Farmers National Bank Boston Consulting Group Matrix

See the Bigger Picture

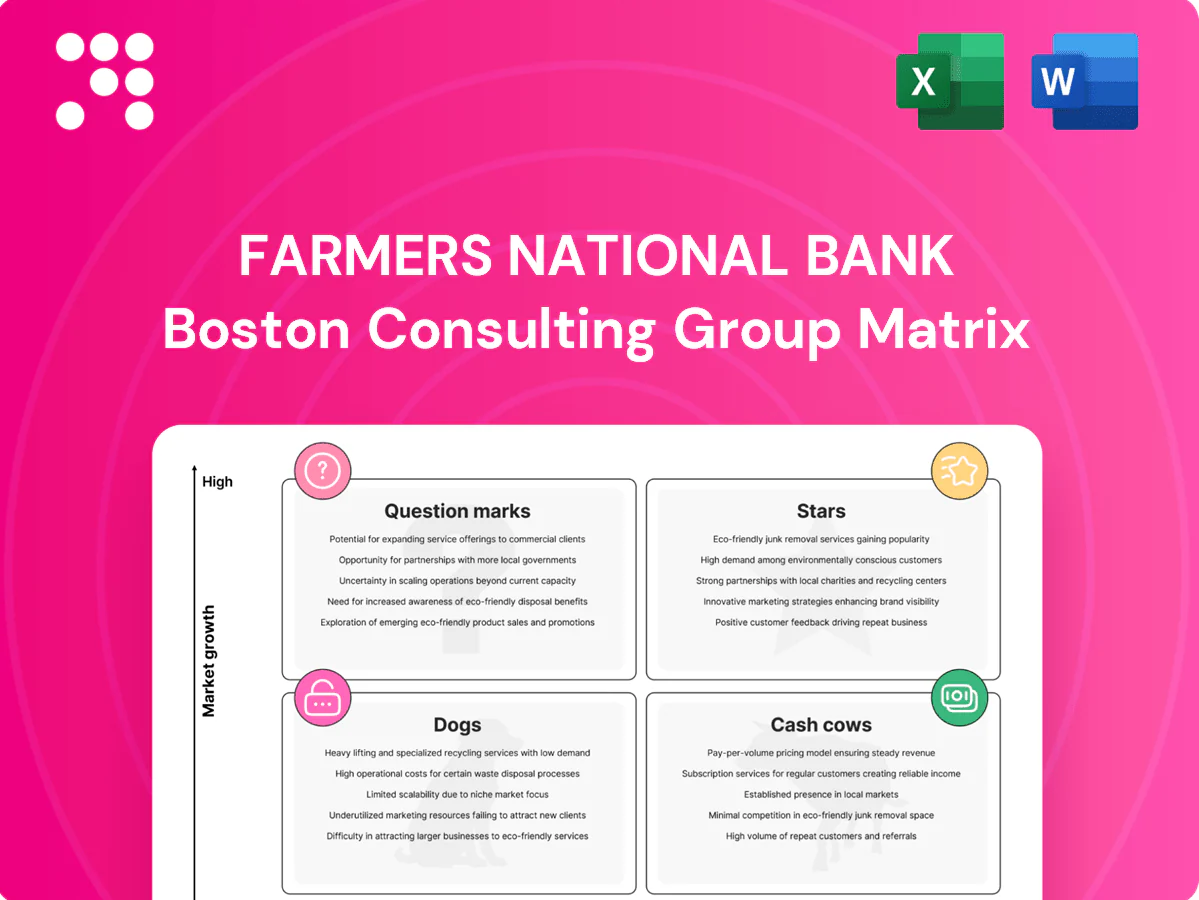

Farmers National Bank’s quick BCG snapshot teases where products might sit—Stars driving growth, Cash Cows funding the core, Dogs dragging returns, and Question Marks begging a decision. Want the full picture with quadrant-by-quadrant placement, data-backed recommendations and a ready-to-present roadmap? Purchase the complete BCG Matrix for a detailed Word report plus an editable Excel summary and start making smarter allocation and product decisions today.

