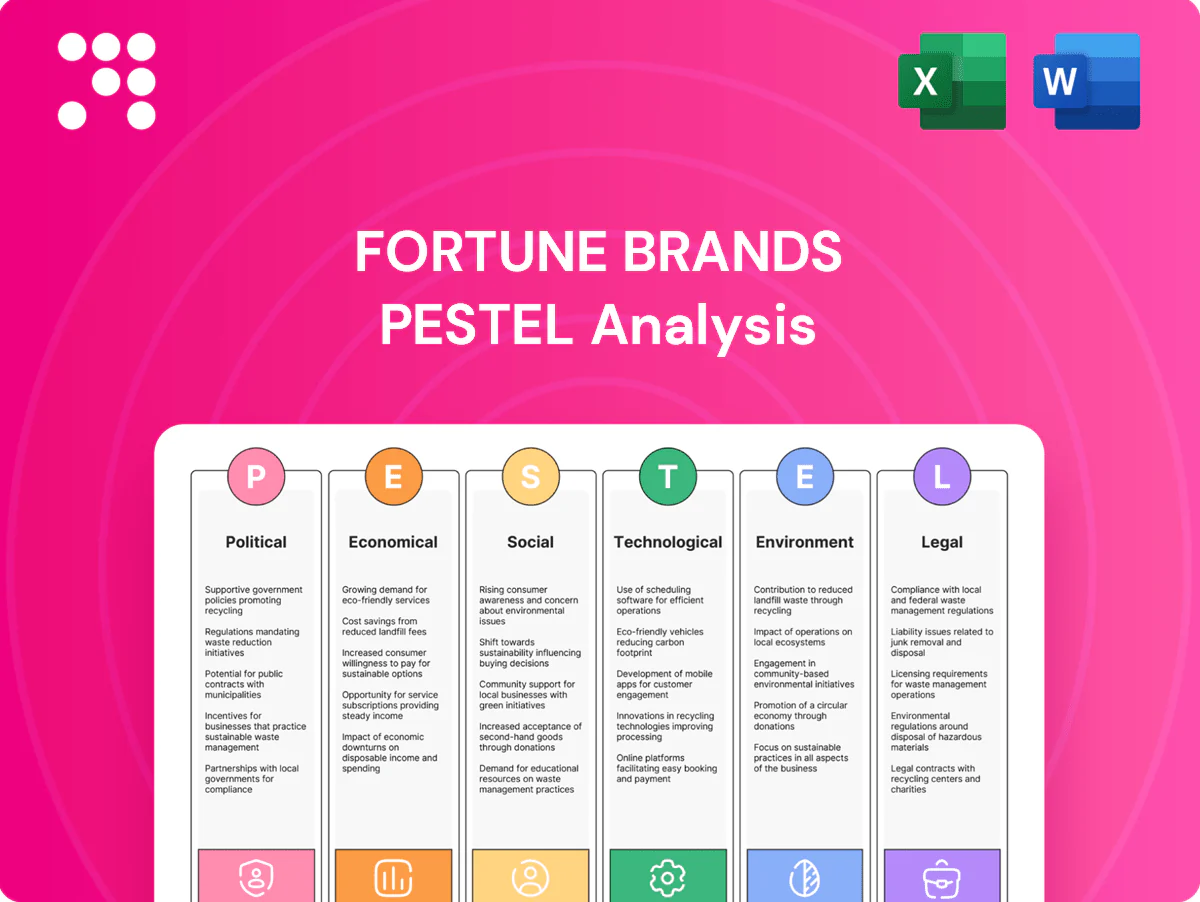

Fortune Brands PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and technological trends are shaping Fortune Brands' prospects in our concise PESTLE snapshot. This strategic briefing highlights risks and opportunities you can act on immediately. Purchase the full PESTLE for the complete, editable analysis and actionable intelligence.

Political factors

Trade policy and tariffs

Import duties such as the US 25% steel and 10% aluminum Section 232 tariffs and remaining US-China tariffs up to 25% can materially swing input costs for metals, resins, and finished hardware, forcing pricing adjustments. Changes in US-China relations or USMCA rules (in force since 2020) alter sourcing economics for faucets, locks, and decking components. Retaliatory tariffs have driven supplier diversification and nearshoring trends, while stable trade policy underpins predictable margins and inventory planning.

