FILA Holdings Porter's Five Forces Analysis

From Overview to Strategy Blueprint

FILA Holdings faces varied competitive pressures—from intense retail rivalry and shifting consumer tastes to supplier negotiating power and substitute threats in athleisure. This brief highlights key tensions and strategic levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and actionable recommendations. Get the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Tiered sourcing concentration

Footwear and apparel rely on concentrated tiers of leather, rubber, synthetics and cotton suppliers, with industry estimates in 2024 indicating the top 5 producers control roughly 50–70% of specialty EVA/PU capacity, raising switching costs for brands like FILA. Capacity constraints and tightening compliance standards increase supplier leverage, while FILA reduces risk through multi-sourcing and regional vendor bases across APAC and Europe.

Contract manufacturers’ leverage

FILA’s Asian ODM/OEM partners hold critical process know-how and scheduling power—Asia supplies over 70% of global footwear production (UN Comtrade 2023), and factory utilization often exceeds 85% in peak months, shifting bargaining power to manufacturers on price and lead times. Compliance, quality and speed-to-market needs limit easy substitution, while multi-year volume commitments and long-term contracts help temper cost volatility.

Branded component dependence

Performance lines use proprietary foams, outsoles and trims from specialized firms, which restrict interchangeability and often require design rework; in 2024 many premium midsole technologies remained concentrated among a handful of suppliers, amplifying supplier leverage. Unique molds and lasts create tooling lock-in that raises switching costs and amortization risk. FILA mitigates influence through negotiated IP licenses and volume rebates to preserve margins and supply continuity.

Logistics and trade exposure

Ocean freight volatility (container spot rates fell ~60–70% from 2021 peaks to 2024 averages), port congestion (dwell times rose up to 20% in some hubs) and shifting tariff regimes materially raise landed cost and tighten supplier terms; logistics providers can capture premiums in tight capacity cycles (cost swings 15–30%). Currency moves in KRW, USD and CNY (intra-year ±8–12% in 2024) complicate contract pricing while diversified forwarders/3PLs cut single-point risk.

- Ocean freight: spot rates down ~60–70% vs 2021

- Port congestion: dwell times ↑ up to 20%

- Capacity cycles: freight swings 15–30%

- Currency volatility: KRW/USD/CNY ±8–12% (2024)

- Mitigation: multi-forwarder/3PL diversification

Acushnet partial hedge

Acushnet, owned by FILA since 2011, partially hedges supplier concentration by adding golf-equipment sourcing to FILA Holdings’ apparel and footwear supply base, diversifying materials and vendor ecosystems.

Acushnet’s scale and procurement intelligence—notably in golf balls, clubs and footwear—can strengthen apparel-side negotiations, though specialized golf components (precision cores, club heads) maintain distinct supplier power dynamics.

- Diversification: reduces apparel/footwear supplier concentration

- Procurement leverage: Acushnet sourcing expertise informs negotiations

- Specialization risk: golf components retain niche supplier power

Suppliers exert moderate-to-high leverage with concentrated EVA/PU and Asia OEM dominance

Suppliers hold moderate-to-high bargaining power for FILA due to concentrated specialty materials (top-5 EVA/PU capacity 50–70% in 2024) and Asia OEM dominance (>70% footwear output). FILA mitigates via multi-sourcing, regional vendors, Acushnet procurement and long-term contracts. Logistics and FX volatility (KRW/USD/CNY ±8–12% 2024) add supplier leverage.

| Factor | 2024 Metric |

|---|---|

| Top-5 EVA/PU share | 50–70% |

| Asia footwear output | >70% |

| FX intra-year | ±8–12% |

What is included in the product

Concise Porter's Five Forces assessment of FILA Holdings, evaluating competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and highlighting disruptive trends and entry barriers that shape its pricing power and strategic positioning.

A one-sheet Porter's Five Forces summary for FILA Holdings that quantifies competitive pressures, with customizable scores and a spider chart for instant strategic insight—ready to drop into decks or Excel dashboards.

Customers Bargaining Power

Wholesale retailer clout

Global sporting goods chains and department stores command volume and shelf space — for example, Decathlon operated about 1,900 stores across 70+ countries in 2024 — allowing negotiation of markdown support, payment terms and exclusives; consolidation intensifies retailer leverage, while FILA offsets pressure via selective distribution and regional partner agreements.

