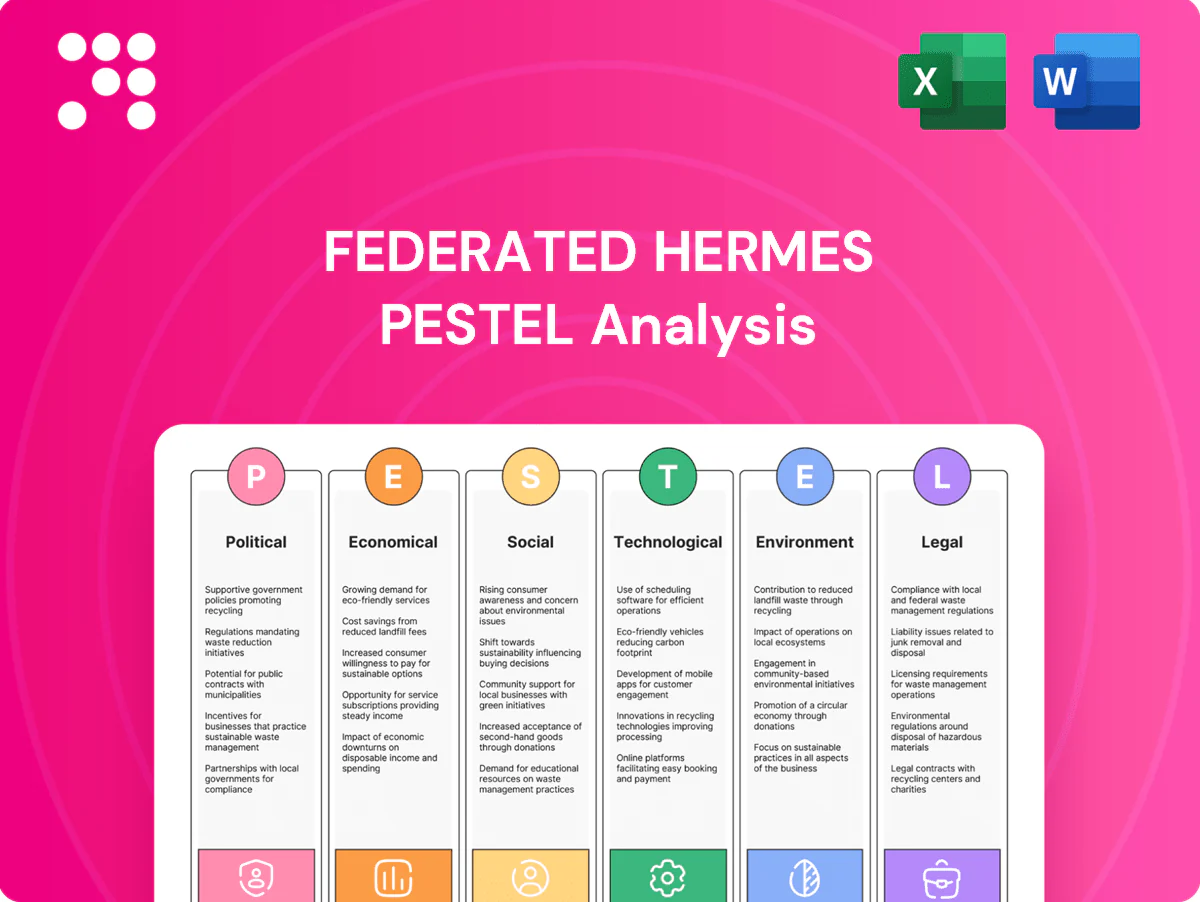

Federated Hermes PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock strategic foresight with our Federated Hermes PESTLE Analysis—concise, actionable insights on political, economic, social, technological, legal and environmental forces shaping performance. Buy the full report for the complete deep-dive and ready-to-use deliverables.

Political factors

Global regulatory alignment

Shifts in SEC (proposals 2022–24), FCA (2023 SDR updates) and EU CSRD rollout (phased 2024–26) are driving tighter coordination in product design and disclosures for Federated Hermes. Divergent rules for funds, benchmarks and stewardship elevate compliance complexity and operational frictions across jurisdictions. Harmonising processes and proactive policy engagement, including IOSCO guidance (2023), helps reduce uncertainty and protect margins.