Stars

Core commercial & industrial lending in footprint

Growing local business formation and reshoring trends—reflected in sustained elevated business formation applications reported by the US Census since 2020—are boosting loan demand in Farmers National Bank’s footprint. Farmers holds a strong share via relationship bankers and fast credit turns, supporting above-market commercial loan growth. Keep investing in talent and targeted marketing to stay top-of-mind; if momentum sustains as the market matures, this will transition into a Cash Cow.

SMB treasury & cash management

SMB treasury & cash management drives sticky fee income and high share of revenue among existing business clients, with solid cross‑sell from lending; NACHA reports the ACH Network handled over 36 billion payments in 2023, reflecting rising ACH adoption. Remote deposit and stronger fraud controls cut risk and boost retention. Requires ongoing UX and integration investment but payback is fast—protect the lead and keep shipping features.

Wealth management & trust services

Demographics are a clear tailwind: baby boomers held about 70% of U.S. net worth in 2024, driving sizeable intergenerational transfers that increase demand for trust services.

Farmers National Bank’s local brand trust yields outsized share versus national platforms for complex trust work, especially high-net-worth estate transitions.

Scaling requires targeted advisor hiring and upgraded digital reporting to convert demand into assets under administration; sustain share and trust fees become a predictable annuity.

Commercial real estate specialties (owner‑occupied)

Commercial real estate specialties (owner‑occupied) show a healthy pipeline in medical, light industrial and owner‑occupied offices; strong underwriting and deep local knowledge sustain market share. Growth persists even as the Fed funds rate held near 5.25–5.50% in 2024, so maintain disciplined structure to preserve star status.

- Pipeline: medical, light industrial, owner‑occupied offices

- Edge: underwriting + local knowledge

- Watch: rates ~5.25–5.50% (2024) — preserve structure

Digital banking for existing customers

Mobile adoption is climbing and engagement is deep: in 2024 more than half of retail banking interactions shifted to digital channels (McKinsey 2024), and Farmers’ app is capturing share-of-wallet within its deposit base. Continued investment in usability, real-time alerts and instant-issue cards is driving higher retention and fee income. Keep iterating—digital enhancements anchor the franchise and expand lifetime value.

- 2024 digital interactions >50% (McKinsey)

- App-led share-of-wallet gains within base

- Usability + alerts + instant-issue = higher retention

Commercial loan surge, sticky ACH fees 36B, over 50% digital — invest in talent

Stars: strong commercial loan growth from elevated business formation, sticky SMB treasury fees (ACH 36B payments 2023), >50% digital interactions in 2024 and durable trust demand from baby‑boomer wealth transfer; invest in talent, UX and underwriting to secure scale and convert to Cash Cow.

| Segment | 2024 metric | Implication |

|---|---|---|

| Commercial loans | Above‑market growth | Invest underwriting |

| Treasury | ACH 36B (2023) | Sticky fee income |

| Digital | >50% interactions | Prioritize UX |

What is included in the product

Comprehensive BCG analysis of Farmers National Bank's units, identifying Stars, Cash Cows, Question Marks, Dogs with strategic recommendations.

One-page BCG matrix easing portfolio decisions for Farmers National Bank

Cash Cows

Core retail deposits (checking, savings, money market)

Core retail deposits—checking, savings and money market accounts—constitute a large, low-cost funding base for Farmers National Bank, with community-bank core deposits averaging about 70% of total funding in FDIC 2024 data, reflecting long customer relationships and funding stability.

Market growth for these products is modest but FNB’s share is strong locally, requiring minimal promotion beyond periodic rate hygiene tied to the prevailing policy rate environment in 2024.

Strategy: milk stable margins while actively defending balances against rate shoppers through relationship banking, digital convenience and selective retention pricing informed by 2024 deposit-cost benchmarks.

Mortgage servicing and secondary-market sales

Mortgage servicing and secondary-market sales provide steady fee income for Farmers National Bank: origination volumes are lumpy, but servicing fees in 2024 remain recurring with thin incremental cost and established workflows. Growth is limited, making these true cash cows that reliably fund operations and capital needs. Optimize hedging and manage prepayment speeds to protect MSR economics and preserve spread capture.

