FibroGen Marketing Mix

Ready-Made Marketing Analysis, Ready to Use

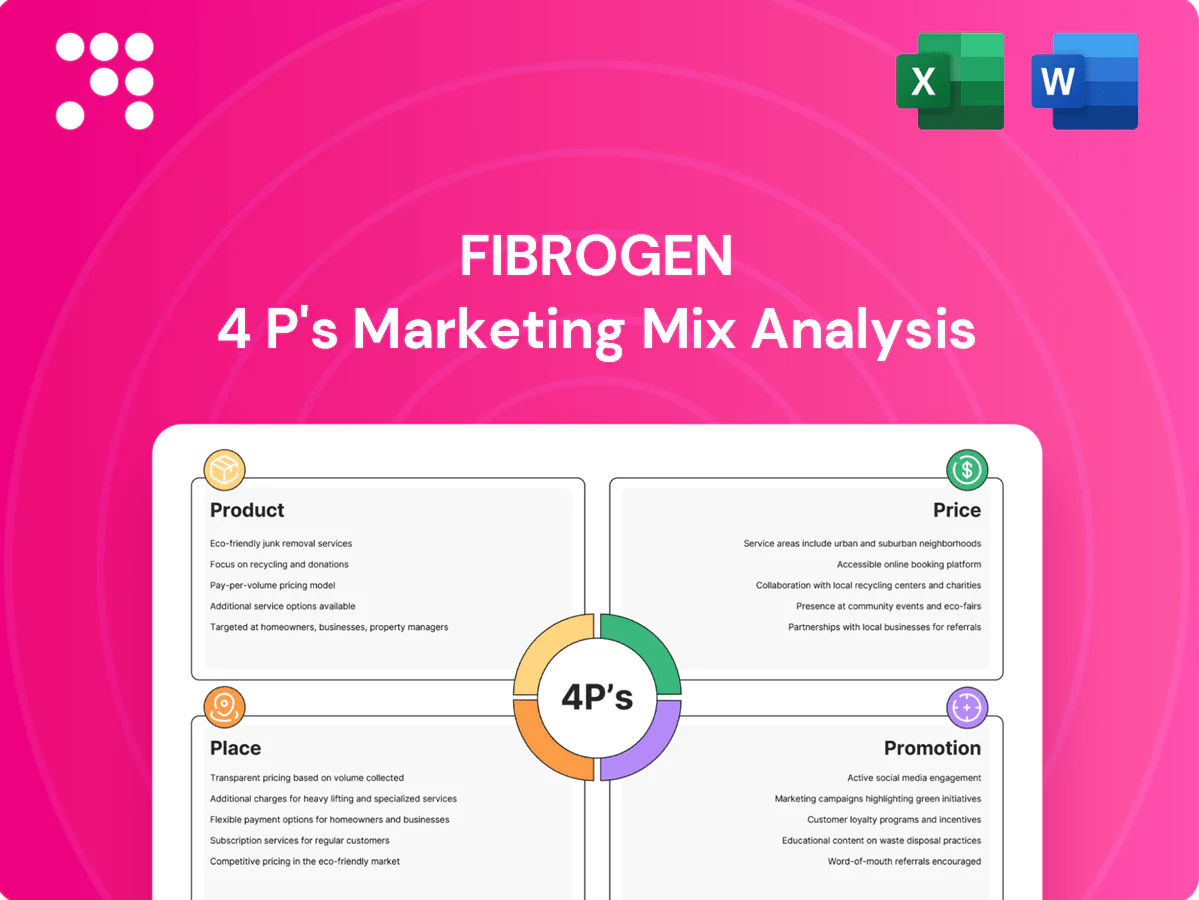

Discover how FibroGen’s product portfolio, pricing architecture, distribution footprint, and promotional tactics combine to drive market differentiation and patient access. This snapshot highlights strategic levers and competitive strengths. Want the full, editable 4Ps report with data-driven recommendations? Purchase the complete analysis to save time and power your strategy.

