Fedbank Financial Services PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Explore how political shifts, economic cycles, social trends, technological disruption, legal reforms, and environmental pressures are shaping Fedbank Financial Services' strategic outlook. This concise PESTLE snapshot highlights risks and opportunity areas for investors and planners. Purchase the full analysis to unlock detailed, actionable insights and ready-to-use charts for immediate strategy work.

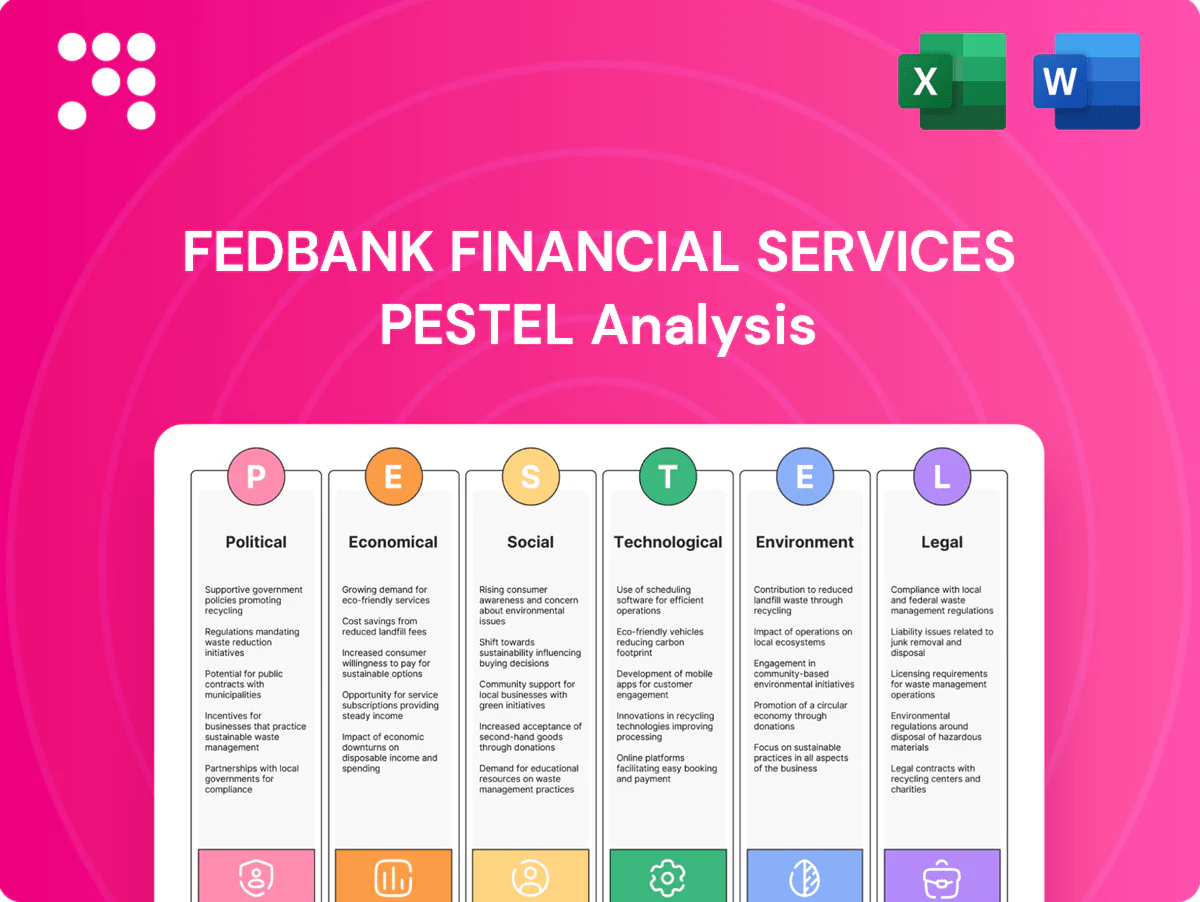

Political factors

Regulatory stance of RBI on NBFCs

RBI’s Scale-Based Regulation, introduced in 2022, sets the tone for NBFC growth, capital buffers and governance; tighter SBR norms increase compliance costs while strengthening sector resilience. Regulatory tightening raises funding and capital costs but improves shock-absorption; targeted relaxation for well-governed retail secured lenders could be growth-accretive. Fedbank Financial Services must align risk, liquidity and governance to these RBI priorities.

