Far East Horizon PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, regulatory changes, social trends, technological advances, and environmental risks are shaping Far East Horizon’s strategic outlook. This concise PESTLE preview highlights key external pressures and opportunities. Buy the full analysis for granular insights and ready-to-use strategic recommendations.

Political factors

Central policy direction and financial leasing

China’s State Council and sector regulators set financing priorities for the real economy, shaping leasing quotas, incentives and constraints to steer credit toward strategic areas amid a 2024 GDP growth of about 5.2% (IMF). Emphasis on high-quality development and advanced manufacturing channels support to industry-integrated lessors, favoring asset types tied to tech and green upgrades. Sudden policy shifts—such as tightening around property and local government debt—can swiftly reallocate credit away from vulnerable sectors. Far East Horizon must align portfolios with policy-favored sectors to sustain access to funding and growth.

Healthcare and education policy shifts

Regulatory adjustments in public–private participation, pricing and private education oversight directly affect demand and credit quality for Far East Horizon, as China’s health spending reached about 7% of GDP and continues to expand. Healthcare equipment funding may benefit from import substitution and domestic innovation, with domestic device share near 55% in 2023. Education policy tightening since the 2021 reforms cut private tutoring activity by roughly 60%, curbing lease volumes. Ongoing monitoring of subsidy regimes and procurement rules is critical.

Central–local dynamics and fiscal stress

Local governments’ fiscal health—official local government bond balance ~RMB 40.4 trillion at end‑2023—directly shapes infrastructure, construction and hospital capex, so tighter LGFV controls can slow pipelines and elevate counterparty risk for lenders like Far East Horizon. Beijing’s episodic targeted stimulus (eg. 2023–24 bond and project pushes) can revive demand temporarily. Far East Horizon must deepen local ties and tighten regional risk filters to manage divergence.

Geopolitical tensions and trade controls

US–China tech restrictions (expanded since 2022 and tightened through 2023–24) are constraining availability and raising costs for advanced medical imaging, chips and telecom equipment, increasing procurement lead times. Sanctions and export-control risk force deeper due diligence in cross-border trades and financing; supply-chain rerouting delays deployments and can impair collateral values; diversified sourcing and strict compliance screening are necessary.

- Restrictive export controls: higher equipment costs and longer lead times

- Sanctions risk: elevated KYC and financing scrutiny

- Supply-chain reroute: deployment delays, lower collateral liquidity

- Mitigation: diversified suppliers and enhanced compliance screening

Hong Kong–Mainland regulatory interplay

Hong Kong listing and financing expose Far East Horizon to HKEX governance and disclosure standards while still requiring adherence to Mainland operational and leasing regulations; Stock Connect, launched in 2014, remains the primary channel linking the markets. Evolving capital-account facilitation and Connect enhancements directly influence funding flexibility and cost of capital, and political stability plus cross-border policy coordination drive investor confidence and valuation multiples. Dual-compliance capability (HK and Mainland) is increasingly a competitive, risk-management necessity.

- Tag: StockConnect — launched 2014

- Tag: Dual-compliance — HKEX governance + Mainland rules

- Tag: Funding flexibility — driven by capital-account and Connect changes

- Tag: Investor confidence — tied to political stability and policy coordination

Align assets with Beijing 2024 growth: prioritize advanced manufacturing and green leases

Far East Horizon must align assets with Beijing’s 2024 high‑quality growth focus (China GDP ~5.2% 2024 IMF), favoring advanced-manufacturing and green leases while avoiding property/LGFV exposure (LG bond balance ~RMB40.4trn end‑2023). US–China tech export controls raise equipment costs and lead times; HK listing exposes dual-compliance and funding-cost sensitivity via StockConnect (launched 2014).

| Metric | Value |

|---|---|

| China GDP 2024 | ~5.2% (IMF) |

| LG bond balance | RMB40.4 trn (end‑2023) |

| Healthcare spend | ~7% GDP |

| Domestic device share 2023 | ~55% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Far East Horizon, combining data-driven trends and region-specific examples to reveal risks, opportunities and competitive impacts; delivered in clean, investor-ready format with forward-looking insights for strategic planning.

