Fedrus International SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Explore a concise Fedrus International SWOT snapshot and see why the company stands out in its sector—then unlock the full analysis for in-depth strengths, risks, and growth levers. Purchase the complete, editable report (Word + Excel) for research-grade insights, strategic recommendations, and investor-ready deliverables.

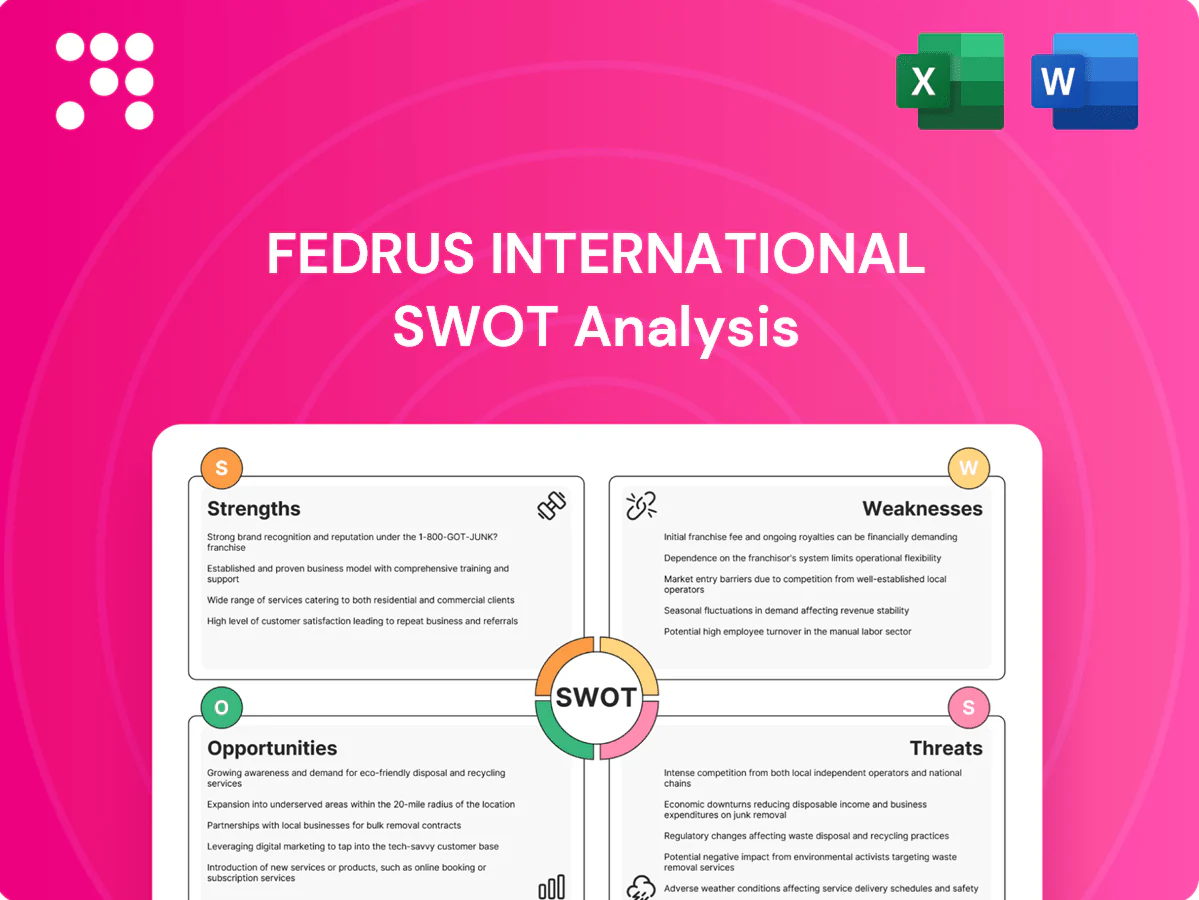

Strengths

Broad building-envelope portfolio

Fedrus International offers membranes, insulation and accessories covering end-to-end envelope needs, enabling bundled specification control across projects. This breadth reduces vendor fragmentation for customers and supports single-source procurement. Cross-selling of envelope components raises average order value while building envelope upgrades can cut HVAC energy use by up to 40% (U.S. DOE), reinforcing value and loyalty.