Housing and infrastructure agendas

Government incentives—notably the 2021 Bipartisan Infrastructure Law (about 55 billion for water and 110 billion for roads/bridges) and the Inflation Reduction Act (~369 billion for clean energy)—boost demand for plumbing, security, and energy-efficient building products, supporting Fortune Brands (FY2024 net sales ~4.7 billion). Public infrastructure spending and regional grants accelerate pro-channel activity, while appropriations delays or post-election policy shifts create order volatility and push SKU mix toward rebate-compliant, high-efficiency products.

“Buy American” and local content

Procurement preferences increasingly favor domestically produced fixtures, locks and decking for public projects, amplifying opportunities for Fortune Brands' Moen, Master Lock and Fiberon lines. Meeting Buy American/local content thresholds—relevant across many federal and state programs in a US procurement market roughly 700 billion USD annually (2023–24)—may require supply‑chain reconfiguration and near‑term capex. Benefits include access to government contracts and stronger US brand positioning. Non‑compliance risks bid exclusion and reputational damage.

Geopolitical supply chain exposure

Political tensions increasingly disrupt ocean freight and port operations, with Red Sea route attacks in 2023–24 prompting rerouting that raised voyage costs and added war-risk surcharges often reaching tens of thousands of dollars per transit; export controls on advanced electronics since 2023 have constrained chips and modules used in smart locks and water systems. Companies must maintain multi-region tooling and dual sourcing to mitigate single-country exposure; insurers, lead times and buffer inventory have risen materially, with some firms reporting 20–40% longer lead times and higher inventory carrying costs.

- Exposure: ocean freight route risk; ports & transshipment chokepoints

- Controls: export sanctions on electronics affecting smart products

- Mitigation: multi-region tooling, dual sourcing, regional inventories

- Costs: war-risk premiums, higher insurance, 20–40% longer lead times

State and local policy fragmentation

State and local fragmentation forces Fortune Brands to navigate 50 state regimes and 19,000+ local building departments, complicating go-to-market timing and pricing. Divergent water-use rules (eg California Title 24) and varied security/fixture standards raise certification and compliance costs and require sustained advocacy and code-tracking. Misalignment can delay product launches and shrink addressable markets.

- 50 states; 19,000+ local jurisdictions impacting approvals

- California Title 24 cited as stricter standard

- Continuous advocacy and code-tracking operationally required

- Regulatory misalignment risks launch delays and lost market access

Tariffs and BIL/IRA lift demand; FY2024 sales 4.7B, supply risks rise

Tariffs (US 25% steel, 10% aluminum; US‑China up to 25%) and trade shifts materially affect input costs and sourcing for faucets, locks and decking. US infrastructure/energy laws (BIL, IRA) and ~700B/yr public procurement boost demand; FY2024 sales ~4.7B. Port disruptions and export controls raise lead times and insurance.

| Metric | Value |

|---|---|

| FY2024 sales | 4.7B |

| US procurement | ~700B/yr |

| Tariff rates | 25%/10% |

What is included in the product

Explores how macro forces—Political, Economic, Social, Technological, Environmental and Legal—specifically shape Fortune Brands’ opportunities and risks, with data-backed trends and industry examples. Designed for executives and investors to inform strategy, scenario planning and funding narratives.

A concise, visually segmented Fortune Brands PESTLE summary that’s editable for region- or product-specific notes, drop-in ready for presentations, and easily shareable to align teams on external risks and strategy.

Economic factors

Housing cycle sensitivity

Housing-cycle sensitivity is high for Fortune Brands: US housing starts ran around 1.4M annualized in 2024 (Census) and existing-home sales near 4.0M (NAR), directly affecting volumes for Moen, Master Lock and Fiberon. Higher mortgage rates (30-yr ~7% in 2024, Freddie Mac) typically curb new construction but shift spend to repair/remodel — US remodel spending ~$450B in 2024 (JCHS). Pro-channel backlogs buffer short-term swings; security/maintenance demand is more resilient than discretionary upgrades.

Consumer discretionary spend

Real income and confidence drive mid-to-premium fixture and outdoor living demand; with inflation easing to roughly 3% in 2024 and Conference Board confidence near 100 in mid-2025, higher-end conversion remains viable. Promotional intensity at big-box and e-commerce channels can accelerate or postpone purchases and heighten trade-down risk in downturns, compressing mix. Affluent segments continue to sustain premium adoption even in softer cycles.