Financial inclusion and priority agendas

Government push for credit access—RBI's co-lending scheme launched in 2020 and PMMY which has disbursed over 18 lakh crore—favors secured small-ticket lending, expanding Fedbank Financial Services' addressable market. Schemes encouraging co-lending and MSME credit flow can scale originations, but execution hinges on partner networks and last-mile operational readiness. Brand trust and branch reach amplify these policy tailwinds.

Public-sector influence and competition

Public-sector banks, which still provide roughly 60% of India’s bank credit as of 2024, and large government-backed schemes compress yields and reset customer expectations on price and risk. Subsidised or guarantee-backed MSME lending (several lakh crore rupees in support since 2020) constrains NBFC pricing power. NBFCs must therefore win on speed, convenience and niche underwriting, while selective collaboration with public entities can offset competitive pressure.

Election cycles and policy continuity

Election periods (April–May 2024) can delay policy rollouts and public spending, softening near-term credit demand for Fedbank Financial Services; continuity in central infrastructure and housing programs supports LAP and home‑loan flows. Regulatory certainty post-election lowers cost‑of‑capital volatility, while scenario planning preserves portfolio momentum across cycles.

- Election timing: April–May 2024

- Focus: LAP/home loans benefit from policy continuity

- Risk: temporary credit demand dip during campaign periods

- Mitigation: scenario planning reduces volatility impact

State-level policies and local governance

Stamp duties, registration norms and enforcement efficacy differ materially by state, with stamp/registration cost variances of up to about 300 basis points across Indian states; local administration drives collateral recovery timelines and legal costs, which can range from months to multiple years. Fedbank’s branch-led model must adapt to regional policy nuances; geographic diversification reduces concentrated political risk.

- Stamp/registration variance: ~up to 300 bps

- Recovery timelines: months to years

- Branch model: requires regional policy adaptation

- Diversification: mitigates state-level political concentration

SBR raises resilience and costs; PMMY >18 lakh cr, PSBs ~60%

RBI’s Scale-Based Regulation (2022) raises compliance and capital costs but strengthens resilience; SBR-driven buffers pushed NBFC CET1 and leverage scrutiny higher. PMMY/disbursements >18 lakh crore and co-lending expand small-ticket LAP/home markets; PSBs still supply ~60% of bank credit (2024), pressuring yields. State stamp/registration variance up to ~300 bps affects recovery costs; election timing Apr–May 2024 can transiently soften demand.

| Indicator | 2024/2025 Metric | Implication |

|---|---|---|

| SBR (RBI) | 2022 policy; higher buffers | ↑Compliance, ↑resilience |

| PMMY/co-lending | >18 lakh crore disbursed | ↑Retail originations |

| PSB credit share | ~60% | ↓NBFC pricing power |

| Stamp variance | ~up to 300 bps | ↑Regional cost variability |

| Elections | Apr–May 2024 | Temporary demand dip |

What is included in the product

Provides a concise PESTLE assessment of Fedbank Financial Services, examining Political, Economic, Social, Technological, Environmental and Legal drivers with data-backed trends and region-specific regulatory context; designed for executives and investors to spot risks, opportunities and inform scenario-based strategy.

Condensed PESTLE summary for Fedbank Financial Services that segments political, economic, social, technological, legal and environmental factors for quick team alignment and easy insertion into reports or presentations.

Economic factors

Interest rate cycle and funding costs

RBI repo at 6.50% (July 2025) transmits to NBFC borrowing costs, typically adding 250–400 bps, squeezing lending spreads and affordability for target segments; higher rates can dampen loan demand. Active ALM and diversified funding mix help stabilize NIMs, while strict pricing discipline and secured structures (collateral, LTV limits) protect returns.

GDP growth and MSME health

Economic expansion—India GDP 7.2% in FY2023‑24—boosts MSME cash flows, lifting LAP and business loan originations and reducing defaults; MSMEs contribute ~30% of GDP and ~45% of exports. Slowdowns raise delinquencies and curb ticket sizes. Fedbank limits sectoral exposure and uses counter‑cyclical underwriting with tighter collections to manage cyclicality.

