Fuyo General Lease PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are reshaping Fuyo General Lease’s outlook in our concise PESTLE snapshot—ideal for investors and strategists seeking a competitive edge. This professionally researched analysis highlights risks and opportunities you can act on immediately. Purchase the full PESTLE to access the complete, editable report and make informed decisions today.

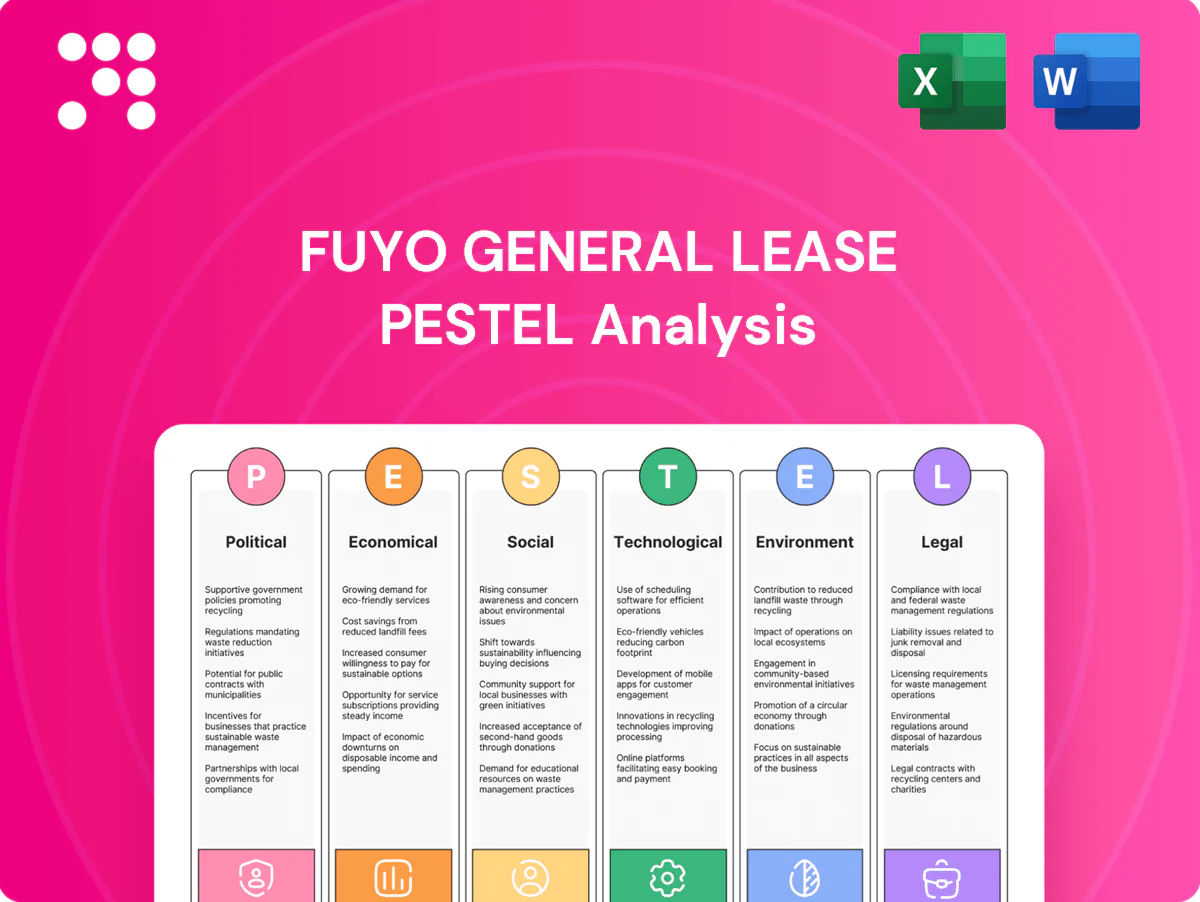

Political factors

Japan’s industrial and SME support policies

Pro-growth programs, subsidies and tax incentives in Japan—where SMEs number about 3.7 million and represent roughly 99.7% of firms and 70% of employment—encourage capital investment that underpins leasing demand. Fuyo can package leases with government-backed guarantees and subsidy schemes to reduce client cost of capital. Policy continuity favors manufacturing, healthcare and logistics, though shifts in priority sectors can re-weight origination pipelines.