DTC and e-commerce options

FILA’s DTC e-commerce and flagship stores are margin-accretive channels that capture higher gross margins and first‑party data; with global e-commerce penetration at about 22% in 2024 this reduces reliance on powerful wholesalers. Consumers’ expectation of frequent online promotions raises price transparency and churn, while strong omnichannel execution—omnichannel shoppers spend roughly 2x more—helps moderate buyer power.

Price-sensitive segments

Large portions of demand for FILA fall in value and mid-tier price points, consistent with the $95B global athletic footwear market in 2024 where price sensitivity is high. Shoppers frequently switch to private labels or discounted legacy models, and a high promotional cadence increases elasticity. Targeted design drops and collaborations have softened price pressure by boosting perceived differentiation and limited-edition demand.

Athletes and influencers

Athletes and influencers shape consumer preference and retail buys for FILA; influencer marketing was valued at about 21.1 billion USD in 2023, underlining major sway. Star power boosts negotiating leverage with retailers but increases endorsement costs, as top-tier athlete deals can exceed 10 million USD annually. Contract renewals create binary revenue and image risk if not renewed, while diversified ambassador rosters dilute concentration risk.

Acushnet’s trade customers

Acushnet’s trade customers—golf retailers, pro shops and fitters—wield informed bargaining power, favoring fit-driven purchases that are less price elastic but require demonstrable performance; Acushnet reported approximately $1.7 billion in net sales in 2023, with Titleist and FootJoy driving core demand. Seasonal cycles and tour-driven sell-through compress reorder windows and strengthen buyers’ leverage on terms, while cross-brand bundling within FILA Holdings mitigates pressure by enabling package deals and broader assortment strategies.

- Informed buyers: fit vs price

- Performance proof required

- Seasonal/tour-driven reorder pressure

- Bundling reduces single-brand leverage

Retailer consolidation boosts buyer leverage; DTC and e‑commerce reshape margins

Retailer consolidation and chains like Decathlon (≈1,900 stores, 70+ countries in 2024) give buyers leverage on terms; FILA counters via selective distribution and regional partners. DTC and flagship channels (global e‑commerce ≈22% in 2024) raise margins and data capture but online price transparency increases churn. Mid‑tier price sensitivity in the $95B 2024 athletic footwear market elevates promotional elasticity; influencer spend (~21.1B USD in 2023) further shapes demand.

