Fair Isaac Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

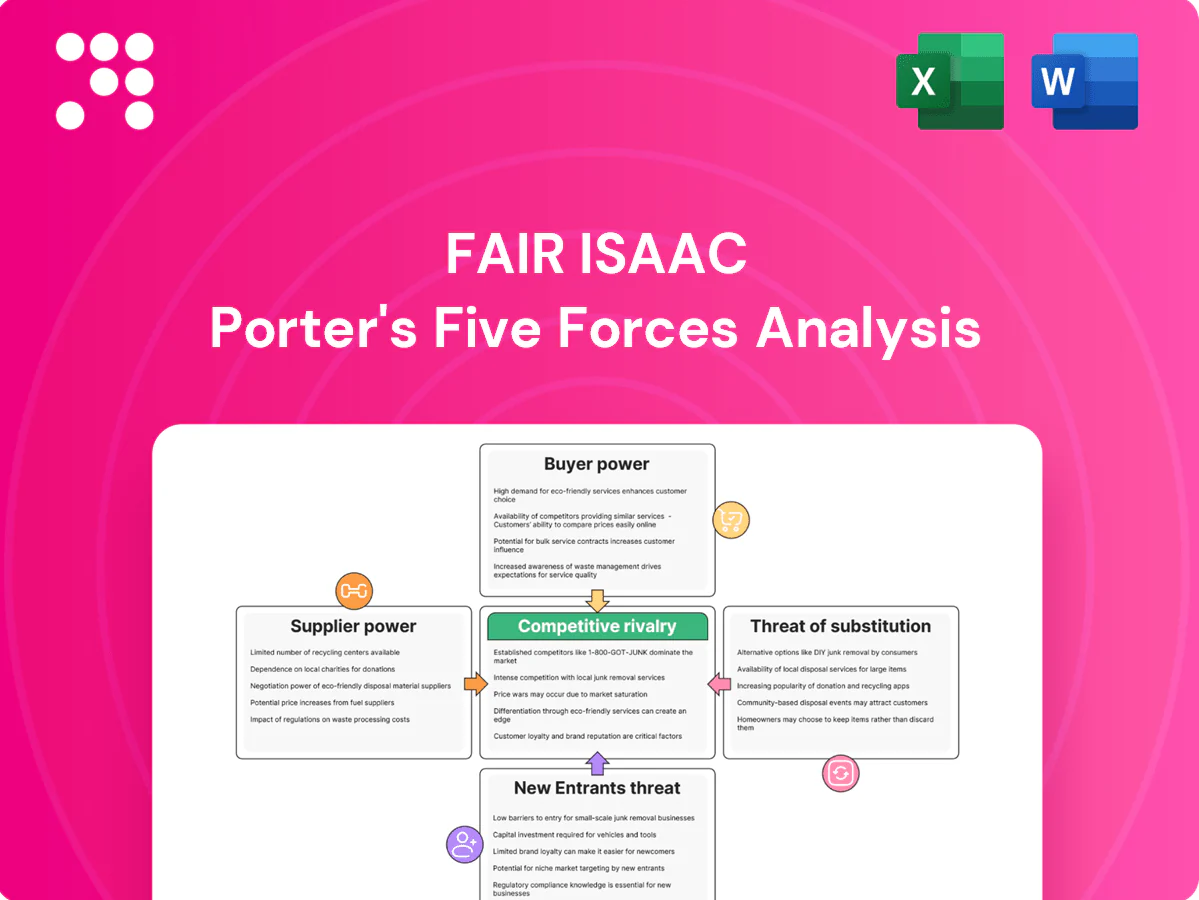

This brief Porter's Five Forces snapshot highlights Fair Isaac’s competitive dynamics—buyer and supplier power, rivalry intensity, and threats from new entrants and substitutes—to frame current market pressures. Want deeper, force-by-force ratings, visuals, and clear business implications? Unlock the full analysis to drive smarter investment and strategy decisions.

Suppliers Bargaining Power

Specialized data providers

Core inputs for FICO—credit bureau, consortium and alternative data—are concentrated among three major bureaus that together supply roughly 90% of U.S. consumer credit files, limiting substitutes and raising switching costs and compliance risk. FICO’s brand and penetration—its scoring models are used by about 90% of top U.S. lenders—gives it negotiating leverage with these suppliers. Long-term data agreements reduce short-term pricing volatility but often include escalation clauses that can lock in higher costs over time.

