FINEOS Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

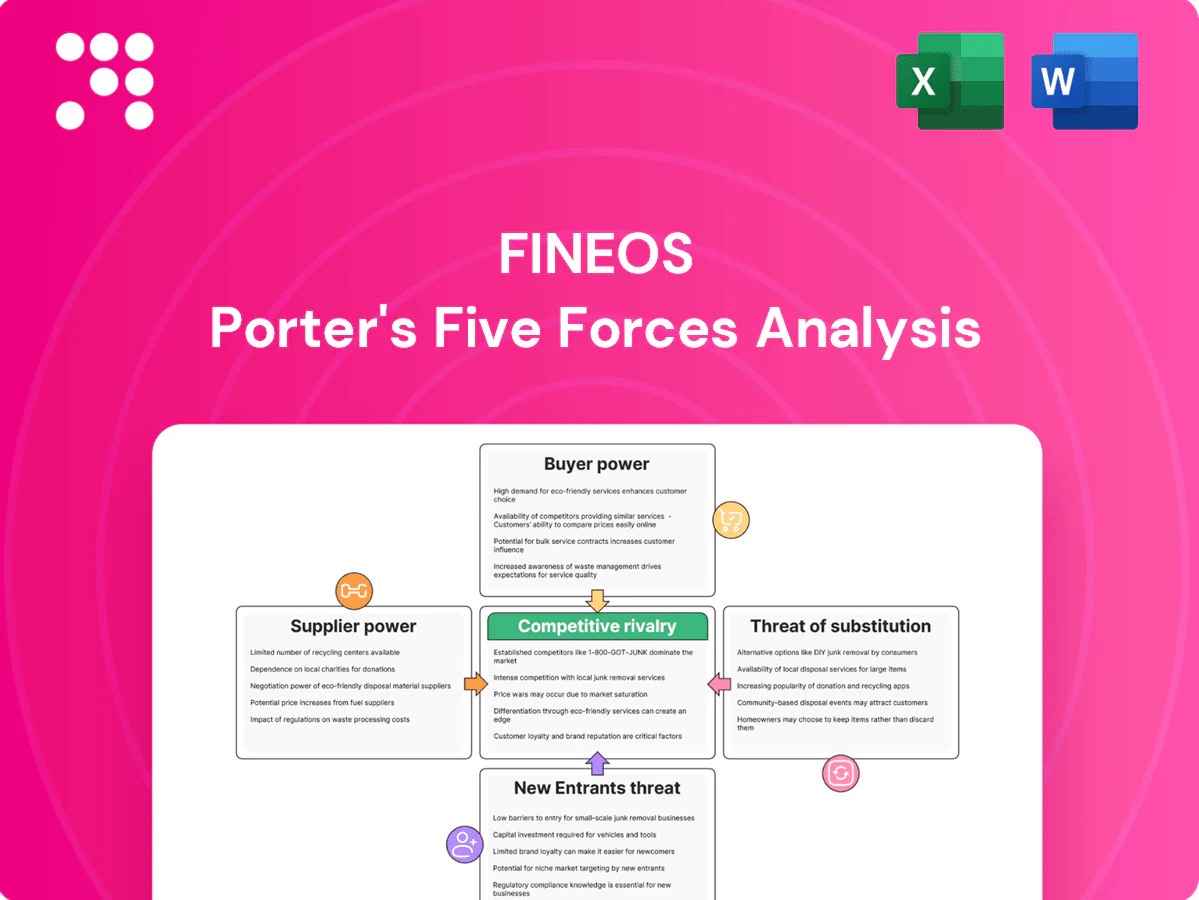

FINEOS faces moderate buyer power, concentrated enterprise buyers, rising competitive rivalry from niche insurtechs, limited supplier leverage, and manageable threat from new entrants but growing substitute solutions; regulatory shifts add external pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore FINEOS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Hyperscaler dependence

FINEOS faces concentrated cloud supplier power as AWS (32%), Microsoft Azure (22%) and Google Cloud (11%) held the lion’s share of global IaaS/PaaS in 2024 (Synergy Research), giving providers leverage on pricing, credits and roadmap access. Outage, data residency and performance SLA demands can force tighter commercial terms. Multicloud reduces single‑vendor risk but adds operational complexity and cost. Negotiating volume commitments and reserved/committed use discounts (up to ~70% in some cases) tempers supplier power.

