First Interstate Bank Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

First Interstate Bank faces moderate competitive intensity: a strong regional brand and customer loyalty tempered by rising fintech entrants and margin pressure. Supplier and buyer power are balanced—depositors influence pricing while interbank funding and technology partners shape costs. Regulatory and substitute risks remain material. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis for a detailed strategic breakdown.

Suppliers Bargaining Power

Concentration of core tech vendors

Core banking platforms, digital suites and payment rails are concentrated among a few vendors—Fiserv, FIS and Jack Henry together control roughly 70% of US bank core processing by assets—creating high switching costs and pricing power. Dependency on these providers shapes roadmap, uptime and cyber posture, with 2023–24 outages highlighting systemic risk. Negotiating leverage rises with scale, while banks under $10B (over 90% of institutions by count) have limited power; ongoing vendor consolidation further tightens contract terms and integration timelines.

Funding sources and deposit mix

Depositors supply the funding raw material while wholesale markets and brokered CDs backstop liquidity; First Interstate leans on low-cost core deposits to limit supplier power. In tight 2024 liquidity cycles brokered-CD and wholesale suppliers pushed rates up, compressing NIMs as short-term yields (3-month T-bills ~5.3%) and money-market yields (~4.5%) rose. Stable community deposits cut supplier leverage; surge pricing on CDs and competition from money funds and T-bills raise required yields and supplier power.

Skilled labor and compliance talent

Credit underwriting, risk, cybersecurity and compliance talent are scarce and costly, with the ISC2 2024 estimate of a global cybersecurity workforce gap around 3.4 million, pushing wages up and giving employees supplier-like leverage. Wage inflation and 2023–24 banking turnover raised replacement costs as talent migrates to larger banks and fintechs. Remote work expands the talent pool but intensifies competition and hiring costs for First Interstate Bank.

Card networks and payment ecosystems

Visa and Mastercard (roughly 80%+ combined network share) and ACH operators (NACHA: >30 billion annual ACH transactions) set fees, interchange frameworks and network rules with limited bank-level negotiation, directly influencing First Interstate Bank’s noninterest income and card economics.

- High supplier power

- Interchange drives NII exposure

- Few alternatives

- Volume rebates mitigate for larger issuers

- Community bank scale limits leverage

Regulatory capital and supervision

Regulators function as quasi-suppliers by allocating licensure and balance-sheet capacity through capital rules (minimum CET1 4.5% plus 2.5% conservation buffer = 7.0% under US rules in 2024). Heightened standards raise compliance costs, limit product flexibility, reshape cost structures and slow time-to-market; examination findings can mandate spending on specific vendors or processes.

Supplier dominance, funding spikes and talent gaps squeeze regional bank margins

Suppliers exert high power: core processors (Fiserv, FIS, Jack Henry ~70% by assets) and card networks (~80%+ share) set prices and terms, raising costs for First Interstate. Deposit and wholesale funding spikes (3M T-bill ~5.3% in 2024) increase rate pressure. Talent shortfalls (ISC2 gap ~3.4M) and regulatory capital (CET1 7.0% 2024) add supplier-like constraints.