Geopolitical tensions

Geopolitical tensions — via sanctions, trade restrictions and capital controls — constrain portfolio exposures and custody flows, forcing Federated Hermes to re-route assets and adjust regional weightings; the firm, with roughly £350bn AUM in 2024, reports heightened monitoring of sanctioned jurisdictions. Heightened volatility (VIX avg ~20 in 2024) has shifted client risk appetite and allocation mixes toward liquidity and quality. Cross-border distribution faces licensing delays, extending time-to-market for some products. Scenario planning is used to stress liquidity and counterparty risk under tail scenarios.

Public-sector investment priorities

Fiscal programs and industrial policy shift sector leadership and financing costs; US Bipartisan Infrastructure Law mobilizes roughly $1.2 trillion and the Inflation Reduction Act allocates about $369 billion for clean energy, shaping investment themes. Public pension policies drive mandate pipelines—global pension assets exceed $50 trillion—so close monitoring aligns Federated Hermes strategies with policy-driven flows.

Political scrutiny of ESG

Polarization around ESG has led over 20 US states to adopt or propose restrictions while EU SFDR and evolving national rules reshape labeling, proxy voting and marketing obligations; Federated Hermes must calibrate messages to avoid political backlash. Neutral, outcomes-focused reporting tied to SFDR metrics can help maintain broad client trust.

- Political risk: over 20 US states with ESG actions

- Regulatory focus: SFDR and national disclosure rules

- Firm response: neutral, outcome-based reporting

Tax policy and fund domicile

Changes to fund taxation, carried interest rules or withholding rates — including the OECD Pillar Two 15% minimum tax adopted by 137 jurisdictions — directly reduce after-tax returns and may require fee or structure changes; treaty updates (eg bilateral treaty revisions) reshape cross-border vehicle use and investor onboarding; domicile choice (eg Luxembourg funds holding over €5tn) alters distribution reach and operating costs; regular domicile and tax reviews protect competitiveness and net yields.

- Tax change: OECD Pillar Two 15%

- Treaties: affect cross-border onboarding

- Domicile: distribution reach vs costs (eg Luxembourg >€5tn)

- Action: periodic review to safeguard net yields

Regulation, sanctions and Pillar Two push capital to liquidity, quality and IRA-backed energy

Regulatory tightening (SEC proposals 2022–24, FCA SDR 2023, CSRD phased 2024–26) increases disclosure and product alignment costs for Federated Hermes (≈£350bn AUM in 2024). Geopolitical sanctions and trade limits compress regional exposures; VIX ~20 (2024) shifts clients to liquidity/quality. OECD Pillar Two (15% adopted by 137 jurisd.) and US policy ($1.2T infra, $369B IRA) reshape sector flows and tax mixes.

| Metric | Value |

|---|---|

| AUM (2024) | ≈£350bn |

| VIX (avg 2024) | ~20 |

| Pillar Two | 15%, 137 jurisdictions |

What is included in the product

Explores how external macro-environmental factors uniquely affect Federated Hermes across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights tailored to asset management and its regions to support strategic planning, risk identification and investor communications.

A concise, visually segmented PESTLE summary for Federated Hermes that can be dropped into presentations or shared across teams, with editable notes for regional or business-line context to streamline planning and risk discussions.

Economic factors

Interest-rate cycles

Interest-rate cycles—with the fed funds target at 5.25–5.50% (June 2025) and the 10-year Treasury near 4.1%—push money-market yields and tilt fixed-income flows into cash products while compressing valuation multiples. Higher rates bolster cash offerings but pressure duration-sensitive assets, forcing reallocations when rapid pivots occur. Redemption spikes make dynamic duration and liquidity tools critical for Federated Hermes risk management.

Market volatility and beta

Equity drawdowns, notably the S&P 500 2022 peak-to-trough decline of about 24%, and widened credit spreads compress performance and fee revenue while boosting dispersion among active managers. Volatility shifts investor flows between active and passive, and rising demand for diversification lifted alternatives—global alternatives AUM reached roughly 14.6 trillion in 2023. Risk-managed solutions help stabilize client retention during such swings.