Energy transition and green procurement directives

Japan’s GX policies target carbon neutrality by 2050 with a 46% GHG reduction by 2030, and stronger public-sector green procurement is steering buyers toward low‑carbon assets. This shifts demand to renewable, efficiency and EV-related leases, and public procurement—about 12% of GDP (OECD)—amplifies scale. Fuyo can leverage subsidies and preferential financing to structure competitive solutions, while tightening policy raises risk and potential penalties for high‑emission legacy asset classes.

Geopolitical tensions and supply chain security

US export controls on advanced semiconductors and AI chips to China since 2022 and regional security frictions raise equipment scarcity and price pressure for lessors. Japan has rolled out roughly ¥2.2 trillion in reshoring/supply-chain resilience support in 2023–24, likely boosting domestic capex. Historical disruptions produced delivery delays of months, driving cost spikes that affect lease terms and residual assumptions. Diversified sourcing and cross-border risk controls are therefore critical.

Public infrastructure and digital nation initiatives

Government pushes into data centers, 5G and public infrastructure increase leasing demand for equipment and property, aligning Fuyo General Lease with municipal/quasi-public projects; global data‑center investment topped about $180B in 2023 and is forecast to exceed $220B by 2025 (IDC), favoring long‑tenor, lower‑risk assets but dependent on budget cycles and procurement rules.

Monetary-fiscal coordination and political stability

Japan’s stable governance limits abrupt regulatory shocks, supporting Fuyo’s multi-year planning; public debt stood at about 262% of GDP (IMF 2024), so fiscal consolidation pressures could prompt changes to lease tax treatment and incentives. Policy continuity with cautious monetary normalization affects funding spreads and refinancing costs; Fuyo should scenario-plan for shifts in public borrowing and subsidies.

- IMF 2024: public debt ~262% GDP

- Risk: tax changes to lease accounting/incentives

- Impact: funding/refinancing cost sensitivity

- Action: scenario-plan for subsidy and borrowing shifts

Japan policy, GX and reshoring drive low‑carbon capex amid subsidy and budget timing risk

Stable Japanese policy and pro-growth subsidies (SMEs ~3.7M; 70% employment) support leasing demand, while GX targets (carbon neutrality by 2050; −46% GHG by 2030) shift demand to low‑carbon assets. US export controls and ¥2.2T reshoring support (2023–24) raise equipment scarcity and domestic capex. Public procurement (~12% GDP) and high public debt (~262% GDP, IMF 2024) make budget timing and subsidy risk material.

| Metric | Value |

|---|---|

| SMEs | ~3.7M |

| Public procurement | ~12% GDP |

| Public debt | ~262% GDP (IMF 2024) |

| Data‑center capex | $180B (2023) → $220B+ (2025 est.) |

| Reshoring support | ¥2.2T (2023–24) |

What is included in the product

Explores how macro-environmental factors uniquely impact Fuyo General Lease across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses.

A concise, visually segmented PESTLE summary for Fuyo General Lease that frees teams from deep-dive prep by highlighting key political, economic, social, technological, legal and environmental risks at a glance. Easily shareable and editable for presentations, regional notes, or risk workshops to streamline strategic alignment and decision-making.

Economic factors

BOJ rate normalization and funding costs

BOJ rate normalization has lifted funding costs for lessors as 10-year JGB yields moved to about 0.6% in 2024, tightening margins; pricing discipline and active duration hedging are essential to protect spreads. Variable-rate pass-through and shorter-tenor leases help mitigate margin compression, but intense competition in commoditized segments may cap repricing power and slow recovery of yields.

Yen volatility and cross-border asset values

Yen swings—USD/JPY averaged about 150 in 2024 after trading between roughly 140–160 since 2022—drive residual values for aircraft, ships and imported equipment, making asset valuations cyclical. Hedging and currency‑matched financing are widely used to stabilize returns and preserve margins. Clients’ FX exposures materially affect credit risk and demand timing, while a weak yen tends to lift export-sector capex yet raises import costs and maintenance expenses.

Capex cycle across manufacturing and services

Moderate inflation (Japan core CPI ~3% in 2024) and wage gains (shunto raises around 3–4% in 2024) support steady corporate capex, sustaining leasing demand. Automation, logistics and healthcare equipment — sectors where Fuyo has exposure — underpinned resilient volumes, with global robotics investment up ~10% in 2024. Cyclical slowdowns compress originations and raise credit risk, requiring agile asset allocation and remarketing.