Specialized talent scarcity

Domain engineers for L/A&H cores, rules engines and actuarial-grade models remain scarce, tightening supplier power; tight labor markets raise wage pressure and contracting rates, which can elongate delivery timelines and inflate project costs. Investment in tooling and partner enablement partially offsets scarcity. BLS projects 22% employment growth for software developers 2020–2030, underscoring sustained demand.

Systems integrators and SI partners

In 2024 large insurers continue to prefer certified systems integrators for implementation and change management, citing reduced project risk and faster go-live. Leading SIs command premium rates and can sway vendor selection through referenceable enterprise deployments. Dependence on a few elite partners increases supplier bargaining power and pricing pressure. Expanding a mid-tier partner ecosystem reduces concentration risk and improves negotiating leverage.

Third‑party data and services

Integrations with identity, medical, payroll and risk providers (KYC, EHR, credit, payroll APIs) are critical for FINEOS and often carry per-call fees and restrictive SLAs; large platform partners commonly impose annual certification and compliance costs running into tens of thousands of dollars (2024 industry practice). Switching vendors is feasible but requires re-certification and regression testing, increasing time-to-market. Volume pricing and standardized connectors (FHIR, OAuth, ISO 20022) narrow supplier leverage.

Regulatory/compliance tooling

Concentrated cloud suppliers exert pricing leverage; dev scarcity and audits raise OPEX

Supplier power is high: AWS 32%, Azure 22%, Google 11% IaaS/PaaS share (2024 Synergy), giving pricing and roadmap leverage. SI concentration, developer scarcity (BLS 22% dev growth 2020–2030) and integration/certification fees raise costs; payment fees ≈1.5–3% and SOC/ISO audits $50k–$200k/yr add OPEX. Multicloud and internal build reduce but not eliminate leverage.

| Factor | 2024 Data |

|---|---|

| Cloud share | AWS 32% / Azure 22% / GCP 11% |

| Payment & audits | Fees 1.5–3% / SOC $50k–$200k |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power and market entry risks tailored exclusively for FINEOS. Identifies disruptive threats, substitutes and protective market dynamics to inform pricing, strategy and investor materials.

Clear one-sheet FINEOS Porter's Five Forces that instantly visualizes competitive pressure via a spider chart and customizable scores—perfect for fast boardroom decisions and stress-testing scenarios without complex tools.

Customers Bargaining Power

Concentrated enterprise buyers

Large carriers and TPAs drive demand for FINEOS and run formal RFPs. In 2024 the top five US carriers accounted for roughly 50% of commercial enrollment, giving them leverage to extract aggressive discounts, bespoke SLAs and contractual protections. Referenceability and marquee wins push vendors to concede tougher terms. Mid-market buyers wield less power but still actively price-shop.

High switching costs yet tough negotiations

Migrations from legacy cores are costly, risky, and typically span 18–36 months with project budgets commonly exceeding $10m, creating high switching costs that increase buyer stickiness. Despite this, buyers leverage competitive bids to extract price discounts and roadmap concessions, with procurement-led RFPs reported in 70% of enterprise deals in 2024. Exit clauses, data portability requirements, and modular adoption reduce lock-in. Vendors must quantify TCO and demonstrable risk reduction to secure concessions.

Feature depth and configurability demands

Insurers require rich L/A&H product configurability, flexible billing and complex claims handling, driving requests for accelerators and no-code tooling that FINEOS emphasized in 2024 product materials. Buyers increasingly push for rapid delivery without custom code, citing time-to-market and implementation cost pressures. Clear out-of-the-box coverage and prebuilt accelerators reduce buyer leverage by shortening procurement cycles and lowering customization spend.

Integration and openness

Open APIs, eventing, and interoperability with CRM, HRIS, and analytics are mandatory for FINEOS buyers; in 2024 surveys showed more than 50% of enterprise purchasers reject proprietary lock-in and require standards-based interfaces. Data access, latency, and real-time sync SLAs become explicit negotiation levers, while strong partner ecosystems blunt buyer power and raise switching costs.

- Open APIs required

- Buyers resist lock-in

- SLAs (latency, sync) as leverage

- Ecosystem reduces buyer power

Outcome and value-based purchasing

Procurement in 2024 ties payment to KPIs such as FNOL cycle time, straight-through processing and cost-to-serve, shifting implementation risk to vendors and hardening price ceilings. Proofs-of-value and ROI models are now prerequisites; demonstrable outcomes can flip buyer pressure into upsell opportunities.

