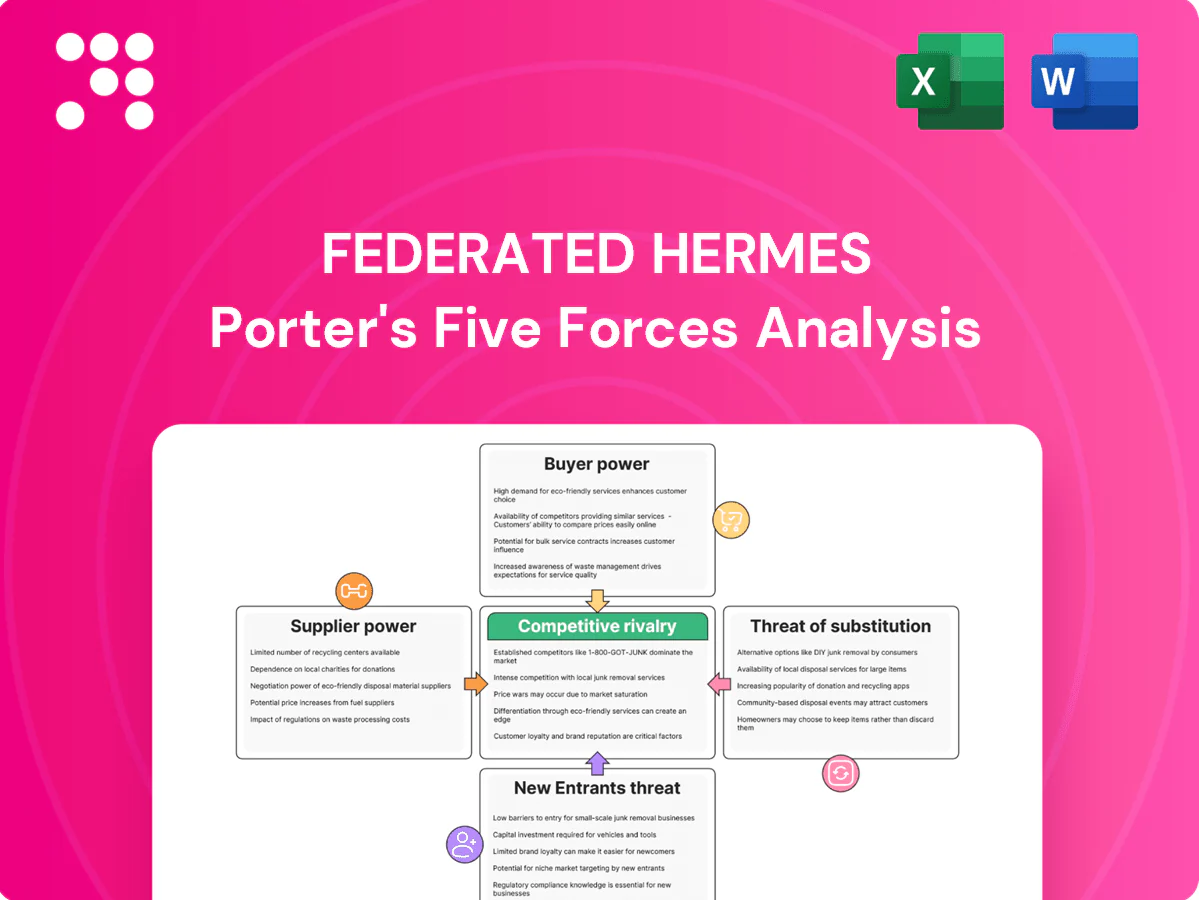

Federated Hermes Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Federated Hermes operates in a capital-intensive, highly regulated asset-management sector where scale, product differentiation, and distribution partnerships shape competitive dynamics. Buyer bargaining and fee compression heighten margin pressure while regulatory shifts and fintech adoption raise disruption risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, data, and strategic implications.