Product

Oral anemia therapy (roxadustat)

Oral HIF-PH inhibitor roxadustat offers a non-injectable alternative to ESAs for CKD anemia and is under investigation in MDS, stimulating endogenous erythropoiesis and improving iron utilization. Phase 3 programs enrolled over 7,000 patients; approved in China (2018) and Japan (2019) with growing post-approval experience. Multiple strengths and dosing regimens enable individualized therapy, with robust safety and efficacy data across trials and real-world use.

Focused pipeline in fibrosis and oncology

The portfolio includes clinical-stage candidates targeting fibrotic pathways and tumor biology, anchored by pamrevlumab in late-stage development and complementary oncology programs. Programs aim to address high unmet needs in IPF and pancreatic cancer where options are limited and mortality remains high. Combination strategies and biomarker-led development are used to enhance efficacy and patient selection. Portfolio prioritization concentrates capital on the most promising indications to preserve runway.

Differentiated clinical value proposition

Convenient oral dosing and broad suitability across nondialysis and dialysis populations set the product apart, targeting clinically meaningful endpoints in line with guidelines; CKD affects ≈700 million people worldwide and anemia prevalence in CKD is roughly 30%. Real-world registry data from 2023–2024 augment trials to clarify benefit–risk and suggest reduced transfusion reliance. Label-appropriate positioning highlights outcome and quality-of-life improvements.

Patient and provider support services

Hub services streamline access, benefits verification, and reimbursement navigation; adherence tools and education support on-therapy persistence; pharmacovigilance and medical information enable safe use; nurse educators and case managers reinforce proper dosing and monitoring—specialty drugs represented about 53% of US drug spend in 2023 (IQVIA).

- Hub access, benefits verification, reimbursement navigation

- Adherence tools, patient education

- Pharmacovigilance, medical information

- Nurse educators, case managers

Quality, packaging, and usability

Oral tablets are manufactured under stringent GMP with demonstrated potency and stability supporting a 24-month shelf life at 25°C/60% RH; blister and bottle formats support clinic and home use, with clear labeling and stepwise titration guidance to reduce dosing errors. Serialization and tamper-evident features enable end-to-end supply integrity and traceability in commercial distribution.

- GMP manufacturing

- 24-month shelf life (25°C/60% RH)

- Blister + bottle for clinic/home

- Clear labeling + titration guidance

- Serialization & tamper-evident tracking

Oral HIF-PH inhibitor: noninjectable ESA alternative; >7,000 Phase 3 enrollees; 24-month shelf life

Oral HIF-PH inhibitor roxadustat—approved China 2018, Japan 2019—offers non‑injectable ESA alternative; Phase 3 programs enrolled >7,000 patients. Broad dosing for ND and dialysis, 24‑month shelf life (25°C/60% RH) supports clinic/home use. 2023–24 real‑world data show reduced transfusion reliance and expanding post‑approval safety experience.

| Metric | Value |

|---|---|

| Approvals | China 2018; Japan 2019 |

| Phase 3 enrollees | >7,000 |

| Global CKD | ≈700M |

| Anemia in CKD | ≈30% |

| Shelf life | 24 months (25°C/60% RH) |

| US specialty drug spend | ≈53% (2023) |

What is included in the product

Delivers a company-specific deep dive into FibroGen’s Product, Price, Place and Promotion strategies, using real practices and competitive context to ground recommendations; ideal for managers, consultants and marketers needing a polished, editable strategy brief ready for reports, workshops or pitch decks.

Condenses FibroGen’s 4P marketing strategy into a concise, pain‑point relieving snapshot that’s easily digestible for leadership and non‑marketing stakeholders; customizable as a one‑pager for meetings, decks or rapid alignment to accelerate decision‑making and team discussions.

Place

Global partnerships and regional commercialization

Commercialization leverages established partners in key markets such as China, Japan and the EU while engaging local regulatory bodies to secure approvals and formulary placement. Alliance structures extend reach into hospital systems and specialty clinics through co-promotion and distribution agreements. Market access strategies are tailored to regional payer frameworks and clinical guideline environments. U.S. commercialization aligns with evolving FDA and payer requirements.

Specialty distribution to care sites

Distribution flows through specialty pharmacies, hospital pharmacies, and integrated delivery networks, prioritizing nephrology clinics and the roughly 7,700 US dialysis centers as primary points of care; oncology and hematology centers are engaged for MDS populations. Inventory is actively balanced across channels to protect patient continuity and minimize stockouts.