| Metric | Value |

|---|---|

| Decathlon stores (2024) | ≈1,900 |

| Global e‑commerce (2024) | ≈22% |

| Athletic footwear market (2024) | $95B |

| Influencer market (2023) | $21.1B |

| Acushnet net sales (2023) | $1.7B |

What You See Is What You Get

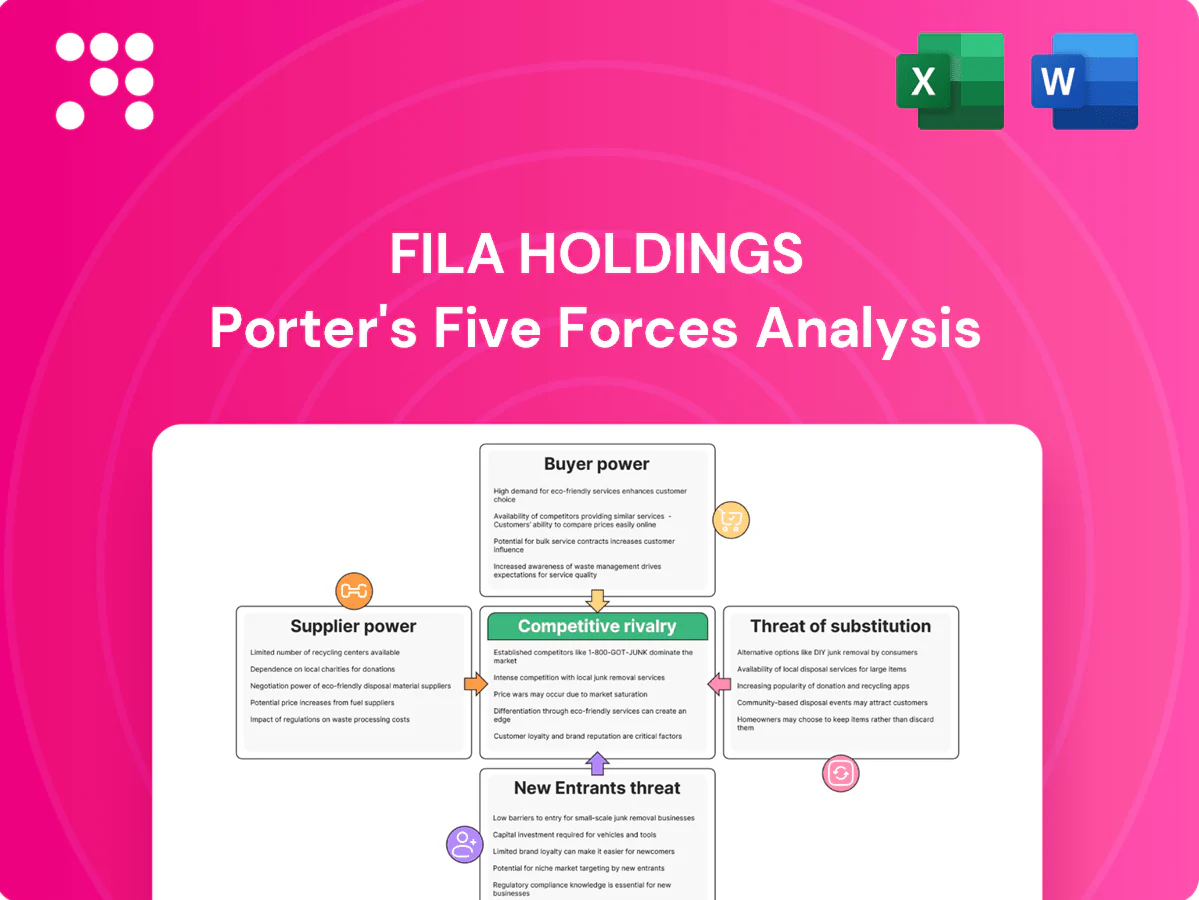

FILA Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for FILA Holdings you'll receive immediately after purchase—no placeholders. The file is professionally formatted and ready to download and use. No mockups or samples; the deliverable is the final, complete analysis.

From Overview to Strategy Blueprint

FILA Holdings faces varied competitive pressures—from intense retail rivalry and shifting consumer tastes to supplier negotiating power and substitute threats in athleisure. This brief highlights key tensions and strategic levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and actionable recommendations. Get the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Tiered sourcing concentration

Footwear and apparel rely on concentrated tiers of leather, rubber, synthetics and cotton suppliers, with industry estimates in 2024 indicating the top 5 producers control roughly 50–70% of specialty EVA/PU capacity, raising switching costs for brands like FILA. Capacity constraints and tightening compliance standards increase supplier leverage, while FILA reduces risk through multi-sourcing and regional vendor bases across APAC and Europe.

Contract manufacturers’ leverage

FILA’s Asian ODM/OEM partners hold critical process know-how and scheduling power—Asia supplies over 70% of global footwear production (UN Comtrade 2023), and factory utilization often exceeds 85% in peak months, shifting bargaining power to manufacturers on price and lead times. Compliance, quality and speed-to-market needs limit easy substitution, while multi-year volume commitments and long-term contracts help temper cost volatility.

Branded component dependence

Performance lines use proprietary foams, outsoles and trims from specialized firms, which restrict interchangeability and often require design rework; in 2024 many premium midsole technologies remained concentrated among a handful of suppliers, amplifying supplier leverage. Unique molds and lasts create tooling lock-in that raises switching costs and amortization risk. FILA mitigates influence through negotiated IP licenses and volume rebates to preserve margins and supply continuity.

