Federal Bank Business Model Canvas

Bank Business Model Canvas — customers, value propositions, channels, revenue levers

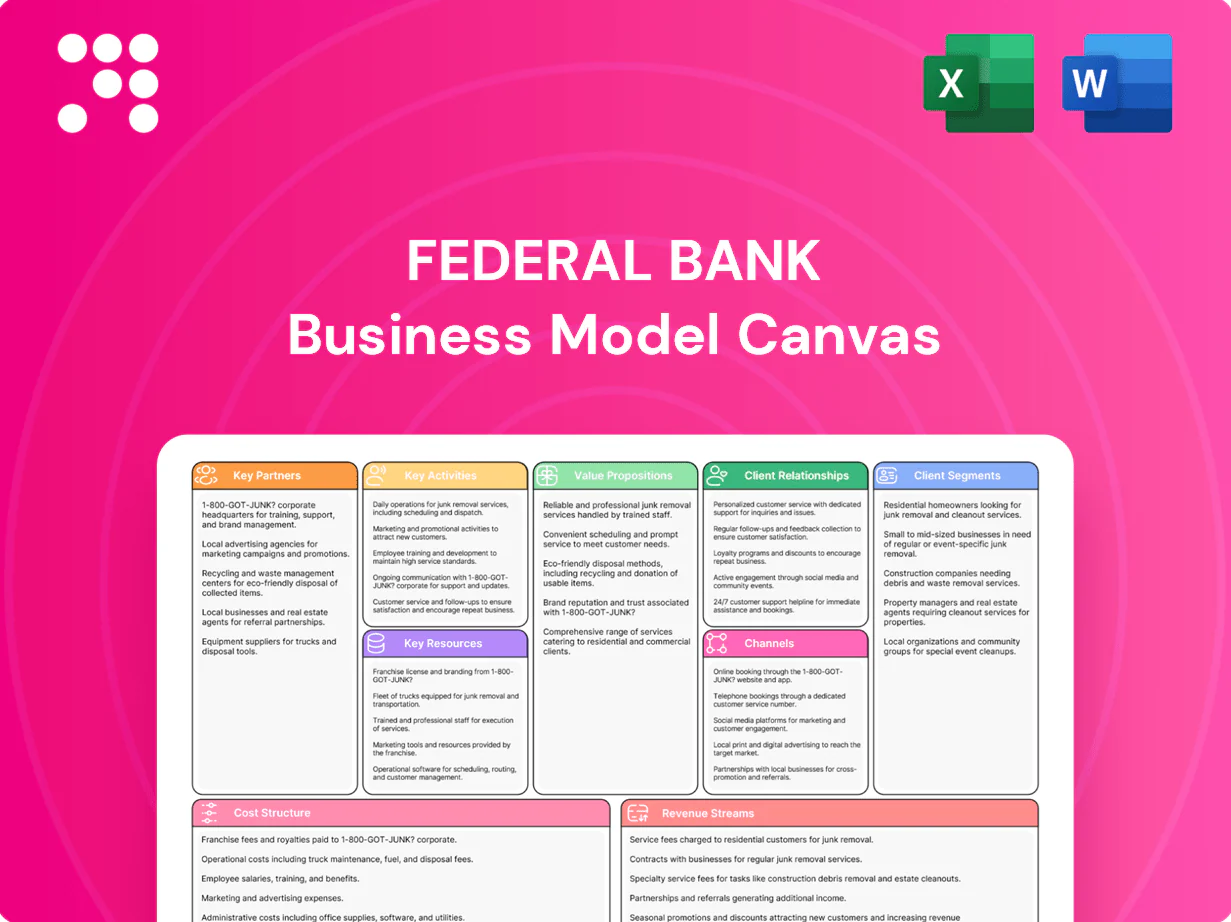

Discover Federal Bank’s strategic DNA with a concise Business Model Canvas that maps customers, value propositions, channels, and revenue levers in one clear view. This snapshot highlights growth drivers and competitive edges—perfect for investors, consultants, and founders. Purchase the full, editable Canvas (Word & Excel) to access detailed insights, financial implications, and a ready-to-use strategic roadmap.