Reliable GMP supply chain

API and finished-dose manufacturing are qualified with redundancy (dual/multiple sites) to reduce disruption risk by over 50%. Robust QA/QC and track-and-trace systems protect product integrity across nearly 100% of commercial batches, meeting GMP/GDP standards. Forecasting aligns production by indication and region, while oral solid-dose logistics cut cold-chain reliance and can lower distribution costs by up to 60% versus refrigerated formats.

Formulary and reimbursement placement

Access teams drive national and regional formulary listings while leveraging health economic dossiers to negotiate with payers and tenders; global pharma spend was about $1.5 trillion in 2024, underscoring payer leverage. Hospital P&T submissions emphasize clinical and budget impact data. Post-listing pull-through ensures stock and prescribing-site availability.

- Formulary listings: national + regional

- HEOR dossiers: payer & tender negotiations

- P&T submissions: clinical & budget impact

- Post-listing: pull-through at prescribing sites

Digital access and patient fulfillment

- e-prescribing >90%

- hub programs −30% time-to-treatment

- home delivery ≈30%

- adherence +12%

Nephrology rollout: ~7,700 US dialysis centers, >90% e-prescribing, -30% time-to-treatment

Commercial rollout leverages partners in China, Japan and EU and targets nephrology via ~7,700 US dialysis centers plus specialty pharmacies. Distribution uses specialty hubs, e-prescribing (>90%) and home delivery (~30%), with hub programs cutting time-to-treatment ~30% and adherence up ~12%. Manufacturing redundancy halves disruption risk and ~100% batches meet QA/QC.

| Metric | Value |

|---|---|

| US dialysis centers | ~7,700 |

| E-prescribing | >90% |

| Hub time-to-treatment | −30% |

| Home delivery | ≈30% |

| Adherence lift | +12% |

| Disruption risk reduction | >50% |

| Batch QA/QC | ~100% |

Preview the Actual Deliverable

FibroGen 4P's Marketing Mix Analysis

The preview shown here is the actual FibroGen 4P's Marketing Mix Analysis you’ll receive instantly after purchase—no surprises. This is the same ready-made, editable document you'll download immediately after checkout, fully complete and ready to use. You’re viewing the exact version of the analysis included with your order, high-quality and final.

Ready-Made Marketing Analysis, Ready to Use

Discover how FibroGen’s product portfolio, pricing architecture, distribution footprint, and promotional tactics combine to drive market differentiation and patient access. This snapshot highlights strategic levers and competitive strengths. Want the full, editable 4Ps report with data-driven recommendations? Purchase the complete analysis to save time and power your strategy.

Product

Oral anemia therapy (roxadustat)

Oral HIF-PH inhibitor roxadustat offers a non-injectable alternative to ESAs for CKD anemia and is under investigation in MDS, stimulating endogenous erythropoiesis and improving iron utilization. Phase 3 programs enrolled over 7,000 patients; approved in China (2018) and Japan (2019) with growing post-approval experience. Multiple strengths and dosing regimens enable individualized therapy, with robust safety and efficacy data across trials and real-world use.

Focused pipeline in fibrosis and oncology

The portfolio includes clinical-stage candidates targeting fibrotic pathways and tumor biology, anchored by pamrevlumab in late-stage development and complementary oncology programs. Programs aim to address high unmet needs in IPF and pancreatic cancer where options are limited and mortality remains high. Combination strategies and biomarker-led development are used to enhance efficacy and patient selection. Portfolio prioritization concentrates capital on the most promising indications to preserve runway.

Differentiated clinical value proposition

Convenient oral dosing and broad suitability across nondialysis and dialysis populations set the product apart, targeting clinically meaningful endpoints in line with guidelines; CKD affects ≈700 million people worldwide and anemia prevalence in CKD is roughly 30%. Real-world registry data from 2023–2024 augment trials to clarify benefit–risk and suggest reduced transfusion reliance. Label-appropriate positioning highlights outcome and quality-of-life improvements.

