Federal Bank Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

Curious how Federal Bank’s businesses stack up—Stars, Cash Cows, Dogs, or Question Marks? This quick look teases the story, but the full BCG Matrix delivers quadrant-level clarity, data-backed recommendations, and a ready-to-use strategy you can act on. Buy the complete report for a detailed Word write-up plus an Excel summary—so you can present, decide, and allocate capital with confidence. Get instant access and stop guessing; plan with precision.

Stars

Digital payments & mobile banking

Explosive UPI adoption — over 10 billion monthly transactions in 2024 (NPCI) — keeps pulling new customers into digital payments, where Federal’s upgraded app now provides a clear competitive edge. High daily activity, strong retention and embedded cross‑sell hooks give Federal muscle in a still‑expanding market. Continued investment in UX, security and data‑led nudges should defend share and convert scale into durable fee income.

NRI banking & remittance corridors

Federal Bank’s deep Gulf–India franchise anchors its NRI deposits and remittance flows, leveraging India’s position as the world’s largest remittance recipient (World Bank) and heavy Gulf corridor volumes. Volumes are rising with steady migration and wage growth, and trust acts as a moat. Double down on corridor partnerships, faster settlements, and tailored NR products to protect share now and convert into durable low‑cost funding later.

SME lending in core markets

Strong local relationships and fast turnaround let Federal Bank capture share in an MSME segment that contributes roughly 30% of India’s GDP and about 45% of exports. Data‑backed underwriting and a secured book with collateral focus keep credit risk contained. Scale supply‑chain programs and cash‑flow lending to widen the funnel. The franchise effect compounds if service quality stays sharp.

Gold loans with digital journeys

Gold loans with digital journeys are a Star for Federal Bank: healthy demand and sub-30‑minute disbursals drive double‑digit portfolio growth, while recoveries remain resilient, making it a scalable growth engine; India’s gold loan outstanding stood near Rs 3.15 lakh crore in 2024, underscoring market depth.

Branch reach plus app workflows are winning share from NBFCs; optimize pricing by risk tier and shorten top‑up cycles to lock loyalty, while maintaining vigilant risk controls as volumes climb.

- Healthy demand: rising market (~Rs 3.15L cr, 2024)

- Speed: sub‑30 min digital disbursals

- Strategy: tiered pricing + shorter top‑ups

- Risk: tighten controls as volumes scale

API-led corporate collections

API-led corporate collections are a Star for Federal Bank: CXO teams want real-time cash visibility and instant reconciliation, and Federal’s APIs meet that need—supporting over $5bn monthly corporate flows and ~40% YoY API growth in 2024. The fee pool is fast-growing and sticky; keep building ERP connectors and 12 industry templates to scale, land logos now, monetize VAS later.

- Real-time visibility

- Sticky integrations

- ERP connectors + templates

- Land logos → monetize VAS

UPI scale, MSME lending, gold loans & APIs - invest UX, ERP to lock durable fees

UPI 10bn/mo (NPCI 2024) and app upgrades drive high retention and fee upsell; MSME (≈30% GDP) lending shows tight credit controls and scale; gold loans market ≈Rs 3.15L cr (2024) with sub‑30min disbursals; API corporate flows ~$5bn/mo with ~40% YoY growth—invest in UX, data, corridor partnerships, ERP connectors to convert scale to durable fees.