A concise, visually segmented PESTLE summary of Far East Horizon that streamlines external risk assessment for quick reference in meetings and presentations. Editable notes and export-ready formatting make it easy to drop into decks, share across teams, and support strategic decision-making.

Economic factors

Growth moderation and sectoral rotation

China’s GDP growth has cooled from ~5.2% in 2024 toward the mid-4% range in 2025, compressing broad credit demand and shifting investment into manufacturing and public services. Construction and transport remain exposed to the property downturn, with real estate investment still contracting. Healthcare capex shows relative resilience but procurement and project timelines lengthen under austerity. Portfolio mix should tilt to counter-cyclical clients (utilities, social services, essential manufacturing).

Interest rates and funding costs

PBoC easing since 2023 left benchmark liquidity loose — 1Y MLF around 2.50% and 1Y LPR near 3.45% with 5Y LPR ~4.20% — driving lower lease pricing but compressing margins as credit spreads for onshore ABS (typically 150–300bp) and bank partnerships set funding cost. Tightening of ABS/liquidity would raise origination cost and scale risk. If funding reprices faster than fixed-lease assets, mismatch risk grows. Active ALM and hedging are essential to protect margins.

Credit risk and NPL cycles

Weaker private developers and contractors have raised default probabilities, reducing equipment recovery values and pressuring Far East Horizon’s leasing book; SME transport clients face freight-price volatility and higher fuel costs that strain cashflows. Robust underwriting, sector-concentration limits and collateral remarketing capabilities mitigate loss severity. Early-warning analytics and standardized restructuring playbooks further bolster resilience against NPL cycles.

RMB exchange rate and import equipment

RMB depreciation (around 5–6% y/y in 2023–24; USD/CNY ~7.2–7.4 in 2024–25) raises costs of USD/EUR-priced medical and industrial equipment roughly by the same magnitude, squeezing client affordability and demand for Far East Horizon leasing. FX volatility can compress residual values and tighten refinancing terms for foreign-priced assets, forcing longer tenor or higher spreads. Passing through costs depends on pricing power and vendor partnerships; selective FX hedges and increased use of domestic alternatives mitigate exposure.

- Impact: import cost ≈ +5–6% per 6% RMB fall

- Risk: lower residuals, higher refinancing spreads

- Mitigation: hedging, vendor deals, domestic sourcing

Commodity and energy price swings

Oil and material swings materially affect Far East Horizon: Brent averaged about $85/bbl in 2024, while Chinese rebar and key material prices remained volatile, pushing input costs up by mid-single digits and squeezing construction and logistics operators’ cashflows. Cost shocks tighten debt-service coverage for leased fleets and machinery, raising lessor credit risk. Dynamic covenants and payment holidays have been used to preserve asset value, while scenario-based stress tests (base/adverse/severe) guide provisioning levels.

- Brent ~85 USD/bbl (2024)

- Input costs ↑ mid-single digits (2024 volatility)

- Higher DSCR pressure on leased fleets

- Use of dynamic covenants/payment holidays

- Scenario stress tests inform provisioning

Align assets with Beijing 2024 growth: prioritize advanced manufacturing and green leases

China GDP cooled from ~5.2% (2024) to mid-4% (2025), shifting demand to manufacturing/public services and compressing credit; PBoC easing (1Y MLF ~2.50%, 1Y LPR ~3.45%, 5Y LPR ~4.20%) lowers lease yields and squeezes margins; Brent ~85 USD/bbl (2024) and USD/CNY ~7.2–7.4 (2024–25) raise import costs ~5–6%, pressuring residuals and refinancing.