Partnerships

Payment networks & NPCI

Partnerships with Visa, Mastercard, RuPay and NPCI enable Federal Bank to offer cards, UPI and instant settlements, leveraging NPCI’s >80 billion UPI transactions in 2023 and global card networks that handle trillions in volume. These ties shorten time-to-market for new payment products and drive co-innovation in acceptance, security and reliability. Scale lowers per-transaction costs and measurably improves customer experience.

Fintechs & technology vendors

Alliances with fintechs speed onboarding, analytics, and digital lending, leveraging partners to scale customer acquisition and credit models. Cloud, core-banking, and cybersecurity vendors provide resilience and low-latency delivery for retail and MSME volumes. Co-branded products broaden reach to digital-first cohorts, while regulatory sandboxes accelerate pilots and feature rollouts; UPI crossed over 100 billion transactions in FY2022-23, underscoring digital traction.

Correspondent & international banks

Global correspondent and international banks enable Federal Bank to process a share of the $111 billion remittance inflows to India in 2023 (World Bank), supporting remittances, trade finance and treasury settlements across corridors. These partners lower cross-border costs via nostro/vostro access and pooled liquidity. Shared compliance frameworks such as FATF standards strengthen AML/CFT controls. Expanded nostro/vostro networks boost NRI and corporate service reach.

Insurance & investment partners

Bancassurance and mutual fund tie-ups expand Federal Bank’s fee-income mix, with India mutual fund AUM at about Rs 52 lakh crore in 2024 and bancassurance driving double-digit premium growth industry-wide in 2023–24, enabling bundled protection and wealth products that deepen customer relationships and raise wallet share.

- Fee diversification

- Bundled protection + wealth

- Deeper distribution

- Lower acquisition cost via co-marketing

Business correspondents & merchant ecosystems

Business correspondent networks expand Federal Banks last-mile access in semi-urban and rural areas, reaching deeper customer segments in 2024 and enabling deposit origination and basic credit delivery; merchant partnerships drive digital acceptance and CASA acquisition through payments rails and POS tie-ups, while embedded finance on platforms (BNPL, wallets) boosts distribution and conversion; integrated cash-management services for MSMEs increase account stickiness and cross-sell of working-capital products.

- BCs: last-mile deposit & credit origination

- Merchants: acceptance-led CASA growth

- Embedded finance: platform distribution

- Cash mgmt: MSME retention & cross-sell

Partnerships unlock >100bn UPI, card rails, remittances and MF distribution

Partnerships with NPCI, Visa/Mastercard and fintechs drive payments, cards and digital lending, tapping NPCI’s >100 billion UPI transactions (FY2022–23) and global card rails. Correspondent banks support remittances (~$111bn inflows to India in 2023) and trade; bancassurance/mutual fund tie-ups tap Rs 52 lakh crore MF AUM (2024). BCs and merchant partners expand rural CASA and MSME distribution.

| Partner | Role | 2023/24 Metric |

|---|---|---|

| NPCI/Visa | Payments/cards | >100bn UPI; global card volumes |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Federal Bank covering customer segments, channels, value propositions and all nine BMC blocks with detailed narratives and competitive analysis; includes SWOT, real-world operational insights and a polished format ideal for presentations, investor or bank funding discussions and strategic decision-making.

High-level view of Federal Bank’s business model with editable cells, relieving the pain of fragmented strategy and saving time on structuring insights for teams and boardrooms.

Activities

Deposit mobilization

Acquire and retain low-cost CASA and term deposits, with Federal Bank reporting a CASA ratio of 36.8% in FY2024, to lower funding costs and support net interest margin. Optimize pricing and targeted campaigns to balance deposit growth and margin compression. Improve branch and digital journeys to shorten account opening times and boost conversion. Proactively manage liquidity to ensure funding for lending and payments while meeting regulatory LCR/CRR requirements.

Credit underwriting & lending

Originate retail, MSME and corporate loans with risk-based pricing across a ~₹1.3 lakh crore advances book (FY2024), using data-driven scorecards and rule-based credit policies to standardize approvals. Continuous portfolio monitoring with early-warning triggers limits slippage and supports GNPA containment. Drive cross-sell and utilization of credit lines to lift yields by widening fee income and improving asset mix.