Cloud and compute platforms

FICO Platform and Scores depend on hyperscaler infra for scalability and low latency; in 2024 AWS, Microsoft Azure and Google Cloud held roughly 32%, 23% and 12% of the cloud market respectively, concentrating supplier power. Dependency on few vendors raises pricing and technical lock-in risk. Multi-cloud architectures and containerization partially offset this power but add complexity. Data residency and security requirements—cited by ~58% of firms in 2024 surveys—further constrain switching.

AI/ML tooling and IP

Proprietary FICO algorithms reduce dependency on third-party models, but open-source ML frameworks and GPUs remain foundational, with NVIDIA holding roughly 80% of the AI accelerator market in 2024, increasing supplier sway. Scarcity of high-end compute and restrictive licensing for some toolchains elevate supplier leverage and can raise costs. FICO’s model IP and patents provide meaningful counterbalance to vendor power. Rapid hardware and software cycles can force upgrades on supplier terms, compressing bargaining windows.

Talent and niche expertise

Data scientists, model validators and regulatory experts remain scarce and mobile; US data science unemployment fell to ~1.7% in 2024 and median total compensation reached ≈$130k, pushing retention costs up 10–20% YoY for leading analytics firms. Hybrid work and global delivery lowered sourcing concentration, and codifying knowledge into the platform reduces single-employee dependency and redeployment risk.

- Scarcity: unemployment ~1.7% (2024)

- Compensation: median ≈$130k

- Retention cost rise: ~10–20% YoY

- Diversification: hybrid + global delivery

- Mitigation: platform codification

Regulatory and standards bodies

Regulatory rule changes in 2024 around fair lending, model risk and privacy act as suppliers of constraints, forcing mandatory compliance tooling, audits and certifications that FICO must integrate; sudden shifts still drive costly rework and vendor reliance. FICO, founded 1956, reported roughly $1.94B revenue in FY2024 and its long regulatory track record limits disruption.

- 2024: mandatory audits ↑ compliance spend

- FICO: long tenure, ~1.94B revenue (FY2024)

- Model risk guidance → vendor lock and rework risk

Supplier concentration: bureaus, hyperscalers, NVIDIA and scarce data talent raise switching costs

Supplier power is high: three bureaus supply ~90% of U.S. credit files, hyperscalers (AWS 32%, Azure 23%, GCP 12% 2024) and NVIDIA (≈80% AI accelerators) concentrate infra, while scarce talent (data science unemployment ~1.7%, median comp ≈$130k 2024) and regulatory mandates raise switching costs; FICO’s IP, scale and multi-cloud use partially mitigate this.

| Metric | 2024 |

|---|---|

| Credit bureaus share | ~90% |

| AWS/Azure/GCP | 32% / 23% / 12% |

| NVIDIA AI accel. | ≈80% |

| Data sci. unemployment | ~1.7% |

| Median comp | ≈$130k |

| FICO revenue (FY) | $1.94B |

What is included in the product

Comprehensive Porter's Five Forces analysis of Fair Isaac that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats, with strategic insights for pricing and market positioning.

Fair Isaac's Porter's Five Forces tool delivers a clear one-sheet summary with customizable pressure levels and an instant spider chart, simplifying competitive analysis into board-ready insights for faster, pain-free decisions.

Customers Bargaining Power

Concentrated financial institutions

Large banks, card issuers and auto lenders drive a major share of FICO’s revenue as US credit card balances exceed 1 trillion and auto loan outstanding tops 1.6 trillion, giving these customers strong price and contract leverage. FICO’s mission-critical scoring and switching risk limit deep discounts despite multi-year deals. Co-development and outcome-based pricing are used to align incentives and preserve margins.

Procurement sophistication

Buyers run formal RFPs comparing FICO to in‑house and rival platforms, with 2024 procurement surveys showing roughly 60% of large enterprises include in‑house options and TCO comparisons in vendor RFIs; compliance features and audit trails are dissected line‑by‑line. Referenceability and documented ROI case studies (often cited as improving win rates by ~15–25% in 2024 deal analyses) blunt buyer bargaining power. However, growing data portability demands and regulatory pressure in 2024 have forced vendors to offer concessions on exportability and interoperability, increasing negotiation leverage for customers.