Inflation and household affordability

Rising prices in 2024–25 have squeezed disposable income for emerging middle-income borrowers as inflation in many emerging markets remained above pre-pandemic norms, elevating delinquencies in unsecured cashflows while secured lending shows lower stress due to collateral buffers. Tenor structuring and strict LTV caps have maintained portfolio resilience, keeping secured default rates contained. Fee discipline and targeted cross-sell helped offset yield pressure and preserve net interest margins.

Gold price volatility

Gold loans hinge on collateral value and LTV headroom; Indian households hold about 25,000 tonnes of gold (World Gold Council 2023/2024) and lenders commonly use LTVs up to 75%, so price dips force top-ups or auctions while sharp price spikes expand eligible loan amounts and borrower demand; dynamic risk policies with daily or weekly revaluations are essential.

- LTV up to 75%

- Household gold ~25,000 tonnes

- Revaluations: daily/weekly

Liquidity conditions and capital access

System liquidity remained in surplus through 2024–25 per RBI reports, supporting NBFC bond issuance and expanding Fedbank Financial Services growth capacity.

Periodic risk aversion in 2024 widened spreads for lower-rated issuers, pressuring funding costs and prompting shifts to bank lines, securitisation and co-lending.

Fedbank’s sustained asset quality has helped preserve market access across cycles, enabling diversified capital sources and stable lending capacity.

- RBI: systemic liquidity in surplus through 2024–25

- Market: spreads widened for lower-rated NBFCs in risk-off episodes

- Funding: bank lines, securitisation, co-lending diversify capital

SBR raises resilience and costs; PMMY >18 lakh cr, PSBs ~60%

RBI repo 6.50% (Jul 2025) pushes NBFC borrowing +250–400bps, squeezing spreads; India GDP 7.2% (FY23‑24) supports MSME loan demand (~30% GDP); household gold ~25,000t with LTVs up to 75% drives gold‑loan volatility; systemic liquidity surplus through 2024‑25 aided Fedbank funding despite wider spreads for lower‑rated issuers.

| Metric | Value | Impact |

|---|---|---|

| Repo rate | 6.50% (Jul 2025) | Higher funding cost |

| GDP | 7.2% FY23‑24 | Stronger demand |

| Household gold | ~25,000t | Gold‑loan collateral buffer |

Preview Before You Purchase

Fedbank Financial Services PESTLE Analysis

This Fedbank Financial Services PESTLE Analysis preview is the exact, fully formatted document you’ll receive after purchase. It contains the complete political, economic, social, technological, legal, and environmental analysis—ready to download and use immediately. No placeholders, no surprises.

Plan Smarter. Present Sharper. Compete Stronger.

Explore how political shifts, economic cycles, social trends, technological disruption, legal reforms, and environmental pressures are shaping Fedbank Financial Services' strategic outlook. This concise PESTLE snapshot highlights risks and opportunity areas for investors and planners. Purchase the full analysis to unlock detailed, actionable insights and ready-to-use charts for immediate strategy work.

Political factors

Regulatory stance of RBI on NBFCs

RBI’s Scale-Based Regulation, introduced in 2022, sets the tone for NBFC growth, capital buffers and governance; tighter SBR norms increase compliance costs while strengthening sector resilience. Regulatory tightening raises funding and capital costs but improves shock-absorption; targeted relaxation for well-governed retail secured lenders could be growth-accretive. Fedbank Financial Services must align risk, liquidity and governance to these RBI priorities.

Financial inclusion and priority agendas

Government push for credit access—RBI's co-lending scheme launched in 2020 and PMMY which has disbursed over 18 lakh crore—favors secured small-ticket lending, expanding Fedbank Financial Services' addressable market. Schemes encouraging co-lending and MSME credit flow can scale originations, but execution hinges on partner networks and last-mile operational readiness. Brand trust and branch reach amplify these policy tailwinds.

Public-sector influence and competition

Public-sector banks, which still provide roughly 60% of India’s bank credit as of 2024, and large government-backed schemes compress yields and reset customer expectations on price and risk. Subsidised or guarantee-backed MSME lending (several lakh crore rupees in support since 2020) constrains NBFC pricing power. NBFCs must therefore win on speed, convenience and niche underwriting, while selective collaboration with public entities can offset competitive pressure.

Election cycles and policy continuity

Election periods (April–May 2024) can delay policy rollouts and public spending, softening near-term credit demand for Fedbank Financial Services; continuity in central infrastructure and housing programs supports LAP and home‑loan flows. Regulatory certainty post-election lowers cost‑of‑capital volatility, while scenario planning preserves portfolio momentum across cycles.