Risk, compliance & governance

Maintain prudential standards across credit, market and operational risk in line with Basel III norms requiring a minimum CRAR of 10.875% and CET1 of 7.0% (RBI framework). Ensure regulatory reporting and audits meet statutory timelines (quarterly financials, annual statutory audit) and data accuracy for RBI/SEBI filings. Strengthen AML/KYC and fraud controls per FIU-IND and RBI guidance, increasing transaction monitoring coverage. Align risk appetite with growth strategy through capital planning and stress-testing.

Digital product development

Federal Bank accelerates digital product development by enhancing mobile, internet, and API platforms while rolling out payments, wealth, and lending features iteratively; UPI crossed ~100 billion transactions in FY2024 supporting rapid payment adoption. The bank leverages analytics and personalization to boost engagement and targets enterprise-grade reliability with 99.99% uptime and strengthened cybersecurity posture.

- Enhance mobile, internet, API platforms

- Iterative launch: payments, wealth, lending

- Analytics-driven personalization

- 99.99% uptime target; strengthen cybersecurity

Treasury & ALM management

Treasury and ALM manage liquidity, interest-rate risk and the investment book to stabilize Federal Bank’s balance sheet and income, optimizing cost of funds and ensuring SLR (18%) and CRR (4.5%) compliance; execute forex and derivative transactions for clients and proprietary needs while hedging asset‑liability mismatches.

- Liquidity & reserves: SLR 18%, CRR 4.5%

- Interest rate hedging: ALM gaps

- Investment book: yield optimization

- Forex/derivatives: client and bank hedges

Acquire low‑cost CASA 36.8%, fund ₹1.3 lakh crore advances; drive UPI 100bn+ TXns

Acquire low‑cost CASA (36.8% FY2024) and term deposits; originate ₹1.3 lakh crore advances with risk‑based pricing and monitoring to contain GNPA; uphold Basel III prudentials (CRAR 10.875% min, CET1 7.0%) and AML/KYC controls; accelerate digital payments/wealthed lending (UPI >100bn TXns FY2024) while ALM ensures SLR 18%/CRR 4.5% compliance.

| Metric | FY2024 |

|---|---|

| CASA ratio | 36.8% |

| Advances | ₹1.3 lakh crore |

| UPI TXns | >100 billion |

| SLR/CRR | 18% / 4.5% |

Full Document Unlocks After Purchase

Business Model Canvas

The Federal Bank Business Model Canvas preview shown here is the exact document you will receive after purchase, not a mockup. Upon completing your order you’ll get the complete, editable file formatted the same way for immediate use in presentations and planning. No hidden content—what you see is the deliverable, ready to edit and share.

Bank Business Model Canvas — customers, value propositions, channels, revenue levers

Discover Federal Bank’s strategic DNA with a concise Business Model Canvas that maps customers, value propositions, channels, and revenue levers in one clear view. This snapshot highlights growth drivers and competitive edges—perfect for investors, consultants, and founders. Purchase the full, editable Canvas (Word & Excel) to access detailed insights, financial implications, and a ready-to-use strategic roadmap.

Partnerships

Payment networks & NPCI

Partnerships with Visa, Mastercard, RuPay and NPCI enable Federal Bank to offer cards, UPI and instant settlements, leveraging NPCI’s >80 billion UPI transactions in 2023 and global card networks that handle trillions in volume. These ties shorten time-to-market for new payment products and drive co-innovation in acceptance, security and reliability. Scale lowers per-transaction costs and measurably improves customer experience.

Fintechs & technology vendors

Alliances with fintechs speed onboarding, analytics, and digital lending, leveraging partners to scale customer acquisition and credit models. Cloud, core-banking, and cybersecurity vendors provide resilience and low-latency delivery for retail and MSME volumes. Co-branded products broaden reach to digital-first cohorts, while regulatory sandboxes accelerate pilots and feature rollouts; UPI crossed over 100 billion transactions in FY2022-23, underscoring digital traction.

Correspondent & international banks

Global correspondent and international banks enable Federal Bank to process a share of the $111 billion remittance inflows to India in 2023 (World Bank), supporting remittances, trade finance and treasury settlements across corridors. These partners lower cross-border costs via nostro/vostro access and pooled liquidity. Shared compliance frameworks such as FATF standards strengthen AML/CFT controls. Expanded nostro/vostro networks boost NRI and corporate service reach.