Global growth divergence

IMF (Apr 2025) projects global growth at 3.0% in 2025 with advanced economies at 1.6% and emerging markets ~4.3%, driving asynchronous recoveries that shift regional allocations; a stronger dollar (DXY ~104, ~+6% YoY) materially changes unhedged returns and revenue translation. Emerging market cycles are reshaping appetite for private credit versus equity, while disciplined country selection and FX hedging reduce earnings variability.

Client budget cycles

Corporate and public clients reprice mandates to hit funding ratios and preserve liquidity, with shifts intensified during 2022-23 market stress; fee pressure rose as institutions sought lower-cost indexing while reallocating cash. Federated Hermes leans on solutions-oriented packaging to defend pricing, and long-dated liability-driven mandates help smooth revenue against cyclical headwinds.

- Funding-driven mandate resets

- Fee pressure in downturns

- Packaging preserves fees

- Long-dated mandates stabilize revenue

Inflation dynamics

Inflation shapes real returns: US CPI averaged 3.4% in 2024 (BLS) and euro‑area HICP ~2.5% (Eurostat), driving stronger demand for TIPS and commodity-linked strategies while real yields compressed, lifting TIPS flows.

- Operating costs: wage and tech spend rising

- Pricing discipline: protect margins vs competitiveness

- Product mix: real‑asset/private markets for inflation hedging

Regulation, sanctions and Pillar Two push capital to liquidity, quality and IRA-backed energy

Higher rates (fed funds 5.25–5.50%, 10y ~4.1%, Jun 2025) and volatile equity/credit markets compress multiples, boost cash/money-market flows and elevate redemption risk; disciplined duration/liquidity tools are essential. Global growth (IMF 2025 3.0%) and a stronger dollar (DXY ~104) shift regional allocations and FX translation. Inflation (US CPI 3.4% 2024) lifts demand for TIPS and real‑asset solutions.

| Indicator | Value |

|---|---|

| Fed funds (Jun 2025) | 5.25–5.50% |

| 10‑yr US Treasury | ~4.1% |

| IMF global GDP 2025 | 3.0% |

| DXY | ~104 |

| US CPI 2024 | 3.4% |

| Alternatives AUM 2023 | $14.6T |

Same Document Delivered

Federated Hermes PESTLE Analysis

The preview shown here is the exact Federated Hermes PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or surprises; the file downloads immediately after payment. Everything displayed is final.

Your Competitive Advantage Starts with This Report

Unlock strategic foresight with our Federated Hermes PESTLE Analysis—concise, actionable insights on political, economic, social, technological, legal and environmental forces shaping performance. Buy the full report for the complete deep-dive and ready-to-use deliverables.

Political factors

Global regulatory alignment

Shifts in SEC (proposals 2022–24), FCA (2023 SDR updates) and EU CSRD rollout (phased 2024–26) are driving tighter coordination in product design and disclosures for Federated Hermes. Divergent rules for funds, benchmarks and stewardship elevate compliance complexity and operational frictions across jurisdictions. Harmonising processes and proactive policy engagement, including IOSCO guidance (2023), helps reduce uncertainty and protect margins.

Geopolitical tensions

Geopolitical tensions — via sanctions, trade restrictions and capital controls — constrain portfolio exposures and custody flows, forcing Federated Hermes to re-route assets and adjust regional weightings; the firm, with roughly £350bn AUM in 2024, reports heightened monitoring of sanctioned jurisdictions. Heightened volatility (VIX avg ~20 in 2024) has shifted client risk appetite and allocation mixes toward liquidity and quality. Cross-border distribution faces licensing delays, extending time-to-market for some products. Scenario planning is used to stress liquidity and counterparty risk under tail scenarios.

Public-sector investment priorities

Fiscal programs and industrial policy shift sector leadership and financing costs; US Bipartisan Infrastructure Law mobilizes roughly $1.2 trillion and the Inflation Reduction Act allocates about $369 billion for clean energy, shaping investment themes. Public pension policies drive mandate pipelines—global pension assets exceed $50 trillion—so close monitoring aligns Federated Hermes strategies with policy-driven flows.