| Metric | Value | Impact |

|---|---|---|

| China GDP (2025) | mid-4% | weaker credit |

| 1Y MLF / LPR | 2.50% / 3.45% | lower yields |

| 5Y LPR | ~4.20% | lease pricing |

| Brent (2024) | ~85 USD/bbl | input cost shock |

| USD/CNY | 7.2–7.4 | import cost +5–6% |

Preview the Actual Deliverable

Far East Horizon PESTLE Analysis

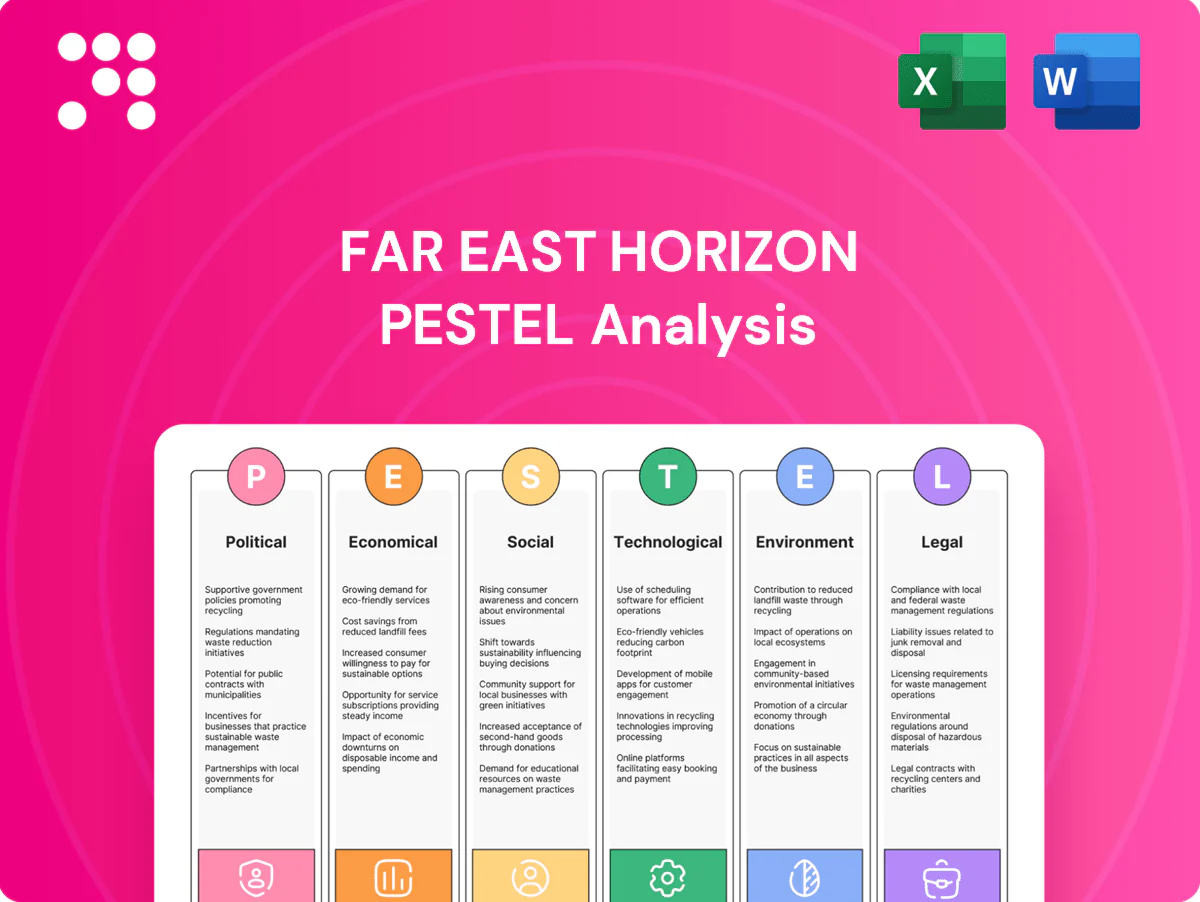

The Far East Horizon PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are the final version with no placeholders or surprises. After payment you’ll instantly download this professionally structured, ready-to-use file.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, regulatory changes, social trends, technological advances, and environmental risks are shaping Far East Horizon’s strategic outlook. This concise PESTLE preview highlights key external pressures and opportunities. Buy the full analysis for granular insights and ready-to-use strategic recommendations.