Home equity lines to prime customers

Home equity lines to prime customers are a mature, low-cost cash cow for Farmers National Bank, with disciplined underwriting and cross-sell driving steady originations; industry HELOC utilization averaged about 25% in 2024 and typical spreads near 300 basis points support solid margins. Low marketing spend—branch and digital referrals capture the bulk of leads—means high operating leverage; maintain strict underwriting and enjoy recurring cash flow.

Trust administration fees

Trust administration fees deliver stable, recurring revenue with low client churn; market growth is limited but Farmers National Bank holds high share across its core counties. Operational investments are fully amortized, enabling low incremental cost to serve. Maintain high service levels and firm pricing to protect margins and retention.

- Recurring revenue: stable

- Churn: low

- Market growth: limited

- Share: high in core counties

- Costs: investments paid off

- Strategy: preserve service and pricing

Commercial deposits and operating accounts

Commercial deposits and operating accounts deliver stable balances tied to lending relationships, with slow growth but strong economics driven by low incremental cost to serve and high retention from cash-flow needs; protect this cash cow through bundled treasury services and relationship pricing to preserve fee income and cross-sell opportunities.

- Stable balances linked to lending

- Slow growth, strong margins

- Low incremental servicing cost

- Protect via bundled services & relationship pricing

Stable, high-margin cash cows: defend core deposits with digital, relationships, strict underwriting

Farmers National Bank cash cows—core deposits (~70% of funding, FDIC 2024), mortgage servicing (recurring fees), HELOCs to prime borrowers (25% utilization, ~300 bps spread) and trust/admin fees—generate stable, high-margin cash flow with limited market growth; strategy: defend share via relationship banking, digital convenience, selective pricing and strict underwriting.

| Product | 2024 Metric | Role |

|---|---|---|

| Core deposits | 70% funding | Low-cost base |

| MSR | Recurring fees | Stable income |

| HELOC | 25% util / 300bps | High margin |

| Trust fees | Low churn | Low cost |

Delivered as Shown

Farmers National Bank BCG Matrix

The file you're previewing is the final Farmers National Bank BCG Matrix you'll receive after purchase. No watermarks, no demo content—just a fully formatted, analysis-ready report designed for strategic clarity. This preview mirrors the exact downloadable document, ready for editing, printing, or presenting to your team. Buy once and get the complete file delivered to your inbox—no surprises.

See the Bigger Picture

Farmers National Bank’s quick BCG snapshot teases where products might sit—Stars driving growth, Cash Cows funding the core, Dogs dragging returns, and Question Marks begging a decision. Want the full picture with quadrant-by-quadrant placement, data-backed recommendations and a ready-to-present roadmap? Purchase the complete BCG Matrix for a detailed Word report plus an editable Excel summary and start making smarter allocation and product decisions today.

Stars

Core commercial & industrial lending in footprint

Growing local business formation and reshoring trends—reflected in sustained elevated business formation applications reported by the US Census since 2020—are boosting loan demand in Farmers National Bank’s footprint. Farmers holds a strong share via relationship bankers and fast credit turns, supporting above-market commercial loan growth. Keep investing in talent and targeted marketing to stay top-of-mind; if momentum sustains as the market matures, this will transition into a Cash Cow.

SMB treasury & cash management

SMB treasury & cash management drives sticky fee income and high share of revenue among existing business clients, with solid cross‑sell from lending; NACHA reports the ACH Network handled over 36 billion payments in 2023, reflecting rising ACH adoption. Remote deposit and stronger fraud controls cut risk and boost retention. Requires ongoing UX and integration investment but payback is fast—protect the lead and keep shipping features.

Wealth management & trust services

Demographics are a clear tailwind: baby boomers held about 70% of U.S. net worth in 2024, driving sizeable intergenerational transfers that increase demand for trust services.

Farmers National Bank’s local brand trust yields outsized share versus national platforms for complex trust work, especially high-net-worth estate transitions.

Scaling requires targeted advisor hiring and upgraded digital reporting to convert demand into assets under administration; sustain share and trust fees become a predictable annuity.