- Election timing: April–May 2024

- Focus: LAP/home loans benefit from policy continuity

- Risk: temporary credit demand dip during campaign periods

- Mitigation: scenario planning reduces volatility impact

State-level policies and local governance

Stamp duties, registration norms and enforcement efficacy differ materially by state, with stamp/registration cost variances of up to about 300 basis points across Indian states; local administration drives collateral recovery timelines and legal costs, which can range from months to multiple years. Fedbank’s branch-led model must adapt to regional policy nuances; geographic diversification reduces concentrated political risk.

- Stamp/registration variance: ~up to 300 bps

- Recovery timelines: months to years

- Branch model: requires regional policy adaptation

- Diversification: mitigates state-level political concentration

SBR raises resilience and costs; PMMY >18 lakh cr, PSBs ~60%

RBI’s Scale-Based Regulation (2022) raises compliance and capital costs but strengthens resilience; SBR-driven buffers pushed NBFC CET1 and leverage scrutiny higher. PMMY/disbursements >18 lakh crore and co-lending expand small-ticket LAP/home markets; PSBs still supply ~60% of bank credit (2024), pressuring yields. State stamp/registration variance up to ~300 bps affects recovery costs; election timing Apr–May 2024 can transiently soften demand.

| Indicator | 2024/2025 Metric | Implication |

|---|---|---|

| SBR (RBI) | 2022 policy; higher buffers | ↑Compliance, ↑resilience |

| PMMY/co-lending | >18 lakh crore disbursed | ↑Retail originations |

| PSB credit share | ~60% | ↓NBFC pricing power |

| Stamp variance | ~up to 300 bps | ↑Regional cost variability |

| Elections | Apr–May 2024 | Temporary demand dip |

What is included in the product

Provides a concise PESTLE assessment of Fedbank Financial Services, examining Political, Economic, Social, Technological, Environmental and Legal drivers with data-backed trends and region-specific regulatory context; designed for executives and investors to spot risks, opportunities and inform scenario-based strategy.

Condensed PESTLE summary for Fedbank Financial Services that segments political, economic, social, technological, legal and environmental factors for quick team alignment and easy insertion into reports or presentations.

Economic factors

Interest rate cycle and funding costs

RBI repo at 6.50% (July 2025) transmits to NBFC borrowing costs, typically adding 250–400 bps, squeezing lending spreads and affordability for target segments; higher rates can dampen loan demand. Active ALM and diversified funding mix help stabilize NIMs, while strict pricing discipline and secured structures (collateral, LTV limits) protect returns.

GDP growth and MSME health

Economic expansion—India GDP 7.2% in FY2023‑24—boosts MSME cash flows, lifting LAP and business loan originations and reducing defaults; MSMEs contribute ~30% of GDP and ~45% of exports. Slowdowns raise delinquencies and curb ticket sizes. Fedbank limits sectoral exposure and uses counter‑cyclical underwriting with tighter collections to manage cyclicality.

Inflation and household affordability

Rising prices in 2024–25 have squeezed disposable income for emerging middle-income borrowers as inflation in many emerging markets remained above pre-pandemic norms, elevating delinquencies in unsecured cashflows while secured lending shows lower stress due to collateral buffers. Tenor structuring and strict LTV caps have maintained portfolio resilience, keeping secured default rates contained. Fee discipline and targeted cross-sell helped offset yield pressure and preserve net interest margins.

Gold price volatility

Gold loans hinge on collateral value and LTV headroom; Indian households hold about 25,000 tonnes of gold (World Gold Council 2023/2024) and lenders commonly use LTVs up to 75%, so price dips force top-ups or auctions while sharp price spikes expand eligible loan amounts and borrower demand; dynamic risk policies with daily or weekly revaluations are essential.

- LTV up to 75%

- Household gold ~25,000 tonnes

- Revaluations: daily/weekly

Liquidity conditions and capital access

System liquidity remained in surplus through 2024–25 per RBI reports, supporting NBFC bond issuance and expanding Fedbank Financial Services growth capacity.

Periodic risk aversion in 2024 widened spreads for lower-rated issuers, pressuring funding costs and prompting shifts to bank lines, securitisation and co-lending.

Fedbank’s sustained asset quality has helped preserve market access across cycles, enabling diversified capital sources and stable lending capacity.