| Supplier | Metric | 2024 Value |

|---|---|---|

| Core processors | Market share | ~70% |

| Card networks | Combined share | 80%+ |

| Funding cost | 3M T-bill | ~5.3% |

| Cyber talent | Workforce gap | ~3.4M |

| Regulatory | CET1 floor | 7.0% |

What is included in the product

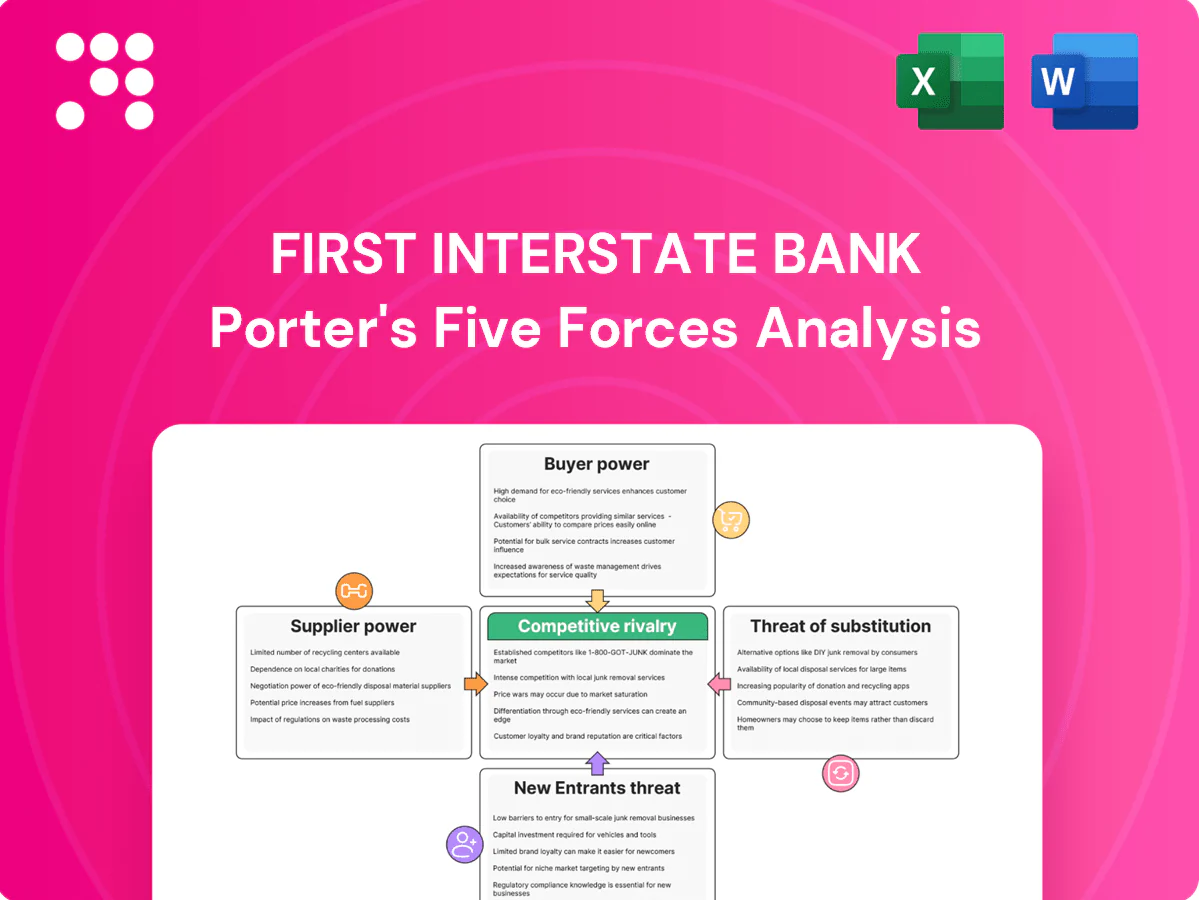

Concise Porter's Five Forces analysis of First Interstate Bank, assessing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and emerging disruptive risks to its regional banking position.

A concise one-sheet Porter's Five Forces for First Interstate Bank that visualizes competitive pressure with an interactive spider chart and customizable scores—ideal for quick boardroom decisions, cleanly formatted for pitch decks, integrates into Excel dashboards, and requires no macros so non-finance users can update scenarios instantly.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive retail and SME depositors can move funds quickly in the 2024 high-rate environment (federal funds ~5.25–5.50%), and digital account opening plus comparison tools have lowered switching frictions. To retain balances, banks must raise deposit rates or layer perks, compressing net interest margin. Relationship pricing helps, but cannot fully eliminate customer leverage or stop rate-driven outflows.

Commercial borrowers’ negotiation power

Middle-market and CRE clients shop terms across local banks, credit unions and non-banks, with non-bank share of CRE originations roughly 25% in recent years. They negotiate aggressively on rate, covenants, fees and speed, using pipeline visibility to demand concessions. First Interstate can offset pressure by bundling treasury and deposit products to deepen relationships.