Commercial real estate specialties (owner‑occupied)

Commercial real estate specialties (owner‑occupied) show a healthy pipeline in medical, light industrial and owner‑occupied offices; strong underwriting and deep local knowledge sustain market share. Growth persists even as the Fed funds rate held near 5.25–5.50% in 2024, so maintain disciplined structure to preserve star status.

- Pipeline: medical, light industrial, owner‑occupied offices

- Edge: underwriting + local knowledge

- Watch: rates ~5.25–5.50% (2024) — preserve structure

Digital banking for existing customers

Mobile adoption is climbing and engagement is deep: in 2024 more than half of retail banking interactions shifted to digital channels (McKinsey 2024), and Farmers’ app is capturing share-of-wallet within its deposit base. Continued investment in usability, real-time alerts and instant-issue cards is driving higher retention and fee income. Keep iterating—digital enhancements anchor the franchise and expand lifetime value.

- 2024 digital interactions >50% (McKinsey)

- App-led share-of-wallet gains within base

- Usability + alerts + instant-issue = higher retention

Commercial loan surge, sticky ACH fees 36B, over 50% digital — invest in talent

Stars: strong commercial loan growth from elevated business formation, sticky SMB treasury fees (ACH 36B payments 2023), >50% digital interactions in 2024 and durable trust demand from baby‑boomer wealth transfer; invest in talent, UX and underwriting to secure scale and convert to Cash Cow.

| Segment | 2024 metric | Implication |

|---|---|---|

| Commercial loans | Above‑market growth | Invest underwriting |

| Treasury | ACH 36B (2023) | Sticky fee income |

| Digital | >50% interactions | Prioritize UX |

What is included in the product

Comprehensive BCG analysis of Farmers National Bank's units, identifying Stars, Cash Cows, Question Marks, Dogs with strategic recommendations.

One-page BCG matrix easing portfolio decisions for Farmers National Bank

Cash Cows

Core retail deposits (checking, savings, money market)

Core retail deposits—checking, savings and money market accounts—constitute a large, low-cost funding base for Farmers National Bank, with community-bank core deposits averaging about 70% of total funding in FDIC 2024 data, reflecting long customer relationships and funding stability.

Market growth for these products is modest but FNB’s share is strong locally, requiring minimal promotion beyond periodic rate hygiene tied to the prevailing policy rate environment in 2024.

Strategy: milk stable margins while actively defending balances against rate shoppers through relationship banking, digital convenience and selective retention pricing informed by 2024 deposit-cost benchmarks.

Mortgage servicing and secondary-market sales

Mortgage servicing and secondary-market sales provide steady fee income for Farmers National Bank: origination volumes are lumpy, but servicing fees in 2024 remain recurring with thin incremental cost and established workflows. Growth is limited, making these true cash cows that reliably fund operations and capital needs. Optimize hedging and manage prepayment speeds to protect MSR economics and preserve spread capture.

Home equity lines to prime customers

Home equity lines to prime customers are a mature, low-cost cash cow for Farmers National Bank, with disciplined underwriting and cross-sell driving steady originations; industry HELOC utilization averaged about 25% in 2024 and typical spreads near 300 basis points support solid margins. Low marketing spend—branch and digital referrals capture the bulk of leads—means high operating leverage; maintain strict underwriting and enjoy recurring cash flow.

Trust administration fees

Trust administration fees deliver stable, recurring revenue with low client churn; market growth is limited but Farmers National Bank holds high share across its core counties. Operational investments are fully amortized, enabling low incremental cost to serve. Maintain high service levels and firm pricing to protect margins and retention.

- Recurring revenue: stable

- Churn: low

- Market growth: limited

- Share: high in core counties

- Costs: investments paid off

- Strategy: preserve service and pricing

Commercial deposits and operating accounts

Commercial deposits and operating accounts deliver stable balances tied to lending relationships, with slow growth but strong economics driven by low incremental cost to serve and high retention from cash-flow needs; protect this cash cow through bundled treasury services and relationship pricing to preserve fee income and cross-sell opportunities.