Commodity and freight costs

Copper (~$9,500/tonne mid‑2025), brass, stainless, zinc, resins and lumber‑derived inputs remain material drivers of Fortune Brands’ COGS, with feedstock swings and freight/container spot volatility (spot transpacific container rates ~ $2,000–$3,000 per FEU in 2024–25) causing landed‑cost unpredictability. Pricing actions typically lag input spikes, compressing gross margins; hedging and long‑term supply contracts mitigate but cannot fully offset rapid moves.

FX and international exposure

Revenue and sourcing in Canada, Europe, and Asia expose Fortune Brands to currency translation and transaction risk, and a stronger dollar can compress reported overseas sales and inflate imported component costs. Local pricing power and natural hedges from local manufacturing reduce but do not eliminate exposure, while volatile FX makes budgeting and cross-border capital allocation more complex.

- Geographic exposure: Canada, Europe, Asia

- Risks: translation, transaction, component cost inflation

- Mitigants: local pricing power, natural hedges

- Impact: complicates budgeting and capital allocation

Retailer and distributor dynamics

Inventory normalization at major retailers has lengthened shipment timing for Fortune Brands, creating more variable order patterns and pressure on fill rates. Private-label growth compresses pricing and shelf space, forcing promotional trade-offs. Omnichannel expectations raise service-level targets and working capital needs, while strategic partnerships secure program placements and co-marketing funds.

- Inventory timing volatility

- Private-label pricing pressure

- Higher omnichannel working capital

- Partnerships lock programs/budgets

Tariffs and BIL/IRA lift demand; FY2024 sales 4.7B, supply risks rise

Housing sensitivity remains high: US housing starts ~1.4M (2024) and existing‑home sales ~4.0M (2024); 30‑yr mortgage ~7% (2024) shifts spend to ~$450B remodel market. Inflation eased to ~3% (2024) supporting premium demand; input cost volatility (copper ~$9,500/t mid‑2025, containers $2k–$3k/FEU 2024–25) pressures margins and working capital; FX exposure from Canada/Europe/Asia can compress reported sales.

| Metric | Value |

|---|---|

| US housing starts | ~1.4M (2024) |

| Remodel spend | ~$450B (2024) |

| Copper | ~$9,500/t (mid‑2025) |

Preview the Actual Deliverable

Fortune Brands PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Fortune Brands PESTLE Analysis provides concise political, economic, social, technological, legal and environmental insights tailored for strategic and investment decisions. The layout, content and recommendations are final and ready to download immediately after checkout.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and technological trends are shaping Fortune Brands' prospects in our concise PESTLE snapshot. This strategic briefing highlights risks and opportunities you can act on immediately. Purchase the full PESTLE for the complete, editable analysis and actionable intelligence.

Political factors

Trade policy and tariffs

Import duties such as the US 25% steel and 10% aluminum Section 232 tariffs and remaining US-China tariffs up to 25% can materially swing input costs for metals, resins, and finished hardware, forcing pricing adjustments. Changes in US-China relations or USMCA rules (in force since 2020) alter sourcing economics for faucets, locks, and decking components. Retaliatory tariffs have driven supplier diversification and nearshoring trends, while stable trade policy underpins predictable margins and inventory planning.

Housing and infrastructure agendas

Government incentives—notably the 2021 Bipartisan Infrastructure Law (about 55 billion for water and 110 billion for roads/bridges) and the Inflation Reduction Act (~369 billion for clean energy)—boost demand for plumbing, security, and energy-efficient building products, supporting Fortune Brands (FY2024 net sales ~4.7 billion). Public infrastructure spending and regional grants accelerate pro-channel activity, while appropriations delays or post-election policy shifts create order volatility and push SKU mix toward rebate-compliant, high-efficiency products.

“Buy American” and local content

Procurement preferences increasingly favor domestically produced fixtures, locks and decking for public projects, amplifying opportunities for Fortune Brands' Moen, Master Lock and Fiberon lines. Meeting Buy American/local content thresholds—relevant across many federal and state programs in a US procurement market roughly 700 billion USD annually (2023–24)—may require supply‑chain reconfiguration and near‑term capex. Benefits include access to government contracts and stronger US brand positioning. Non‑compliance risks bid exclusion and reputational damage.

