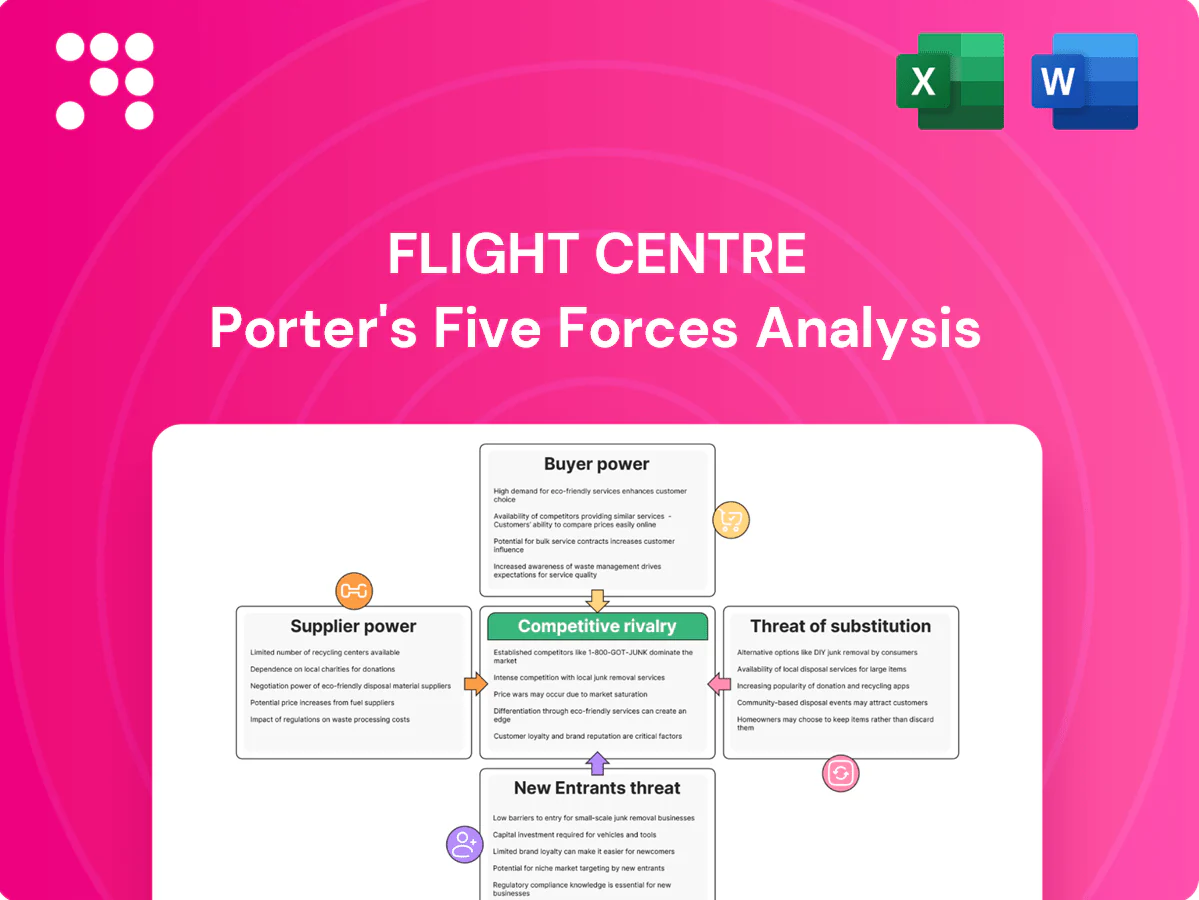

Flight Centre Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Flight Centre faces intense buyer price sensitivity, rising substitute threats from online travel platforms, moderate supplier leverage, and barriers that deter but do not block new entrants. This snapshot hints at strategic risks and opportunities. Unlock the full Porter's Five Forces analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Supplier Power 1

Airlines, hotel chains, cruise lines and car-rental firms are highly concentrated, giving suppliers pricing leverage over commissions and inventory; Amadeus and Sabre together account for roughly 70% of GDS bookings in 2024, adding dependency and fees. Flight Centre mitigates this via scale and preferred agreements and over 2,800 storefronts (2024), but peak-demand capacity constraints and ongoing disintermediation to direct channels keep supplier power elevated.