Logistics and trade exposure

Ocean freight volatility (container spot rates fell ~60–70% from 2021 peaks to 2024 averages), port congestion (dwell times rose up to 20% in some hubs) and shifting tariff regimes materially raise landed cost and tighten supplier terms; logistics providers can capture premiums in tight capacity cycles (cost swings 15–30%). Currency moves in KRW, USD and CNY (intra-year ±8–12% in 2024) complicate contract pricing while diversified forwarders/3PLs cut single-point risk.

- Ocean freight: spot rates down ~60–70% vs 2021

- Port congestion: dwell times ↑ up to 20%

- Capacity cycles: freight swings 15–30%

- Currency volatility: KRW/USD/CNY ±8–12% (2024)

- Mitigation: multi-forwarder/3PL diversification

Acushnet partial hedge

Acushnet, owned by FILA since 2011, partially hedges supplier concentration by adding golf-equipment sourcing to FILA Holdings’ apparel and footwear supply base, diversifying materials and vendor ecosystems.

Acushnet’s scale and procurement intelligence—notably in golf balls, clubs and footwear—can strengthen apparel-side negotiations, though specialized golf components (precision cores, club heads) maintain distinct supplier power dynamics.

- Diversification: reduces apparel/footwear supplier concentration

- Procurement leverage: Acushnet sourcing expertise informs negotiations

- Specialization risk: golf components retain niche supplier power

Suppliers exert moderate-to-high leverage with concentrated EVA/PU and Asia OEM dominance

Suppliers hold moderate-to-high bargaining power for FILA due to concentrated specialty materials (top-5 EVA/PU capacity 50–70% in 2024) and Asia OEM dominance (>70% footwear output). FILA mitigates via multi-sourcing, regional vendors, Acushnet procurement and long-term contracts. Logistics and FX volatility (KRW/USD/CNY ±8–12% 2024) add supplier leverage.

| Factor | 2024 Metric |

|---|---|

| Top-5 EVA/PU share | 50–70% |

| Asia footwear output | >70% |

| FX intra-year | ±8–12% |

What is included in the product

Concise Porter's Five Forces assessment of FILA Holdings, evaluating competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and highlighting disruptive trends and entry barriers that shape its pricing power and strategic positioning.

A one-sheet Porter's Five Forces summary for FILA Holdings that quantifies competitive pressures, with customizable scores and a spider chart for instant strategic insight—ready to drop into decks or Excel dashboards.

Customers Bargaining Power

Wholesale retailer clout

Global sporting goods chains and department stores command volume and shelf space — for example, Decathlon operated about 1,900 stores across 70+ countries in 2024 — allowing negotiation of markdown support, payment terms and exclusives; consolidation intensifies retailer leverage, while FILA offsets pressure via selective distribution and regional partner agreements.

DTC and e-commerce options

FILA’s DTC e-commerce and flagship stores are margin-accretive channels that capture higher gross margins and first‑party data; with global e-commerce penetration at about 22% in 2024 this reduces reliance on powerful wholesalers. Consumers’ expectation of frequent online promotions raises price transparency and churn, while strong omnichannel execution—omnichannel shoppers spend roughly 2x more—helps moderate buyer power.

Price-sensitive segments

Large portions of demand for FILA fall in value and mid-tier price points, consistent with the $95B global athletic footwear market in 2024 where price sensitivity is high. Shoppers frequently switch to private labels or discounted legacy models, and a high promotional cadence increases elasticity. Targeted design drops and collaborations have softened price pressure by boosting perceived differentiation and limited-edition demand.

Athletes and influencers

Athletes and influencers shape consumer preference and retail buys for FILA; influencer marketing was valued at about 21.1 billion USD in 2023, underlining major sway. Star power boosts negotiating leverage with retailers but increases endorsement costs, as top-tier athlete deals can exceed 10 million USD annually. Contract renewals create binary revenue and image risk if not renewed, while diversified ambassador rosters dilute concentration risk.

Acushnet’s trade customers

Acushnet’s trade customers—golf retailers, pro shops and fitters—wield informed bargaining power, favoring fit-driven purchases that are less price elastic but require demonstrable performance; Acushnet reported approximately $1.7 billion in net sales in 2023, with Titleist and FootJoy driving core demand. Seasonal cycles and tour-driven sell-through compress reorder windows and strengthen buyers’ leverage on terms, while cross-brand bundling within FILA Holdings mitigates pressure by enabling package deals and broader assortment strategies.