Political scrutiny of ESG

Polarization around ESG has led over 20 US states to adopt or propose restrictions while EU SFDR and evolving national rules reshape labeling, proxy voting and marketing obligations; Federated Hermes must calibrate messages to avoid political backlash. Neutral, outcomes-focused reporting tied to SFDR metrics can help maintain broad client trust.

- Political risk: over 20 US states with ESG actions

- Regulatory focus: SFDR and national disclosure rules

- Firm response: neutral, outcome-based reporting

Tax policy and fund domicile

Changes to fund taxation, carried interest rules or withholding rates — including the OECD Pillar Two 15% minimum tax adopted by 137 jurisdictions — directly reduce after-tax returns and may require fee or structure changes; treaty updates (eg bilateral treaty revisions) reshape cross-border vehicle use and investor onboarding; domicile choice (eg Luxembourg funds holding over €5tn) alters distribution reach and operating costs; regular domicile and tax reviews protect competitiveness and net yields.

- Tax change: OECD Pillar Two 15%

- Treaties: affect cross-border onboarding

- Domicile: distribution reach vs costs (eg Luxembourg >€5tn)

- Action: periodic review to safeguard net yields

Regulation, sanctions and Pillar Two push capital to liquidity, quality and IRA-backed energy

Regulatory tightening (SEC proposals 2022–24, FCA SDR 2023, CSRD phased 2024–26) increases disclosure and product alignment costs for Federated Hermes (≈£350bn AUM in 2024). Geopolitical sanctions and trade limits compress regional exposures; VIX ~20 (2024) shifts clients to liquidity/quality. OECD Pillar Two (15% adopted by 137 jurisd.) and US policy ($1.2T infra, $369B IRA) reshape sector flows and tax mixes.

| Metric | Value |

|---|---|

| AUM (2024) | ≈£350bn |

| VIX (avg 2024) | ~20 |

| Pillar Two | 15%, 137 jurisdictions |

What is included in the product

Explores how external macro-environmental factors uniquely affect Federated Hermes across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights tailored to asset management and its regions to support strategic planning, risk identification and investor communications.

A concise, visually segmented PESTLE summary for Federated Hermes that can be dropped into presentations or shared across teams, with editable notes for regional or business-line context to streamline planning and risk discussions.

Economic factors

Interest-rate cycles

Interest-rate cycles—with the fed funds target at 5.25–5.50% (June 2025) and the 10-year Treasury near 4.1%—push money-market yields and tilt fixed-income flows into cash products while compressing valuation multiples. Higher rates bolster cash offerings but pressure duration-sensitive assets, forcing reallocations when rapid pivots occur. Redemption spikes make dynamic duration and liquidity tools critical for Federated Hermes risk management.

Market volatility and beta

Equity drawdowns, notably the S&P 500 2022 peak-to-trough decline of about 24%, and widened credit spreads compress performance and fee revenue while boosting dispersion among active managers. Volatility shifts investor flows between active and passive, and rising demand for diversification lifted alternatives—global alternatives AUM reached roughly 14.6 trillion in 2023. Risk-managed solutions help stabilize client retention during such swings.

Global growth divergence

IMF (Apr 2025) projects global growth at 3.0% in 2025 with advanced economies at 1.6% and emerging markets ~4.3%, driving asynchronous recoveries that shift regional allocations; a stronger dollar (DXY ~104, ~+6% YoY) materially changes unhedged returns and revenue translation. Emerging market cycles are reshaping appetite for private credit versus equity, while disciplined country selection and FX hedging reduce earnings variability.

Client budget cycles

Corporate and public clients reprice mandates to hit funding ratios and preserve liquidity, with shifts intensified during 2022-23 market stress; fee pressure rose as institutions sought lower-cost indexing while reallocating cash. Federated Hermes leans on solutions-oriented packaging to defend pricing, and long-dated liability-driven mandates help smooth revenue against cyclical headwinds.

- Funding-driven mandate resets

- Fee pressure in downturns

- Packaging preserves fees

- Long-dated mandates stabilize revenue

Inflation dynamics

Inflation shapes real returns: US CPI averaged 3.4% in 2024 (BLS) and euro‑area HICP ~2.5% (Eurostat), driving stronger demand for TIPS and commodity-linked strategies while real yields compressed, lifting TIPS flows.