Real estate market bifurcation

Prime logistics and hyperscale data centers remained robust into H1 2025, with prime logistics cap rates in Japan compressing to about 3.0–3.5% while some Tokyo office submarkets show softness with vacancy near 7% and rising obsolescence risk. Lease underwriting must build in higher vacancy and refurbishment capex; recent interest-rate volatility lifted cap-rate sensitivity and tightened debt-service coverage ratios. Active asset management and sale-leaseback deals are being used to unlock liquidity and derisk portfolios.

- Prime logistics cap rates ~3.0–3.5% (H1 2025)

- Tokyo office vacancy ~7% (H1 2025)

- Sale-leaseback = liquidity + off-balance risk transfer

Credit cycle and SME health

METI reports SMEs represent 99.7% of Japanese firms and employ about 70% of the workforce; tightening financial conditions since 2022 have elevated funding costs and stressed vulnerable SMEs, raising delinquency risks.

Enhanced credit analytics, tighter collateral monitoring and faster workout processes are essential; government credit guarantee schemes provide partial loss absorption, so pricing must reflect higher PD/LGD and extended recovery timelines.

- SME footprint: 99.7% firms / ~70% employment

- Action: tighten PD/LGD modeling

- Mitigation: use guarantee coverage in loss estimates

- Ops: increase collateral monitoring & recovery speed

Japan policy, GX and reshoring drive low‑carbon capex amid subsidy and budget timing risk

BOJ rate normalization (10y JGB ~0.6% in 2024) raised funding costs, pressuring spreads and forcing tighter pricing and duration hedging. Yen volatility (USD/JPY ~150 avg in 2024) and moderate inflation (core CPI ~3% in 2024) make asset values and capex cyclical; sectoral demand (logistics, data centers) remains strongest. SME stress (99.7% firms; ~70% workforce) raises PD/LGD, so tighter credit and guarantee-aware pricing are required.

| Metric | Value/Date |

|---|---|

| 10y JGB yield | ~0.6% (2024) |

| USD/JPY | ~150 avg (2024) |

| Japan core CPI | ~3% (2024) |

| Shunto wage | 3–4% (2024) |

| Logistics cap rate | 3.0–3.5% (H1 2025) |

| Tokyo office vacancy | ~7% (H1 2025) |

| SME share | 99.7% firms / ~70% employment |

Full Version Awaits

Fuyo General Lease PESTLE Analysis

This Fuyo General Lease PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It covers political, economic, social, technological, legal, and environmental factors specific to Fuyo General Lease with no placeholders or teasers. After checkout you’ll instantly download this same finished file.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are reshaping Fuyo General Lease’s outlook in our concise PESTLE snapshot—ideal for investors and strategists seeking a competitive edge. This professionally researched analysis highlights risks and opportunities you can act on immediately. Purchase the full PESTLE to access the complete, editable report and make informed decisions today.

Political factors

Japan’s industrial and SME support policies

Pro-growth programs, subsidies and tax incentives in Japan—where SMEs number about 3.7 million and represent roughly 99.7% of firms and 70% of employment—encourage capital investment that underpins leasing demand. Fuyo can package leases with government-backed guarantees and subsidy schemes to reduce client cost of capital. Policy continuity favors manufacturing, healthcare and logistics, though shifts in priority sectors can re-weight origination pipelines.

Energy transition and green procurement directives

Japan’s GX policies target carbon neutrality by 2050 with a 46% GHG reduction by 2030, and stronger public-sector green procurement is steering buyers toward low‑carbon assets. This shifts demand to renewable, efficiency and EV-related leases, and public procurement—about 12% of GDP (OECD)—amplifies scale. Fuyo can leverage subsidies and preferential financing to structure competitive solutions, while tightening policy raises risk and potential penalties for high‑emission legacy asset classes.

Geopolitical tensions and supply chain security

US export controls on advanced semiconductors and AI chips to China since 2022 and regional security frictions raise equipment scarcity and price pressure for lessors. Japan has rolled out roughly ¥2.2 trillion in reshoring/supply-chain resilience support in 2023–24, likely boosting domestic capex. Historical disruptions produced delivery delays of months, driving cost spikes that affect lease terms and residual assumptions. Diversified sourcing and cross-border risk controls are therefore critical.

Public infrastructure and digital nation initiatives

Government pushes into data centers, 5G and public infrastructure increase leasing demand for equipment and property, aligning Fuyo General Lease with municipal/quasi-public projects; global data‑center investment topped about $180B in 2023 and is forecast to exceed $220B by 2025 (IDC), favoring long‑tenor, lower‑risk assets but dependent on budget cycles and procurement rules.