| Business | 2024 Metric | Opportunity | Priority |

|---|---|---|---|

| Digital/UPI | 10bn tx/mo | fee income | UX/security |

| MSME | ~30% GDP | cash‑flow lending | scale programs |

| Gold loans | Rs 3.15L cr | fast disburse | tiered pricing |

| APIs | $5bn/mo, +40% YoY | VAS monetization | ERP connectors |

What is included in the product

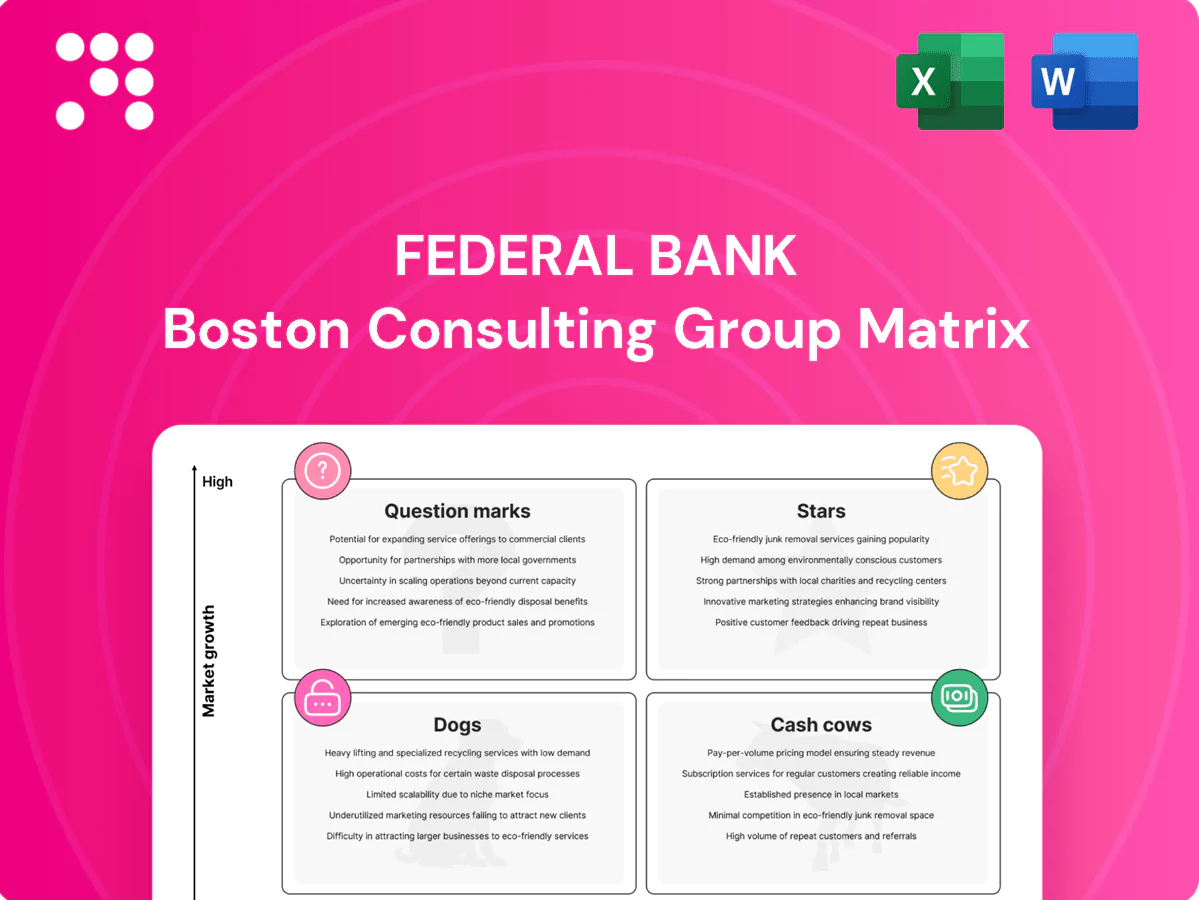

Comprehensive BCG Matrix review of Federal Bank, spotting Stars, Cash Cows, Question Marks and Dogs with strategic recommendations.

One-page BCG matrix for Federal Bank placing units in quadrants to spot priorities and cut decision friction.

Cash Cows

CASA deposits in legacy strongholds

Sticky retail CASA in legacy Kerala strongholds funds the engine: CASA deposits stood at Rs 1.06 lakh crore with a CASA ratio of 40.6% at Mar 2024, delivering low servicing costs and predictable cash flows. Growth is modest but margins remain solid versus term deposits. Maintain relationship programs and light-touch engagement; targeted tech spends to cut churn will pay back quickly.

Home loans to prime salaried

Home loans to prime salaried are a mature, competitive segment for Federal Bank that delivers steady volumes and low credit losses, underpinning dependable margins. Cross‑selling insurance and high auto‑debit repayment rates keep economics healthy, while focus on straight‑through processing and low acquisition cost reduces unit economics. Strategy: milk the book in 2024 while staying selective on pricing and underwriting.

Treasury & fixed‑income book

Treasury & fixed-income book delivers stable earnings via duration management and liquidity deployment, cushioning cycles; India 10-year G-sec hovered ~7.3% in 2024 supporting carry. Tight risk limits and cost discipline kept spreads near 80–120 bps on corporate paper; analytics-driven trading and model tweaks can extract incremental 5–15 bps without major capex.