Supplier Power 2

Airline NDC and direct-connect adoption (about 30% of global seat capacity in 2024) restricts fare access and layers surcharges, pushing Flight Centre's distribution costs higher. Hotel loyalty programs now drive roughly 60% of chain bookings direct, shrinking allocable inventory to intermediaries. Cruise lines tightly control cabin allotments and co-op marketing funds, skewing margin splits, while negotiated consortia rates (covering ~10–15% of bookings) partially offset but remain cyclical.

Supplier Power 3

Insurance underwriters and ancillary providers set product terms that directly affect attach rates and commission levels, constraining Flight Centre’s margins; currency and fuel surcharges from airlines and ground suppliers are typically passed through to customers but can compress package value propositions during volatility. Payment networks and chargebacks add settlement costs and cashflow timing risk. Multi-year preferred supplier deals stabilize margins but reduce procurement flexibility.

Supplier Power 4

Limited air capacity on key routes elevates supplier power during recovery surges and disruptions, while blackout dates and airline yield management restrict agencies’ ability to offer discounts; exclusive supplier direct-channel promotions further undercut agency offers. Flight Centre’s global procurement secures block space and negotiated fares, but supplier leverage remains significant and not fully mitigated.

- Supplier concentration

- Blackout & yield controls

- Direct-channel promos

- Block-space mitigate, not eliminate

Supplier Power 5

Technology-stack reliance on GDS, APIs and aggregators creates switching costs and fee exposure, with ~80% of corporate bookings routed via major GDSs (2024), enabling suppliers to extract commissions. Strong-branded suppliers use co-op marketing to secure shelf space, and data-sharing clauses can enable suppliers to monetize direct channels. Diversifying content sources and white-label deals cuts concentration risk.

- GDS concentration ~80%

- Co-op marketing drives visibility

- Data-sharing = supplier monetization

- White-labels reduce supplier risk

Concentrated suppliers and direct channels squeeze intermediary margins despite scale

Suppliers (airlines, hotels, GDSs) hold high leverage due to concentration and capacity control, raising fees and limiting inventory access for Flight Centre. Direct channels and NDC (~30% global seat capacity in 2024) plus hotel loyalty (~60% direct bookings) squeeze intermediary margins. Flight Centre scale (≈2,800 storefronts, 2024) and preferred deals mitigate but do not remove supplier power.

| Metric | 2024 |

|---|---|

| Amadeus+Sabre GDS share | ~70% |

| Corporate bookings via GDS | ~80% |

| NDC/direct seat capacity | ~30% |

| Hotel direct via loyalty | ~60% |

| Flight Centre storefronts | ≈2,800 |

What is included in the product

Tailored Porter's Five Forces analysis for Flight Centre uncovering key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and disruptive forces that challenge market share; detailed, strategic insights designed for easy inclusion in investor materials, internal strategy decks or academic reports.

A one-sheet Porter's Five Forces for Flight Centre that visualizes competitive pressure with a radar chart and customizable scores—ideal for quick board decisions; plug in your own data, duplicate tabs for scenario analysis, and export slides without macros.

Customers Bargaining Power

Buyer Power 1

Consumers face high price transparency as OTAs and metasearch captured about 50% of online flight bookings in 2024, boosting buyer power. Low switching costs for leisure travelers make price the primary decision factor. Reviews and social proof—with roughly 70% of travelers consulting reviews in 2024—heighten sensitivity to price and service. Flight Centre mitigates this via bundled packages, adviser expertise and service guarantees.

Buyer Power 2

Corporate clients drive intense buyer power via RFPs with SLAs and volume pricing, demanding duty-of-care, reporting and policy control that raise service complexity; consolidated buyers increasingly multi-source or re-tender, boosting leverage, while differentiated TMC tech and account management can command premiums—global business travel spend estimated at about USD 1.4 trillion in 2024.