Insurance & investment partners

Bancassurance and mutual fund tie-ups expand Federal Bank’s fee-income mix, with India mutual fund AUM at about Rs 52 lakh crore in 2024 and bancassurance driving double-digit premium growth industry-wide in 2023–24, enabling bundled protection and wealth products that deepen customer relationships and raise wallet share.

- Fee diversification

- Bundled protection + wealth

- Deeper distribution

- Lower acquisition cost via co-marketing

Business correspondents & merchant ecosystems

Business correspondent networks expand Federal Banks last-mile access in semi-urban and rural areas, reaching deeper customer segments in 2024 and enabling deposit origination and basic credit delivery; merchant partnerships drive digital acceptance and CASA acquisition through payments rails and POS tie-ups, while embedded finance on platforms (BNPL, wallets) boosts distribution and conversion; integrated cash-management services for MSMEs increase account stickiness and cross-sell of working-capital products.

- BCs: last-mile deposit & credit origination

- Merchants: acceptance-led CASA growth

- Embedded finance: platform distribution

- Cash mgmt: MSME retention & cross-sell

Partnerships unlock >100bn UPI, card rails, remittances and MF distribution

Partnerships with NPCI, Visa/Mastercard and fintechs drive payments, cards and digital lending, tapping NPCI’s >100 billion UPI transactions (FY2022–23) and global card rails. Correspondent banks support remittances (~$111bn inflows to India in 2023) and trade; bancassurance/mutual fund tie-ups tap Rs 52 lakh crore MF AUM (2024). BCs and merchant partners expand rural CASA and MSME distribution.

| Partner | Role | 2023/24 Metric |

|---|---|---|

| NPCI/Visa | Payments/cards | >100bn UPI; global card volumes |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Federal Bank covering customer segments, channels, value propositions and all nine BMC blocks with detailed narratives and competitive analysis; includes SWOT, real-world operational insights and a polished format ideal for presentations, investor or bank funding discussions and strategic decision-making.

High-level view of Federal Bank’s business model with editable cells, relieving the pain of fragmented strategy and saving time on structuring insights for teams and boardrooms.

Activities

Deposit mobilization

Acquire and retain low-cost CASA and term deposits, with Federal Bank reporting a CASA ratio of 36.8% in FY2024, to lower funding costs and support net interest margin. Optimize pricing and targeted campaigns to balance deposit growth and margin compression. Improve branch and digital journeys to shorten account opening times and boost conversion. Proactively manage liquidity to ensure funding for lending and payments while meeting regulatory LCR/CRR requirements.

Credit underwriting & lending

Originate retail, MSME and corporate loans with risk-based pricing across a ~₹1.3 lakh crore advances book (FY2024), using data-driven scorecards and rule-based credit policies to standardize approvals. Continuous portfolio monitoring with early-warning triggers limits slippage and supports GNPA containment. Drive cross-sell and utilization of credit lines to lift yields by widening fee income and improving asset mix.

Risk, compliance & governance

Maintain prudential standards across credit, market and operational risk in line with Basel III norms requiring a minimum CRAR of 10.875% and CET1 of 7.0% (RBI framework). Ensure regulatory reporting and audits meet statutory timelines (quarterly financials, annual statutory audit) and data accuracy for RBI/SEBI filings. Strengthen AML/KYC and fraud controls per FIU-IND and RBI guidance, increasing transaction monitoring coverage. Align risk appetite with growth strategy through capital planning and stress-testing.

Digital product development

Federal Bank accelerates digital product development by enhancing mobile, internet, and API platforms while rolling out payments, wealth, and lending features iteratively; UPI crossed ~100 billion transactions in FY2024 supporting rapid payment adoption. The bank leverages analytics and personalization to boost engagement and targets enterprise-grade reliability with 99.99% uptime and strengthened cybersecurity posture.

- Enhance mobile, internet, API platforms

- Iterative launch: payments, wealth, lending

- Analytics-driven personalization

- 99.99% uptime target; strengthen cybersecurity

Treasury & ALM management

Treasury and ALM manage liquidity, interest-rate risk and the investment book to stabilize Federal Bank’s balance sheet and income, optimizing cost of funds and ensuring SLR (18%) and CRR (4.5%) compliance; execute forex and derivative transactions for clients and proprietary needs while hedging asset‑liability mismatches.