Switching and integration costs

Embedded FICO scores and decision flows create sticky integrations—FICO is used in about 90% of U.S. lending decisions (FICO, 2024). Retraining models, revalidation and regulator approvals commonly take 3–12 months and enterprise switching can cost $100k–$1M, raising friction. That lock-in reduces buyer power despite periodic pricing pressure. Open APIs, whose bank adoption rose markedly by 2024, both ease exit and fuel wider adoption.

Price sensitivity vs outcomes

Price sensitivity is secondary to measurable risk and fraud outcomes: 2024 client benchmarks show approval lifts of 5–12% and charge-off reductions of 15–30%, which justify premium pricing for proven models that lower loss rates and raise net yield.

- Value: outcome-driven pricing

- Evidence: 5–12% approvals, 15–30% charge-offs (2024)

- Downturn: tighter budgets, annual reviews

- Pricing: tiered modules & usage options

Segment diversity

Segment diversity across SMBs, fintechs and non-financial sectors creates fragmented requirements for FICO products; SMBs (SMEs make up ~90% of firms worldwide) have less procurement leverage but typically show higher churn versus enterprises, while fintechs demand rapid integration and non-financial buyers prioritize analytics and compliance.

- SMBs: low leverage, higher churn

- Fintechs: fast integration needs

- Non-financial: compliance-driven

- Partners/resellers: aggregate demand

FICO Dominance and High Switching Costs Keep Pricing Power with Large Banks

Large banks and card issuers (US card debt >1T, auto loans >1.6T) hold negotiating leverage, yet FICO’s mission‑critical scoring (~90% of US lending decisions, 2024) and switching costs ($100k–$1M, 3–12 months) limit deep discounts. Buyers run RFPs with ~60% including in‑house options (2024), but documented 5–12% approval lifts and 15–30% charge‑off reduction justify premiums.

| Metric | 2024 |

|---|---|

| US card balances | >$1T |

| Auto loans | $1.6T |

| FICO usage | ~90% |

| RFPs with in‑house | ~60% |

What You See Is What You Get

Fair Isaac Porter's Five Forces Analysis

This preview is the exact Fair Isaac Porter's Five Forces Analysis document you'll receive immediately after purchase—fully formatted and ready for use. No placeholders or samples, just the complete professional analysis. Once bought, you get this same file instantly for download and implementation.

A Must-Have Tool for Decision-Makers

This brief Porter's Five Forces snapshot highlights Fair Isaac’s competitive dynamics—buyer and supplier power, rivalry intensity, and threats from new entrants and substitutes—to frame current market pressures. Want deeper, force-by-force ratings, visuals, and clear business implications? Unlock the full analysis to drive smarter investment and strategy decisions.

Suppliers Bargaining Power

Specialized data providers

Core inputs for FICO—credit bureau, consortium and alternative data—are concentrated among three major bureaus that together supply roughly 90% of U.S. consumer credit files, limiting substitutes and raising switching costs and compliance risk. FICO’s brand and penetration—its scoring models are used by about 90% of top U.S. lenders—gives it negotiating leverage with these suppliers. Long-term data agreements reduce short-term pricing volatility but often include escalation clauses that can lock in higher costs over time.

Cloud and compute platforms

FICO Platform and Scores depend on hyperscaler infra for scalability and low latency; in 2024 AWS, Microsoft Azure and Google Cloud held roughly 32%, 23% and 12% of the cloud market respectively, concentrating supplier power. Dependency on few vendors raises pricing and technical lock-in risk. Multi-cloud architectures and containerization partially offset this power but add complexity. Data residency and security requirements—cited by ~58% of firms in 2024 surveys—further constrain switching.

AI/ML tooling and IP

Proprietary FICO algorithms reduce dependency on third-party models, but open-source ML frameworks and GPUs remain foundational, with NVIDIA holding roughly 80% of the AI accelerator market in 2024, increasing supplier sway. Scarcity of high-end compute and restrictive licensing for some toolchains elevate supplier leverage and can raise costs. FICO’s model IP and patents provide meaningful counterbalance to vendor power. Rapid hardware and software cycles can force upgrades on supplier terms, compressing bargaining windows.

