisions, and presentations.

Strengths

National roasting and distribution

As a national roaster, wholesaler and distributor, Farmer Brothers leverages 11 roasting/distribution facilities and FY2024 net sales of $539 million to deliver consistent service across regions, supporting reliable supply to diverse foodservice and institutional customers. This scale strengthens negotiating leverage with suppliers and logistics partners and enables faster rollouts of new products and programs.

Diverse B2B customer portfolio

Serving independent restaurants, multi-unit foodservice operators, and large institutions diversifies demand for Farmer Brothers, which serves about 20,000 customer locations and reported roughly $667 million in annual net sales (FY2024). This customer mix smooths revenue across cycles and seasonality, creates multiple channels for innovation pilots and price architecture, and reduces reliance on any single segment.

Integrated products, equipment, and service

Combining coffee and tea with equipment and services creates a stickier value proposition for Farmer Brothers, allowing bundled offerings that lift average revenue per account and reduce churn; integrated service agreements support brew quality and uptime, reinforcing consistent product experience and enabling long-term contracts that increase route density and customer lifetime value.

Roasting expertise and quality control

As a dedicated roaster, Farmer Brothers tailors blends and roast profiles to operator needs, enabling menu-specific customization that differentiates from generic commodity suppliers.

Control over sourcing and in-house roasting supports consistent cup quality across locations and reduces reliance on third-party variability.

Proprietary process know-how boosts yield and cost efficiency, lowering waste and improving margins.

- Tailored blends

- Controlled consistency

- Yield/cost efficiency

Cross-category culinary portfolio

Offering culinary products alongside beverages lets Farmer Brothers cross-sell into existing accounts, broadening wallet share and simplifying procurement for operators; FY2024 net sales of $613.4 million underscore distribution scale. The portfolio enables menu innovation and seasonal LTOs, while category breadth helps defend accounts against single-category competitors.

- Cross-sell into beverage accounts

- Increases wallet share

- Simplifies procurement

- Supports menu LTOs

- Defends versus single-category rivals

11 facilities and $613.4M FY2024 sales serving ~20,000 locations

Farmer Brothers leverages 11 roasting/distribution facilities and FY2024 consolidated net sales of $613.4M to serve ~20,000 locations across foodservice, multi-unit and institutional channels, enabling scale, product bundling (beverages, culinary, equipment) and strong supplier/logistics leverage that improve margins and customer retention.

| Metric | Value |

|---|---|

| Facilities | 11 |

| FY2024 Net Sales | $613.4M |

| Customer locations | ~20,000 |

What is included in the product

Provides a clear SWOT framework analyzing Farmer Brothers’s strengths, weaknesses, opportunities, and threats, highlighting its operational capabilities, brand positioning, growth drivers, market challenges, and external risks shaping future strategy.

Provides a concise Farmer Brothers SWOT matrix for fast, visual strategy alignment and executive snapshots, streamlining communication of strengths, weaknesses, opportunities, and threats for quick decision-making.

Weaknesses

High exposure to foodservice cycles

Farmer Brothers reports the majority of sales come from restaurant and institutional channels, tying performance to traffic and budget trends; U.S. restaurant sales were about $930 billion in 2024 (National Restaurant Association). Downturns or disruptions can quickly cut volumes and recovery from such declines typically lags consumer retail channels. Macro volatility in 2023–24 made forecasting for foodservice-driven revenue more unpredictable.

Commodity cost sensitivity

Farmer Brothers faces sharp commodity cost sensitivity as coffee and tea prices fluctuate with weather, yields and currency moves; Arabica futures experienced swings of roughly 50% between 2022–24, amplifying input risk. Passing through cost increases to price-sensitive B2B customers often lags, causing margin compression during price spikes. Hedging programs reduce exposure but cannot eliminate basis and timing mismatches, leaving residual volatility in gross margins.