- RBI: systemic liquidity in surplus through 2024–25

- Market: spreads widened for lower-rated NBFCs in risk-off episodes

- Funding: bank lines, securitisation, co-lending diversify capital

SBR raises resilience and costs; PMMY >18 lakh cr, PSBs ~60%

RBI repo 6.50% (Jul 2025) pushes NBFC borrowing +250–400bps, squeezing spreads; India GDP 7.2% (FY23‑24) supports MSME loan demand (~30% GDP); household gold ~25,000t with LTVs up to 75% drives gold‑loan volatility; systemic liquidity surplus through 2024‑25 aided Fedbank funding despite wider spreads for lower‑rated issuers.

| Metric | Value | Impact |

|---|---|---|

| Repo rate | 6.50% (Jul 2025) | Higher funding cost |

| GDP | 7.2% FY23‑24 | Stronger demand |

| Household gold | ~25,000t | Gold‑loan collateral buffer |

Preview Before You Purchase

Fedbank Financial Services PESTLE Analysis

This Fedbank Financial Services PESTLE Analysis preview is the exact, fully formatted document you’ll receive after purchase. It contains the complete political, economic, social, technological, legal, and environmental analysis—ready to download and use immediately. No placeholders, no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Explore how political shifts, economic cycles, social trends, technological disruption, legal reforms, and environmental pressures are shaping Fedbank Financial Services' strategic outlook. This concise PESTLE snapshot highlights risks and opportunity areas for investors and planners. Purchase the full analysis to unlock detailed, actionable insights and ready-to-use charts for immediate strategy work.

Political factors

Regulatory stance of RBI on NBFCs

RBI’s Scale-Based Regulation, introduced in 2022, sets the tone for NBFC growth, capital buffers and governance; tighter SBR norms increase compliance costs while strengthening sector resilience. Regulatory tightening raises funding and capital costs but improves shock-absorption; targeted relaxation for well-governed retail secured lenders could be growth-accretive. Fedbank Financial Services must align risk, liquidity and governance to these RBI priorities.

Financial inclusion and priority agendas

Government push for credit access—RBI's co-lending scheme launched in 2020 and PMMY which has disbursed over 18 lakh crore—favors secured small-ticket lending, expanding Fedbank Financial Services' addressable market. Schemes encouraging co-lending and MSME credit flow can scale originations, but execution hinges on partner networks and last-mile operational readiness. Brand trust and branch reach amplify these policy tailwinds.

Public-sector influence and competition

Public-sector banks, which still provide roughly 60% of India’s bank credit as of 2024, and large government-backed schemes compress yields and reset customer expectations on price and risk. Subsidised or guarantee-backed MSME lending (several lakh crore rupees in support since 2020) constrains NBFC pricing power. NBFCs must therefore win on speed, convenience and niche underwriting, while selective collaboration with public entities can offset competitive pressure.

Election cycles and policy continuity

Election periods (April–May 2024) can delay policy rollouts and public spending, softening near-term credit demand for Fedbank Financial Services; continuity in central infrastructure and housing programs supports LAP and home‑loan flows. Regulatory certainty post-election lowers cost‑of‑capital volatility, while scenario planning preserves portfolio momentum across cycles.

- Election timing: April–May 2024

- Focus: LAP/home loans benefit from policy continuity

- Risk: temporary credit demand dip during campaign periods

- Mitigation: scenario planning reduces volatility impact

State-level policies and local governance

Stamp duties, registration norms and enforcement efficacy differ materially by state, with stamp/registration cost variances of up to about 300 basis points across Indian states; local administration drives collateral recovery timelines and legal costs, which can range from months to multiple years. Fedbank’s branch-led model must adapt to regional policy nuances; geographic diversification reduces concentrated political risk.