Geopolitical supply chain exposure

Political tensions increasingly disrupt ocean freight and port operations, with Red Sea route attacks in 2023–24 prompting rerouting that raised voyage costs and added war-risk surcharges often reaching tens of thousands of dollars per transit; export controls on advanced electronics since 2023 have constrained chips and modules used in smart locks and water systems. Companies must maintain multi-region tooling and dual sourcing to mitigate single-country exposure; insurers, lead times and buffer inventory have risen materially, with some firms reporting 20–40% longer lead times and higher inventory carrying costs.

- Exposure: ocean freight route risk; ports & transshipment chokepoints

- Controls: export sanctions on electronics affecting smart products

- Mitigation: multi-region tooling, dual sourcing, regional inventories

- Costs: war-risk premiums, higher insurance, 20–40% longer lead times

State and local policy fragmentation

State and local fragmentation forces Fortune Brands to navigate 50 state regimes and 19,000+ local building departments, complicating go-to-market timing and pricing. Divergent water-use rules (eg California Title 24) and varied security/fixture standards raise certification and compliance costs and require sustained advocacy and code-tracking. Misalignment can delay product launches and shrink addressable markets.

- 50 states; 19,000+ local jurisdictions impacting approvals

- California Title 24 cited as stricter standard

- Continuous advocacy and code-tracking operationally required

- Regulatory misalignment risks launch delays and lost market access

Tariffs and BIL/IRA lift demand; FY2024 sales 4.7B, supply risks rise

Tariffs (US 25% steel, 10% aluminum; US‑China up to 25%) and trade shifts materially affect input costs and sourcing for faucets, locks and decking. US infrastructure/energy laws (BIL, IRA) and ~700B/yr public procurement boost demand; FY2024 sales ~4.7B. Port disruptions and export controls raise lead times and insurance.

| Metric | Value |

|---|---|

| FY2024 sales | 4.7B |

| US procurement | ~700B/yr |

| Tariff rates | 25%/10% |

What is included in the product

Explores how macro forces—Political, Economic, Social, Technological, Environmental and Legal—specifically shape Fortune Brands’ opportunities and risks, with data-backed trends and industry examples. Designed for executives and investors to inform strategy, scenario planning and funding narratives.

A concise, visually segmented Fortune Brands PESTLE summary that’s editable for region- or product-specific notes, drop-in ready for presentations, and easily shareable to align teams on external risks and strategy.

Economic factors

Housing cycle sensitivity

Housing-cycle sensitivity is high for Fortune Brands: US housing starts ran around 1.4M annualized in 2024 (Census) and existing-home sales near 4.0M (NAR), directly affecting volumes for Moen, Master Lock and Fiberon. Higher mortgage rates (30-yr ~7% in 2024, Freddie Mac) typically curb new construction but shift spend to repair/remodel — US remodel spending ~$450B in 2024 (JCHS). Pro-channel backlogs buffer short-term swings; security/maintenance demand is more resilient than discretionary upgrades.

Consumer discretionary spend

Real income and confidence drive mid-to-premium fixture and outdoor living demand; with inflation easing to roughly 3% in 2024 and Conference Board confidence near 100 in mid-2025, higher-end conversion remains viable. Promotional intensity at big-box and e-commerce channels can accelerate or postpone purchases and heighten trade-down risk in downturns, compressing mix. Affluent segments continue to sustain premium adoption even in softer cycles.

Commodity and freight costs

Copper (~$9,500/tonne mid‑2025), brass, stainless, zinc, resins and lumber‑derived inputs remain material drivers of Fortune Brands’ COGS, with feedstock swings and freight/container spot volatility (spot transpacific container rates ~ $2,000–$3,000 per FEU in 2024–25) causing landed‑cost unpredictability. Pricing actions typically lag input spikes, compressing gross margins; hedging and long‑term supply contracts mitigate but cannot fully offset rapid moves.

FX and international exposure

Revenue and sourcing in Canada, Europe, and Asia expose Fortune Brands to currency translation and transaction risk, and a stronger dollar can compress reported overseas sales and inflate imported component costs. Local pricing power and natural hedges from local manufacturing reduce but do not eliminate exposure, while volatile FX makes budgeting and cross-border capital allocation more complex.

- Geographic exposure: Canada, Europe, Asia

- Risks: translation, transaction, component cost inflation

- Mitigants: local pricing power, natural hedges

- Impact: complicates budgeting and capital allocation

Retailer and distributor dynamics

Inventory normalization at major retailers has lengthened shipment timing for Fortune Brands, creating more variable order patterns and pressure on fill rates. Private-label growth compresses pricing and shelf space, forcing promotional trade-offs. Omnichannel expectations raise service-level targets and working capital needs, while strategic partnerships secure program placements and co-marketing funds.