Political factors

Central policy direction and financial leasing

China’s State Council and sector regulators set financing priorities for the real economy, shaping leasing quotas, incentives and constraints to steer credit toward strategic areas amid a 2024 GDP growth of about 5.2% (IMF). Emphasis on high-quality development and advanced manufacturing channels support to industry-integrated lessors, favoring asset types tied to tech and green upgrades. Sudden policy shifts—such as tightening around property and local government debt—can swiftly reallocate credit away from vulnerable sectors. Far East Horizon must align portfolios with policy-favored sectors to sustain access to funding and growth.

Healthcare and education policy shifts

Regulatory adjustments in public–private participation, pricing and private education oversight directly affect demand and credit quality for Far East Horizon, as China’s health spending reached about 7% of GDP and continues to expand. Healthcare equipment funding may benefit from import substitution and domestic innovation, with domestic device share near 55% in 2023. Education policy tightening since the 2021 reforms cut private tutoring activity by roughly 60%, curbing lease volumes. Ongoing monitoring of subsidy regimes and procurement rules is critical.

Central–local dynamics and fiscal stress

Local governments’ fiscal health—official local government bond balance ~RMB 40.4 trillion at end‑2023—directly shapes infrastructure, construction and hospital capex, so tighter LGFV controls can slow pipelines and elevate counterparty risk for lenders like Far East Horizon. Beijing’s episodic targeted stimulus (eg. 2023–24 bond and project pushes) can revive demand temporarily. Far East Horizon must deepen local ties and tighten regional risk filters to manage divergence.

Geopolitical tensions and trade controls

US–China tech restrictions (expanded since 2022 and tightened through 2023–24) are constraining availability and raising costs for advanced medical imaging, chips and telecom equipment, increasing procurement lead times. Sanctions and export-control risk force deeper due diligence in cross-border trades and financing; supply-chain rerouting delays deployments and can impair collateral values; diversified sourcing and strict compliance screening are necessary.

- Restrictive export controls: higher equipment costs and longer lead times

- Sanctions risk: elevated KYC and financing scrutiny

- Supply-chain reroute: deployment delays, lower collateral liquidity

- Mitigation: diversified suppliers and enhanced compliance screening

Hong Kong–Mainland regulatory interplay

Hong Kong listing and financing expose Far East Horizon to HKEX governance and disclosure standards while still requiring adherence to Mainland operational and leasing regulations; Stock Connect, launched in 2014, remains the primary channel linking the markets. Evolving capital-account facilitation and Connect enhancements directly influence funding flexibility and cost of capital, and political stability plus cross-border policy coordination drive investor confidence and valuation multiples. Dual-compliance capability (HK and Mainland) is increasingly a competitive, risk-management necessity.

- Tag: StockConnect — launched 2014

- Tag: Dual-compliance — HKEX governance + Mainland rules

- Tag: Funding flexibility — driven by capital-account and Connect changes

- Tag: Investor confidence — tied to political stability and policy coordination

Align assets with Beijing 2024 growth: prioritize advanced manufacturing and green leases

Far East Horizon must align assets with Beijing’s 2024 high‑quality growth focus (China GDP ~5.2% 2024 IMF), favoring advanced-manufacturing and green leases while avoiding property/LGFV exposure (LG bond balance ~RMB40.4trn end‑2023). US–China tech export controls raise equipment costs and lead times; HK listing exposes dual-compliance and funding-cost sensitivity via StockConnect (launched 2014).

| Metric | Value |

|---|---|

| China GDP 2024 | ~5.2% (IMF) |

| LG bond balance | RMB40.4 trn (end‑2023) |

| Healthcare spend | ~7% GDP |

| Domestic device share 2023 | ~55% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Far East Horizon, combining data-driven trends and region-specific examples to reveal risks, opportunities and competitive impacts; delivered in clean, investor-ready format with forward-looking insights for strategic planning.

A concise, visually segmented PESTLE summary of Far East Horizon that streamlines external risk assessment for quick reference in meetings and presentations. Editable notes and export-ready formatting make it easy to drop into decks, share across teams, and support strategic decision-making.