Talent and niche expertise

Data scientists, model validators and regulatory experts remain scarce and mobile; US data science unemployment fell to ~1.7% in 2024 and median total compensation reached ≈$130k, pushing retention costs up 10–20% YoY for leading analytics firms. Hybrid work and global delivery lowered sourcing concentration, and codifying knowledge into the platform reduces single-employee dependency and redeployment risk.

- Scarcity: unemployment ~1.7% (2024)

- Compensation: median ≈$130k

- Retention cost rise: ~10–20% YoY

- Diversification: hybrid + global delivery

- Mitigation: platform codification

Regulatory and standards bodies

Regulatory rule changes in 2024 around fair lending, model risk and privacy act as suppliers of constraints, forcing mandatory compliance tooling, audits and certifications that FICO must integrate; sudden shifts still drive costly rework and vendor reliance. FICO, founded 1956, reported roughly $1.94B revenue in FY2024 and its long regulatory track record limits disruption.

- 2024: mandatory audits ↑ compliance spend

- FICO: long tenure, ~1.94B revenue (FY2024)

- Model risk guidance → vendor lock and rework risk

Supplier concentration: bureaus, hyperscalers, NVIDIA and scarce data talent raise switching costs

Supplier power is high: three bureaus supply ~90% of U.S. credit files, hyperscalers (AWS 32%, Azure 23%, GCP 12% 2024) and NVIDIA (≈80% AI accelerators) concentrate infra, while scarce talent (data science unemployment ~1.7%, median comp ≈$130k 2024) and regulatory mandates raise switching costs; FICO’s IP, scale and multi-cloud use partially mitigate this.

| Metric | 2024 |

|---|---|

| Credit bureaus share | ~90% |

| AWS/Azure/GCP | 32% / 23% / 12% |

| NVIDIA AI accel. | ≈80% |

| Data sci. unemployment | ~1.7% |

| Median comp | ≈$130k |

| FICO revenue (FY) | $1.94B |

What is included in the product

Comprehensive Porter's Five Forces analysis of Fair Isaac that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats, with strategic insights for pricing and market positioning.

Fair Isaac's Porter's Five Forces tool delivers a clear one-sheet summary with customizable pressure levels and an instant spider chart, simplifying competitive analysis into board-ready insights for faster, pain-free decisions.

Customers Bargaining Power

Concentrated financial institutions

Large banks, card issuers and auto lenders drive a major share of FICO’s revenue as US credit card balances exceed 1 trillion and auto loan outstanding tops 1.6 trillion, giving these customers strong price and contract leverage. FICO’s mission-critical scoring and switching risk limit deep discounts despite multi-year deals. Co-development and outcome-based pricing are used to align incentives and preserve margins.

Procurement sophistication

Buyers run formal RFPs comparing FICO to in‑house and rival platforms, with 2024 procurement surveys showing roughly 60% of large enterprises include in‑house options and TCO comparisons in vendor RFIs; compliance features and audit trails are dissected line‑by‑line. Referenceability and documented ROI case studies (often cited as improving win rates by ~15–25% in 2024 deal analyses) blunt buyer bargaining power. However, growing data portability demands and regulatory pressure in 2024 have forced vendors to offer concessions on exportability and interoperability, increasing negotiation leverage for customers.

Switching and integration costs

Embedded FICO scores and decision flows create sticky integrations—FICO is used in about 90% of U.S. lending decisions (FICO, 2024). Retraining models, revalidation and regulator approvals commonly take 3–12 months and enterprise switching can cost $100k–$1M, raising friction. That lock-in reduces buyer power despite periodic pricing pressure. Open APIs, whose bank adoption rose markedly by 2024, both ease exit and fuel wider adoption.

Price sensitivity vs outcomes

Price sensitivity is secondary to measurable risk and fraud outcomes: 2024 client benchmarks show approval lifts of 5–12% and charge-off reductions of 15–30%, which justify premium pricing for proven models that lower loss rates and raise net yield.

- Value: outcome-driven pricing

- Evidence: 5–12% approvals, 15–30% charge-offs (2024)

- Downturn: tighter budgets, annual reviews

- Pricing: tiered modules & usage options

Segment diversity

Segment diversity across SMBs, fintechs and non-financial sectors creates fragmented requirements for FICO products; SMBs (SMEs make up ~90% of firms worldwide) have less procurement leverage but typically show higher churn versus enterprises, while fintechs demand rapid integration and non-financial buyers prioritize analytics and compliance.