Suppliers Bargaining Power

Dependence on investment talent

Star portfolio managers, analysts and PM teams are scarce and mobile, giving them high bargaining power because track records are portable and recruitment competition is intense. Federated Hermes uses retention packages, carried-interest-like incentives and culture to temper this power. Diversified teams and codified investment processes reduce key-person risk and limit supplier leverage.

Data and index vendor leverage

Essential market data and benchmark licenses are concentrated among MSCI, S&P Dow Jones and FTSE Russell, supplying the bulk of investable indexes while global ETF assets exceeded $10 trillion in 2024. Switching costs and compliance constraints give these vendors pricing power, though multi-vendor sourcing and negotiated enterprise agreements reduce fees. Proprietary research and custom benchmarks further dilute vendor leverage by lowering dependence on third-party indexes.

Technology and custody infrastructure

Order management, risk systems and cybersecurity depend on a few enterprise platforms and cloud providers—top three cloud vendors held over 65% market share in 2024—giving suppliers pricing power and integration stickiness. Federated Hermes’ in-house administration, custody and transfer services offset some reliance on external vendors. Ongoing vendor risk management and modular architectures reduce long-term lock-in and bargaining leverage.

Distribution and platform gatekeepers

Distribution gatekeepers — wirehouses, retirement recordkeepers and model marketplaces — constrain Federated Hermes by controlling product shelf space and imposing placement fees, revenue-share accords and rigorous due diligence, effectively acting as suppliers with leverage.

- Platform control over shelf space raises supplier-like bargaining power

- Placement fees and revenue-sharing increase distribution costs

- Direct institutional relationships cut dependence on gatekeepers

- Multi-channel distribution spreads exposure

Alternative asset deal flow sources

General partners, deal sponsors and placement agents continue to gate private markets; scarce top-tier capacity gives them fee and allocation leverage, with global private capital dry powder ≈ 3.0 trillion in 2024 concentrating demand for top GPs. Strategic partnerships and co-invest rights can rebalance terms while internal origination and thematic networks reduce supplier dependence.

- Top GPs/placement agents control access

- ~3.0T dry powder (2024)

- Co-invests/partnerships lower fees

- Internal origination cuts reliance

Suppliers exert high leverage: talent, benchmark fees, top3 cloud ≈65%, GPs $3T

Suppliers exert moderate-to-high power: star PMs are mobile so talent costs and retention packages matter; benchmark vendors (MSCI/S&P/FTSE) and cloud providers (top3 ≈65% share in 2024) hold pricing leverage; distribution gatekeepers and top GPs (≈3.0T private dry powder in 2024) control access and fees, while internal capabilities and multi-vendor sourcing reduce dependence.

| Supplier | 2024 Metric |

|---|---|

| ETF assets | $10T+ |

| Top3 cloud share | ≈65% |

| Private dry powder | $3.0T |

What is included in the product

Tailored Porter's Five Forces analysis for Federated Hermes that uncovers competitive drivers, buyer and supplier power, entry barriers, substitute threats, and disruptive/regulatory risks, with strategic commentary and data-backed insights. Delivered in fully editable Word format for investor reports, strategy decks, or academic use.

A clear one-sheet Porter's Five Forces for Federated Hermes—visualize competitive pressures instantly with an editable radar chart and clean layout, ready to drop into pitch decks or executive reports.

Customers Bargaining Power

Institutional fee negotiation

Pensions, endowments and sovereigns—with global pension assets around $56 trillion and sovereign wealth funds about $10.8 trillion in 2023—use professional procurement to demand breakpoints, performance fees and bespoke mandates. Their sizable mandates create persistent pricing pressure on managers like Federated Hermes. Strong outcomes, ESG and differentiated capabilities help preserve margins by justifying premium fees. Customization requests increase operational costs but deepen client lock‑in.

Consultant and OCIO influence

Consultants and OCIOs act as gatekeepers for Federated Hermes, shaping shortlists and model allocations and often determining mandate wins in 2024. Their ratings can trigger material inflows or redemptions, forcing fee concessions and greater transparency to gain model approval. Consequently, deep relationship management and timely, robust reporting are critical to retain placement and influence.