Economic factors

Growth moderation and sectoral rotation

China’s GDP growth has cooled from ~5.2% in 2024 toward the mid-4% range in 2025, compressing broad credit demand and shifting investment into manufacturing and public services. Construction and transport remain exposed to the property downturn, with real estate investment still contracting. Healthcare capex shows relative resilience but procurement and project timelines lengthen under austerity. Portfolio mix should tilt to counter-cyclical clients (utilities, social services, essential manufacturing).

Interest rates and funding costs

PBoC easing since 2023 left benchmark liquidity loose — 1Y MLF around 2.50% and 1Y LPR near 3.45% with 5Y LPR ~4.20% — driving lower lease pricing but compressing margins as credit spreads for onshore ABS (typically 150–300bp) and bank partnerships set funding cost. Tightening of ABS/liquidity would raise origination cost and scale risk. If funding reprices faster than fixed-lease assets, mismatch risk grows. Active ALM and hedging are essential to protect margins.

Credit risk and NPL cycles

Weaker private developers and contractors have raised default probabilities, reducing equipment recovery values and pressuring Far East Horizon’s leasing book; SME transport clients face freight-price volatility and higher fuel costs that strain cashflows. Robust underwriting, sector-concentration limits and collateral remarketing capabilities mitigate loss severity. Early-warning analytics and standardized restructuring playbooks further bolster resilience against NPL cycles.

RMB exchange rate and import equipment

RMB depreciation (around 5–6% y/y in 2023–24; USD/CNY ~7.2–7.4 in 2024–25) raises costs of USD/EUR-priced medical and industrial equipment roughly by the same magnitude, squeezing client affordability and demand for Far East Horizon leasing. FX volatility can compress residual values and tighten refinancing terms for foreign-priced assets, forcing longer tenor or higher spreads. Passing through costs depends on pricing power and vendor partnerships; selective FX hedges and increased use of domestic alternatives mitigate exposure.

- Impact: import cost ≈ +5–6% per 6% RMB fall

- Risk: lower residuals, higher refinancing spreads

- Mitigation: hedging, vendor deals, domestic sourcing

Commodity and energy price swings

Oil and material swings materially affect Far East Horizon: Brent averaged about $85/bbl in 2024, while Chinese rebar and key material prices remained volatile, pushing input costs up by mid-single digits and squeezing construction and logistics operators’ cashflows. Cost shocks tighten debt-service coverage for leased fleets and machinery, raising lessor credit risk. Dynamic covenants and payment holidays have been used to preserve asset value, while scenario-based stress tests (base/adverse/severe) guide provisioning levels.

- Brent ~85 USD/bbl (2024)

- Input costs ↑ mid-single digits (2024 volatility)

- Higher DSCR pressure on leased fleets

- Use of dynamic covenants/payment holidays

- Scenario stress tests inform provisioning

Align assets with Beijing 2024 growth: prioritize advanced manufacturing and green leases

China GDP cooled from ~5.2% (2024) to mid-4% (2025), shifting demand to manufacturing/public services and compressing credit; PBoC easing (1Y MLF ~2.50%, 1Y LPR ~3.45%, 5Y LPR ~4.20%) lowers lease yields and squeezes margins; Brent ~85 USD/bbl (2024) and USD/CNY ~7.2–7.4 (2024–25) raise import costs ~5–6%, pressuring residuals and refinancing.

| Metric | Value | Impact |

|---|---|---|

| China GDP (2025) | mid-4% | weaker credit |

| 1Y MLF / LPR | 2.50% / 3.45% | lower yields |

| 5Y LPR | ~4.20% | lease pricing |

| Brent (2024) | ~85 USD/bbl | input cost shock |

| USD/CNY | 7.2–7.4 | import cost +5–6% |

Preview the Actual Deliverable

Far East Horizon PESTLE Analysis

The Far East Horizon PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are the final version with no placeholders or surprises. After payment you’ll instantly download this professionally structured, ready-to-use file.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, regulatory changes, social trends, technological advances, and environmental risks are shaping Far East Horizon’s strategic outlook. This concise PESTLE preview highlights key external pressures and opportunities. Buy the full analysis for granular insights and ready-to-use strategic recommendations.