Margin pressure from large buyers

Institutional and chain accounts exert strong pricing power, representing roughly 45% of Farmer Brothers’ fiscal 2024 net sales of about $1.05 billion, forcing competitive bids that compress gross margins to the mid-20% range. Private-label alternatives and aggressive RFPs have tightened realized margins by several hundred basis points year-over-year. Service-level commitments—route delivery, inventory guarantees—add fixed costs that are hard to recover, while multi-year contracts limit rapid price adjustments.

Capital and service intensity

Equipment provisioning, maintenance and route service demand heavy capital and skilled labor, squeezing cash flow and raising fixed costs for Farmer Brothers; utilization dips materially worsen unit economics and can turn profitable routes loss-making. Field service complexity increases training costs and downtime, while geographic expansion with low density dilutes margins and raises per-unit delivery costs.

- High capex and OPEX for equipment and service

- Utilization sensitivity hurts unit economics

- Training and field complexity raise fixed costs

- Low-density scaling dilutes margins

Limited consumer brand pull

Farmer Brothers focus on B2B limits household brand recognition versus retail-focused peers such as Starbucks and Nestlé, reducing direct consumer pull. Weak consumer awareness restricts ability to command premium pricing from operators and constrains retail channel expansion. Marketing efficiency trails competitors with established consumer brands, raising customer acquisition costs.

- Lower household awareness vs retail leaders

- Reduced premium pricing leverage

- Hindered retail expansion

- Higher marketing CAC vs consumer brands

B2B-heavy coffee supplier tied to restaurant traffic; 50% Arabica swings

Heavy B2B mix (≈45% of $1.05B net sales in FY2024) ties revenue to restaurant traffic ($930B U.S. industry in 2024) and makes recovery slow after downturns. Arabica price swings of ~50% (2022–24) and lagged passthrough compress margins; realized gross margins sit in the mid-20% range. High capex/OPEX for equipment, route service and low-density expansion raise fixed costs and unit risk.

| Metric | Value |

|---|---|

| FY2024 Net Sales | $1.05B |

| Institutional/Chain Share | ≈45% |

| U.S. Restaurant Sales (2024) | $930B |

| Arabica Futures Move (2022–24) | ≈50% |

| Gross Margin | Mid-20% |

Preview Before You Purchase

Farmer Brothers SWOT Analysis

This is the actual Farmer Brothers SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content. Buy now to unlock the complete, detailed version for download.

Your Strategic Toolkit Starts Here

Explore Farmer Brothers' strategic standing with a concise SWOT snapshot highlighting brand strengths, supply-chain risks, market opportunities, and competitive pressures. Want deeper, actionable intelligence? Purchase the full SWOT analysis for a research-backed, editable report and Excel matrix—designed to inform strategy, investment decisions, and presentations.

Strengths

National roasting and distribution

As a national roaster, wholesaler and distributor, Farmer Brothers leverages 11 roasting/distribution facilities and FY2024 net sales of $539 million to deliver consistent service across regions, supporting reliable supply to diverse foodservice and institutional customers. This scale strengthens negotiating leverage with suppliers and logistics partners and enables faster rollouts of new products and programs.

Diverse B2B customer portfolio

Serving independent restaurants, multi-unit foodservice operators, and large institutions diversifies demand for Farmer Brothers, which serves about 20,000 customer locations and reported roughly $667 million in annual net sales (FY2024). This customer mix smooths revenue across cycles and seasonality, creates multiple channels for innovation pilots and price architecture, and reduces reliance on any single segment.

Integrated products, equipment, and service

Combining coffee and tea with equipment and services creates a stickier value proposition for Farmer Brothers, allowing bundled offerings that lift average revenue per account and reduce churn; integrated service agreements support brew quality and uptime, reinforcing consistent product experience and enabling long-term contracts that increase route density and customer lifetime value.

Roasting expertise and quality control

As a dedicated roaster, Farmer Brothers tailors blends and roast profiles to operator needs, enabling menu-specific customization that differentiates from generic commodity suppliers.