Transaction banking fees

Transaction banking fees from CMS, payroll and bulk payments deliver steady, recurring low-touch revenue for Federal Bank; industry retention for embedded payroll/CMS clients exceeds 85% and growth is moderate, supporting predictable fee income in 2024.

Tight SLAs and rational pricing preserve margins; light add-ons such as real-time alerts and payments analytics typically lift ARPU by 10–20%, per 2024 sector benchmarks.

- Recurring low-touch fees: stable cash cow

- Retention: >85% once embedded

- Growth: moderate; focus on SLAs/pricing

- Add-ons: alerts/analytics → +10–20% ARPU

ATM and branch cash services

ATM and branch cash services show mature, predictable utilization in cash-heavy pockets; Federal Bank maintains a stable footprint with approximately 1,300 branches and 1,500 ATMs in 2024, driving steady fee and interchange revenue while opex is well understood. Focus: optimize footprint, migrate low-value transactions to digital channels; treat as harvest, not a growth bet.

- Utilization: mature, predictable

- Network: ~1,300 branches / ~1,500 ATMs (2024)

- Opex: known; revenue: steady ticks

- Strategic action: optimize footprint, digitize low-value activity

- Positioning: harvest play

Sticky CASA funds low-cost lending; harvest efficiency, reduce churn

Sticky retail CASA (Rs 1.06 lakh crore; CASA 40.6% at Mar 2024) funds low-cost lending; home loans to prime salaried deliver steady volumes and low losses; treasury carry (India 10y ~7.3% in 2024) cushions earnings; transaction banking, branches/ATMs (~1,300 branches, ~1,500 ATMs) and cash services provide predictable fee income—focus on harvest, efficiency and selective tech to reduce churn.

| Metric | 2024 |

|---|---|

| CASA | Rs 1.06L cr (40.6%) |

| Branches/ATMs | ~1,300 / ~1,500 |

| India 10y | ~7.3% |

What You See Is What You Get

Federal Bank BCG Matrix

The Federal Bank BCG Matrix you’re previewing here is the exact file you’ll receive after purchase. No watermarks, no placeholders—just the finished, professionally formatted analysis ready for strategy sessions. Buy once and download immediately; the full document is editable, printable, and presentation-ready. No surprises, just clear insights tailored for Federal Bank decision-making.

Visual. Strategic. Downloadable.

Curious how Federal Bank’s businesses stack up—Stars, Cash Cows, Dogs, or Question Marks? This quick look teases the story, but the full BCG Matrix delivers quadrant-level clarity, data-backed recommendations, and a ready-to-use strategy you can act on. Buy the complete report for a detailed Word write-up plus an Excel summary—so you can present, decide, and allocate capital with confidence. Get instant access and stop guessing; plan with precision.

Stars

Digital payments & mobile banking

Explosive UPI adoption — over 10 billion monthly transactions in 2024 (NPCI) — keeps pulling new customers into digital payments, where Federal’s upgraded app now provides a clear competitive edge. High daily activity, strong retention and embedded cross‑sell hooks give Federal muscle in a still‑expanding market. Continued investment in UX, security and data‑led nudges should defend share and convert scale into durable fee income.

NRI banking & remittance corridors

Federal Bank’s deep Gulf–India franchise anchors its NRI deposits and remittance flows, leveraging India’s position as the world’s largest remittance recipient (World Bank) and heavy Gulf corridor volumes. Volumes are rising with steady migration and wage growth, and trust acts as a moat. Double down on corridor partnerships, faster settlements, and tailored NR products to protect share now and convert into durable low‑cost funding later.

SME lending in core markets

Strong local relationships and fast turnaround let Federal Bank capture share in an MSME segment that contributes roughly 30% of India’s GDP and about 45% of exports. Data‑backed underwriting and a secured book with collateral focus keep credit risk contained. Scale supply‑chain programs and cash‑flow lending to widen the funnel. The franchise effect compounds if service quality stays sharp.

Gold loans with digital journeys

Gold loans with digital journeys are a Star for Federal Bank: healthy demand and sub-30‑minute disbursals drive double‑digit portfolio growth, while recoveries remain resilient, making it a scalable growth engine; India’s gold loan outstanding stood near Rs 3.15 lakh crore in 2024, underscoring market depth.