Political factors

Central policy direction and financial leasing

China’s State Council and sector regulators set financing priorities for the real economy, shaping leasing quotas, incentives and constraints to steer credit toward strategic areas amid a 2024 GDP growth of about 5.2% (IMF). Emphasis on high-quality development and advanced manufacturing channels support to industry-integrated lessors, favoring asset types tied to tech and green upgrades. Sudden policy shifts—such as tightening around property and local government debt—can swiftly reallocate credit away from vulnerable sectors. Far East Horizon must align portfolios with policy-favored sectors to sustain access to funding and growth.

Healthcare and education policy shifts

Regulatory adjustments in public–private participation, pricing and private education oversight directly affect demand and credit quality for Far East Horizon, as China’s health spending reached about 7% of GDP and continues to expand. Healthcare equipment funding may benefit from import substitution and domestic innovation, with domestic device share near 55% in 2023. Education policy tightening since the 2021 reforms cut private tutoring activity by roughly 60%, curbing lease volumes. Ongoing monitoring of subsidy regimes and procurement rules is critical.

Central–local dynamics and fiscal stress

Local governments’ fiscal health—official local government bond balance ~RMB 40.4 trillion at end‑2023—directly shapes infrastructure, construction and hospital capex, so tighter LGFV controls can slow pipelines and elevate counterparty risk for lenders like Far East Horizon. Beijing’s episodic targeted stimulus (eg. 2023–24 bond and project pushes) can revive demand temporarily. Far East Horizon must deepen local ties and tighten regional risk filters to manage divergence.

Geopolitical tensions and trade controls

US–China tech restrictions (expanded since 2022 and tightened through 2023–24) are constraining availability and raising costs for advanced medical imaging, chips and telecom equipment, increasing procurement lead times. Sanctions and export-control risk force deeper due diligence in cross-border trades and financing; supply-chain rerouting delays deployments and can impair collateral values; diversified sourcing and strict compliance screening are necessary.

- Restrictive export controls: higher equipment costs and longer lead times

- Sanctions risk: elevated KYC and financing scrutiny

- Supply-chain reroute: deployment delays, lower collateral liquidity

- Mitigation: diversified suppliers and enhanced compliance screening

Hong Kong–Mainland regulatory interplay

Hong Kong listing and financing expose Far East Horizon to HKEX governance and disclosure standards while still requiring adherence to Mainland operational and leasing regulations; Stock Connect, launched in 2014, remains the primary channel linking the markets. Evolving capital-account facilitation and Connect enhancements directly influence funding flexibility and cost of capital, and political stability plus cross-border policy coordination drive investor confidence and valuation multiples. Dual-compliance capability (HK and Mainland) is increasingly a competitive, risk-management necessity.

- Tag: StockConnect — launched 2014

- Tag: Dual-compliance — HKEX governance + Mainland rules

- Tag: Funding flexibility — driven by capital-account and Connect changes

- Tag: Investor confidence — tied to political stability and policy coordination

Align assets with Beijing 2024 growth: prioritize advanced manufacturing and green leases

Far East Horizon must align assets with Beijing’s 2024 high‑quality growth focus (China GDP ~5.2% 2024 IMF), favoring advanced-manufacturing and green leases while avoiding property/LGFV exposure (LG bond balance ~RMB40.4trn end‑2023). US–China tech export controls raise equipment costs and lead times; HK listing exposes dual-compliance and funding-cost sensitivity via StockConnect (launched 2014).

| Metric | Value |

|---|---|

| China GDP 2024 | ~5.2% (IMF) |

| LG bond balance | RMB40.4 trn (end‑2023) |

| Healthcare spend | ~7% GDP |

| Domestic device share 2023 | ~55% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Far East Horizon, combining data-driven trends and region-specific examples to reveal risks, opportunities and competitive impacts; delivered in clean, investor-ready format with forward-looking insights for strategic planning.