- SMBs: low leverage, higher churn

- Fintechs: fast integration needs

- Non-financial: compliance-driven

- Partners/resellers: aggregate demand

FICO Dominance and High Switching Costs Keep Pricing Power with Large Banks

Large banks and card issuers (US card debt >1T, auto loans >1.6T) hold negotiating leverage, yet FICO’s mission‑critical scoring (~90% of US lending decisions, 2024) and switching costs ($100k–$1M, 3–12 months) limit deep discounts. Buyers run RFPs with ~60% including in‑house options (2024), but documented 5–12% approval lifts and 15–30% charge‑off reduction justify premiums.

| Metric | 2024 |

|---|---|

| US card balances | >$1T |

| Auto loans | $1.6T |

| FICO usage | ~90% |

| RFPs with in‑house | ~60% |

What You See Is What You Get

Fair Isaac Porter's Five Forces Analysis

This preview is the exact Fair Isaac Porter's Five Forces Analysis document you'll receive immediately after purchase—fully formatted and ready for use. No placeholders or samples, just the complete professional analysis. Once bought, you get this same file instantly for download and implementation.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

This brief Porter's Five Forces snapshot highlights Fair Isaac’s competitive dynamics—buyer and supplier power, rivalry intensity, and threats from new entrants and substitutes—to frame current market pressures. Want deeper, force-by-force ratings, visuals, and clear business implications? Unlock the full analysis to drive smarter investment and strategy decisions.

Suppliers Bargaining Power

Specialized data providers

Core inputs for FICO—credit bureau, consortium and alternative data—are concentrated among three major bureaus that together supply roughly 90% of U.S. consumer credit files, limiting substitutes and raising switching costs and compliance risk. FICO’s brand and penetration—its scoring models are used by about 90% of top U.S. lenders—gives it negotiating leverage with these suppliers. Long-term data agreements reduce short-term pricing volatility but often include escalation clauses that can lock in higher costs over time.

Cloud and compute platforms

FICO Platform and Scores depend on hyperscaler infra for scalability and low latency; in 2024 AWS, Microsoft Azure and Google Cloud held roughly 32%, 23% and 12% of the cloud market respectively, concentrating supplier power. Dependency on few vendors raises pricing and technical lock-in risk. Multi-cloud architectures and containerization partially offset this power but add complexity. Data residency and security requirements—cited by ~58% of firms in 2024 surveys—further constrain switching.

AI/ML tooling and IP

Proprietary FICO algorithms reduce dependency on third-party models, but open-source ML frameworks and GPUs remain foundational, with NVIDIA holding roughly 80% of the AI accelerator market in 2024, increasing supplier sway. Scarcity of high-end compute and restrictive licensing for some toolchains elevate supplier leverage and can raise costs. FICO’s model IP and patents provide meaningful counterbalance to vendor power. Rapid hardware and software cycles can force upgrades on supplier terms, compressing bargaining windows.

Talent and niche expertise

Data scientists, model validators and regulatory experts remain scarce and mobile; US data science unemployment fell to ~1.7% in 2024 and median total compensation reached ≈$130k, pushing retention costs up 10–20% YoY for leading analytics firms. Hybrid work and global delivery lowered sourcing concentration, and codifying knowledge into the platform reduces single-employee dependency and redeployment risk.

- Scarcity: unemployment ~1.7% (2024)

- Compensation: median ≈$130k

- Retention cost rise: ~10–20% YoY

- Diversification: hybrid + global delivery

- Mitigation: platform codification

Regulatory and standards bodies

Regulatory rule changes in 2024 around fair lending, model risk and privacy act as suppliers of constraints, forcing mandatory compliance tooling, audits and certifications that FICO must integrate; sudden shifts still drive costly rework and vendor reliance. FICO, founded 1956, reported roughly $1.94B revenue in FY2024 and its long regulatory track record limits disruption.