Buyer Power 3

Airlines and hotel loyalty programs pull buyers toward direct channels, and IATA reported in 2024 that direct distribution accounted for over half of airline ticket sales, reducing intermediary reliance.

Credit card rewards and status tiers further lock customers into direct ecosystems, pressuring OTAs and agents.

Flight Centre’s loyalty initiatives and tailored perks can partly offset this, so value-added services and bespoke advisory fees become critical to retain share.

Buyer Power 4

Buyer Power 4: Large MICE and group buyers, driving part of the ~USD 1.4 trillion 2024 global business-travel market, have seasonal, negotiable demand and use flexible dates/venues to extract concessions. Cancellation terms and risk-sharing are key levers; packaging air, hotel and events improves economics and client stickiness.

- High spend: seasonal leverage

- Key levers: cancellations & risk-share

- Strategy: bundle air+hotel+events

Buyer Power 5

SMB buyers (World Bank 2024: SMEs ≈90% of businesses) are price-sensitive and seek simple tools, yet remain service-dependent; DIY digital options raise alternatives while support during disruptions retains loyalty. Transparent fees and fast-response service lower churn; cross-selling insurance and ancillaries helps offset margin pressure for Flight Centre.

- SMB price-driven

- DIY digital alternatives

- Support retains loyalty

- Transparent fees cut churn

- Cross-sell boosts margins

High transparency (~50% OTAs) and reviews (~70%) strengthen buyer power vs direct airline sales

High price transparency (OTAs/metasearch ~50% online bookings 2024) and review use (~70% consult reviews 2024) increase buyer power. Corporate buyers (global business travel ≈USD1.4T 2024) extract volume discounts and SLAs. Direct airline sales >50% (IATA 2024) and card loyalty raise switching costs. Flight Centre offsets via bundles, adviser fees and loyalty perks.

| Metric | 2024 |

|---|---|

| OTA share | ~50% |

| Review consult | ~70% |

| Business travel | USD 1.4T |

| Direct airline sales | >50% |

Same Document Delivered

Flight Centre Porter's Five Forces Analysis

This preview shows the exact Flight Centre Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the final, professionally formatted file and includes the full competitive intensity assessment, forces breakdown, and strategic implications. You're looking at the actual deliverable; once you buy, you'll get instant access to this identical file. No mockups or samples—what you see is what you download.

A Must-Have Tool for Decision-Makers

Flight Centre faces intense buyer price sensitivity, rising substitute threats from online travel platforms, moderate supplier leverage, and barriers that deter but do not block new entrants. This snapshot hints at strategic risks and opportunities. Unlock the full Porter's Five Forces analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Supplier Power 1

Airlines, hotel chains, cruise lines and car-rental firms are highly concentrated, giving suppliers pricing leverage over commissions and inventory; Amadeus and Sabre together account for roughly 70% of GDS bookings in 2024, adding dependency and fees. Flight Centre mitigates this via scale and preferred agreements and over 2,800 storefronts (2024), but peak-demand capacity constraints and ongoing disintermediation to direct channels keep supplier power elevated.

Supplier Power 2

Airline NDC and direct-connect adoption (about 30% of global seat capacity in 2024) restricts fare access and layers surcharges, pushing Flight Centre's distribution costs higher. Hotel loyalty programs now drive roughly 60% of chain bookings direct, shrinking allocable inventory to intermediaries. Cruise lines tightly control cabin allotments and co-op marketing funds, skewing margin splits, while negotiated consortia rates (covering ~10–15% of bookings) partially offset but remain cyclical.

Supplier Power 3

Insurance underwriters and ancillary providers set product terms that directly affect attach rates and commission levels, constraining Flight Centre’s margins; currency and fuel surcharges from airlines and ground suppliers are typically passed through to customers but can compress package value propositions during volatility. Payment networks and chargebacks add settlement costs and cashflow timing risk. Multi-year preferred supplier deals stabilize margins but reduce procurement flexibility.