- Liquidity & reserves: SLR 18%, CRR 4.5%

- Interest rate hedging: ALM gaps

- Investment book: yield optimization

- Forex/derivatives: client and bank hedges

Acquire low‑cost CASA 36.8%, fund ₹1.3 lakh crore advances; drive UPI 100bn+ TXns

Acquire low‑cost CASA (36.8% FY2024) and term deposits; originate ₹1.3 lakh crore advances with risk‑based pricing and monitoring to contain GNPA; uphold Basel III prudentials (CRAR 10.875% min, CET1 7.0%) and AML/KYC controls; accelerate digital payments/wealthed lending (UPI >100bn TXns FY2024) while ALM ensures SLR 18%/CRR 4.5% compliance.

| Metric | FY2024 |

|---|---|

| CASA ratio | 36.8% |

| Advances | ₹1.3 lakh crore |

| UPI TXns | >100 billion |

| SLR/CRR | 18% / 4.5% |

Full Document Unlocks After Purchase

Business Model Canvas

The Federal Bank Business Model Canvas preview shown here is the exact document you will receive after purchase, not a mockup. Upon completing your order you’ll get the complete, editable file formatted the same way for immediate use in presentations and planning. No hidden content—what you see is the deliverable, ready to edit and share.

Description

Bank Business Model Canvas — customers, value propositions, channels, revenue levers

Discover Federal Bank’s strategic DNA with a concise Business Model Canvas that maps customers, value propositions, channels, and revenue levers in one clear view. This snapshot highlights growth drivers and competitive edges—perfect for investors, consultants, and founders. Purchase the full, editable Canvas (Word & Excel) to access detailed insights, financial implications, and a ready-to-use strategic roadmap.

Partnerships

Payment networks & NPCI

Partnerships with Visa, Mastercard, RuPay and NPCI enable Federal Bank to offer cards, UPI and instant settlements, leveraging NPCI’s >80 billion UPI transactions in 2023 and global card networks that handle trillions in volume. These ties shorten time-to-market for new payment products and drive co-innovation in acceptance, security and reliability. Scale lowers per-transaction costs and measurably improves customer experience.

Fintechs & technology vendors

Alliances with fintechs speed onboarding, analytics, and digital lending, leveraging partners to scale customer acquisition and credit models. Cloud, core-banking, and cybersecurity vendors provide resilience and low-latency delivery for retail and MSME volumes. Co-branded products broaden reach to digital-first cohorts, while regulatory sandboxes accelerate pilots and feature rollouts; UPI crossed over 100 billion transactions in FY2022-23, underscoring digital traction.

Correspondent & international banks

Global correspondent and international banks enable Federal Bank to process a share of the $111 billion remittance inflows to India in 2023 (World Bank), supporting remittances, trade finance and treasury settlements across corridors. These partners lower cross-border costs via nostro/vostro access and pooled liquidity. Shared compliance frameworks such as FATF standards strengthen AML/CFT controls. Expanded nostro/vostro networks boost NRI and corporate service reach.

Insurance & investment partners

Bancassurance and mutual fund tie-ups expand Federal Bank’s fee-income mix, with India mutual fund AUM at about Rs 52 lakh crore in 2024 and bancassurance driving double-digit premium growth industry-wide in 2023–24, enabling bundled protection and wealth products that deepen customer relationships and raise wallet share.

- Fee diversification

- Bundled protection + wealth

- Deeper distribution

- Lower acquisition cost via co-marketing

Business correspondents & merchant ecosystems

Business correspondent networks expand Federal Banks last-mile access in semi-urban and rural areas, reaching deeper customer segments in 2024 and enabling deposit origination and basic credit delivery; merchant partnerships drive digital acceptance and CASA acquisition through payments rails and POS tie-ups, while embedded finance on platforms (BNPL, wallets) boosts distribution and conversion; integrated cash-management services for MSMEs increase account stickiness and cross-sell of working-capital products.