- KPIs: FNOL cycle, STP, cost-to-serve

- Must: PoV, ROI models

- Effect: risk shift, price ceilings, upsell

Procurement-led RFPs, Open APIs and SLAs drive steep vendor discounts and pricing caps

Large US carriers (~50% commercial enrollment in 2024) and TPAs hold strong leverage via RFPs; buyers extract steep discounts. Migrations (18–36 months; typical budgets >$10m) increase stickiness, yet 70% of enterprise deals used procurement-led RFPs in 2024. Open APIs, SLAs and PoV/KPI-linked payments (FNOL, STP) shift risk to vendors and cap pricing.

| Metric | 2024 |

|---|---|

| Top-5 carrier share | ~50% |

| Migration timeline | 18–36 mo |

| Procurement-led deals | 70% |

| Typical project budget | >$10m |

Same Document Delivered

FINEOS Porter's Five Forces Analysis

This preview is the exact FINEOS Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The file shown is fully formatted, professionally written, and ready for download and use the moment you buy. No changes or setup required.

Go Beyond the Preview—Access the Full Strategic Report

FINEOS faces moderate buyer power, concentrated enterprise buyers, rising competitive rivalry from niche insurtechs, limited supplier leverage, and manageable threat from new entrants but growing substitute solutions; regulatory shifts add external pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore FINEOS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Hyperscaler dependence

FINEOS faces concentrated cloud supplier power as AWS (32%), Microsoft Azure (22%) and Google Cloud (11%) held the lion’s share of global IaaS/PaaS in 2024 (Synergy Research), giving providers leverage on pricing, credits and roadmap access. Outage, data residency and performance SLA demands can force tighter commercial terms. Multicloud reduces single‑vendor risk but adds operational complexity and cost. Negotiating volume commitments and reserved/committed use discounts (up to ~70% in some cases) tempers supplier power.

Specialized talent scarcity

Domain engineers for L/A&H cores, rules engines and actuarial-grade models remain scarce, tightening supplier power; tight labor markets raise wage pressure and contracting rates, which can elongate delivery timelines and inflate project costs. Investment in tooling and partner enablement partially offsets scarcity. BLS projects 22% employment growth for software developers 2020–2030, underscoring sustained demand.

Systems integrators and SI partners

In 2024 large insurers continue to prefer certified systems integrators for implementation and change management, citing reduced project risk and faster go-live. Leading SIs command premium rates and can sway vendor selection through referenceable enterprise deployments. Dependence on a few elite partners increases supplier bargaining power and pricing pressure. Expanding a mid-tier partner ecosystem reduces concentration risk and improves negotiating leverage.

Third‑party data and services

Integrations with identity, medical, payroll and risk providers (KYC, EHR, credit, payroll APIs) are critical for FINEOS and often carry per-call fees and restrictive SLAs; large platform partners commonly impose annual certification and compliance costs running into tens of thousands of dollars (2024 industry practice). Switching vendors is feasible but requires re-certification and regression testing, increasing time-to-market. Volume pricing and standardized connectors (FHIR, OAuth, ISO 20022) narrow supplier leverage.

Regulatory/compliance tooling

Concentrated cloud suppliers exert pricing leverage; dev scarcity and audits raise OPEX

Supplier power is high: AWS 32%, Azure 22%, Google 11% IaaS/PaaS share (2024 Synergy), giving pricing and roadmap leverage. SI concentration, developer scarcity (BLS 22% dev growth 2020–2030) and integration/certification fees raise costs; payment fees ≈1.5–3% and SOC/ISO audits $50k–$200k/yr add OPEX. Multicloud and internal build reduce but not eliminate leverage.

| Factor | 2024 Data |

|---|---|

| Cloud share | AWS 32% / Azure 22% / GCP 11% |

| Payment & audits | Fees 1.5–3% / SOC $50k–$200k |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power and market entry risks tailored exclusively for FINEOS. Identifies disruptive threats, substitutes and protective market dynamics to inform pricing, strategy and investor materials.

Clear one-sheet FINEOS Porter's Five Forces that instantly visualizes competitive pressure via a spider chart and customizable scores—perfect for fast boardroom decisions and stress-testing scenarios without complex tools.

Customers Bargaining Power

Concentrated enterprise buyers

Large carriers and TPAs drive demand for FINEOS and run formal RFPs. In 2024 the top five US carriers accounted for roughly 50% of commercial enrollment, giving them leverage to extract aggressive discounts, bespoke SLAs and contractual protections. Referenceability and marquee wins push vendors to concede tougher terms. Mid-market buyers wield less power but still actively price-shop.