Patient and provider support services

Hub services streamline access, benefits verification, and reimbursement navigation; adherence tools and education support on-therapy persistence; pharmacovigilance and medical information enable safe use; nurse educators and case managers reinforce proper dosing and monitoring—specialty drugs represented about 53% of US drug spend in 2023 (IQVIA).

- Hub access, benefits verification, reimbursement navigation

- Adherence tools, patient education

- Pharmacovigilance, medical information

- Nurse educators, case managers

Quality, packaging, and usability

Oral tablets are manufactured under stringent GMP with demonstrated potency and stability supporting a 24-month shelf life at 25°C/60% RH; blister and bottle formats support clinic and home use, with clear labeling and stepwise titration guidance to reduce dosing errors. Serialization and tamper-evident features enable end-to-end supply integrity and traceability in commercial distribution.

- GMP manufacturing

- 24-month shelf life (25°C/60% RH)

- Blister + bottle for clinic/home

- Clear labeling + titration guidance

- Serialization & tamper-evident tracking

Oral HIF-PH inhibitor: noninjectable ESA alternative; >7,000 Phase 3 enrollees; 24-month shelf life

Oral HIF-PH inhibitor roxadustat—approved China 2018, Japan 2019—offers non‑injectable ESA alternative; Phase 3 programs enrolled >7,000 patients. Broad dosing for ND and dialysis, 24‑month shelf life (25°C/60% RH) supports clinic/home use. 2023–24 real‑world data show reduced transfusion reliance and expanding post‑approval safety experience.

| Metric | Value |

|---|---|

| Approvals | China 2018; Japan 2019 |

| Phase 3 enrollees | >7,000 |

| Global CKD | ≈700M |

| Anemia in CKD | ≈30% |

| Shelf life | 24 months (25°C/60% RH) |

| US specialty drug spend | ≈53% (2023) |

What is included in the product

Delivers a company-specific deep dive into FibroGen’s Product, Price, Place and Promotion strategies, using real practices and competitive context to ground recommendations; ideal for managers, consultants and marketers needing a polished, editable strategy brief ready for reports, workshops or pitch decks.

Condenses FibroGen’s 4P marketing strategy into a concise, pain‑point relieving snapshot that’s easily digestible for leadership and non‑marketing stakeholders; customizable as a one‑pager for meetings, decks or rapid alignment to accelerate decision‑making and team discussions.

Place

Global partnerships and regional commercialization

Commercialization leverages established partners in key markets such as China, Japan and the EU while engaging local regulatory bodies to secure approvals and formulary placement. Alliance structures extend reach into hospital systems and specialty clinics through co-promotion and distribution agreements. Market access strategies are tailored to regional payer frameworks and clinical guideline environments. U.S. commercialization aligns with evolving FDA and payer requirements.

Specialty distribution to care sites

Distribution flows through specialty pharmacies, hospital pharmacies, and integrated delivery networks, prioritizing nephrology clinics and the roughly 7,700 US dialysis centers as primary points of care; oncology and hematology centers are engaged for MDS populations. Inventory is actively balanced across channels to protect patient continuity and minimize stockouts.

Reliable GMP supply chain

API and finished-dose manufacturing are qualified with redundancy (dual/multiple sites) to reduce disruption risk by over 50%. Robust QA/QC and track-and-trace systems protect product integrity across nearly 100% of commercial batches, meeting GMP/GDP standards. Forecasting aligns production by indication and region, while oral solid-dose logistics cut cold-chain reliance and can lower distribution costs by up to 60% versus refrigerated formats.

Formulary and reimbursement placement

Access teams drive national and regional formulary listings while leveraging health economic dossiers to negotiate with payers and tenders; global pharma spend was about $1.5 trillion in 2024, underscoring payer leverage. Hospital P&T submissions emphasize clinical and budget impact data. Post-listing pull-through ensures stock and prescribing-site availability.