Branch reach plus app workflows are winning share from NBFCs; optimize pricing by risk tier and shorten top‑up cycles to lock loyalty, while maintaining vigilant risk controls as volumes climb.

- Healthy demand: rising market (~Rs 3.15L cr, 2024)

- Speed: sub‑30 min digital disbursals

- Strategy: tiered pricing + shorter top‑ups

- Risk: tighten controls as volumes scale

API-led corporate collections

API-led corporate collections are a Star for Federal Bank: CXO teams want real-time cash visibility and instant reconciliation, and Federal’s APIs meet that need—supporting over $5bn monthly corporate flows and ~40% YoY API growth in 2024. The fee pool is fast-growing and sticky; keep building ERP connectors and 12 industry templates to scale, land logos now, monetize VAS later.

- Real-time visibility

- Sticky integrations

- ERP connectors + templates

- Land logos → monetize VAS

UPI scale, MSME lending, gold loans & APIs - invest UX, ERP to lock durable fees

UPI 10bn/mo (NPCI 2024) and app upgrades drive high retention and fee upsell; MSME (≈30% GDP) lending shows tight credit controls and scale; gold loans market ≈Rs 3.15L cr (2024) with sub‑30min disbursals; API corporate flows ~$5bn/mo with ~40% YoY growth—invest in UX, data, corridor partnerships, ERP connectors to convert scale to durable fees.

| Business | 2024 Metric | Opportunity | Priority |

|---|---|---|---|

| Digital/UPI | 10bn tx/mo | fee income | UX/security |

| MSME | ~30% GDP | cash‑flow lending | scale programs |

| Gold loans | Rs 3.15L cr | fast disburse | tiered pricing |

| APIs | $5bn/mo, +40% YoY | VAS monetization | ERP connectors |

What is included in the product

Comprehensive BCG Matrix review of Federal Bank, spotting Stars, Cash Cows, Question Marks and Dogs with strategic recommendations.

One-page BCG matrix for Federal Bank placing units in quadrants to spot priorities and cut decision friction.

Cash Cows

CASA deposits in legacy strongholds

Sticky retail CASA in legacy Kerala strongholds funds the engine: CASA deposits stood at Rs 1.06 lakh crore with a CASA ratio of 40.6% at Mar 2024, delivering low servicing costs and predictable cash flows. Growth is modest but margins remain solid versus term deposits. Maintain relationship programs and light-touch engagement; targeted tech spends to cut churn will pay back quickly.

Home loans to prime salaried

Home loans to prime salaried are a mature, competitive segment for Federal Bank that delivers steady volumes and low credit losses, underpinning dependable margins. Cross‑selling insurance and high auto‑debit repayment rates keep economics healthy, while focus on straight‑through processing and low acquisition cost reduces unit economics. Strategy: milk the book in 2024 while staying selective on pricing and underwriting.

Treasury & fixed‑income book

Treasury & fixed-income book delivers stable earnings via duration management and liquidity deployment, cushioning cycles; India 10-year G-sec hovered ~7.3% in 2024 supporting carry. Tight risk limits and cost discipline kept spreads near 80–120 bps on corporate paper; analytics-driven trading and model tweaks can extract incremental 5–15 bps without major capex.

Transaction banking fees

Transaction banking fees from CMS, payroll and bulk payments deliver steady, recurring low-touch revenue for Federal Bank; industry retention for embedded payroll/CMS clients exceeds 85% and growth is moderate, supporting predictable fee income in 2024.

Tight SLAs and rational pricing preserve margins; light add-ons such as real-time alerts and payments analytics typically lift ARPU by 10–20%, per 2024 sector benchmarks.

- Recurring low-touch fees: stable cash cow

- Retention: >85% once embedded

- Growth: moderate; focus on SLAs/pricing

- Add-ons: alerts/analytics → +10–20% ARPU

ATM and branch cash services

ATM and branch cash services show mature, predictable utilization in cash-heavy pockets; Federal Bank maintains a stable footprint with approximately 1,300 branches and 1,500 ATMs in 2024, driving steady fee and interchange revenue while opex is well understood. Focus: optimize footprint, migrate low-value transactions to digital channels; treat as harvest, not a growth bet.