Supplier Power 4

Limited air capacity on key routes elevates supplier power during recovery surges and disruptions, while blackout dates and airline yield management restrict agencies’ ability to offer discounts; exclusive supplier direct-channel promotions further undercut agency offers. Flight Centre’s global procurement secures block space and negotiated fares, but supplier leverage remains significant and not fully mitigated.

- Supplier concentration

- Blackout & yield controls

- Direct-channel promos

- Block-space mitigate, not eliminate

Supplier Power 5

Technology-stack reliance on GDS, APIs and aggregators creates switching costs and fee exposure, with ~80% of corporate bookings routed via major GDSs (2024), enabling suppliers to extract commissions. Strong-branded suppliers use co-op marketing to secure shelf space, and data-sharing clauses can enable suppliers to monetize direct channels. Diversifying content sources and white-label deals cuts concentration risk.

- GDS concentration ~80%

- Co-op marketing drives visibility

- Data-sharing = supplier monetization

- White-labels reduce supplier risk

Concentrated suppliers and direct channels squeeze intermediary margins despite scale

Suppliers (airlines, hotels, GDSs) hold high leverage due to concentration and capacity control, raising fees and limiting inventory access for Flight Centre. Direct channels and NDC (~30% global seat capacity in 2024) plus hotel loyalty (~60% direct bookings) squeeze intermediary margins. Flight Centre scale (≈2,800 storefronts, 2024) and preferred deals mitigate but do not remove supplier power.

| Metric | 2024 |

|---|---|

| Amadeus+Sabre GDS share | ~70% |

| Corporate bookings via GDS | ~80% |

| NDC/direct seat capacity | ~30% |

| Hotel direct via loyalty | ~60% |

| Flight Centre storefronts | ≈2,800 |

What is included in the product

Tailored Porter's Five Forces analysis for Flight Centre uncovering key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and disruptive forces that challenge market share; detailed, strategic insights designed for easy inclusion in investor materials, internal strategy decks or academic reports.

A one-sheet Porter's Five Forces for Flight Centre that visualizes competitive pressure with a radar chart and customizable scores—ideal for quick board decisions; plug in your own data, duplicate tabs for scenario analysis, and export slides without macros.

Customers Bargaining Power

Buyer Power 1

Consumers face high price transparency as OTAs and metasearch captured about 50% of online flight bookings in 2024, boosting buyer power. Low switching costs for leisure travelers make price the primary decision factor. Reviews and social proof—with roughly 70% of travelers consulting reviews in 2024—heighten sensitivity to price and service. Flight Centre mitigates this via bundled packages, adviser expertise and service guarantees.

Buyer Power 2

Corporate clients drive intense buyer power via RFPs with SLAs and volume pricing, demanding duty-of-care, reporting and policy control that raise service complexity; consolidated buyers increasingly multi-source or re-tender, boosting leverage, while differentiated TMC tech and account management can command premiums—global business travel spend estimated at about USD 1.4 trillion in 2024.

Buyer Power 3

Airlines and hotel loyalty programs pull buyers toward direct channels, and IATA reported in 2024 that direct distribution accounted for over half of airline ticket sales, reducing intermediary reliance.

Credit card rewards and status tiers further lock customers into direct ecosystems, pressuring OTAs and agents.

Flight Centre’s loyalty initiatives and tailored perks can partly offset this, so value-added services and bespoke advisory fees become critical to retain share.

Buyer Power 4

Buyer Power 4: Large MICE and group buyers, driving part of the ~USD 1.4 trillion 2024 global business-travel market, have seasonal, negotiable demand and use flexible dates/venues to extract concessions. Cancellation terms and risk-sharing are key levers; packaging air, hotel and events improves economics and client stickiness.

- High spend: seasonal leverage

- Key levers: cancellations & risk-share

- Strategy: bundle air+hotel+events

Buyer Power 5

SMB buyers (World Bank 2024: SMEs ≈90% of businesses) are price-sensitive and seek simple tools, yet remain service-dependent; DIY digital options raise alternatives while support during disruptions retains loyalty. Transparent fees and fast-response service lower churn; cross-selling insurance and ancillaries helps offset margin pressure for Flight Centre.