Monetary-fiscal coordination and political stability

Japan’s stable governance limits abrupt regulatory shocks, supporting Fuyo’s multi-year planning; public debt stood at about 262% of GDP (IMF 2024), so fiscal consolidation pressures could prompt changes to lease tax treatment and incentives. Policy continuity with cautious monetary normalization affects funding spreads and refinancing costs; Fuyo should scenario-plan for shifts in public borrowing and subsidies.

- IMF 2024: public debt ~262% GDP

- Risk: tax changes to lease accounting/incentives

- Impact: funding/refinancing cost sensitivity

- Action: scenario-plan for subsidy and borrowing shifts

Japan policy, GX and reshoring drive low‑carbon capex amid subsidy and budget timing risk

Stable Japanese policy and pro-growth subsidies (SMEs ~3.7M; 70% employment) support leasing demand, while GX targets (carbon neutrality by 2050; −46% GHG by 2030) shift demand to low‑carbon assets. US export controls and ¥2.2T reshoring support (2023–24) raise equipment scarcity and domestic capex. Public procurement (~12% GDP) and high public debt (~262% GDP, IMF 2024) make budget timing and subsidy risk material.

| Metric | Value |

|---|---|

| SMEs | ~3.7M |

| Public procurement | ~12% GDP |

| Public debt | ~262% GDP (IMF 2024) |

| Data‑center capex | $180B (2023) → $220B+ (2025 est.) |

| Reshoring support | ¥2.2T (2023–24) |

What is included in the product

Explores how macro-environmental factors uniquely impact Fuyo General Lease across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses.

A concise, visually segmented PESTLE summary for Fuyo General Lease that frees teams from deep-dive prep by highlighting key political, economic, social, technological, legal and environmental risks at a glance. Easily shareable and editable for presentations, regional notes, or risk workshops to streamline strategic alignment and decision-making.

Economic factors

BOJ rate normalization and funding costs

BOJ rate normalization has lifted funding costs for lessors as 10-year JGB yields moved to about 0.6% in 2024, tightening margins; pricing discipline and active duration hedging are essential to protect spreads. Variable-rate pass-through and shorter-tenor leases help mitigate margin compression, but intense competition in commoditized segments may cap repricing power and slow recovery of yields.

Yen volatility and cross-border asset values

Yen swings—USD/JPY averaged about 150 in 2024 after trading between roughly 140–160 since 2022—drive residual values for aircraft, ships and imported equipment, making asset valuations cyclical. Hedging and currency‑matched financing are widely used to stabilize returns and preserve margins. Clients’ FX exposures materially affect credit risk and demand timing, while a weak yen tends to lift export-sector capex yet raises import costs and maintenance expenses.

Capex cycle across manufacturing and services

Moderate inflation (Japan core CPI ~3% in 2024) and wage gains (shunto raises around 3–4% in 2024) support steady corporate capex, sustaining leasing demand. Automation, logistics and healthcare equipment — sectors where Fuyo has exposure — underpinned resilient volumes, with global robotics investment up ~10% in 2024. Cyclical slowdowns compress originations and raise credit risk, requiring agile asset allocation and remarketing.

Real estate market bifurcation

Prime logistics and hyperscale data centers remained robust into H1 2025, with prime logistics cap rates in Japan compressing to about 3.0–3.5% while some Tokyo office submarkets show softness with vacancy near 7% and rising obsolescence risk. Lease underwriting must build in higher vacancy and refurbishment capex; recent interest-rate volatility lifted cap-rate sensitivity and tightened debt-service coverage ratios. Active asset management and sale-leaseback deals are being used to unlock liquidity and derisk portfolios.

- Prime logistics cap rates ~3.0–3.5% (H1 2025)

- Tokyo office vacancy ~7% (H1 2025)

- Sale-leaseback = liquidity + off-balance risk transfer

Credit cycle and SME health

METI reports SMEs represent 99.7% of Japanese firms and employ about 70% of the workforce; tightening financial conditions since 2022 have elevated funding costs and stressed vulnerable SMEs, raising delinquency risks.

Enhanced credit analytics, tighter collateral monitoring and faster workout processes are essential; government credit guarantee schemes provide partial loss absorption, so pricing must reflect higher PD/LGD and extended recovery timelines.