- Informed buyers: fit vs price

- Performance proof required

- Seasonal/tour-driven reorder pressure

- Bundling reduces single-brand leverage

Retailer consolidation boosts buyer leverage; DTC and e‑commerce reshape margins

Retailer consolidation and chains like Decathlon (≈1,900 stores, 70+ countries in 2024) give buyers leverage on terms; FILA counters via selective distribution and regional partners. DTC and flagship channels (global e‑commerce ≈22% in 2024) raise margins and data capture but online price transparency increases churn. Mid‑tier price sensitivity in the $95B 2024 athletic footwear market elevates promotional elasticity; influencer spend (~21.1B USD in 2023) further shapes demand.

| Metric | Value |

|---|---|

| Decathlon stores (2024) | ≈1,900 |

| Global e‑commerce (2024) | ≈22% |

| Athletic footwear market (2024) | $95B |

| Influencer market (2023) | $21.1B |

| Acushnet net sales (2023) | $1.7B |

What You See Is What You Get

FILA Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for FILA Holdings you'll receive immediately after purchase—no placeholders. The file is professionally formatted and ready to download and use. No mockups or samples; the deliverable is the final, complete analysis.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

FILA Holdings faces varied competitive pressures—from intense retail rivalry and shifting consumer tastes to supplier negotiating power and substitute threats in athleisure. This brief highlights key tensions and strategic levers but only scratches the surface. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and actionable recommendations. Get the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Tiered sourcing concentration

Footwear and apparel rely on concentrated tiers of leather, rubber, synthetics and cotton suppliers, with industry estimates in 2024 indicating the top 5 producers control roughly 50–70% of specialty EVA/PU capacity, raising switching costs for brands like FILA. Capacity constraints and tightening compliance standards increase supplier leverage, while FILA reduces risk through multi-sourcing and regional vendor bases across APAC and Europe.

Contract manufacturers’ leverage

FILA’s Asian ODM/OEM partners hold critical process know-how and scheduling power—Asia supplies over 70% of global footwear production (UN Comtrade 2023), and factory utilization often exceeds 85% in peak months, shifting bargaining power to manufacturers on price and lead times. Compliance, quality and speed-to-market needs limit easy substitution, while multi-year volume commitments and long-term contracts help temper cost volatility.

Branded component dependence

Performance lines use proprietary foams, outsoles and trims from specialized firms, which restrict interchangeability and often require design rework; in 2024 many premium midsole technologies remained concentrated among a handful of suppliers, amplifying supplier leverage. Unique molds and lasts create tooling lock-in that raises switching costs and amortization risk. FILA mitigates influence through negotiated IP licenses and volume rebates to preserve margins and supply continuity.

Logistics and trade exposure

Ocean freight volatility (container spot rates fell ~60–70% from 2021 peaks to 2024 averages), port congestion (dwell times rose up to 20% in some hubs) and shifting tariff regimes materially raise landed cost and tighten supplier terms; logistics providers can capture premiums in tight capacity cycles (cost swings 15–30%). Currency moves in KRW, USD and CNY (intra-year ±8–12% in 2024) complicate contract pricing while diversified forwarders/3PLs cut single-point risk.

- Ocean freight: spot rates down ~60–70% vs 2021

- Port congestion: dwell times ↑ up to 20%

- Capacity cycles: freight swings 15–30%

- Currency volatility: KRW/USD/CNY ±8–12% (2024)

- Mitigation: multi-forwarder/3PL diversification

Acushnet partial hedge

Acushnet, owned by FILA since 2011, partially hedges supplier concentration by adding golf-equipment sourcing to FILA Holdings’ apparel and footwear supply base, diversifying materials and vendor ecosystems.

Acushnet’s scale and procurement intelligence—notably in golf balls, clubs and footwear—can strengthen apparel-side negotiations, though specialized golf components (precision cores, club heads) maintain distinct supplier power dynamics.