Wealth and affluent clients

High-balance clients at First Interstate exert strong pricing power over advisory, mortgage and lending terms, pushing for lower advisory fees and preferred loan pricing; platform breadth and advisor reputation are key retention levers, while fee compression and growth of passive ETFs provide low-cost alternatives; personalized, concierge wealth services can offset churn but demand higher headcount and tech investment to scale.

Digital-first expectations

By 2024, over 80% of U.S. customers use mobile banking, and demand for instant payments and 24/7 support makes service gaps a primary driver of churn; app store ratings and social proof (regional banks average ~4.4 stars) amplify customer voice, lowering switching friction and increasing bargaining power, so continuous UX upgrades and rapid feature delivery are essential to retain clients.

- Mobile adoption: >80% (2024)

- Instant payments & 24/7 support expected

- App ratings ≈4.4 amplify voice

- Low switching friction → higher churn risk

- Continuous UX upgrades reduce bargaining power

Community relationships vs. choice abundance

Long-term community ties at First Interstate lower buyer power through entrenched relationships and trust, but abundant nearby banks and online options increase switching pressure; over 80% of US customers used online banking in 2024, restoring comparison leverage. Niche focus on agriculture and small business reduces price elasticity for those segments, while visible local presence partially neutralizes pure price shopping.

- Long-term ties: lower buyer power

- Digital access: >80% online banking (2024) raises leverage

- Niche (ag, SMB): reduces elasticity

- Trust/local branches: offsets some price competition

Deposit churn rises as fed funds 5.25–5.50%; mobile >80%

Customers hold elevated bargaining power in 2024: rate-sensitive depositors shift quickly in a 5.25–5.50% fed funds environment, digital tools lower switching costs, non-bank CRE originations ≈25%, and mobile adoption >80% increases churn risk; First Interstate counters via relationship pricing, product bundling and concierge wealth services.

| Metric | 2024 Value |

|---|---|

| Fed funds rate | 5.25–5.50% |

| Mobile adoption | >80% |

| Non-bank CRE share | ≈25% |

| Regional bank app rating | ~4.4 |

Preview Before You Purchase

First Interstate Bank Porter's Five Forces Analysis

This preview shows the exact First Interstate Bank Porter’s Five Forces analysis you’ll receive—no placeholders, no mockups. It’s the final, professionally formatted document ready for immediate download upon purchase. Use it as-is for decision-making or reporting.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

First Interstate Bank faces moderate competitive intensity: a strong regional brand and customer loyalty tempered by rising fintech entrants and margin pressure. Supplier and buyer power are balanced—depositors influence pricing while interbank funding and technology partners shape costs. Regulatory and substitute risks remain material. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis for a detailed strategic breakdown.

Suppliers Bargaining Power

Concentration of core tech vendors

Core banking platforms, digital suites and payment rails are concentrated among a few vendors—Fiserv, FIS and Jack Henry together control roughly 70% of US bank core processing by assets—creating high switching costs and pricing power. Dependency on these providers shapes roadmap, uptime and cyber posture, with 2023–24 outages highlighting systemic risk. Negotiating leverage rises with scale, while banks under $10B (over 90% of institutions by count) have limited power; ongoing vendor consolidation further tightens contract terms and integration timelines.

Funding sources and deposit mix

Depositors supply the funding raw material while wholesale markets and brokered CDs backstop liquidity; First Interstate leans on low-cost core deposits to limit supplier power. In tight 2024 liquidity cycles brokered-CD and wholesale suppliers pushed rates up, compressing NIMs as short-term yields (3-month T-bills ~5.3%) and money-market yields (~4.5%) rose. Stable community deposits cut supplier leverage; surge pricing on CDs and competition from money funds and T-bills raise required yields and supplier power.

Skilled labor and compliance talent

Credit underwriting, risk, cybersecurity and compliance talent are scarce and costly, with the ISC2 2024 estimate of a global cybersecurity workforce gap around 3.4 million, pushing wages up and giving employees supplier-like leverage. Wage inflation and 2023–24 banking turnover raised replacement costs as talent migrates to larger banks and fintechs. Remote work expands the talent pool but intensifies competition and hiring costs for First Interstate Bank.