- SME footprint: 99.7% firms / ~70% employment

- Action: tighten PD/LGD modeling

- Mitigation: use guarantee coverage in loss estimates

- Ops: increase collateral monitoring & recovery speed

Japan policy, GX and reshoring drive low‑carbon capex amid subsidy and budget timing risk

BOJ rate normalization (10y JGB ~0.6% in 2024) raised funding costs, pressuring spreads and forcing tighter pricing and duration hedging. Yen volatility (USD/JPY ~150 avg in 2024) and moderate inflation (core CPI ~3% in 2024) make asset values and capex cyclical; sectoral demand (logistics, data centers) remains strongest. SME stress (99.7% firms; ~70% workforce) raises PD/LGD, so tighter credit and guarantee-aware pricing are required.

| Metric | Value/Date |

|---|---|

| 10y JGB yield | ~0.6% (2024) |

| USD/JPY | ~150 avg (2024) |

| Japan core CPI | ~3% (2024) |

| Shunto wage | 3–4% (2024) |

| Logistics cap rate | 3.0–3.5% (H1 2025) |

| Tokyo office vacancy | ~7% (H1 2025) |

| SME share | 99.7% firms / ~70% employment |

Full Version Awaits

Fuyo General Lease PESTLE Analysis

This Fuyo General Lease PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It covers political, economic, social, technological, legal, and environmental factors specific to Fuyo General Lease with no placeholders or teasers. After checkout you’ll instantly download this same finished file.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are reshaping Fuyo General Lease’s outlook in our concise PESTLE snapshot—ideal for investors and strategists seeking a competitive edge. This professionally researched analysis highlights risks and opportunities you can act on immediately. Purchase the full PESTLE to access the complete, editable report and make informed decisions today.

Political factors

Japan’s industrial and SME support policies

Pro-growth programs, subsidies and tax incentives in Japan—where SMEs number about 3.7 million and represent roughly 99.7% of firms and 70% of employment—encourage capital investment that underpins leasing demand. Fuyo can package leases with government-backed guarantees and subsidy schemes to reduce client cost of capital. Policy continuity favors manufacturing, healthcare and logistics, though shifts in priority sectors can re-weight origination pipelines.

Energy transition and green procurement directives

Japan’s GX policies target carbon neutrality by 2050 with a 46% GHG reduction by 2030, and stronger public-sector green procurement is steering buyers toward low‑carbon assets. This shifts demand to renewable, efficiency and EV-related leases, and public procurement—about 12% of GDP (OECD)—amplifies scale. Fuyo can leverage subsidies and preferential financing to structure competitive solutions, while tightening policy raises risk and potential penalties for high‑emission legacy asset classes.

Geopolitical tensions and supply chain security

US export controls on advanced semiconductors and AI chips to China since 2022 and regional security frictions raise equipment scarcity and price pressure for lessors. Japan has rolled out roughly ¥2.2 trillion in reshoring/supply-chain resilience support in 2023–24, likely boosting domestic capex. Historical disruptions produced delivery delays of months, driving cost spikes that affect lease terms and residual assumptions. Diversified sourcing and cross-border risk controls are therefore critical.

Public infrastructure and digital nation initiatives

Government pushes into data centers, 5G and public infrastructure increase leasing demand for equipment and property, aligning Fuyo General Lease with municipal/quasi-public projects; global data‑center investment topped about $180B in 2023 and is forecast to exceed $220B by 2025 (IDC), favoring long‑tenor, lower‑risk assets but dependent on budget cycles and procurement rules.

Monetary-fiscal coordination and political stability

Japan’s stable governance limits abrupt regulatory shocks, supporting Fuyo’s multi-year planning; public debt stood at about 262% of GDP (IMF 2024), so fiscal consolidation pressures could prompt changes to lease tax treatment and incentives. Policy continuity with cautious monetary normalization affects funding spreads and refinancing costs; Fuyo should scenario-plan for shifts in public borrowing and subsidies.

- IMF 2024: public debt ~262% GDP

- Risk: tax changes to lease accounting/incentives

- Impact: funding/refinancing cost sensitivity

- Action: scenario-plan for subsidy and borrowing shifts

Japan policy, GX and reshoring drive low‑carbon capex amid subsidy and budget timing risk

Stable Japanese policy and pro-growth subsidies (SMEs ~3.7M; 70% employment) support leasing demand, while GX targets (carbon neutrality by 2050; −46% GHG by 2030) shift demand to low‑carbon assets. US export controls and ¥2.2T reshoring support (2023–24) raise equipment scarcity and domestic capex. Public procurement (~12% GDP) and high public debt (~262% GDP, IMF 2024) make budget timing and subsidy risk material.

| Metric | Value |

|---|---|

| SMEs | ~3.7M |

| Public procurement | ~12% GDP |

| Public debt | ~262% GDP (IMF 2024) |

| Data‑center capex | $180B (2023) → $220B+ (2025 est.) |

| Reshoring support | ¥2.2T (2023–24) |

What is included in the product

Explores how macro-environmental factors uniquely impact Fuyo General Lease across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses.