Integrated solutions capability

Fedrus International’s integrated solutions capability enables delivery of complete systems rather than standalone products, reducing coordination burden and enabling single-source system warranties and verified compatibility that lower risk for contractors and owners. Industry studies in 2024 showed system-based procurements cut on-site installation hours by up to 25% and procurement cycles by roughly 18%, simplifying workflows. This approach strengthens brand trust with specifiers and supports higher-margin bundled sales.

Diverse customer reach

Serving both residential and commercial clients, Fedrus International reduces cyclical risk by balancing revenue from new-build projects and retrofit contracts. Diversified channel access across distributors, contractors and direct sales stabilizes demand through construction and maintenance cycles. This reach allows tailored product and service packages by project size and complexity, improving win rates and margin consistency.

Technical know-how in membranes and insulation

Fedrus International combines deep technical know-how in bituminous and synthetic membranes and insulation assemblies, delivering solutions that meet thermal, moisture and durability performance specifications and supporting architects and engineers with value-engineering and code-compliance advice. This capability strengthens project win rates and positions the firm as a trusted technical partner in complex builds.

- Expertise: membrane + insulation assemblies

- Performance: thermal, moisture, durability

- Advisory: value engineering & compliance

- Market positioning: architects & engineers

Distribution footprint and availability

Integrated manufacturing and distribution shorten lead times, enabling Fedrus to meet contractors’ tight schedules and reduce project delays; this availability boosts service levels and drives repeat business. Strong stock positions act as a practical barrier to entry versus niche producers, supporting contract wins and longer customer lifecycles. Operational integration also improves order fill rates and margin stability.

- Shorter lead times

- Higher order fill rates

- Improved repeat business

- Barrier to niche competitors

Envelope upgrades cut HVAC use up to 40%; systems trim install hours 25%

Fedrus bundles membranes, insulation and accessories for single-source procurement and higher AOV; U.S. DOE finds envelope upgrades can cut HVAC energy use by up to 40%. Integrated system delivery reduces coordination and risk, and 2024 studies show system-based procurements cut on-site installation hours by up to 25% and procurement cycles by ~18%, supporting margins and repeat business.

| Metric | Value | Source |

|---|---|---|

| HVAC energy reduction | up to 40% | U.S. DOE |

| Installation hours | up to 25% ↓ | 2024 studies |

| Procurement cycle | ~18% ↓ | 2024 studies |

What is included in the product

Provides a concise SWOT analysis of Fedrus International, highlighting internal strengths and weaknesses and external opportunities and threats shaping its competitive position and strategic growth prospects.

Provides a concise, visual SWOT matrix tailored to Fedrus International for rapid strategy alignment and stakeholder-ready summaries, enabling quick edits to reflect shifting priorities.

Weaknesses

Material cost sensitivity

Inputs like polymers, bitumen and foams are commodity-linked and accounted for roughly 30–40% of raw-material spend for comparable building-materials firms in 2024, so price swings materially affect margins. Volatility (polymer spot moves ~20% in 2024) squeezes margins when pricing passes lag. Hedging and surcharge mechanisms often trail market moves, undermining project budget predictability.

Project-cycle dependence

Revenue for Fedrus International is highly project-cycle dependent, tying sales to construction starts and refurbishment waves in a global construction market valued at roughly 12 trillion USD; permitting or financing delays—often stretching months—directly cut demand, regional backlog visibility varies widely, and fixed overheads magnify downturns, squeezing margins during slower quarters.

Complex portfolio management

Wide SKU range raises inventory and obsolescence risk, increasing holding costs and write-offs for legacy parts. Ensuring compatibility across product generations demands complex systems engineering and frequent firmware/hardware updates. Training installers across channels is resource-intensive, requiring ongoing programs and certification. Field mistakes can trigger warranty claims and replacement costs that erode margins.

Potential geographic concentration

Concentration of sales in a few countries leaves Fedrus International exposed to sharper impact from regional macro shocks, regulatory changes and housing market slowdowns, which can cascade through revenue and orderbook; cross-border margins are vulnerable to currency volatility, and meaningful geographic diversification will require targeted capital and operational investment.

Brand differentiation vs. global majors

No verified public financials for Fedrus International are available as of July 2025; industry comparisons use market averages for membranes and insulation.

Fedrus competes directly with global majors in membranes and insulation, often facing lower marketing scale and R&D budgets, which forces aggressive pricing to win specs and reduces bargaining power with mega-distributors.