- Operating costs: wage and tech spend rising

- Pricing discipline: protect margins vs competitiveness

- Product mix: real‑asset/private markets for inflation hedging

Regulation, sanctions and Pillar Two push capital to liquidity, quality and IRA-backed energy

Higher rates (fed funds 5.25–5.50%, 10y ~4.1%, Jun 2025) and volatile equity/credit markets compress multiples, boost cash/money-market flows and elevate redemption risk; disciplined duration/liquidity tools are essential. Global growth (IMF 2025 3.0%) and a stronger dollar (DXY ~104) shift regional allocations and FX translation. Inflation (US CPI 3.4% 2024) lifts demand for TIPS and real‑asset solutions.

| Indicator | Value |

|---|---|

| Fed funds (Jun 2025) | 5.25–5.50% |

| 10‑yr US Treasury | ~4.1% |

| IMF global GDP 2025 | 3.0% |

| DXY | ~104 |

| US CPI 2024 | 3.4% |

| Alternatives AUM 2023 | $14.6T |

Same Document Delivered

Federated Hermes PESTLE Analysis

The preview shown here is the exact Federated Hermes PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or surprises; the file downloads immediately after payment. Everything displayed is final.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Unlock strategic foresight with our Federated Hermes PESTLE Analysis—concise, actionable insights on political, economic, social, technological, legal and environmental forces shaping performance. Buy the full report for the complete deep-dive and ready-to-use deliverables.

Political factors

Global regulatory alignment

Shifts in SEC (proposals 2022–24), FCA (2023 SDR updates) and EU CSRD rollout (phased 2024–26) are driving tighter coordination in product design and disclosures for Federated Hermes. Divergent rules for funds, benchmarks and stewardship elevate compliance complexity and operational frictions across jurisdictions. Harmonising processes and proactive policy engagement, including IOSCO guidance (2023), helps reduce uncertainty and protect margins.

Geopolitical tensions

Geopolitical tensions — via sanctions, trade restrictions and capital controls — constrain portfolio exposures and custody flows, forcing Federated Hermes to re-route assets and adjust regional weightings; the firm, with roughly £350bn AUM in 2024, reports heightened monitoring of sanctioned jurisdictions. Heightened volatility (VIX avg ~20 in 2024) has shifted client risk appetite and allocation mixes toward liquidity and quality. Cross-border distribution faces licensing delays, extending time-to-market for some products. Scenario planning is used to stress liquidity and counterparty risk under tail scenarios.

Public-sector investment priorities

Fiscal programs and industrial policy shift sector leadership and financing costs; US Bipartisan Infrastructure Law mobilizes roughly $1.2 trillion and the Inflation Reduction Act allocates about $369 billion for clean energy, shaping investment themes. Public pension policies drive mandate pipelines—global pension assets exceed $50 trillion—so close monitoring aligns Federated Hermes strategies with policy-driven flows.

Political scrutiny of ESG

Polarization around ESG has led over 20 US states to adopt or propose restrictions while EU SFDR and evolving national rules reshape labeling, proxy voting and marketing obligations; Federated Hermes must calibrate messages to avoid political backlash. Neutral, outcomes-focused reporting tied to SFDR metrics can help maintain broad client trust.

- Political risk: over 20 US states with ESG actions

- Regulatory focus: SFDR and national disclosure rules

- Firm response: neutral, outcome-based reporting

Tax policy and fund domicile

Changes to fund taxation, carried interest rules or withholding rates — including the OECD Pillar Two 15% minimum tax adopted by 137 jurisdictions — directly reduce after-tax returns and may require fee or structure changes; treaty updates (eg bilateral treaty revisions) reshape cross-border vehicle use and investor onboarding; domicile choice (eg Luxembourg funds holding over €5tn) alters distribution reach and operating costs; regular domicile and tax reviews protect competitiveness and net yields.