Card networks and payment ecosystems

Visa and Mastercard (roughly 80%+ combined network share) and ACH operators (NACHA: >30 billion annual ACH transactions) set fees, interchange frameworks and network rules with limited bank-level negotiation, directly influencing First Interstate Bank’s noninterest income and card economics.

- High supplier power

- Interchange drives NII exposure

- Few alternatives

- Volume rebates mitigate for larger issuers

- Community bank scale limits leverage

Regulatory capital and supervision

Regulators function as quasi-suppliers by allocating licensure and balance-sheet capacity through capital rules (minimum CET1 4.5% plus 2.5% conservation buffer = 7.0% under US rules in 2024). Heightened standards raise compliance costs, limit product flexibility, reshape cost structures and slow time-to-market; examination findings can mandate spending on specific vendors or processes.

Supplier dominance, funding spikes and talent gaps squeeze regional bank margins

Suppliers exert high power: core processors (Fiserv, FIS, Jack Henry ~70% by assets) and card networks (~80%+ share) set prices and terms, raising costs for First Interstate. Deposit and wholesale funding spikes (3M T-bill ~5.3% in 2024) increase rate pressure. Talent shortfalls (ISC2 gap ~3.4M) and regulatory capital (CET1 7.0% 2024) add supplier-like constraints.

| Supplier | Metric | 2024 Value |

|---|---|---|

| Core processors | Market share | ~70% |

| Card networks | Combined share | 80%+ |

| Funding cost | 3M T-bill | ~5.3% |

| Cyber talent | Workforce gap | ~3.4M |

| Regulatory | CET1 floor | 7.0% |

What is included in the product

Concise Porter's Five Forces analysis of First Interstate Bank, assessing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and emerging disruptive risks to its regional banking position.

A concise one-sheet Porter's Five Forces for First Interstate Bank that visualizes competitive pressure with an interactive spider chart and customizable scores—ideal for quick boardroom decisions, cleanly formatted for pitch decks, integrates into Excel dashboards, and requires no macros so non-finance users can update scenarios instantly.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive retail and SME depositors can move funds quickly in the 2024 high-rate environment (federal funds ~5.25–5.50%), and digital account opening plus comparison tools have lowered switching frictions. To retain balances, banks must raise deposit rates or layer perks, compressing net interest margin. Relationship pricing helps, but cannot fully eliminate customer leverage or stop rate-driven outflows.

Commercial borrowers’ negotiation power

Middle-market and CRE clients shop terms across local banks, credit unions and non-banks, with non-bank share of CRE originations roughly 25% in recent years. They negotiate aggressively on rate, covenants, fees and speed, using pipeline visibility to demand concessions. First Interstate can offset pressure by bundling treasury and deposit products to deepen relationships.

Wealth and affluent clients

High-balance clients at First Interstate exert strong pricing power over advisory, mortgage and lending terms, pushing for lower advisory fees and preferred loan pricing; platform breadth and advisor reputation are key retention levers, while fee compression and growth of passive ETFs provide low-cost alternatives; personalized, concierge wealth services can offset churn but demand higher headcount and tech investment to scale.

Digital-first expectations

By 2024, over 80% of U.S. customers use mobile banking, and demand for instant payments and 24/7 support makes service gaps a primary driver of churn; app store ratings and social proof (regional banks average ~4.4 stars) amplify customer voice, lowering switching friction and increasing bargaining power, so continuous UX upgrades and rapid feature delivery are essential to retain clients.

- Mobile adoption: >80% (2024)

- Instant payments & 24/7 support expected

- App ratings ≈4.4 amplify voice

- Low switching friction → higher churn risk

- Continuous UX upgrades reduce bargaining power

Community relationships vs. choice abundance

Long-term community ties at First Interstate lower buyer power through entrenched relationships and trust, but abundant nearby banks and online options increase switching pressure; over 80% of US customers used online banking in 2024, restoring comparison leverage. Niche focus on agriculture and small business reduces price elasticity for those segments, while visible local presence partially neutralizes pure price shopping.