- Competition: multinationals

- Budget gap: marketing/R&D

- Pricing pressure: win specs

- Distribution: limited leverage

Polymer-driven input shocks and project cyclicality squeeze margins in concentrated markets

Raw-materials (polymers/bitumen/foams) account for ~30–40% of spend; polymer spot moved ~20% in 2024, squeezing margins. Revenue is project-cycle dependent in a ~12 trillion USD global construction market, so permitting/financing delays and fixed overheads amplify downturns. Sales concentrated in few countries; FX and competition with global majors force pricing pressure and limit R&D/marketing scale.

| Weakness | Metric | Impact |

|---|---|---|

| Raw-material exposure | 30–40% spend | Margin volatility |

| Polymer volatility | ~20% move (2024) | Pricing lag |

| Market cyclicality | $12T construction market | Demand swings |

| Public disclosures | None (Jul 2025) | Benchmarking limits |

Same Document Delivered

Fedrus International SWOT Analysis

This is a real excerpt from the complete Fedrus International SWOT analysis you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable document included in your download. Buy now to unlock the entire in-depth version immediately after checkout.

Make Insightful Decisions Backed by Expert Research

Explore a concise Fedrus International SWOT snapshot and see why the company stands out in its sector—then unlock the full analysis for in-depth strengths, risks, and growth levers. Purchase the complete, editable report (Word + Excel) for research-grade insights, strategic recommendations, and investor-ready deliverables.

Strengths

Broad building-envelope portfolio

Fedrus International offers membranes, insulation and accessories covering end-to-end envelope needs, enabling bundled specification control across projects. This breadth reduces vendor fragmentation for customers and supports single-source procurement. Cross-selling of envelope components raises average order value while building envelope upgrades can cut HVAC energy use by up to 40% (U.S. DOE), reinforcing value and loyalty.

Integrated solutions capability

Fedrus International’s integrated solutions capability enables delivery of complete systems rather than standalone products, reducing coordination burden and enabling single-source system warranties and verified compatibility that lower risk for contractors and owners. Industry studies in 2024 showed system-based procurements cut on-site installation hours by up to 25% and procurement cycles by roughly 18%, simplifying workflows. This approach strengthens brand trust with specifiers and supports higher-margin bundled sales.

Diverse customer reach

Serving both residential and commercial clients, Fedrus International reduces cyclical risk by balancing revenue from new-build projects and retrofit contracts. Diversified channel access across distributors, contractors and direct sales stabilizes demand through construction and maintenance cycles. This reach allows tailored product and service packages by project size and complexity, improving win rates and margin consistency.

Technical know-how in membranes and insulation

Fedrus International combines deep technical know-how in bituminous and synthetic membranes and insulation assemblies, delivering solutions that meet thermal, moisture and durability performance specifications and supporting architects and engineers with value-engineering and code-compliance advice. This capability strengthens project win rates and positions the firm as a trusted technical partner in complex builds.

- Expertise: membrane + insulation assemblies

- Performance: thermal, moisture, durability

- Advisory: value engineering & compliance

- Market positioning: architects & engineers

Distribution footprint and availability

Integrated manufacturing and distribution shorten lead times, enabling Fedrus to meet contractors’ tight schedules and reduce project delays; this availability boosts service levels and drives repeat business. Strong stock positions act as a practical barrier to entry versus niche producers, supporting contract wins and longer customer lifecycles. Operational integration also improves order fill rates and margin stability.

- Shorter lead times

- Higher order fill rates

- Improved repeat business

- Barrier to niche competitors

Envelope upgrades cut HVAC use up to 40%; systems trim install hours 25%

Fedrus bundles membranes, insulation and accessories for single-source procurement and higher AOV; U.S. DOE finds envelope upgrades can cut HVAC energy use by up to 40%. Integrated system delivery reduces coordination and risk, and 2024 studies show system-based procurements cut on-site installation hours by up to 25% and procurement cycles by ~18%, supporting margins and repeat business.

| Metric | Value | Source |

|---|---|---|

| HVAC energy reduction | up to 40% | U.S. DOE |

| Installation hours | up to 25% ↓ | 2024 studies |

| Procurement cycle | ~18% ↓ | 2024 studies |

What is included in the product

Provides a concise SWOT analysis of Fedrus International, highlighting internal strengths and weaknesses and external opportunities and threats shaping its competitive position and strategic growth prospects.

Provides a concise, visual SWOT matrix tailored to Fedrus International for rapid strategy alignment and stakeholder-ready summaries, enabling quick edits to reflect shifting priorities.