Retail platform sensitivity

Intermediated retail clients are highly price- and performance-sensitive, driven by platform comparators and transparency; ETFs, which held over $10 trillion globally by 2024, heighten elasticity and accelerate outflows from underperforming active funds. Share-class engineering and bundled value-add services can moderate churn, while Federated Hermes brand and stewardship credentials strengthen client loyalty and retention.

Switching costs and portability

Operational switching costs at Federated Hermes are moderate; perceived risk varies by retail versus institutional clients, with institutions able to reallocate rapidly after underperformance. Lockups in alternatives (commonly 1–3 years) can delay exits but heighten renewal scrutiny. Consistent alpha and high service quality materially reduce churn.

- Switching costs: moderate

- Alternatives lockups: 1–3 years

- Institutions: fast reallocation

- Alpha/service: key to retention

Demand for ESG and impact

Clients increasingly demand ESG integration and stewardship reporting, giving them specification power over data standards, engagement outcomes and disclosure frequency; Federated Hermes’ long-standing stewardship capabilities address many mandates, but continuous enhancement of reporting, engagement metrics and stewardship tools is required to retain credibility and mandates.

- ESG integration: client-driven specification power

- Data & disclosures: rising granularity expectations

- Stewardship: Federated Hermes heritage aligned with demand

- Need: continuous enhancement to retain mandates

Pensions, SWFs and ETFs drive fee pressure and liquidity risk across global capital pools

Pensions, endowments and sovereigns (global pensions ~$56T; SWFs ~$10.8T in 2023) exert strong fee and mandate specification power, pressuring margins. Consultants/OCIOs gatekeep mandates and force transparency. Retail/ETFs (global ETFs >$10T in 2024) amplify price sensitivity and redemption risk; alternatives lockups 1–3 years mitigate short-term exits.

| Segment | Power | Key datapoint |

|---|---|---|

| Pensions/SWFs | High | $56T / $10.8T (2023) |

| ETFs/Retail | High | $>10T (2024) |

| Alternatives | Moderate | Lockups 1–3 yrs |

Full Version Awaits

Federated Hermes Porter's Five Forces Analysis

This preview shows the exact Federated Hermes Porter's Five Forces analysis you'll receive immediately after purchase; no placeholders or sample pages. The document is the final, professionally formatted version, comprehensive and ready for download. You’ll get instant access to this identical file once you buy.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Federated Hermes operates in a capital-intensive, highly regulated asset-management sector where scale, product differentiation, and distribution partnerships shape competitive dynamics. Buyer bargaining and fee compression heighten margin pressure while regulatory shifts and fintech adoption raise disruption risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, data, and strategic implications.

Suppliers Bargaining Power

Dependence on investment talent

Star portfolio managers, analysts and PM teams are scarce and mobile, giving them high bargaining power because track records are portable and recruitment competition is intense. Federated Hermes uses retention packages, carried-interest-like incentives and culture to temper this power. Diversified teams and codified investment processes reduce key-person risk and limit supplier leverage.

Data and index vendor leverage

Essential market data and benchmark licenses are concentrated among MSCI, S&P Dow Jones and FTSE Russell, supplying the bulk of investable indexes while global ETF assets exceeded $10 trillion in 2024. Switching costs and compliance constraints give these vendors pricing power, though multi-vendor sourcing and negotiated enterprise agreements reduce fees. Proprietary research and custom benchmarks further dilute vendor leverage by lowering dependence on third-party indexes.

Technology and custody infrastructure

Order management, risk systems and cybersecurity depend on a few enterprise platforms and cloud providers—top three cloud vendors held over 65% market share in 2024—giving suppliers pricing power and integration stickiness. Federated Hermes’ in-house administration, custody and transfer services offset some reliance on external vendors. Ongoing vendor risk management and modular architectures reduce long-term lock-in and bargaining leverage.