- Long-term ties: lower buyer power

- Digital access: >80% online banking (2024) raises leverage

- Niche (ag, SMB): reduces elasticity

- Trust/local branches: offsets some price competition

Deposit churn rises as fed funds 5.25–5.50%; mobile >80%

Customers hold elevated bargaining power in 2024: rate-sensitive depositors shift quickly in a 5.25–5.50% fed funds environment, digital tools lower switching costs, non-bank CRE originations ≈25%, and mobile adoption >80% increases churn risk; First Interstate counters via relationship pricing, product bundling and concierge wealth services.

| Metric | 2024 Value |

|---|---|

| Fed funds rate | 5.25–5.50% |

| Mobile adoption | >80% |

| Non-bank CRE share | ≈25% |

| Regional bank app rating | ~4.4 |

Preview Before You Purchase

First Interstate Bank Porter's Five Forces Analysis

This preview shows the exact First Interstate Bank Porter’s Five Forces analysis you’ll receive—no placeholders, no mockups. It’s the final, professionally formatted document ready for immediate download upon purchase. Use it as-is for decision-making or reporting.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

First Interstate Bank faces moderate competitive intensity: a strong regional brand and customer loyalty tempered by rising fintech entrants and margin pressure. Supplier and buyer power are balanced—depositors influence pricing while interbank funding and technology partners shape costs. Regulatory and substitute risks remain material. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis for a detailed strategic breakdown.

Suppliers Bargaining Power

Concentration of core tech vendors

Core banking platforms, digital suites and payment rails are concentrated among a few vendors—Fiserv, FIS and Jack Henry together control roughly 70% of US bank core processing by assets—creating high switching costs and pricing power. Dependency on these providers shapes roadmap, uptime and cyber posture, with 2023–24 outages highlighting systemic risk. Negotiating leverage rises with scale, while banks under $10B (over 90% of institutions by count) have limited power; ongoing vendor consolidation further tightens contract terms and integration timelines.

Funding sources and deposit mix

Depositors supply the funding raw material while wholesale markets and brokered CDs backstop liquidity; First Interstate leans on low-cost core deposits to limit supplier power. In tight 2024 liquidity cycles brokered-CD and wholesale suppliers pushed rates up, compressing NIMs as short-term yields (3-month T-bills ~5.3%) and money-market yields (~4.5%) rose. Stable community deposits cut supplier leverage; surge pricing on CDs and competition from money funds and T-bills raise required yields and supplier power.

Skilled labor and compliance talent

Credit underwriting, risk, cybersecurity and compliance talent are scarce and costly, with the ISC2 2024 estimate of a global cybersecurity workforce gap around 3.4 million, pushing wages up and giving employees supplier-like leverage. Wage inflation and 2023–24 banking turnover raised replacement costs as talent migrates to larger banks and fintechs. Remote work expands the talent pool but intensifies competition and hiring costs for First Interstate Bank.

Card networks and payment ecosystems

Visa and Mastercard (roughly 80%+ combined network share) and ACH operators (NACHA: >30 billion annual ACH transactions) set fees, interchange frameworks and network rules with limited bank-level negotiation, directly influencing First Interstate Bank’s noninterest income and card economics.

- High supplier power

- Interchange drives NII exposure

- Few alternatives

- Volume rebates mitigate for larger issuers

- Community bank scale limits leverage

Regulatory capital and supervision

Regulators function as quasi-suppliers by allocating licensure and balance-sheet capacity through capital rules (minimum CET1 4.5% plus 2.5% conservation buffer = 7.0% under US rules in 2024). Heightened standards raise compliance costs, limit product flexibility, reshape cost structures and slow time-to-market; examination findings can mandate spending on specific vendors or processes.