- BCs: last-mile deposit & credit origination

- Merchants: acceptance-led CASA growth

- Embedded finance: platform distribution

- Cash mgmt: MSME retention & cross-sell

Partnerships unlock >100bn UPI, card rails, remittances and MF distribution

Partnerships with NPCI, Visa/Mastercard and fintechs drive payments, cards and digital lending, tapping NPCI’s >100 billion UPI transactions (FY2022–23) and global card rails. Correspondent banks support remittances (~$111bn inflows to India in 2023) and trade; bancassurance/mutual fund tie-ups tap Rs 52 lakh crore MF AUM (2024). BCs and merchant partners expand rural CASA and MSME distribution.

| Partner | Role | 2023/24 Metric |

|---|---|---|

| NPCI/Visa | Payments/cards | >100bn UPI; global card volumes |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Federal Bank covering customer segments, channels, value propositions and all nine BMC blocks with detailed narratives and competitive analysis; includes SWOT, real-world operational insights and a polished format ideal for presentations, investor or bank funding discussions and strategic decision-making.

High-level view of Federal Bank’s business model with editable cells, relieving the pain of fragmented strategy and saving time on structuring insights for teams and boardrooms.

Activities

Deposit mobilization

Acquire and retain low-cost CASA and term deposits, with Federal Bank reporting a CASA ratio of 36.8% in FY2024, to lower funding costs and support net interest margin. Optimize pricing and targeted campaigns to balance deposit growth and margin compression. Improve branch and digital journeys to shorten account opening times and boost conversion. Proactively manage liquidity to ensure funding for lending and payments while meeting regulatory LCR/CRR requirements.

Credit underwriting & lending

Originate retail, MSME and corporate loans with risk-based pricing across a ~₹1.3 lakh crore advances book (FY2024), using data-driven scorecards and rule-based credit policies to standardize approvals. Continuous portfolio monitoring with early-warning triggers limits slippage and supports GNPA containment. Drive cross-sell and utilization of credit lines to lift yields by widening fee income and improving asset mix.

Risk, compliance & governance

Maintain prudential standards across credit, market and operational risk in line with Basel III norms requiring a minimum CRAR of 10.875% and CET1 of 7.0% (RBI framework). Ensure regulatory reporting and audits meet statutory timelines (quarterly financials, annual statutory audit) and data accuracy for RBI/SEBI filings. Strengthen AML/KYC and fraud controls per FIU-IND and RBI guidance, increasing transaction monitoring coverage. Align risk appetite with growth strategy through capital planning and stress-testing.

Digital product development

Federal Bank accelerates digital product development by enhancing mobile, internet, and API platforms while rolling out payments, wealth, and lending features iteratively; UPI crossed ~100 billion transactions in FY2024 supporting rapid payment adoption. The bank leverages analytics and personalization to boost engagement and targets enterprise-grade reliability with 99.99% uptime and strengthened cybersecurity posture.

- Enhance mobile, internet, API platforms

- Iterative launch: payments, wealth, lending

- Analytics-driven personalization

- 99.99% uptime target; strengthen cybersecurity

Treasury & ALM management

Treasury and ALM manage liquidity, interest-rate risk and the investment book to stabilize Federal Bank’s balance sheet and income, optimizing cost of funds and ensuring SLR (18%) and CRR (4.5%) compliance; execute forex and derivative transactions for clients and proprietary needs while hedging asset‑liability mismatches.

- Liquidity & reserves: SLR 18%, CRR 4.5%

- Interest rate hedging: ALM gaps

- Investment book: yield optimization

- Forex/derivatives: client and bank hedges

Acquire low‑cost CASA 36.8%, fund ₹1.3 lakh crore advances; drive UPI 100bn+ TXns

Acquire low‑cost CASA (36.8% FY2024) and term deposits; originate ₹1.3 lakh crore advances with risk‑based pricing and monitoring to contain GNPA; uphold Basel III prudentials (CRAR 10.875% min, CET1 7.0%) and AML/KYC controls; accelerate digital payments/wealthed lending (UPI >100bn TXns FY2024) while ALM ensures SLR 18%/CRR 4.5% compliance.

| Metric | FY2024 |

|---|---|

| CASA ratio | 36.8% |

| Advances | ₹1.3 lakh crore |

| UPI TXns | >100 billion |

| SLR/CRR | 18% / 4.5% |

Full Document Unlocks After Purchase

Business Model Canvas

The Federal Bank Business Model Canvas preview shown here is the exact document you will receive after purchase, not a mockup. Upon completing your order you’ll get the complete, editable file formatted the same way for immediate use in presentations and planning. No hidden content—what you see is the deliverable, ready to edit and share.