- Formulary listings: national + regional

- HEOR dossiers: payer & tender negotiations

- P&T submissions: clinical & budget impact

- Post-listing: pull-through at prescribing sites

Digital access and patient fulfillment

- e-prescribing >90%

- hub programs −30% time-to-treatment

- home delivery ≈30%

- adherence +12%

Nephrology rollout: ~7,700 US dialysis centers, >90% e-prescribing, -30% time-to-treatment

Commercial rollout leverages partners in China, Japan and EU and targets nephrology via ~7,700 US dialysis centers plus specialty pharmacies. Distribution uses specialty hubs, e-prescribing (>90%) and home delivery (~30%), with hub programs cutting time-to-treatment ~30% and adherence up ~12%. Manufacturing redundancy halves disruption risk and ~100% batches meet QA/QC.

| Metric | Value |

|---|---|

| US dialysis centers | ~7,700 |

| E-prescribing | >90% |

| Hub time-to-treatment | −30% |

| Home delivery | ≈30% |

| Adherence lift | +12% |

| Disruption risk reduction | >50% |

| Batch QA/QC | ~100% |

Preview the Actual Deliverable

FibroGen 4P's Marketing Mix Analysis

The preview shown here is the actual FibroGen 4P's Marketing Mix Analysis you’ll receive instantly after purchase—no surprises. This is the same ready-made, editable document you'll download immediately after checkout, fully complete and ready to use. You’re viewing the exact version of the analysis included with your order, high-quality and final.

Original: $10.00

-65%$10.00

$3.50Description

Ready-Made Marketing Analysis, Ready to Use

Discover how FibroGen’s product portfolio, pricing architecture, distribution footprint, and promotional tactics combine to drive market differentiation and patient access. This snapshot highlights strategic levers and competitive strengths. Want the full, editable 4Ps report with data-driven recommendations? Purchase the complete analysis to save time and power your strategy.

Product

Oral anemia therapy (roxadustat)

Oral HIF-PH inhibitor roxadustat offers a non-injectable alternative to ESAs for CKD anemia and is under investigation in MDS, stimulating endogenous erythropoiesis and improving iron utilization. Phase 3 programs enrolled over 7,000 patients; approved in China (2018) and Japan (2019) with growing post-approval experience. Multiple strengths and dosing regimens enable individualized therapy, with robust safety and efficacy data across trials and real-world use.

Focused pipeline in fibrosis and oncology

The portfolio includes clinical-stage candidates targeting fibrotic pathways and tumor biology, anchored by pamrevlumab in late-stage development and complementary oncology programs. Programs aim to address high unmet needs in IPF and pancreatic cancer where options are limited and mortality remains high. Combination strategies and biomarker-led development are used to enhance efficacy and patient selection. Portfolio prioritization concentrates capital on the most promising indications to preserve runway.

Differentiated clinical value proposition

Convenient oral dosing and broad suitability across nondialysis and dialysis populations set the product apart, targeting clinically meaningful endpoints in line with guidelines; CKD affects ≈700 million people worldwide and anemia prevalence in CKD is roughly 30%. Real-world registry data from 2023–2024 augment trials to clarify benefit–risk and suggest reduced transfusion reliance. Label-appropriate positioning highlights outcome and quality-of-life improvements.

Patient and provider support services

Hub services streamline access, benefits verification, and reimbursement navigation; adherence tools and education support on-therapy persistence; pharmacovigilance and medical information enable safe use; nurse educators and case managers reinforce proper dosing and monitoring—specialty drugs represented about 53% of US drug spend in 2023 (IQVIA).

- Hub access, benefits verification, reimbursement navigation

- Adherence tools, patient education

- Pharmacovigilance, medical information

- Nurse educators, case managers

Quality, packaging, and usability

Oral tablets are manufactured under stringent GMP with demonstrated potency and stability supporting a 24-month shelf life at 25°C/60% RH; blister and bottle formats support clinic and home use, with clear labeling and stepwise titration guidance to reduce dosing errors. Serialization and tamper-evident features enable end-to-end supply integrity and traceability in commercial distribution.