- Stamp/registration variance: ~up to 300 bps

- Recovery timelines: months to years

- Branch model: requires regional policy adaptation

- Diversification: mitigates state-level political concentration

SBR raises resilience and costs; PMMY >18 lakh cr, PSBs ~60%

RBI’s Scale-Based Regulation (2022) raises compliance and capital costs but strengthens resilience; SBR-driven buffers pushed NBFC CET1 and leverage scrutiny higher. PMMY/disbursements >18 lakh crore and co-lending expand small-ticket LAP/home markets; PSBs still supply ~60% of bank credit (2024), pressuring yields. State stamp/registration variance up to ~300 bps affects recovery costs; election timing Apr–May 2024 can transiently soften demand.

| Indicator | 2024/2025 Metric | Implication |

|---|---|---|

| SBR (RBI) | 2022 policy; higher buffers | ↑Compliance, ↑resilience |

| PMMY/co-lending | >18 lakh crore disbursed | ↑Retail originations |

| PSB credit share | ~60% | ↓NBFC pricing power |

| Stamp variance | ~up to 300 bps | ↑Regional cost variability |

| Elections | Apr–May 2024 | Temporary demand dip |

What is included in the product

Provides a concise PESTLE assessment of Fedbank Financial Services, examining Political, Economic, Social, Technological, Environmental and Legal drivers with data-backed trends and region-specific regulatory context; designed for executives and investors to spot risks, opportunities and inform scenario-based strategy.

Condensed PESTLE summary for Fedbank Financial Services that segments political, economic, social, technological, legal and environmental factors for quick team alignment and easy insertion into reports or presentations.

Economic factors

Interest rate cycle and funding costs

RBI repo at 6.50% (July 2025) transmits to NBFC borrowing costs, typically adding 250–400 bps, squeezing lending spreads and affordability for target segments; higher rates can dampen loan demand. Active ALM and diversified funding mix help stabilize NIMs, while strict pricing discipline and secured structures (collateral, LTV limits) protect returns.

GDP growth and MSME health

Economic expansion—India GDP 7.2% in FY2023‑24—boosts MSME cash flows, lifting LAP and business loan originations and reducing defaults; MSMEs contribute ~30% of GDP and ~45% of exports. Slowdowns raise delinquencies and curb ticket sizes. Fedbank limits sectoral exposure and uses counter‑cyclical underwriting with tighter collections to manage cyclicality.

Inflation and household affordability

Rising prices in 2024–25 have squeezed disposable income for emerging middle-income borrowers as inflation in many emerging markets remained above pre-pandemic norms, elevating delinquencies in unsecured cashflows while secured lending shows lower stress due to collateral buffers. Tenor structuring and strict LTV caps have maintained portfolio resilience, keeping secured default rates contained. Fee discipline and targeted cross-sell helped offset yield pressure and preserve net interest margins.

Gold price volatility

Gold loans hinge on collateral value and LTV headroom; Indian households hold about 25,000 tonnes of gold (World Gold Council 2023/2024) and lenders commonly use LTVs up to 75%, so price dips force top-ups or auctions while sharp price spikes expand eligible loan amounts and borrower demand; dynamic risk policies with daily or weekly revaluations are essential.

- LTV up to 75%

- Household gold ~25,000 tonnes

- Revaluations: daily/weekly

Liquidity conditions and capital access

System liquidity remained in surplus through 2024–25 per RBI reports, supporting NBFC bond issuance and expanding Fedbank Financial Services growth capacity.

Periodic risk aversion in 2024 widened spreads for lower-rated issuers, pressuring funding costs and prompting shifts to bank lines, securitisation and co-lending.

Fedbank’s sustained asset quality has helped preserve market access across cycles, enabling diversified capital sources and stable lending capacity.

- RBI: systemic liquidity in surplus through 2024–25

- Market: spreads widened for lower-rated NBFCs in risk-off episodes

- Funding: bank lines, securitisation, co-lending diversify capital

SBR raises resilience and costs; PMMY >18 lakh cr, PSBs ~60%

RBI repo 6.50% (Jul 2025) pushes NBFC borrowing +250–400bps, squeezing spreads; India GDP 7.2% (FY23‑24) supports MSME loan demand (~30% GDP); household gold ~25,000t with LTVs up to 75% drives gold‑loan volatility; systemic liquidity surplus through 2024‑25 aided Fedbank funding despite wider spreads for lower‑rated issuers.

| Metric | Value | Impact |

|---|---|---|

| Repo rate | 6.50% (Jul 2025) | Higher funding cost |

| GDP | 7.2% FY23‑24 | Stronger demand |

| Household gold | ~25,000t | Gold‑loan collateral buffer |

Preview Before You Purchase

Fedbank Financial Services PESTLE Analysis

This Fedbank Financial Services PESTLE Analysis preview is the exact, fully formatted document you’ll receive after purchase. It contains the complete political, economic, social, technological, legal, and environmental analysis—ready to download and use immediately. No placeholders, no surprises.