- Inventory timing volatility

- Private-label pricing pressure

- Higher omnichannel working capital

- Partnerships lock programs/budgets

Tariffs and BIL/IRA lift demand; FY2024 sales 4.7B, supply risks rise

Housing sensitivity remains high: US housing starts ~1.4M (2024) and existing‑home sales ~4.0M (2024); 30‑yr mortgage ~7% (2024) shifts spend to ~$450B remodel market. Inflation eased to ~3% (2024) supporting premium demand; input cost volatility (copper ~$9,500/t mid‑2025, containers $2k–$3k/FEU 2024–25) pressures margins and working capital; FX exposure from Canada/Europe/Asia can compress reported sales.

| Metric | Value |

|---|---|

| US housing starts | ~1.4M (2024) |

| Remodel spend | ~$450B (2024) |

| Copper | ~$9,500/t (mid‑2025) |

Preview the Actual Deliverable

Fortune Brands PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Fortune Brands PESTLE Analysis provides concise political, economic, social, technological, legal and environmental insights tailored for strategic and investment decisions. The layout, content and recommendations are final and ready to download immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and technological trends are shaping Fortune Brands' prospects in our concise PESTLE snapshot. This strategic briefing highlights risks and opportunities you can act on immediately. Purchase the full PESTLE for the complete, editable analysis and actionable intelligence.

Political factors

Trade policy and tariffs

Import duties such as the US 25% steel and 10% aluminum Section 232 tariffs and remaining US-China tariffs up to 25% can materially swing input costs for metals, resins, and finished hardware, forcing pricing adjustments. Changes in US-China relations or USMCA rules (in force since 2020) alter sourcing economics for faucets, locks, and decking components. Retaliatory tariffs have driven supplier diversification and nearshoring trends, while stable trade policy underpins predictable margins and inventory planning.

Housing and infrastructure agendas

Government incentives—notably the 2021 Bipartisan Infrastructure Law (about 55 billion for water and 110 billion for roads/bridges) and the Inflation Reduction Act (~369 billion for clean energy)—boost demand for plumbing, security, and energy-efficient building products, supporting Fortune Brands (FY2024 net sales ~4.7 billion). Public infrastructure spending and regional grants accelerate pro-channel activity, while appropriations delays or post-election policy shifts create order volatility and push SKU mix toward rebate-compliant, high-efficiency products.

“Buy American” and local content

Procurement preferences increasingly favor domestically produced fixtures, locks and decking for public projects, amplifying opportunities for Fortune Brands' Moen, Master Lock and Fiberon lines. Meeting Buy American/local content thresholds—relevant across many federal and state programs in a US procurement market roughly 700 billion USD annually (2023–24)—may require supply‑chain reconfiguration and near‑term capex. Benefits include access to government contracts and stronger US brand positioning. Non‑compliance risks bid exclusion and reputational damage.

Geopolitical supply chain exposure

Political tensions increasingly disrupt ocean freight and port operations, with Red Sea route attacks in 2023–24 prompting rerouting that raised voyage costs and added war-risk surcharges often reaching tens of thousands of dollars per transit; export controls on advanced electronics since 2023 have constrained chips and modules used in smart locks and water systems. Companies must maintain multi-region tooling and dual sourcing to mitigate single-country exposure; insurers, lead times and buffer inventory have risen materially, with some firms reporting 20–40% longer lead times and higher inventory carrying costs.

- Exposure: ocean freight route risk; ports & transshipment chokepoints

- Controls: export sanctions on electronics affecting smart products

- Mitigation: multi-region tooling, dual sourcing, regional inventories

- Costs: war-risk premiums, higher insurance, 20–40% longer lead times

State and local policy fragmentation

State and local fragmentation forces Fortune Brands to navigate 50 state regimes and 19,000+ local building departments, complicating go-to-market timing and pricing. Divergent water-use rules (eg California Title 24) and varied security/fixture standards raise certification and compliance costs and require sustained advocacy and code-tracking. Misalignment can delay product launches and shrink addressable markets.