- Stable balances linked to lending

- Slow growth, strong margins

- Low incremental servicing cost

- Protect via bundled services & relationship pricing

Stable, high-margin cash cows: defend core deposits with digital, relationships, strict underwriting

Farmers National Bank cash cows—core deposits (~70% of funding, FDIC 2024), mortgage servicing (recurring fees), HELOCs to prime borrowers (25% utilization, ~300 bps spread) and trust/admin fees—generate stable, high-margin cash flow with limited market growth; strategy: defend share via relationship banking, digital convenience, selective pricing and strict underwriting.

| Product | 2024 Metric | Role |

|---|---|---|

| Core deposits | 70% funding | Low-cost base |

| MSR | Recurring fees | Stable income |

| HELOC | 25% util / 300bps | High margin |

| Trust fees | Low churn | Low cost |

Delivered as Shown

Farmers National Bank BCG Matrix

The file you're previewing is the final Farmers National Bank BCG Matrix you'll receive after purchase. No watermarks, no demo content—just a fully formatted, analysis-ready report designed for strategic clarity. This preview mirrors the exact downloadable document, ready for editing, printing, or presenting to your team. Buy once and get the complete file delivered to your inbox—no surprises.

Original: $10.00

-65%$10.00

$3.50Description

See the Bigger Picture

Farmers National Bank’s quick BCG snapshot teases where products might sit—Stars driving growth, Cash Cows funding the core, Dogs dragging returns, and Question Marks begging a decision. Want the full picture with quadrant-by-quadrant placement, data-backed recommendations and a ready-to-present roadmap? Purchase the complete BCG Matrix for a detailed Word report plus an editable Excel summary and start making smarter allocation and product decisions today.

Stars

Core commercial & industrial lending in footprint

Growing local business formation and reshoring trends—reflected in sustained elevated business formation applications reported by the US Census since 2020—are boosting loan demand in Farmers National Bank’s footprint. Farmers holds a strong share via relationship bankers and fast credit turns, supporting above-market commercial loan growth. Keep investing in talent and targeted marketing to stay top-of-mind; if momentum sustains as the market matures, this will transition into a Cash Cow.

SMB treasury & cash management

SMB treasury & cash management drives sticky fee income and high share of revenue among existing business clients, with solid cross‑sell from lending; NACHA reports the ACH Network handled over 36 billion payments in 2023, reflecting rising ACH adoption. Remote deposit and stronger fraud controls cut risk and boost retention. Requires ongoing UX and integration investment but payback is fast—protect the lead and keep shipping features.

Wealth management & trust services

Demographics are a clear tailwind: baby boomers held about 70% of U.S. net worth in 2024, driving sizeable intergenerational transfers that increase demand for trust services.

Farmers National Bank’s local brand trust yields outsized share versus national platforms for complex trust work, especially high-net-worth estate transitions.

Scaling requires targeted advisor hiring and upgraded digital reporting to convert demand into assets under administration; sustain share and trust fees become a predictable annuity.

Commercial real estate specialties (owner‑occupied)

Commercial real estate specialties (owner‑occupied) show a healthy pipeline in medical, light industrial and owner‑occupied offices; strong underwriting and deep local knowledge sustain market share. Growth persists even as the Fed funds rate held near 5.25–5.50% in 2024, so maintain disciplined structure to preserve star status.

- Pipeline: medical, light industrial, owner‑occupied offices

- Edge: underwriting + local knowledge

- Watch: rates ~5.25–5.50% (2024) — preserve structure

Digital banking for existing customers

Mobile adoption is climbing and engagement is deep: in 2024 more than half of retail banking interactions shifted to digital channels (McKinsey 2024), and Farmers’ app is capturing share-of-wallet within its deposit base. Continued investment in usability, real-time alerts and instant-issue cards is driving higher retention and fee income. Keep iterating—digital enhancements anchor the franchise and expand lifetime value.