A concise, visually segmented PESTLE summary for Fuyo General Lease that frees teams from deep-dive prep by highlighting key political, economic, social, technological, legal and environmental risks at a glance. Easily shareable and editable for presentations, regional notes, or risk workshops to streamline strategic alignment and decision-making.

Economic factors

BOJ rate normalization and funding costs

BOJ rate normalization has lifted funding costs for lessors as 10-year JGB yields moved to about 0.6% in 2024, tightening margins; pricing discipline and active duration hedging are essential to protect spreads. Variable-rate pass-through and shorter-tenor leases help mitigate margin compression, but intense competition in commoditized segments may cap repricing power and slow recovery of yields.

Yen volatility and cross-border asset values

Yen swings—USD/JPY averaged about 150 in 2024 after trading between roughly 140–160 since 2022—drive residual values for aircraft, ships and imported equipment, making asset valuations cyclical. Hedging and currency‑matched financing are widely used to stabilize returns and preserve margins. Clients’ FX exposures materially affect credit risk and demand timing, while a weak yen tends to lift export-sector capex yet raises import costs and maintenance expenses.

Capex cycle across manufacturing and services

Moderate inflation (Japan core CPI ~3% in 2024) and wage gains (shunto raises around 3–4% in 2024) support steady corporate capex, sustaining leasing demand. Automation, logistics and healthcare equipment — sectors where Fuyo has exposure — underpinned resilient volumes, with global robotics investment up ~10% in 2024. Cyclical slowdowns compress originations and raise credit risk, requiring agile asset allocation and remarketing.

Real estate market bifurcation

Prime logistics and hyperscale data centers remained robust into H1 2025, with prime logistics cap rates in Japan compressing to about 3.0–3.5% while some Tokyo office submarkets show softness with vacancy near 7% and rising obsolescence risk. Lease underwriting must build in higher vacancy and refurbishment capex; recent interest-rate volatility lifted cap-rate sensitivity and tightened debt-service coverage ratios. Active asset management and sale-leaseback deals are being used to unlock liquidity and derisk portfolios.

- Prime logistics cap rates ~3.0–3.5% (H1 2025)

- Tokyo office vacancy ~7% (H1 2025)

- Sale-leaseback = liquidity + off-balance risk transfer

Credit cycle and SME health

METI reports SMEs represent 99.7% of Japanese firms and employ about 70% of the workforce; tightening financial conditions since 2022 have elevated funding costs and stressed vulnerable SMEs, raising delinquency risks.

Enhanced credit analytics, tighter collateral monitoring and faster workout processes are essential; government credit guarantee schemes provide partial loss absorption, so pricing must reflect higher PD/LGD and extended recovery timelines.

- SME footprint: 99.7% firms / ~70% employment

- Action: tighten PD/LGD modeling

- Mitigation: use guarantee coverage in loss estimates

- Ops: increase collateral monitoring & recovery speed

Japan policy, GX and reshoring drive low‑carbon capex amid subsidy and budget timing risk

BOJ rate normalization (10y JGB ~0.6% in 2024) raised funding costs, pressuring spreads and forcing tighter pricing and duration hedging. Yen volatility (USD/JPY ~150 avg in 2024) and moderate inflation (core CPI ~3% in 2024) make asset values and capex cyclical; sectoral demand (logistics, data centers) remains strongest. SME stress (99.7% firms; ~70% workforce) raises PD/LGD, so tighter credit and guarantee-aware pricing are required.

| Metric | Value/Date |

|---|---|

| 10y JGB yield | ~0.6% (2024) |

| USD/JPY | ~150 avg (2024) |

| Japan core CPI | ~3% (2024) |

| Shunto wage | 3–4% (2024) |

| Logistics cap rate | 3.0–3.5% (H1 2025) |

| Tokyo office vacancy | ~7% (H1 2025) |

| SME share | 99.7% firms / ~70% employment |

Full Version Awaits

Fuyo General Lease PESTLE Analysis

This Fuyo General Lease PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It covers political, economic, social, technological, legal, and environmental factors specific to Fuyo General Lease with no placeholders or teasers. After checkout you’ll instantly download this same finished file.