Weaknesses

Material cost sensitivity

Inputs like polymers, bitumen and foams are commodity-linked and accounted for roughly 30–40% of raw-material spend for comparable building-materials firms in 2024, so price swings materially affect margins. Volatility (polymer spot moves ~20% in 2024) squeezes margins when pricing passes lag. Hedging and surcharge mechanisms often trail market moves, undermining project budget predictability.

Project-cycle dependence

Revenue for Fedrus International is highly project-cycle dependent, tying sales to construction starts and refurbishment waves in a global construction market valued at roughly 12 trillion USD; permitting or financing delays—often stretching months—directly cut demand, regional backlog visibility varies widely, and fixed overheads magnify downturns, squeezing margins during slower quarters.

Complex portfolio management

Wide SKU range raises inventory and obsolescence risk, increasing holding costs and write-offs for legacy parts. Ensuring compatibility across product generations demands complex systems engineering and frequent firmware/hardware updates. Training installers across channels is resource-intensive, requiring ongoing programs and certification. Field mistakes can trigger warranty claims and replacement costs that erode margins.

Potential geographic concentration

Concentration of sales in a few countries leaves Fedrus International exposed to sharper impact from regional macro shocks, regulatory changes and housing market slowdowns, which can cascade through revenue and orderbook; cross-border margins are vulnerable to currency volatility, and meaningful geographic diversification will require targeted capital and operational investment.

Brand differentiation vs. global majors

No verified public financials for Fedrus International are available as of July 2025; industry comparisons use market averages for membranes and insulation.

Fedrus competes directly with global majors in membranes and insulation, often facing lower marketing scale and R&D budgets, which forces aggressive pricing to win specs and reduces bargaining power with mega-distributors.

- Competition: multinationals

- Budget gap: marketing/R&D

- Pricing pressure: win specs

- Distribution: limited leverage

Polymer-driven input shocks and project cyclicality squeeze margins in concentrated markets

Raw-materials (polymers/bitumen/foams) account for ~30–40% of spend; polymer spot moved ~20% in 2024, squeezing margins. Revenue is project-cycle dependent in a ~12 trillion USD global construction market, so permitting/financing delays and fixed overheads amplify downturns. Sales concentrated in few countries; FX and competition with global majors force pricing pressure and limit R&D/marketing scale.

| Weakness | Metric | Impact |

|---|---|---|

| Raw-material exposure | 30–40% spend | Margin volatility |

| Polymer volatility | ~20% move (2024) | Pricing lag |

| Market cyclicality | $12T construction market | Demand swings |

| Public disclosures | None (Jul 2025) | Benchmarking limits |

Same Document Delivered

Fedrus International SWOT Analysis

This is a real excerpt from the complete Fedrus International SWOT analysis you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable document included in your download. Buy now to unlock the entire in-depth version immediately after checkout.

Description

Make Insightful Decisions Backed by Expert Research

Explore a concise Fedrus International SWOT snapshot and see why the company stands out in its sector—then unlock the full analysis for in-depth strengths, risks, and growth levers. Purchase the complete, editable report (Word + Excel) for research-grade insights, strategic recommendations, and investor-ready deliverables.

Strengths

Broad building-envelope portfolio

Fedrus International offers membranes, insulation and accessories covering end-to-end envelope needs, enabling bundled specification control across projects. This breadth reduces vendor fragmentation for customers and supports single-source procurement. Cross-selling of envelope components raises average order value while building envelope upgrades can cut HVAC energy use by up to 40% (U.S. DOE), reinforcing value and loyalty.

Integrated solutions capability

Fedrus International’s integrated solutions capability enables delivery of complete systems rather than standalone products, reducing coordination burden and enabling single-source system warranties and verified compatibility that lower risk for contractors and owners. Industry studies in 2024 showed system-based procurements cut on-site installation hours by up to 25% and procurement cycles by roughly 18%, simplifying workflows. This approach strengthens brand trust with specifiers and supports higher-margin bundled sales.

Diverse customer reach

Serving both residential and commercial clients, Fedrus International reduces cyclical risk by balancing revenue from new-build projects and retrofit contracts. Diversified channel access across distributors, contractors and direct sales stabilizes demand through construction and maintenance cycles. This reach allows tailored product and service packages by project size and complexity, improving win rates and margin consistency.

Technical know-how in membranes and insulation

Fedrus International combines deep technical know-how in bituminous and synthetic membranes and insulation assemblies, delivering solutions that meet thermal, moisture and durability performance specifications and supporting architects and engineers with value-engineering and code-compliance advice. This capability strengthens project win rates and positions the firm as a trusted technical partner in complex builds.