- 2024 digital interactions >50% (McKinsey)

- App-led share-of-wallet gains within base

- Usability + alerts + instant-issue = higher retention

Commercial loan surge, sticky ACH fees 36B, over 50% digital — invest in talent

Stars: strong commercial loan growth from elevated business formation, sticky SMB treasury fees (ACH 36B payments 2023), >50% digital interactions in 2024 and durable trust demand from baby‑boomer wealth transfer; invest in talent, UX and underwriting to secure scale and convert to Cash Cow.

| Segment | 2024 metric | Implication |

|---|---|---|

| Commercial loans | Above‑market growth | Invest underwriting |

| Treasury | ACH 36B (2023) | Sticky fee income |

| Digital | >50% interactions | Prioritize UX |

What is included in the product

Comprehensive BCG analysis of Farmers National Bank's units, identifying Stars, Cash Cows, Question Marks, Dogs with strategic recommendations.

One-page BCG matrix easing portfolio decisions for Farmers National Bank

Cash Cows

Core retail deposits (checking, savings, money market)

Core retail deposits—checking, savings and money market accounts—constitute a large, low-cost funding base for Farmers National Bank, with community-bank core deposits averaging about 70% of total funding in FDIC 2024 data, reflecting long customer relationships and funding stability.

Market growth for these products is modest but FNB’s share is strong locally, requiring minimal promotion beyond periodic rate hygiene tied to the prevailing policy rate environment in 2024.

Strategy: milk stable margins while actively defending balances against rate shoppers through relationship banking, digital convenience and selective retention pricing informed by 2024 deposit-cost benchmarks.

Mortgage servicing and secondary-market sales

Mortgage servicing and secondary-market sales provide steady fee income for Farmers National Bank: origination volumes are lumpy, but servicing fees in 2024 remain recurring with thin incremental cost and established workflows. Growth is limited, making these true cash cows that reliably fund operations and capital needs. Optimize hedging and manage prepayment speeds to protect MSR economics and preserve spread capture.

Home equity lines to prime customers

Home equity lines to prime customers are a mature, low-cost cash cow for Farmers National Bank, with disciplined underwriting and cross-sell driving steady originations; industry HELOC utilization averaged about 25% in 2024 and typical spreads near 300 basis points support solid margins. Low marketing spend—branch and digital referrals capture the bulk of leads—means high operating leverage; maintain strict underwriting and enjoy recurring cash flow.

Trust administration fees

Trust administration fees deliver stable, recurring revenue with low client churn; market growth is limited but Farmers National Bank holds high share across its core counties. Operational investments are fully amortized, enabling low incremental cost to serve. Maintain high service levels and firm pricing to protect margins and retention.

- Recurring revenue: stable

- Churn: low

- Market growth: limited

- Share: high in core counties

- Costs: investments paid off

- Strategy: preserve service and pricing

Commercial deposits and operating accounts

Commercial deposits and operating accounts deliver stable balances tied to lending relationships, with slow growth but strong economics driven by low incremental cost to serve and high retention from cash-flow needs; protect this cash cow through bundled treasury services and relationship pricing to preserve fee income and cross-sell opportunities.

- Stable balances linked to lending

- Slow growth, strong margins

- Low incremental servicing cost

- Protect via bundled services & relationship pricing

Stable, high-margin cash cows: defend core deposits with digital, relationships, strict underwriting

Farmers National Bank cash cows—core deposits (~70% of funding, FDIC 2024), mortgage servicing (recurring fees), HELOCs to prime borrowers (25% utilization, ~300 bps spread) and trust/admin fees—generate stable, high-margin cash flow with limited market growth; strategy: defend share via relationship banking, digital convenience, selective pricing and strict underwriting.

| Product | 2024 Metric | Role |

|---|---|---|

| Core deposits | 70% funding | Low-cost base |

| MSR | Recurring fees | Stable income |

| HELOC | 25% util / 300bps | High margin |

| Trust fees | Low churn | Low cost |

Delivered as Shown

Farmers National Bank BCG Matrix

The file you're previewing is the final Farmers National Bank BCG Matrix you'll receive after purchase. No watermarks, no demo content—just a fully formatted, analysis-ready report designed for strategic clarity. This preview mirrors the exact downloadable document, ready for editing, printing, or presenting to your team. Buy once and get the complete file delivered to your inbox—no surprises.