High switching costs yet tough negotiations

Migrations from legacy cores are costly, risky, and typically span 18–36 months with project budgets commonly exceeding $10m, creating high switching costs that increase buyer stickiness. Despite this, buyers leverage competitive bids to extract price discounts and roadmap concessions, with procurement-led RFPs reported in 70% of enterprise deals in 2024. Exit clauses, data portability requirements, and modular adoption reduce lock-in. Vendors must quantify TCO and demonstrable risk reduction to secure concessions.

Feature depth and configurability demands

Insurers require rich L/A&H product configurability, flexible billing and complex claims handling, driving requests for accelerators and no-code tooling that FINEOS emphasized in 2024 product materials. Buyers increasingly push for rapid delivery without custom code, citing time-to-market and implementation cost pressures. Clear out-of-the-box coverage and prebuilt accelerators reduce buyer leverage by shortening procurement cycles and lowering customization spend.

Integration and openness

Open APIs, eventing, and interoperability with CRM, HRIS, and analytics are mandatory for FINEOS buyers; in 2024 surveys showed more than 50% of enterprise purchasers reject proprietary lock-in and require standards-based interfaces. Data access, latency, and real-time sync SLAs become explicit negotiation levers, while strong partner ecosystems blunt buyer power and raise switching costs.

- Open APIs required

- Buyers resist lock-in

- SLAs (latency, sync) as leverage

- Ecosystem reduces buyer power

Outcome and value-based purchasing

Procurement in 2024 ties payment to KPIs such as FNOL cycle time, straight-through processing and cost-to-serve, shifting implementation risk to vendors and hardening price ceilings. Proofs-of-value and ROI models are now prerequisites; demonstrable outcomes can flip buyer pressure into upsell opportunities.

- KPIs: FNOL cycle, STP, cost-to-serve

- Must: PoV, ROI models

- Effect: risk shift, price ceilings, upsell

Procurement-led RFPs, Open APIs and SLAs drive steep vendor discounts and pricing caps

Large US carriers (~50% commercial enrollment in 2024) and TPAs hold strong leverage via RFPs; buyers extract steep discounts. Migrations (18–36 months; typical budgets >$10m) increase stickiness, yet 70% of enterprise deals used procurement-led RFPs in 2024. Open APIs, SLAs and PoV/KPI-linked payments (FNOL, STP) shift risk to vendors and cap pricing.

| Metric | 2024 |

|---|---|

| Top-5 carrier share | ~50% |

| Migration timeline | 18–36 mo |

| Procurement-led deals | 70% |

| Typical project budget | >$10m |

Same Document Delivered

FINEOS Porter's Five Forces Analysis

This preview is the exact FINEOS Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The file shown is fully formatted, professionally written, and ready for download and use the moment you buy. No changes or setup required.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

FINEOS faces moderate buyer power, concentrated enterprise buyers, rising competitive rivalry from niche insurtechs, limited supplier leverage, and manageable threat from new entrants but growing substitute solutions; regulatory shifts add external pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore FINEOS’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Hyperscaler dependence

FINEOS faces concentrated cloud supplier power as AWS (32%), Microsoft Azure (22%) and Google Cloud (11%) held the lion’s share of global IaaS/PaaS in 2024 (Synergy Research), giving providers leverage on pricing, credits and roadmap access. Outage, data residency and performance SLA demands can force tighter commercial terms. Multicloud reduces single‑vendor risk but adds operational complexity and cost. Negotiating volume commitments and reserved/committed use discounts (up to ~70% in some cases) tempers supplier power.

Specialized talent scarcity

Domain engineers for L/A&H cores, rules engines and actuarial-grade models remain scarce, tightening supplier power; tight labor markets raise wage pressure and contracting rates, which can elongate delivery timelines and inflate project costs. Investment in tooling and partner enablement partially offsets scarcity. BLS projects 22% employment growth for software developers 2020–2030, underscoring sustained demand.

Systems integrators and SI partners

In 2024 large insurers continue to prefer certified systems integrators for implementation and change management, citing reduced project risk and faster go-live. Leading SIs command premium rates and can sway vendor selection through referenceable enterprise deployments. Dependence on a few elite partners increases supplier bargaining power and pricing pressure. Expanding a mid-tier partner ecosystem reduces concentration risk and improves negotiating leverage.

Third‑party data and services

Integrations with identity, medical, payroll and risk providers (KYC, EHR, credit, payroll APIs) are critical for FINEOS and often carry per-call fees and restrictive SLAs; large platform partners commonly impose annual certification and compliance costs running into tens of thousands of dollars (2024 industry practice). Switching vendors is feasible but requires re-certification and regression testing, increasing time-to-market. Volume pricing and standardized connectors (FHIR, OAuth, ISO 20022) narrow supplier leverage.