- Diversification: reduces apparel/footwear supplier concentration

- Procurement leverage: Acushnet sourcing expertise informs negotiations

- Specialization risk: golf components retain niche supplier power

Suppliers exert moderate-to-high leverage with concentrated EVA/PU and Asia OEM dominance

Suppliers hold moderate-to-high bargaining power for FILA due to concentrated specialty materials (top-5 EVA/PU capacity 50–70% in 2024) and Asia OEM dominance (>70% footwear output). FILA mitigates via multi-sourcing, regional vendors, Acushnet procurement and long-term contracts. Logistics and FX volatility (KRW/USD/CNY ±8–12% 2024) add supplier leverage.

| Factor | 2024 Metric |

|---|---|

| Top-5 EVA/PU share | 50–70% |

| Asia footwear output | >70% |

| FX intra-year | ±8–12% |

What is included in the product

Concise Porter's Five Forces assessment of FILA Holdings, evaluating competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and highlighting disruptive trends and entry barriers that shape its pricing power and strategic positioning.

A one-sheet Porter's Five Forces summary for FILA Holdings that quantifies competitive pressures, with customizable scores and a spider chart for instant strategic insight—ready to drop into decks or Excel dashboards.

Customers Bargaining Power

Wholesale retailer clout

Global sporting goods chains and department stores command volume and shelf space — for example, Decathlon operated about 1,900 stores across 70+ countries in 2024 — allowing negotiation of markdown support, payment terms and exclusives; consolidation intensifies retailer leverage, while FILA offsets pressure via selective distribution and regional partner agreements.

DTC and e-commerce options

FILA’s DTC e-commerce and flagship stores are margin-accretive channels that capture higher gross margins and first‑party data; with global e-commerce penetration at about 22% in 2024 this reduces reliance on powerful wholesalers. Consumers’ expectation of frequent online promotions raises price transparency and churn, while strong omnichannel execution—omnichannel shoppers spend roughly 2x more—helps moderate buyer power.

Price-sensitive segments

Large portions of demand for FILA fall in value and mid-tier price points, consistent with the $95B global athletic footwear market in 2024 where price sensitivity is high. Shoppers frequently switch to private labels or discounted legacy models, and a high promotional cadence increases elasticity. Targeted design drops and collaborations have softened price pressure by boosting perceived differentiation and limited-edition demand.

Athletes and influencers

Athletes and influencers shape consumer preference and retail buys for FILA; influencer marketing was valued at about 21.1 billion USD in 2023, underlining major sway. Star power boosts negotiating leverage with retailers but increases endorsement costs, as top-tier athlete deals can exceed 10 million USD annually. Contract renewals create binary revenue and image risk if not renewed, while diversified ambassador rosters dilute concentration risk.

Acushnet’s trade customers

Acushnet’s trade customers—golf retailers, pro shops and fitters—wield informed bargaining power, favoring fit-driven purchases that are less price elastic but require demonstrable performance; Acushnet reported approximately $1.7 billion in net sales in 2023, with Titleist and FootJoy driving core demand. Seasonal cycles and tour-driven sell-through compress reorder windows and strengthen buyers’ leverage on terms, while cross-brand bundling within FILA Holdings mitigates pressure by enabling package deals and broader assortment strategies.

- Informed buyers: fit vs price

- Performance proof required

- Seasonal/tour-driven reorder pressure

- Bundling reduces single-brand leverage

Retailer consolidation boosts buyer leverage; DTC and e‑commerce reshape margins

Retailer consolidation and chains like Decathlon (≈1,900 stores, 70+ countries in 2024) give buyers leverage on terms; FILA counters via selective distribution and regional partners. DTC and flagship channels (global e‑commerce ≈22% in 2024) raise margins and data capture but online price transparency increases churn. Mid‑tier price sensitivity in the $95B 2024 athletic footwear market elevates promotional elasticity; influencer spend (~21.1B USD in 2023) further shapes demand.

| Metric | Value |

|---|---|

| Decathlon stores (2024) | ≈1,900 |

| Global e‑commerce (2024) | ≈22% |

| Athletic footwear market (2024) | $95B |

| Influencer market (2023) | $21.1B |

| Acushnet net sales (2023) | $1.7B |

What You See Is What You Get

FILA Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for FILA Holdings you'll receive immediately after purchase—no placeholders. The file is professionally formatted and ready to download and use. No mockups or samples; the deliverable is the final, complete analysis.