- Expertise: membrane + insulation assemblies

- Performance: thermal, moisture, durability

- Advisory: value engineering & compliance

- Market positioning: architects & engineers

Distribution footprint and availability

Integrated manufacturing and distribution shorten lead times, enabling Fedrus to meet contractors’ tight schedules and reduce project delays; this availability boosts service levels and drives repeat business. Strong stock positions act as a practical barrier to entry versus niche producers, supporting contract wins and longer customer lifecycles. Operational integration also improves order fill rates and margin stability.

- Shorter lead times

- Higher order fill rates

- Improved repeat business

- Barrier to niche competitors

Envelope upgrades cut HVAC use up to 40%; systems trim install hours 25%

Fedrus bundles membranes, insulation and accessories for single-source procurement and higher AOV; U.S. DOE finds envelope upgrades can cut HVAC energy use by up to 40%. Integrated system delivery reduces coordination and risk, and 2024 studies show system-based procurements cut on-site installation hours by up to 25% and procurement cycles by ~18%, supporting margins and repeat business.

| Metric | Value | Source |

|---|---|---|

| HVAC energy reduction | up to 40% | U.S. DOE |

| Installation hours | up to 25% ↓ | 2024 studies |

| Procurement cycle | ~18% ↓ | 2024 studies |

What is included in the product

Provides a concise SWOT analysis of Fedrus International, highlighting internal strengths and weaknesses and external opportunities and threats shaping its competitive position and strategic growth prospects.

Provides a concise, visual SWOT matrix tailored to Fedrus International for rapid strategy alignment and stakeholder-ready summaries, enabling quick edits to reflect shifting priorities.

Weaknesses

Material cost sensitivity

Inputs like polymers, bitumen and foams are commodity-linked and accounted for roughly 30–40% of raw-material spend for comparable building-materials firms in 2024, so price swings materially affect margins. Volatility (polymer spot moves ~20% in 2024) squeezes margins when pricing passes lag. Hedging and surcharge mechanisms often trail market moves, undermining project budget predictability.

Project-cycle dependence

Revenue for Fedrus International is highly project-cycle dependent, tying sales to construction starts and refurbishment waves in a global construction market valued at roughly 12 trillion USD; permitting or financing delays—often stretching months—directly cut demand, regional backlog visibility varies widely, and fixed overheads magnify downturns, squeezing margins during slower quarters.

Complex portfolio management

Wide SKU range raises inventory and obsolescence risk, increasing holding costs and write-offs for legacy parts. Ensuring compatibility across product generations demands complex systems engineering and frequent firmware/hardware updates. Training installers across channels is resource-intensive, requiring ongoing programs and certification. Field mistakes can trigger warranty claims and replacement costs that erode margins.

Potential geographic concentration

Concentration of sales in a few countries leaves Fedrus International exposed to sharper impact from regional macro shocks, regulatory changes and housing market slowdowns, which can cascade through revenue and orderbook; cross-border margins are vulnerable to currency volatility, and meaningful geographic diversification will require targeted capital and operational investment.

Brand differentiation vs. global majors

No verified public financials for Fedrus International are available as of July 2025; industry comparisons use market averages for membranes and insulation.

Fedrus competes directly with global majors in membranes and insulation, often facing lower marketing scale and R&D budgets, which forces aggressive pricing to win specs and reduces bargaining power with mega-distributors.

- Competition: multinationals

- Budget gap: marketing/R&D

- Pricing pressure: win specs

- Distribution: limited leverage

Polymer-driven input shocks and project cyclicality squeeze margins in concentrated markets

Raw-materials (polymers/bitumen/foams) account for ~30–40% of spend; polymer spot moved ~20% in 2024, squeezing margins. Revenue is project-cycle dependent in a ~12 trillion USD global construction market, so permitting/financing delays and fixed overheads amplify downturns. Sales concentrated in few countries; FX and competition with global majors force pricing pressure and limit R&D/marketing scale.

| Weakness | Metric | Impact |

|---|---|---|

| Raw-material exposure | 30–40% spend | Margin volatility |

| Polymer volatility | ~20% move (2024) | Pricing lag |

| Market cyclicality | $12T construction market | Demand swings |

| Public disclosures | None (Jul 2025) | Benchmarking limits |

Same Document Delivered

Fedrus International SWOT Analysis

This is a real excerpt from the complete Fedrus International SWOT analysis you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable document included in your download. Buy now to unlock the entire in-depth version immediately after checkout.