- Utilization: mature, predictable

- Network: ~1,300 branches / ~1,500 ATMs (2024)

- Opex: known; revenue: steady ticks

- Strategic action: optimize footprint, digitize low-value activity

- Positioning: harvest play

Sticky CASA funds low-cost lending; harvest efficiency, reduce churn

Sticky retail CASA (Rs 1.06 lakh crore; CASA 40.6% at Mar 2024) funds low-cost lending; home loans to prime salaried deliver steady volumes and low losses; treasury carry (India 10y ~7.3% in 2024) cushions earnings; transaction banking, branches/ATMs (~1,300 branches, ~1,500 ATMs) and cash services provide predictable fee income—focus on harvest, efficiency and selective tech to reduce churn.

| Metric | 2024 |

|---|---|

| CASA | Rs 1.06L cr (40.6%) |

| Branches/ATMs | ~1,300 / ~1,500 |

| India 10y | ~7.3% |

What You See Is What You Get

Federal Bank BCG Matrix

The Federal Bank BCG Matrix you’re previewing here is the exact file you’ll receive after purchase. No watermarks, no placeholders—just the finished, professionally formatted analysis ready for strategy sessions. Buy once and download immediately; the full document is editable, printable, and presentation-ready. No surprises, just clear insights tailored for Federal Bank decision-making.

Description

Visual. Strategic. Downloadable.

Curious how Federal Bank’s businesses stack up—Stars, Cash Cows, Dogs, or Question Marks? This quick look teases the story, but the full BCG Matrix delivers quadrant-level clarity, data-backed recommendations, and a ready-to-use strategy you can act on. Buy the complete report for a detailed Word write-up plus an Excel summary—so you can present, decide, and allocate capital with confidence. Get instant access and stop guessing; plan with precision.

Stars

Digital payments & mobile banking

Explosive UPI adoption — over 10 billion monthly transactions in 2024 (NPCI) — keeps pulling new customers into digital payments, where Federal’s upgraded app now provides a clear competitive edge. High daily activity, strong retention and embedded cross‑sell hooks give Federal muscle in a still‑expanding market. Continued investment in UX, security and data‑led nudges should defend share and convert scale into durable fee income.

NRI banking & remittance corridors

Federal Bank’s deep Gulf–India franchise anchors its NRI deposits and remittance flows, leveraging India’s position as the world’s largest remittance recipient (World Bank) and heavy Gulf corridor volumes. Volumes are rising with steady migration and wage growth, and trust acts as a moat. Double down on corridor partnerships, faster settlements, and tailored NR products to protect share now and convert into durable low‑cost funding later.

SME lending in core markets

Strong local relationships and fast turnaround let Federal Bank capture share in an MSME segment that contributes roughly 30% of India’s GDP and about 45% of exports. Data‑backed underwriting and a secured book with collateral focus keep credit risk contained. Scale supply‑chain programs and cash‑flow lending to widen the funnel. The franchise effect compounds if service quality stays sharp.

Gold loans with digital journeys

Gold loans with digital journeys are a Star for Federal Bank: healthy demand and sub-30‑minute disbursals drive double‑digit portfolio growth, while recoveries remain resilient, making it a scalable growth engine; India’s gold loan outstanding stood near Rs 3.15 lakh crore in 2024, underscoring market depth.

Branch reach plus app workflows are winning share from NBFCs; optimize pricing by risk tier and shorten top‑up cycles to lock loyalty, while maintaining vigilant risk controls as volumes climb.

- Healthy demand: rising market (~Rs 3.15L cr, 2024)

- Speed: sub‑30 min digital disbursals

- Strategy: tiered pricing + shorter top‑ups

- Risk: tighten controls as volumes scale

API-led corporate collections

API-led corporate collections are a Star for Federal Bank: CXO teams want real-time cash visibility and instant reconciliation, and Federal’s APIs meet that need—supporting over $5bn monthly corporate flows and ~40% YoY API growth in 2024. The fee pool is fast-growing and sticky; keep building ERP connectors and 12 industry templates to scale, land logos now, monetize VAS later.