- SMB price-driven

- DIY digital alternatives

- Support retains loyalty

- Transparent fees cut churn

- Cross-sell boosts margins

High transparency (~50% OTAs) and reviews (~70%) strengthen buyer power vs direct airline sales

High price transparency (OTAs/metasearch ~50% online bookings 2024) and review use (~70% consult reviews 2024) increase buyer power. Corporate buyers (global business travel ≈USD1.4T 2024) extract volume discounts and SLAs. Direct airline sales >50% (IATA 2024) and card loyalty raise switching costs. Flight Centre offsets via bundles, adviser fees and loyalty perks.

| Metric | 2024 |

|---|---|

| OTA share | ~50% |

| Review consult | ~70% |

| Business travel | USD 1.4T |

| Direct airline sales | >50% |

Same Document Delivered

Flight Centre Porter's Five Forces Analysis

This preview shows the exact Flight Centre Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the final, professionally formatted file and includes the full competitive intensity assessment, forces breakdown, and strategic implications. You're looking at the actual deliverable; once you buy, you'll get instant access to this identical file. No mockups or samples—what you see is what you download.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Flight Centre faces intense buyer price sensitivity, rising substitute threats from online travel platforms, moderate supplier leverage, and barriers that deter but do not block new entrants. This snapshot hints at strategic risks and opportunities. Unlock the full Porter's Five Forces analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Supplier Power 1

Airlines, hotel chains, cruise lines and car-rental firms are highly concentrated, giving suppliers pricing leverage over commissions and inventory; Amadeus and Sabre together account for roughly 70% of GDS bookings in 2024, adding dependency and fees. Flight Centre mitigates this via scale and preferred agreements and over 2,800 storefronts (2024), but peak-demand capacity constraints and ongoing disintermediation to direct channels keep supplier power elevated.

Supplier Power 2

Airline NDC and direct-connect adoption (about 30% of global seat capacity in 2024) restricts fare access and layers surcharges, pushing Flight Centre's distribution costs higher. Hotel loyalty programs now drive roughly 60% of chain bookings direct, shrinking allocable inventory to intermediaries. Cruise lines tightly control cabin allotments and co-op marketing funds, skewing margin splits, while negotiated consortia rates (covering ~10–15% of bookings) partially offset but remain cyclical.

Supplier Power 3

Insurance underwriters and ancillary providers set product terms that directly affect attach rates and commission levels, constraining Flight Centre’s margins; currency and fuel surcharges from airlines and ground suppliers are typically passed through to customers but can compress package value propositions during volatility. Payment networks and chargebacks add settlement costs and cashflow timing risk. Multi-year preferred supplier deals stabilize margins but reduce procurement flexibility.

Supplier Power 4

Limited air capacity on key routes elevates supplier power during recovery surges and disruptions, while blackout dates and airline yield management restrict agencies’ ability to offer discounts; exclusive supplier direct-channel promotions further undercut agency offers. Flight Centre’s global procurement secures block space and negotiated fares, but supplier leverage remains significant and not fully mitigated.

- Supplier concentration

- Blackout & yield controls

- Direct-channel promos

- Block-space mitigate, not eliminate

Supplier Power 5

Technology-stack reliance on GDS, APIs and aggregators creates switching costs and fee exposure, with ~80% of corporate bookings routed via major GDSs (2024), enabling suppliers to extract commissions. Strong-branded suppliers use co-op marketing to secure shelf space, and data-sharing clauses can enable suppliers to monetize direct channels. Diversifying content sources and white-label deals cuts concentration risk.