Regulatory/compliance tooling

Concentrated cloud suppliers exert pricing leverage; dev scarcity and audits raise OPEX

Supplier power is high: AWS 32%, Azure 22%, Google 11% IaaS/PaaS share (2024 Synergy), giving pricing and roadmap leverage. SI concentration, developer scarcity (BLS 22% dev growth 2020–2030) and integration/certification fees raise costs; payment fees ≈1.5–3% and SOC/ISO audits $50k–$200k/yr add OPEX. Multicloud and internal build reduce but not eliminate leverage.

| Factor | 2024 Data |

|---|---|

| Cloud share | AWS 32% / Azure 22% / GCP 11% |

| Payment & audits | Fees 1.5–3% / SOC $50k–$200k |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power and market entry risks tailored exclusively for FINEOS. Identifies disruptive threats, substitutes and protective market dynamics to inform pricing, strategy and investor materials.

Clear one-sheet FINEOS Porter's Five Forces that instantly visualizes competitive pressure via a spider chart and customizable scores—perfect for fast boardroom decisions and stress-testing scenarios without complex tools.

Customers Bargaining Power

Concentrated enterprise buyers

Large carriers and TPAs drive demand for FINEOS and run formal RFPs. In 2024 the top five US carriers accounted for roughly 50% of commercial enrollment, giving them leverage to extract aggressive discounts, bespoke SLAs and contractual protections. Referenceability and marquee wins push vendors to concede tougher terms. Mid-market buyers wield less power but still actively price-shop.

High switching costs yet tough negotiations

Migrations from legacy cores are costly, risky, and typically span 18–36 months with project budgets commonly exceeding $10m, creating high switching costs that increase buyer stickiness. Despite this, buyers leverage competitive bids to extract price discounts and roadmap concessions, with procurement-led RFPs reported in 70% of enterprise deals in 2024. Exit clauses, data portability requirements, and modular adoption reduce lock-in. Vendors must quantify TCO and demonstrable risk reduction to secure concessions.

Feature depth and configurability demands

Insurers require rich L/A&H product configurability, flexible billing and complex claims handling, driving requests for accelerators and no-code tooling that FINEOS emphasized in 2024 product materials. Buyers increasingly push for rapid delivery without custom code, citing time-to-market and implementation cost pressures. Clear out-of-the-box coverage and prebuilt accelerators reduce buyer leverage by shortening procurement cycles and lowering customization spend.

Integration and openness

Open APIs, eventing, and interoperability with CRM, HRIS, and analytics are mandatory for FINEOS buyers; in 2024 surveys showed more than 50% of enterprise purchasers reject proprietary lock-in and require standards-based interfaces. Data access, latency, and real-time sync SLAs become explicit negotiation levers, while strong partner ecosystems blunt buyer power and raise switching costs.

- Open APIs required

- Buyers resist lock-in

- SLAs (latency, sync) as leverage

- Ecosystem reduces buyer power

Outcome and value-based purchasing

Procurement in 2024 ties payment to KPIs such as FNOL cycle time, straight-through processing and cost-to-serve, shifting implementation risk to vendors and hardening price ceilings. Proofs-of-value and ROI models are now prerequisites; demonstrable outcomes can flip buyer pressure into upsell opportunities.

- KPIs: FNOL cycle, STP, cost-to-serve

- Must: PoV, ROI models

- Effect: risk shift, price ceilings, upsell

Procurement-led RFPs, Open APIs and SLAs drive steep vendor discounts and pricing caps

Large US carriers (~50% commercial enrollment in 2024) and TPAs hold strong leverage via RFPs; buyers extract steep discounts. Migrations (18–36 months; typical budgets >$10m) increase stickiness, yet 70% of enterprise deals used procurement-led RFPs in 2024. Open APIs, SLAs and PoV/KPI-linked payments (FNOL, STP) shift risk to vendors and cap pricing.

| Metric | 2024 |

|---|---|

| Top-5 carrier share | ~50% |

| Migration timeline | 18–36 mo |

| Procurement-led deals | 70% |

| Typical project budget | >$10m |

Same Document Delivered

FINEOS Porter's Five Forces Analysis

This preview is the exact FINEOS Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The file shown is fully formatted, professionally written, and ready for download and use the moment you buy. No changes or setup required.