Control over sourcing and in-house roasting supports consistent cup quality across locations and reduces reliance on third-party variability.

Proprietary process know-how boosts yield and cost efficiency, lowering waste and improving margins.

- Tailored blends

- Controlled consistency

- Yield/cost efficiency

Cross-category culinary portfolio

Offering culinary products alongside beverages lets Farmer Brothers cross-sell into existing accounts, broadening wallet share and simplifying procurement for operators; FY2024 net sales of $613.4 million underscore distribution scale. The portfolio enables menu innovation and seasonal LTOs, while category breadth helps defend accounts against single-category competitors.

- Cross-sell into beverage accounts

- Increases wallet share

- Simplifies procurement

- Supports menu LTOs

- Defends versus single-category rivals

11 facilities and $613.4M FY2024 sales serving ~20,000 locations

Farmer Brothers leverages 11 roasting/distribution facilities and FY2024 consolidated net sales of $613.4M to serve ~20,000 locations across foodservice, multi-unit and institutional channels, enabling scale, product bundling (beverages, culinary, equipment) and strong supplier/logistics leverage that improve margins and customer retention.

| Metric | Value |

|---|---|

| Facilities | 11 |

| FY2024 Net Sales | $613.4M |

| Customer locations | ~20,000 |

What is included in the product

Provides a clear SWOT framework analyzing Farmer Brothers’s strengths, weaknesses, opportunities, and threats, highlighting its operational capabilities, brand positioning, growth drivers, market challenges, and external risks shaping future strategy.

Provides a concise Farmer Brothers SWOT matrix for fast, visual strategy alignment and executive snapshots, streamlining communication of strengths, weaknesses, opportunities, and threats for quick decision-making.

Weaknesses

High exposure to foodservice cycles

Farmer Brothers reports the majority of sales come from restaurant and institutional channels, tying performance to traffic and budget trends; U.S. restaurant sales were about $930 billion in 2024 (National Restaurant Association). Downturns or disruptions can quickly cut volumes and recovery from such declines typically lags consumer retail channels. Macro volatility in 2023–24 made forecasting for foodservice-driven revenue more unpredictable.

Commodity cost sensitivity

Farmer Brothers faces sharp commodity cost sensitivity as coffee and tea prices fluctuate with weather, yields and currency moves; Arabica futures experienced swings of roughly 50% between 2022–24, amplifying input risk. Passing through cost increases to price-sensitive B2B customers often lags, causing margin compression during price spikes. Hedging programs reduce exposure but cannot eliminate basis and timing mismatches, leaving residual volatility in gross margins.

Margin pressure from large buyers

Institutional and chain accounts exert strong pricing power, representing roughly 45% of Farmer Brothers’ fiscal 2024 net sales of about $1.05 billion, forcing competitive bids that compress gross margins to the mid-20% range. Private-label alternatives and aggressive RFPs have tightened realized margins by several hundred basis points year-over-year. Service-level commitments—route delivery, inventory guarantees—add fixed costs that are hard to recover, while multi-year contracts limit rapid price adjustments.

Capital and service intensity

Equipment provisioning, maintenance and route service demand heavy capital and skilled labor, squeezing cash flow and raising fixed costs for Farmer Brothers; utilization dips materially worsen unit economics and can turn profitable routes loss-making. Field service complexity increases training costs and downtime, while geographic expansion with low density dilutes margins and raises per-unit delivery costs.

- High capex and OPEX for equipment and service

- Utilization sensitivity hurts unit economics

- Training and field complexity raise fixed costs

- Low-density scaling dilutes margins

Limited consumer brand pull

Farmer Brothers focus on B2B limits household brand recognition versus retail-focused peers such as Starbucks and Nestlé, reducing direct consumer pull. Weak consumer awareness restricts ability to command premium pricing from operators and constrains retail channel expansion. Marketing efficiency trails competitors with established consumer brands, raising customer acquisition costs.