A concise, visually segmented PESTLE summary of Far East Horizon that streamlines external risk assessment for quick reference in meetings and presentations. Editable notes and export-ready formatting make it easy to drop into decks, share across teams, and support strategic decision-making.

Economic factors

Growth moderation and sectoral rotation

China’s GDP growth has cooled from ~5.2% in 2024 toward the mid-4% range in 2025, compressing broad credit demand and shifting investment into manufacturing and public services. Construction and transport remain exposed to the property downturn, with real estate investment still contracting. Healthcare capex shows relative resilience but procurement and project timelines lengthen under austerity. Portfolio mix should tilt to counter-cyclical clients (utilities, social services, essential manufacturing).

Interest rates and funding costs

PBoC easing since 2023 left benchmark liquidity loose — 1Y MLF around 2.50% and 1Y LPR near 3.45% with 5Y LPR ~4.20% — driving lower lease pricing but compressing margins as credit spreads for onshore ABS (typically 150–300bp) and bank partnerships set funding cost. Tightening of ABS/liquidity would raise origination cost and scale risk. If funding reprices faster than fixed-lease assets, mismatch risk grows. Active ALM and hedging are essential to protect margins.

Credit risk and NPL cycles

Weaker private developers and contractors have raised default probabilities, reducing equipment recovery values and pressuring Far East Horizon’s leasing book; SME transport clients face freight-price volatility and higher fuel costs that strain cashflows. Robust underwriting, sector-concentration limits and collateral remarketing capabilities mitigate loss severity. Early-warning analytics and standardized restructuring playbooks further bolster resilience against NPL cycles.

RMB exchange rate and import equipment

RMB depreciation (around 5–6% y/y in 2023–24; USD/CNY ~7.2–7.4 in 2024–25) raises costs of USD/EUR-priced medical and industrial equipment roughly by the same magnitude, squeezing client affordability and demand for Far East Horizon leasing. FX volatility can compress residual values and tighten refinancing terms for foreign-priced assets, forcing longer tenor or higher spreads. Passing through costs depends on pricing power and vendor partnerships; selective FX hedges and increased use of domestic alternatives mitigate exposure.

- Impact: import cost ≈ +5–6% per 6% RMB fall

- Risk: lower residuals, higher refinancing spreads

- Mitigation: hedging, vendor deals, domestic sourcing

Commodity and energy price swings

Oil and material swings materially affect Far East Horizon: Brent averaged about $85/bbl in 2024, while Chinese rebar and key material prices remained volatile, pushing input costs up by mid-single digits and squeezing construction and logistics operators’ cashflows. Cost shocks tighten debt-service coverage for leased fleets and machinery, raising lessor credit risk. Dynamic covenants and payment holidays have been used to preserve asset value, while scenario-based stress tests (base/adverse/severe) guide provisioning levels.

- Brent ~85 USD/bbl (2024)

- Input costs ↑ mid-single digits (2024 volatility)

- Higher DSCR pressure on leased fleets

- Use of dynamic covenants/payment holidays

- Scenario stress tests inform provisioning

Align assets with Beijing 2024 growth: prioritize advanced manufacturing and green leases

China GDP cooled from ~5.2% (2024) to mid-4% (2025), shifting demand to manufacturing/public services and compressing credit; PBoC easing (1Y MLF ~2.50%, 1Y LPR ~3.45%, 5Y LPR ~4.20%) lowers lease yields and squeezes margins; Brent ~85 USD/bbl (2024) and USD/CNY ~7.2–7.4 (2024–25) raise import costs ~5–6%, pressuring residuals and refinancing.

| Metric | Value | Impact |

|---|---|---|

| China GDP (2025) | mid-4% | weaker credit |

| 1Y MLF / LPR | 2.50% / 3.45% | lower yields |

| 5Y LPR | ~4.20% | lease pricing |

| Brent (2024) | ~85 USD/bbl | input cost shock |

| USD/CNY | 7.2–7.4 | import cost +5–6% |

Preview the Actual Deliverable

Far East Horizon PESTLE Analysis

The Far East Horizon PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are the final version with no placeholders or surprises. After payment you’ll instantly download this professionally structured, ready-to-use file.