Distribution and platform gatekeepers

Distribution gatekeepers — wirehouses, retirement recordkeepers and model marketplaces — constrain Federated Hermes by controlling product shelf space and imposing placement fees, revenue-share accords and rigorous due diligence, effectively acting as suppliers with leverage.

- Platform control over shelf space raises supplier-like bargaining power

- Placement fees and revenue-sharing increase distribution costs

- Direct institutional relationships cut dependence on gatekeepers

- Multi-channel distribution spreads exposure

Alternative asset deal flow sources

General partners, deal sponsors and placement agents continue to gate private markets; scarce top-tier capacity gives them fee and allocation leverage, with global private capital dry powder ≈ 3.0 trillion in 2024 concentrating demand for top GPs. Strategic partnerships and co-invest rights can rebalance terms while internal origination and thematic networks reduce supplier dependence.

- Top GPs/placement agents control access

- ~3.0T dry powder (2024)

- Co-invests/partnerships lower fees

- Internal origination cuts reliance

Suppliers exert high leverage: talent, benchmark fees, top3 cloud ≈65%, GPs $3T

Suppliers exert moderate-to-high power: star PMs are mobile so talent costs and retention packages matter; benchmark vendors (MSCI/S&P/FTSE) and cloud providers (top3 ≈65% share in 2024) hold pricing leverage; distribution gatekeepers and top GPs (≈3.0T private dry powder in 2024) control access and fees, while internal capabilities and multi-vendor sourcing reduce dependence.

| Supplier | 2024 Metric |

|---|---|

| ETF assets | $10T+ |

| Top3 cloud share | ≈65% |

| Private dry powder | $3.0T |

What is included in the product

Tailored Porter's Five Forces analysis for Federated Hermes that uncovers competitive drivers, buyer and supplier power, entry barriers, substitute threats, and disruptive/regulatory risks, with strategic commentary and data-backed insights. Delivered in fully editable Word format for investor reports, strategy decks, or academic use.

A clear one-sheet Porter's Five Forces for Federated Hermes—visualize competitive pressures instantly with an editable radar chart and clean layout, ready to drop into pitch decks or executive reports.

Customers Bargaining Power

Institutional fee negotiation

Pensions, endowments and sovereigns—with global pension assets around $56 trillion and sovereign wealth funds about $10.8 trillion in 2023—use professional procurement to demand breakpoints, performance fees and bespoke mandates. Their sizable mandates create persistent pricing pressure on managers like Federated Hermes. Strong outcomes, ESG and differentiated capabilities help preserve margins by justifying premium fees. Customization requests increase operational costs but deepen client lock‑in.

Consultant and OCIO influence

Consultants and OCIOs act as gatekeepers for Federated Hermes, shaping shortlists and model allocations and often determining mandate wins in 2024. Their ratings can trigger material inflows or redemptions, forcing fee concessions and greater transparency to gain model approval. Consequently, deep relationship management and timely, robust reporting are critical to retain placement and influence.

Retail platform sensitivity

Intermediated retail clients are highly price- and performance-sensitive, driven by platform comparators and transparency; ETFs, which held over $10 trillion globally by 2024, heighten elasticity and accelerate outflows from underperforming active funds. Share-class engineering and bundled value-add services can moderate churn, while Federated Hermes brand and stewardship credentials strengthen client loyalty and retention.

Switching costs and portability

Operational switching costs at Federated Hermes are moderate; perceived risk varies by retail versus institutional clients, with institutions able to reallocate rapidly after underperformance. Lockups in alternatives (commonly 1–3 years) can delay exits but heighten renewal scrutiny. Consistent alpha and high service quality materially reduce churn.

- Switching costs: moderate

- Alternatives lockups: 1–3 years

- Institutions: fast reallocation

- Alpha/service: key to retention

Demand for ESG and impact

Clients increasingly demand ESG integration and stewardship reporting, giving them specification power over data standards, engagement outcomes and disclosure frequency; Federated Hermes’ long-standing stewardship capabilities address many mandates, but continuous enhancement of reporting, engagement metrics and stewardship tools is required to retain credibility and mandates.