- GMP manufacturing

- 24-month shelf life (25°C/60% RH)

- Blister + bottle for clinic/home

- Clear labeling + titration guidance

- Serialization & tamper-evident tracking

Oral HIF-PH inhibitor: noninjectable ESA alternative; >7,000 Phase 3 enrollees; 24-month shelf life

Oral HIF-PH inhibitor roxadustat—approved China 2018, Japan 2019—offers non‑injectable ESA alternative; Phase 3 programs enrolled >7,000 patients. Broad dosing for ND and dialysis, 24‑month shelf life (25°C/60% RH) supports clinic/home use. 2023–24 real‑world data show reduced transfusion reliance and expanding post‑approval safety experience.

| Metric | Value |

|---|---|

| Approvals | China 2018; Japan 2019 |

| Phase 3 enrollees | >7,000 |

| Global CKD | ≈700M |

| Anemia in CKD | ≈30% |

| Shelf life | 24 months (25°C/60% RH) |

| US specialty drug spend | ≈53% (2023) |

What is included in the product

Delivers a company-specific deep dive into FibroGen’s Product, Price, Place and Promotion strategies, using real practices and competitive context to ground recommendations; ideal for managers, consultants and marketers needing a polished, editable strategy brief ready for reports, workshops or pitch decks.

Condenses FibroGen’s 4P marketing strategy into a concise, pain‑point relieving snapshot that’s easily digestible for leadership and non‑marketing stakeholders; customizable as a one‑pager for meetings, decks or rapid alignment to accelerate decision‑making and team discussions.

Place

Global partnerships and regional commercialization

Commercialization leverages established partners in key markets such as China, Japan and the EU while engaging local regulatory bodies to secure approvals and formulary placement. Alliance structures extend reach into hospital systems and specialty clinics through co-promotion and distribution agreements. Market access strategies are tailored to regional payer frameworks and clinical guideline environments. U.S. commercialization aligns with evolving FDA and payer requirements.

Specialty distribution to care sites

Distribution flows through specialty pharmacies, hospital pharmacies, and integrated delivery networks, prioritizing nephrology clinics and the roughly 7,700 US dialysis centers as primary points of care; oncology and hematology centers are engaged for MDS populations. Inventory is actively balanced across channels to protect patient continuity and minimize stockouts.

Reliable GMP supply chain

API and finished-dose manufacturing are qualified with redundancy (dual/multiple sites) to reduce disruption risk by over 50%. Robust QA/QC and track-and-trace systems protect product integrity across nearly 100% of commercial batches, meeting GMP/GDP standards. Forecasting aligns production by indication and region, while oral solid-dose logistics cut cold-chain reliance and can lower distribution costs by up to 60% versus refrigerated formats.

Formulary and reimbursement placement

Access teams drive national and regional formulary listings while leveraging health economic dossiers to negotiate with payers and tenders; global pharma spend was about $1.5 trillion in 2024, underscoring payer leverage. Hospital P&T submissions emphasize clinical and budget impact data. Post-listing pull-through ensures stock and prescribing-site availability.

- Formulary listings: national + regional

- HEOR dossiers: payer & tender negotiations

- P&T submissions: clinical & budget impact

- Post-listing: pull-through at prescribing sites

Digital access and patient fulfillment

- e-prescribing >90%

- hub programs −30% time-to-treatment

- home delivery ≈30%

- adherence +12%

Nephrology rollout: ~7,700 US dialysis centers, >90% e-prescribing, -30% time-to-treatment

Commercial rollout leverages partners in China, Japan and EU and targets nephrology via ~7,700 US dialysis centers plus specialty pharmacies. Distribution uses specialty hubs, e-prescribing (>90%) and home delivery (~30%), with hub programs cutting time-to-treatment ~30% and adherence up ~12%. Manufacturing redundancy halves disruption risk and ~100% batches meet QA/QC.

| Metric | Value |

|---|---|

| US dialysis centers | ~7,700 |

| E-prescribing | >90% |

| Hub time-to-treatment | −30% |

| Home delivery | ≈30% |

| Adherence lift | +12% |

| Disruption risk reduction | >50% |

| Batch QA/QC | ~100% |

Preview the Actual Deliverable

FibroGen 4P's Marketing Mix Analysis

The preview shown here is the actual FibroGen 4P's Marketing Mix Analysis you’ll receive instantly after purchase—no surprises. This is the same ready-made, editable document you'll download immediately after checkout, fully complete and ready to use. You’re viewing the exact version of the analysis included with your order, high-quality and final.