- Tax change: OECD Pillar Two 15%

- Treaties: affect cross-border onboarding

- Domicile: distribution reach vs costs (eg Luxembourg >€5tn)

- Action: periodic review to safeguard net yields

Regulation, sanctions and Pillar Two push capital to liquidity, quality and IRA-backed energy

Regulatory tightening (SEC proposals 2022–24, FCA SDR 2023, CSRD phased 2024–26) increases disclosure and product alignment costs for Federated Hermes (≈£350bn AUM in 2024). Geopolitical sanctions and trade limits compress regional exposures; VIX ~20 (2024) shifts clients to liquidity/quality. OECD Pillar Two (15% adopted by 137 jurisd.) and US policy ($1.2T infra, $369B IRA) reshape sector flows and tax mixes.

| Metric | Value |

|---|---|

| AUM (2024) | ≈£350bn |

| VIX (avg 2024) | ~20 |

| Pillar Two | 15%, 137 jurisdictions |

What is included in the product

Explores how external macro-environmental factors uniquely affect Federated Hermes across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights tailored to asset management and its regions to support strategic planning, risk identification and investor communications.

A concise, visually segmented PESTLE summary for Federated Hermes that can be dropped into presentations or shared across teams, with editable notes for regional or business-line context to streamline planning and risk discussions.

Economic factors

Interest-rate cycles

Interest-rate cycles—with the fed funds target at 5.25–5.50% (June 2025) and the 10-year Treasury near 4.1%—push money-market yields and tilt fixed-income flows into cash products while compressing valuation multiples. Higher rates bolster cash offerings but pressure duration-sensitive assets, forcing reallocations when rapid pivots occur. Redemption spikes make dynamic duration and liquidity tools critical for Federated Hermes risk management.

Market volatility and beta

Equity drawdowns, notably the S&P 500 2022 peak-to-trough decline of about 24%, and widened credit spreads compress performance and fee revenue while boosting dispersion among active managers. Volatility shifts investor flows between active and passive, and rising demand for diversification lifted alternatives—global alternatives AUM reached roughly 14.6 trillion in 2023. Risk-managed solutions help stabilize client retention during such swings.

Global growth divergence

IMF (Apr 2025) projects global growth at 3.0% in 2025 with advanced economies at 1.6% and emerging markets ~4.3%, driving asynchronous recoveries that shift regional allocations; a stronger dollar (DXY ~104, ~+6% YoY) materially changes unhedged returns and revenue translation. Emerging market cycles are reshaping appetite for private credit versus equity, while disciplined country selection and FX hedging reduce earnings variability.

Client budget cycles

Corporate and public clients reprice mandates to hit funding ratios and preserve liquidity, with shifts intensified during 2022-23 market stress; fee pressure rose as institutions sought lower-cost indexing while reallocating cash. Federated Hermes leans on solutions-oriented packaging to defend pricing, and long-dated liability-driven mandates help smooth revenue against cyclical headwinds.

- Funding-driven mandate resets

- Fee pressure in downturns

- Packaging preserves fees

- Long-dated mandates stabilize revenue

Inflation dynamics

Inflation shapes real returns: US CPI averaged 3.4% in 2024 (BLS) and euro‑area HICP ~2.5% (Eurostat), driving stronger demand for TIPS and commodity-linked strategies while real yields compressed, lifting TIPS flows.

- Operating costs: wage and tech spend rising

- Pricing discipline: protect margins vs competitiveness

- Product mix: real‑asset/private markets for inflation hedging

Regulation, sanctions and Pillar Two push capital to liquidity, quality and IRA-backed energy

Higher rates (fed funds 5.25–5.50%, 10y ~4.1%, Jun 2025) and volatile equity/credit markets compress multiples, boost cash/money-market flows and elevate redemption risk; disciplined duration/liquidity tools are essential. Global growth (IMF 2025 3.0%) and a stronger dollar (DXY ~104) shift regional allocations and FX translation. Inflation (US CPI 3.4% 2024) lifts demand for TIPS and real‑asset solutions.

| Indicator | Value |

|---|---|

| Fed funds (Jun 2025) | 5.25–5.50% |

| 10‑yr US Treasury | ~4.1% |

| IMF global GDP 2025 | 3.0% |

| DXY | ~104 |

| US CPI 2024 | 3.4% |

| Alternatives AUM 2023 | $14.6T |

Same Document Delivered

Federated Hermes PESTLE Analysis

The preview shown here is the exact Federated Hermes PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or surprises; the file downloads immediately after payment. Everything displayed is final.