- ESG integration: client-driven specification power

- Data & disclosures: rising granularity expectations

- Stewardship: Federated Hermes heritage aligned with demand

- Need: continuous enhancement to retain mandates

Pensions, SWFs and ETFs drive fee pressure and liquidity risk across global capital pools

Pensions, endowments and sovereigns (global pensions ~$56T; SWFs ~$10.8T in 2023) exert strong fee and mandate specification power, pressuring margins. Consultants/OCIOs gatekeep mandates and force transparency. Retail/ETFs (global ETFs >$10T in 2024) amplify price sensitivity and redemption risk; alternatives lockups 1–3 years mitigate short-term exits.

| Segment | Power | Key datapoint |

|---|---|---|

| Pensions/SWFs | High | $56T / $10.8T (2023) |

| ETFs/Retail | High | $>10T (2024) |

| Alternatives | Moderate | Lockups 1–3 yrs |

Full Version Awaits

Federated Hermes Porter's Five Forces Analysis

This preview shows the exact Federated Hermes Porter's Five Forces analysis you'll receive immediately after purchase; no placeholders or sample pages. The document is the final, professionally formatted version, comprehensive and ready for download. You’ll get instant access to this identical file once you buy.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Federated Hermes operates in a capital-intensive, highly regulated asset-management sector where scale, product differentiation, and distribution partnerships shape competitive dynamics. Buyer bargaining and fee compression heighten margin pressure while regulatory shifts and fintech adoption raise disruption risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore detailed force ratings, data, and strategic implications.

Suppliers Bargaining Power

Dependence on investment talent

Star portfolio managers, analysts and PM teams are scarce and mobile, giving them high bargaining power because track records are portable and recruitment competition is intense. Federated Hermes uses retention packages, carried-interest-like incentives and culture to temper this power. Diversified teams and codified investment processes reduce key-person risk and limit supplier leverage.

Data and index vendor leverage

Essential market data and benchmark licenses are concentrated among MSCI, S&P Dow Jones and FTSE Russell, supplying the bulk of investable indexes while global ETF assets exceeded $10 trillion in 2024. Switching costs and compliance constraints give these vendors pricing power, though multi-vendor sourcing and negotiated enterprise agreements reduce fees. Proprietary research and custom benchmarks further dilute vendor leverage by lowering dependence on third-party indexes.

Technology and custody infrastructure

Order management, risk systems and cybersecurity depend on a few enterprise platforms and cloud providers—top three cloud vendors held over 65% market share in 2024—giving suppliers pricing power and integration stickiness. Federated Hermes’ in-house administration, custody and transfer services offset some reliance on external vendors. Ongoing vendor risk management and modular architectures reduce long-term lock-in and bargaining leverage.

Distribution and platform gatekeepers

Distribution gatekeepers — wirehouses, retirement recordkeepers and model marketplaces — constrain Federated Hermes by controlling product shelf space and imposing placement fees, revenue-share accords and rigorous due diligence, effectively acting as suppliers with leverage.

- Platform control over shelf space raises supplier-like bargaining power

- Placement fees and revenue-sharing increase distribution costs

- Direct institutional relationships cut dependence on gatekeepers

- Multi-channel distribution spreads exposure

Alternative asset deal flow sources

General partners, deal sponsors and placement agents continue to gate private markets; scarce top-tier capacity gives them fee and allocation leverage, with global private capital dry powder ≈ 3.0 trillion in 2024 concentrating demand for top GPs. Strategic partnerships and co-invest rights can rebalance terms while internal origination and thematic networks reduce supplier dependence.