- 50 states; 19,000+ local jurisdictions impacting approvals

- California Title 24 cited as stricter standard

- Continuous advocacy and code-tracking operationally required

- Regulatory misalignment risks launch delays and lost market access

Tariffs and BIL/IRA lift demand; FY2024 sales 4.7B, supply risks rise

Tariffs (US 25% steel, 10% aluminum; US‑China up to 25%) and trade shifts materially affect input costs and sourcing for faucets, locks and decking. US infrastructure/energy laws (BIL, IRA) and ~700B/yr public procurement boost demand; FY2024 sales ~4.7B. Port disruptions and export controls raise lead times and insurance.

| Metric | Value |

|---|---|

| FY2024 sales | 4.7B |

| US procurement | ~700B/yr |

| Tariff rates | 25%/10% |

What is included in the product

Explores how macro forces—Political, Economic, Social, Technological, Environmental and Legal—specifically shape Fortune Brands’ opportunities and risks, with data-backed trends and industry examples. Designed for executives and investors to inform strategy, scenario planning and funding narratives.

A concise, visually segmented Fortune Brands PESTLE summary that’s editable for region- or product-specific notes, drop-in ready for presentations, and easily shareable to align teams on external risks and strategy.

Economic factors

Housing cycle sensitivity

Housing-cycle sensitivity is high for Fortune Brands: US housing starts ran around 1.4M annualized in 2024 (Census) and existing-home sales near 4.0M (NAR), directly affecting volumes for Moen, Master Lock and Fiberon. Higher mortgage rates (30-yr ~7% in 2024, Freddie Mac) typically curb new construction but shift spend to repair/remodel — US remodel spending ~$450B in 2024 (JCHS). Pro-channel backlogs buffer short-term swings; security/maintenance demand is more resilient than discretionary upgrades.

Consumer discretionary spend

Real income and confidence drive mid-to-premium fixture and outdoor living demand; with inflation easing to roughly 3% in 2024 and Conference Board confidence near 100 in mid-2025, higher-end conversion remains viable. Promotional intensity at big-box and e-commerce channels can accelerate or postpone purchases and heighten trade-down risk in downturns, compressing mix. Affluent segments continue to sustain premium adoption even in softer cycles.

Commodity and freight costs

Copper (~$9,500/tonne mid‑2025), brass, stainless, zinc, resins and lumber‑derived inputs remain material drivers of Fortune Brands’ COGS, with feedstock swings and freight/container spot volatility (spot transpacific container rates ~ $2,000–$3,000 per FEU in 2024–25) causing landed‑cost unpredictability. Pricing actions typically lag input spikes, compressing gross margins; hedging and long‑term supply contracts mitigate but cannot fully offset rapid moves.

FX and international exposure

Revenue and sourcing in Canada, Europe, and Asia expose Fortune Brands to currency translation and transaction risk, and a stronger dollar can compress reported overseas sales and inflate imported component costs. Local pricing power and natural hedges from local manufacturing reduce but do not eliminate exposure, while volatile FX makes budgeting and cross-border capital allocation more complex.

- Geographic exposure: Canada, Europe, Asia

- Risks: translation, transaction, component cost inflation

- Mitigants: local pricing power, natural hedges

- Impact: complicates budgeting and capital allocation

Retailer and distributor dynamics

Inventory normalization at major retailers has lengthened shipment timing for Fortune Brands, creating more variable order patterns and pressure on fill rates. Private-label growth compresses pricing and shelf space, forcing promotional trade-offs. Omnichannel expectations raise service-level targets and working capital needs, while strategic partnerships secure program placements and co-marketing funds.

- Inventory timing volatility

- Private-label pricing pressure

- Higher omnichannel working capital

- Partnerships lock programs/budgets

Tariffs and BIL/IRA lift demand; FY2024 sales 4.7B, supply risks rise

Housing sensitivity remains high: US housing starts ~1.4M (2024) and existing‑home sales ~4.0M (2024); 30‑yr mortgage ~7% (2024) shifts spend to ~$450B remodel market. Inflation eased to ~3% (2024) supporting premium demand; input cost volatility (copper ~$9,500/t mid‑2025, containers $2k–$3k/FEU 2024–25) pressures margins and working capital; FX exposure from Canada/Europe/Asia can compress reported sales.

| Metric | Value |

|---|---|

| US housing starts | ~1.4M (2024) |

| Remodel spend | ~$450B (2024) |

| Copper | ~$9,500/t (mid‑2025) |

Preview the Actual Deliverable

Fortune Brands PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Fortune Brands PESTLE Analysis provides concise political, economic, social, technological, legal and environmental insights tailored for strategic and investment decisions. The layout, content and recommendations are final and ready to download immediately after checkout.