- Lower household awareness vs retail leaders

- Reduced premium pricing leverage

- Hindered retail expansion

- Higher marketing CAC vs consumer brands

B2B-heavy coffee supplier tied to restaurant traffic; 50% Arabica swings

Heavy B2B mix (≈45% of $1.05B net sales in FY2024) ties revenue to restaurant traffic ($930B U.S. industry in 2024) and makes recovery slow after downturns. Arabica price swings of ~50% (2022–24) and lagged passthrough compress margins; realized gross margins sit in the mid-20% range. High capex/OPEX for equipment, route service and low-density expansion raise fixed costs and unit risk.

| Metric | Value |

|---|---|

| FY2024 Net Sales | $1.05B |

| Institutional/Chain Share | ≈45% |

| U.S. Restaurant Sales (2024) | $930B |

| Arabica Futures Move (2022–24) | ≈50% |

| Gross Margin | Mid-20% |

Preview Before You Purchase

Farmer Brothers SWOT Analysis

This is the actual Farmer Brothers SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content. Buy now to unlock the complete, detailed version for download.

Description

Your Strategic Toolkit Starts Here

Explore Farmer Brothers' strategic standing with a concise SWOT snapshot highlighting brand strengths, supply-chain risks, market opportunities, and competitive pressures. Want deeper, actionable intelligence? Purchase the full SWOT analysis for a research-backed, editable report and Excel matrix—designed to inform strategy, investment decisions, and presentations.

Strengths

National roasting and distribution

As a national roaster, wholesaler and distributor, Farmer Brothers leverages 11 roasting/distribution facilities and FY2024 net sales of $539 million to deliver consistent service across regions, supporting reliable supply to diverse foodservice and institutional customers. This scale strengthens negotiating leverage with suppliers and logistics partners and enables faster rollouts of new products and programs.

Diverse B2B customer portfolio

Serving independent restaurants, multi-unit foodservice operators, and large institutions diversifies demand for Farmer Brothers, which serves about 20,000 customer locations and reported roughly $667 million in annual net sales (FY2024). This customer mix smooths revenue across cycles and seasonality, creates multiple channels for innovation pilots and price architecture, and reduces reliance on any single segment.

Integrated products, equipment, and service

Combining coffee and tea with equipment and services creates a stickier value proposition for Farmer Brothers, allowing bundled offerings that lift average revenue per account and reduce churn; integrated service agreements support brew quality and uptime, reinforcing consistent product experience and enabling long-term contracts that increase route density and customer lifetime value.

Roasting expertise and quality control

As a dedicated roaster, Farmer Brothers tailors blends and roast profiles to operator needs, enabling menu-specific customization that differentiates from generic commodity suppliers.

Control over sourcing and in-house roasting supports consistent cup quality across locations and reduces reliance on third-party variability.

Proprietary process know-how boosts yield and cost efficiency, lowering waste and improving margins.

- Tailored blends

- Controlled consistency

- Yield/cost efficiency

Cross-category culinary portfolio

Offering culinary products alongside beverages lets Farmer Brothers cross-sell into existing accounts, broadening wallet share and simplifying procurement for operators; FY2024 net sales of $613.4 million underscore distribution scale. The portfolio enables menu innovation and seasonal LTOs, while category breadth helps defend accounts against single-category competitors.

- Cross-sell into beverage accounts

- Increases wallet share

- Simplifies procurement

- Supports menu LTOs

- Defends versus single-category rivals

11 facilities and $613.4M FY2024 sales serving ~20,000 locations

Farmer Brothers leverages 11 roasting/distribution facilities and FY2024 consolidated net sales of $613.4M to serve ~20,000 locations across foodservice, multi-unit and institutional channels, enabling scale, product bundling (beverages, culinary, equipment) and strong supplier/logistics leverage that improve margins and customer retention.

| Metric | Value |

|---|---|

| Facilities | 11 |

| FY2024 Net Sales | $613.4M |

| Customer locations | ~20,000 |

What is included in the product

Provides a clear SWOT framework analyzing Farmer Brothers’s strengths, weaknesses, opportunities, and threats, highlighting its operational capabilities, brand positioning, growth drivers, market challenges, and external risks shaping future strategy.