- Top GPs/placement agents control access

- ~3.0T dry powder (2024)

- Co-invests/partnerships lower fees

- Internal origination cuts reliance

Suppliers exert high leverage: talent, benchmark fees, top3 cloud ≈65%, GPs $3T

Suppliers exert moderate-to-high power: star PMs are mobile so talent costs and retention packages matter; benchmark vendors (MSCI/S&P/FTSE) and cloud providers (top3 ≈65% share in 2024) hold pricing leverage; distribution gatekeepers and top GPs (≈3.0T private dry powder in 2024) control access and fees, while internal capabilities and multi-vendor sourcing reduce dependence.

| Supplier | 2024 Metric |

|---|---|

| ETF assets | $10T+ |

| Top3 cloud share | ≈65% |

| Private dry powder | $3.0T |

What is included in the product

Tailored Porter's Five Forces analysis for Federated Hermes that uncovers competitive drivers, buyer and supplier power, entry barriers, substitute threats, and disruptive/regulatory risks, with strategic commentary and data-backed insights. Delivered in fully editable Word format for investor reports, strategy decks, or academic use.

A clear one-sheet Porter's Five Forces for Federated Hermes—visualize competitive pressures instantly with an editable radar chart and clean layout, ready to drop into pitch decks or executive reports.

Customers Bargaining Power

Institutional fee negotiation

Pensions, endowments and sovereigns—with global pension assets around $56 trillion and sovereign wealth funds about $10.8 trillion in 2023—use professional procurement to demand breakpoints, performance fees and bespoke mandates. Their sizable mandates create persistent pricing pressure on managers like Federated Hermes. Strong outcomes, ESG and differentiated capabilities help preserve margins by justifying premium fees. Customization requests increase operational costs but deepen client lock‑in.

Consultant and OCIO influence

Consultants and OCIOs act as gatekeepers for Federated Hermes, shaping shortlists and model allocations and often determining mandate wins in 2024. Their ratings can trigger material inflows or redemptions, forcing fee concessions and greater transparency to gain model approval. Consequently, deep relationship management and timely, robust reporting are critical to retain placement and influence.

Retail platform sensitivity

Intermediated retail clients are highly price- and performance-sensitive, driven by platform comparators and transparency; ETFs, which held over $10 trillion globally by 2024, heighten elasticity and accelerate outflows from underperforming active funds. Share-class engineering and bundled value-add services can moderate churn, while Federated Hermes brand and stewardship credentials strengthen client loyalty and retention.

Switching costs and portability

Operational switching costs at Federated Hermes are moderate; perceived risk varies by retail versus institutional clients, with institutions able to reallocate rapidly after underperformance. Lockups in alternatives (commonly 1–3 years) can delay exits but heighten renewal scrutiny. Consistent alpha and high service quality materially reduce churn.

- Switching costs: moderate

- Alternatives lockups: 1–3 years

- Institutions: fast reallocation

- Alpha/service: key to retention

Demand for ESG and impact

Clients increasingly demand ESG integration and stewardship reporting, giving them specification power over data standards, engagement outcomes and disclosure frequency; Federated Hermes’ long-standing stewardship capabilities address many mandates, but continuous enhancement of reporting, engagement metrics and stewardship tools is required to retain credibility and mandates.

- ESG integration: client-driven specification power

- Data & disclosures: rising granularity expectations

- Stewardship: Federated Hermes heritage aligned with demand

- Need: continuous enhancement to retain mandates

Pensions, SWFs and ETFs drive fee pressure and liquidity risk across global capital pools

Pensions, endowments and sovereigns (global pensions ~$56T; SWFs ~$10.8T in 2023) exert strong fee and mandate specification power, pressuring margins. Consultants/OCIOs gatekeep mandates and force transparency. Retail/ETFs (global ETFs >$10T in 2024) amplify price sensitivity and redemption risk; alternatives lockups 1–3 years mitigate short-term exits.

| Segment | Power | Key datapoint |

|---|---|---|

| Pensions/SWFs | High | $56T / $10.8T (2023) |

| ETFs/Retail | High | $>10T (2024) |

| Alternatives | Moderate | Lockups 1–3 yrs |

Full Version Awaits

Federated Hermes Porter's Five Forces Analysis

This preview shows the exact Federated Hermes Porter's Five Forces analysis you'll receive immediately after purchase; no placeholders or sample pages. The document is the final, professionally formatted version, comprehensive and ready for download. You’ll get instant access to this identical file once you buy.