Supplier dominance, funding spikes and talent gaps squeeze regional bank margins

Suppliers exert high power: core processors (Fiserv, FIS, Jack Henry ~70% by assets) and card networks (~80%+ share) set prices and terms, raising costs for First Interstate. Deposit and wholesale funding spikes (3M T-bill ~5.3% in 2024) increase rate pressure. Talent shortfalls (ISC2 gap ~3.4M) and regulatory capital (CET1 7.0% 2024) add supplier-like constraints.

| Supplier | Metric | 2024 Value |

|---|---|---|

| Core processors | Market share | ~70% |

| Card networks | Combined share | 80%+ |

| Funding cost | 3M T-bill | ~5.3% |

| Cyber talent | Workforce gap | ~3.4M |

| Regulatory | CET1 floor | 7.0% |

What is included in the product

Concise Porter's Five Forces analysis of First Interstate Bank, assessing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and emerging disruptive risks to its regional banking position.

A concise one-sheet Porter's Five Forces for First Interstate Bank that visualizes competitive pressure with an interactive spider chart and customizable scores—ideal for quick boardroom decisions, cleanly formatted for pitch decks, integrates into Excel dashboards, and requires no macros so non-finance users can update scenarios instantly.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive retail and SME depositors can move funds quickly in the 2024 high-rate environment (federal funds ~5.25–5.50%), and digital account opening plus comparison tools have lowered switching frictions. To retain balances, banks must raise deposit rates or layer perks, compressing net interest margin. Relationship pricing helps, but cannot fully eliminate customer leverage or stop rate-driven outflows.

Commercial borrowers’ negotiation power

Middle-market and CRE clients shop terms across local banks, credit unions and non-banks, with non-bank share of CRE originations roughly 25% in recent years. They negotiate aggressively on rate, covenants, fees and speed, using pipeline visibility to demand concessions. First Interstate can offset pressure by bundling treasury and deposit products to deepen relationships.

Wealth and affluent clients

High-balance clients at First Interstate exert strong pricing power over advisory, mortgage and lending terms, pushing for lower advisory fees and preferred loan pricing; platform breadth and advisor reputation are key retention levers, while fee compression and growth of passive ETFs provide low-cost alternatives; personalized, concierge wealth services can offset churn but demand higher headcount and tech investment to scale.

Digital-first expectations

By 2024, over 80% of U.S. customers use mobile banking, and demand for instant payments and 24/7 support makes service gaps a primary driver of churn; app store ratings and social proof (regional banks average ~4.4 stars) amplify customer voice, lowering switching friction and increasing bargaining power, so continuous UX upgrades and rapid feature delivery are essential to retain clients.

- Mobile adoption: >80% (2024)

- Instant payments & 24/7 support expected

- App ratings ≈4.4 amplify voice

- Low switching friction → higher churn risk

- Continuous UX upgrades reduce bargaining power

Community relationships vs. choice abundance

Long-term community ties at First Interstate lower buyer power through entrenched relationships and trust, but abundant nearby banks and online options increase switching pressure; over 80% of US customers used online banking in 2024, restoring comparison leverage. Niche focus on agriculture and small business reduces price elasticity for those segments, while visible local presence partially neutralizes pure price shopping.

- Long-term ties: lower buyer power

- Digital access: >80% online banking (2024) raises leverage

- Niche (ag, SMB): reduces elasticity

- Trust/local branches: offsets some price competition

Deposit churn rises as fed funds 5.25–5.50%; mobile >80%

Customers hold elevated bargaining power in 2024: rate-sensitive depositors shift quickly in a 5.25–5.50% fed funds environment, digital tools lower switching costs, non-bank CRE originations ≈25%, and mobile adoption >80% increases churn risk; First Interstate counters via relationship pricing, product bundling and concierge wealth services.

| Metric | 2024 Value |

|---|---|

| Fed funds rate | 5.25–5.50% |

| Mobile adoption | >80% |

| Non-bank CRE share | ≈25% |

| Regional bank app rating | ~4.4 |

Preview Before You Purchase

First Interstate Bank Porter's Five Forces Analysis

This preview shows the exact First Interstate Bank Porter’s Five Forces analysis you’ll receive—no placeholders, no mockups. It’s the final, professionally formatted document ready for immediate download upon purchase. Use it as-is for decision-making or reporting.