- Real-time visibility

- Sticky integrations

- ERP connectors + templates

- Land logos → monetize VAS

UPI scale, MSME lending, gold loans & APIs - invest UX, ERP to lock durable fees

UPI 10bn/mo (NPCI 2024) and app upgrades drive high retention and fee upsell; MSME (≈30% GDP) lending shows tight credit controls and scale; gold loans market ≈Rs 3.15L cr (2024) with sub‑30min disbursals; API corporate flows ~$5bn/mo with ~40% YoY growth—invest in UX, data, corridor partnerships, ERP connectors to convert scale to durable fees.

| Business | 2024 Metric | Opportunity | Priority |

|---|---|---|---|

| Digital/UPI | 10bn tx/mo | fee income | UX/security |

| MSME | ~30% GDP | cash‑flow lending | scale programs |

| Gold loans | Rs 3.15L cr | fast disburse | tiered pricing |

| APIs | $5bn/mo, +40% YoY | VAS monetization | ERP connectors |

What is included in the product

Comprehensive BCG Matrix review of Federal Bank, spotting Stars, Cash Cows, Question Marks and Dogs with strategic recommendations.

One-page BCG matrix for Federal Bank placing units in quadrants to spot priorities and cut decision friction.

Cash Cows

CASA deposits in legacy strongholds

Sticky retail CASA in legacy Kerala strongholds funds the engine: CASA deposits stood at Rs 1.06 lakh crore with a CASA ratio of 40.6% at Mar 2024, delivering low servicing costs and predictable cash flows. Growth is modest but margins remain solid versus term deposits. Maintain relationship programs and light-touch engagement; targeted tech spends to cut churn will pay back quickly.

Home loans to prime salaried

Home loans to prime salaried are a mature, competitive segment for Federal Bank that delivers steady volumes and low credit losses, underpinning dependable margins. Cross‑selling insurance and high auto‑debit repayment rates keep economics healthy, while focus on straight‑through processing and low acquisition cost reduces unit economics. Strategy: milk the book in 2024 while staying selective on pricing and underwriting.

Treasury & fixed‑income book

Treasury & fixed-income book delivers stable earnings via duration management and liquidity deployment, cushioning cycles; India 10-year G-sec hovered ~7.3% in 2024 supporting carry. Tight risk limits and cost discipline kept spreads near 80–120 bps on corporate paper; analytics-driven trading and model tweaks can extract incremental 5–15 bps without major capex.

Transaction banking fees

Transaction banking fees from CMS, payroll and bulk payments deliver steady, recurring low-touch revenue for Federal Bank; industry retention for embedded payroll/CMS clients exceeds 85% and growth is moderate, supporting predictable fee income in 2024.

Tight SLAs and rational pricing preserve margins; light add-ons such as real-time alerts and payments analytics typically lift ARPU by 10–20%, per 2024 sector benchmarks.

- Recurring low-touch fees: stable cash cow

- Retention: >85% once embedded

- Growth: moderate; focus on SLAs/pricing

- Add-ons: alerts/analytics → +10–20% ARPU

ATM and branch cash services

ATM and branch cash services show mature, predictable utilization in cash-heavy pockets; Federal Bank maintains a stable footprint with approximately 1,300 branches and 1,500 ATMs in 2024, driving steady fee and interchange revenue while opex is well understood. Focus: optimize footprint, migrate low-value transactions to digital channels; treat as harvest, not a growth bet.

- Utilization: mature, predictable

- Network: ~1,300 branches / ~1,500 ATMs (2024)

- Opex: known; revenue: steady ticks

- Strategic action: optimize footprint, digitize low-value activity

- Positioning: harvest play

Sticky CASA funds low-cost lending; harvest efficiency, reduce churn

Sticky retail CASA (Rs 1.06 lakh crore; CASA 40.6% at Mar 2024) funds low-cost lending; home loans to prime salaried deliver steady volumes and low losses; treasury carry (India 10y ~7.3% in 2024) cushions earnings; transaction banking, branches/ATMs (~1,300 branches, ~1,500 ATMs) and cash services provide predictable fee income—focus on harvest, efficiency and selective tech to reduce churn.

| Metric | 2024 |

|---|---|

| CASA | Rs 1.06L cr (40.6%) |

| Branches/ATMs | ~1,300 / ~1,500 |

| India 10y | ~7.3% |

What You See Is What You Get

Federal Bank BCG Matrix

The Federal Bank BCG Matrix you’re previewing here is the exact file you’ll receive after purchase. No watermarks, no placeholders—just the finished, professionally formatted analysis ready for strategy sessions. Buy once and download immediately; the full document is editable, printable, and presentation-ready. No surprises, just clear insights tailored for Federal Bank decision-making.