Provides a concise Farmer Brothers SWOT matrix for fast, visual strategy alignment and executive snapshots, streamlining communication of strengths, weaknesses, opportunities, and threats for quick decision-making.

Weaknesses

High exposure to foodservice cycles

Farmer Brothers reports the majority of sales come from restaurant and institutional channels, tying performance to traffic and budget trends; U.S. restaurant sales were about $930 billion in 2024 (National Restaurant Association). Downturns or disruptions can quickly cut volumes and recovery from such declines typically lags consumer retail channels. Macro volatility in 2023–24 made forecasting for foodservice-driven revenue more unpredictable.

Commodity cost sensitivity

Farmer Brothers faces sharp commodity cost sensitivity as coffee and tea prices fluctuate with weather, yields and currency moves; Arabica futures experienced swings of roughly 50% between 2022–24, amplifying input risk. Passing through cost increases to price-sensitive B2B customers often lags, causing margin compression during price spikes. Hedging programs reduce exposure but cannot eliminate basis and timing mismatches, leaving residual volatility in gross margins.

Margin pressure from large buyers

Institutional and chain accounts exert strong pricing power, representing roughly 45% of Farmer Brothers’ fiscal 2024 net sales of about $1.05 billion, forcing competitive bids that compress gross margins to the mid-20% range. Private-label alternatives and aggressive RFPs have tightened realized margins by several hundred basis points year-over-year. Service-level commitments—route delivery, inventory guarantees—add fixed costs that are hard to recover, while multi-year contracts limit rapid price adjustments.

Capital and service intensity

Equipment provisioning, maintenance and route service demand heavy capital and skilled labor, squeezing cash flow and raising fixed costs for Farmer Brothers; utilization dips materially worsen unit economics and can turn profitable routes loss-making. Field service complexity increases training costs and downtime, while geographic expansion with low density dilutes margins and raises per-unit delivery costs.

- High capex and OPEX for equipment and service

- Utilization sensitivity hurts unit economics

- Training and field complexity raise fixed costs

- Low-density scaling dilutes margins

Limited consumer brand pull

Farmer Brothers focus on B2B limits household brand recognition versus retail-focused peers such as Starbucks and Nestlé, reducing direct consumer pull. Weak consumer awareness restricts ability to command premium pricing from operators and constrains retail channel expansion. Marketing efficiency trails competitors with established consumer brands, raising customer acquisition costs.

- Lower household awareness vs retail leaders

- Reduced premium pricing leverage

- Hindered retail expansion

- Higher marketing CAC vs consumer brands

B2B-heavy coffee supplier tied to restaurant traffic; 50% Arabica swings

Heavy B2B mix (≈45% of $1.05B net sales in FY2024) ties revenue to restaurant traffic ($930B U.S. industry in 2024) and makes recovery slow after downturns. Arabica price swings of ~50% (2022–24) and lagged passthrough compress margins; realized gross margins sit in the mid-20% range. High capex/OPEX for equipment, route service and low-density expansion raise fixed costs and unit risk.

| Metric | Value |

|---|---|

| FY2024 Net Sales | $1.05B |

| Institutional/Chain Share | ≈45% |

| U.S. Restaurant Sales (2024) | $930B |

| Arabica Futures Move (2022–24) | ≈50% |

| Gross Margin | Mid-20% |

Preview Before You Purchase

Farmer Brothers SWOT Analysis

This is the actual Farmer Brothers SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content. Buy now to unlock the complete, detailed version for download.