- GDS concentration ~80%

- Co-op marketing drives visibility

- Data-sharing = supplier monetization

- White-labels reduce supplier risk

Concentrated suppliers and direct channels squeeze intermediary margins despite scale

Suppliers (airlines, hotels, GDSs) hold high leverage due to concentration and capacity control, raising fees and limiting inventory access for Flight Centre. Direct channels and NDC (~30% global seat capacity in 2024) plus hotel loyalty (~60% direct bookings) squeeze intermediary margins. Flight Centre scale (≈2,800 storefronts, 2024) and preferred deals mitigate but do not remove supplier power.

| Metric | 2024 |

|---|---|

| Amadeus+Sabre GDS share | ~70% |

| Corporate bookings via GDS | ~80% |

| NDC/direct seat capacity | ~30% |

| Hotel direct via loyalty | ~60% |

| Flight Centre storefronts | ≈2,800 |

What is included in the product

Tailored Porter's Five Forces analysis for Flight Centre uncovering key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and disruptive forces that challenge market share; detailed, strategic insights designed for easy inclusion in investor materials, internal strategy decks or academic reports.

A one-sheet Porter's Five Forces for Flight Centre that visualizes competitive pressure with a radar chart and customizable scores—ideal for quick board decisions; plug in your own data, duplicate tabs for scenario analysis, and export slides without macros.

Customers Bargaining Power

Buyer Power 1

Consumers face high price transparency as OTAs and metasearch captured about 50% of online flight bookings in 2024, boosting buyer power. Low switching costs for leisure travelers make price the primary decision factor. Reviews and social proof—with roughly 70% of travelers consulting reviews in 2024—heighten sensitivity to price and service. Flight Centre mitigates this via bundled packages, adviser expertise and service guarantees.

Buyer Power 2

Corporate clients drive intense buyer power via RFPs with SLAs and volume pricing, demanding duty-of-care, reporting and policy control that raise service complexity; consolidated buyers increasingly multi-source or re-tender, boosting leverage, while differentiated TMC tech and account management can command premiums—global business travel spend estimated at about USD 1.4 trillion in 2024.

Buyer Power 3

Airlines and hotel loyalty programs pull buyers toward direct channels, and IATA reported in 2024 that direct distribution accounted for over half of airline ticket sales, reducing intermediary reliance.

Credit card rewards and status tiers further lock customers into direct ecosystems, pressuring OTAs and agents.

Flight Centre’s loyalty initiatives and tailored perks can partly offset this, so value-added services and bespoke advisory fees become critical to retain share.

Buyer Power 4

Buyer Power 4: Large MICE and group buyers, driving part of the ~USD 1.4 trillion 2024 global business-travel market, have seasonal, negotiable demand and use flexible dates/venues to extract concessions. Cancellation terms and risk-sharing are key levers; packaging air, hotel and events improves economics and client stickiness.

- High spend: seasonal leverage

- Key levers: cancellations & risk-share

- Strategy: bundle air+hotel+events

Buyer Power 5

SMB buyers (World Bank 2024: SMEs ≈90% of businesses) are price-sensitive and seek simple tools, yet remain service-dependent; DIY digital options raise alternatives while support during disruptions retains loyalty. Transparent fees and fast-response service lower churn; cross-selling insurance and ancillaries helps offset margin pressure for Flight Centre.

- SMB price-driven

- DIY digital alternatives

- Support retains loyalty

- Transparent fees cut churn

- Cross-sell boosts margins

High transparency (~50% OTAs) and reviews (~70%) strengthen buyer power vs direct airline sales

High price transparency (OTAs/metasearch ~50% online bookings 2024) and review use (~70% consult reviews 2024) increase buyer power. Corporate buyers (global business travel ≈USD1.4T 2024) extract volume discounts and SLAs. Direct airline sales >50% (IATA 2024) and card loyalty raise switching costs. Flight Centre offsets via bundles, adviser fees and loyalty perks.

| Metric | 2024 |

|---|---|

| OTA share | ~50% |

| Review consult | ~70% |

| Business travel | USD 1.4T |

| Direct airline sales | >50% |

Same Document Delivered

Flight Centre Porter's Five Forces Analysis

This preview shows the exact Flight Centre Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the final, professionally formatted file and includes the full competitive intensity assessment, forces breakdown, and strategic implications. You're looking at the actual deliverable; once you buy, you'll get instant access to this identical file. No mockups or samples—what you see is what you download.