- 2024: mandatory audits ↑ compliance spend

- FICO: long tenure, ~1.94B revenue (FY2024)

- Model risk guidance → vendor lock and rework risk

Supplier concentration: bureaus, hyperscalers, NVIDIA and scarce data talent raise switching costs

Supplier power is high: three bureaus supply ~90% of U.S. credit files, hyperscalers (AWS 32%, Azure 23%, GCP 12% 2024) and NVIDIA (≈80% AI accelerators) concentrate infra, while scarce talent (data science unemployment ~1.7%, median comp ≈$130k 2024) and regulatory mandates raise switching costs; FICO’s IP, scale and multi-cloud use partially mitigate this.

| Metric | 2024 |

|---|---|

| Credit bureaus share | ~90% |

| AWS/Azure/GCP | 32% / 23% / 12% |

| NVIDIA AI accel. | ≈80% |

| Data sci. unemployment | ~1.7% |

| Median comp | ≈$130k |

| FICO revenue (FY) | $1.94B |

What is included in the product

Comprehensive Porter's Five Forces analysis of Fair Isaac that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats, with strategic insights for pricing and market positioning.

Fair Isaac's Porter's Five Forces tool delivers a clear one-sheet summary with customizable pressure levels and an instant spider chart, simplifying competitive analysis into board-ready insights for faster, pain-free decisions.

Customers Bargaining Power

Concentrated financial institutions

Large banks, card issuers and auto lenders drive a major share of FICO’s revenue as US credit card balances exceed 1 trillion and auto loan outstanding tops 1.6 trillion, giving these customers strong price and contract leverage. FICO’s mission-critical scoring and switching risk limit deep discounts despite multi-year deals. Co-development and outcome-based pricing are used to align incentives and preserve margins.

Procurement sophistication

Buyers run formal RFPs comparing FICO to in‑house and rival platforms, with 2024 procurement surveys showing roughly 60% of large enterprises include in‑house options and TCO comparisons in vendor RFIs; compliance features and audit trails are dissected line‑by‑line. Referenceability and documented ROI case studies (often cited as improving win rates by ~15–25% in 2024 deal analyses) blunt buyer bargaining power. However, growing data portability demands and regulatory pressure in 2024 have forced vendors to offer concessions on exportability and interoperability, increasing negotiation leverage for customers.

Switching and integration costs

Embedded FICO scores and decision flows create sticky integrations—FICO is used in about 90% of U.S. lending decisions (FICO, 2024). Retraining models, revalidation and regulator approvals commonly take 3–12 months and enterprise switching can cost $100k–$1M, raising friction. That lock-in reduces buyer power despite periodic pricing pressure. Open APIs, whose bank adoption rose markedly by 2024, both ease exit and fuel wider adoption.

Price sensitivity vs outcomes

Price sensitivity is secondary to measurable risk and fraud outcomes: 2024 client benchmarks show approval lifts of 5–12% and charge-off reductions of 15–30%, which justify premium pricing for proven models that lower loss rates and raise net yield.

- Value: outcome-driven pricing

- Evidence: 5–12% approvals, 15–30% charge-offs (2024)

- Downturn: tighter budgets, annual reviews

- Pricing: tiered modules & usage options

Segment diversity

Segment diversity across SMBs, fintechs and non-financial sectors creates fragmented requirements for FICO products; SMBs (SMEs make up ~90% of firms worldwide) have less procurement leverage but typically show higher churn versus enterprises, while fintechs demand rapid integration and non-financial buyers prioritize analytics and compliance.

- SMBs: low leverage, higher churn

- Fintechs: fast integration needs

- Non-financial: compliance-driven

- Partners/resellers: aggregate demand

FICO Dominance and High Switching Costs Keep Pricing Power with Large Banks

Large banks and card issuers (US card debt >1T, auto loans >1.6T) hold negotiating leverage, yet FICO’s mission‑critical scoring (~90% of US lending decisions, 2024) and switching costs ($100k–$1M, 3–12 months) limit deep discounts. Buyers run RFPs with ~60% including in‑house options (2024), but documented 5–12% approval lifts and 15–30% charge‑off reduction justify premiums.

| Metric | 2024 |

|---|---|

| US card balances | >$1T |

| Auto loans | $1.6T |

| FICO usage | ~90% |

| RFPs with in‑house | ~60% |

What You See Is What You Get

Fair Isaac Porter's Five Forces Analysis

This preview is the exact Fair Isaac Porter's Five Forces Analysis document you'll receive immediately after purchase—fully formatted and ready for use. No placeholders or samples, just the complete professional analysis. Once bought, you get this same file instantly for download and implementation.