Finning Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

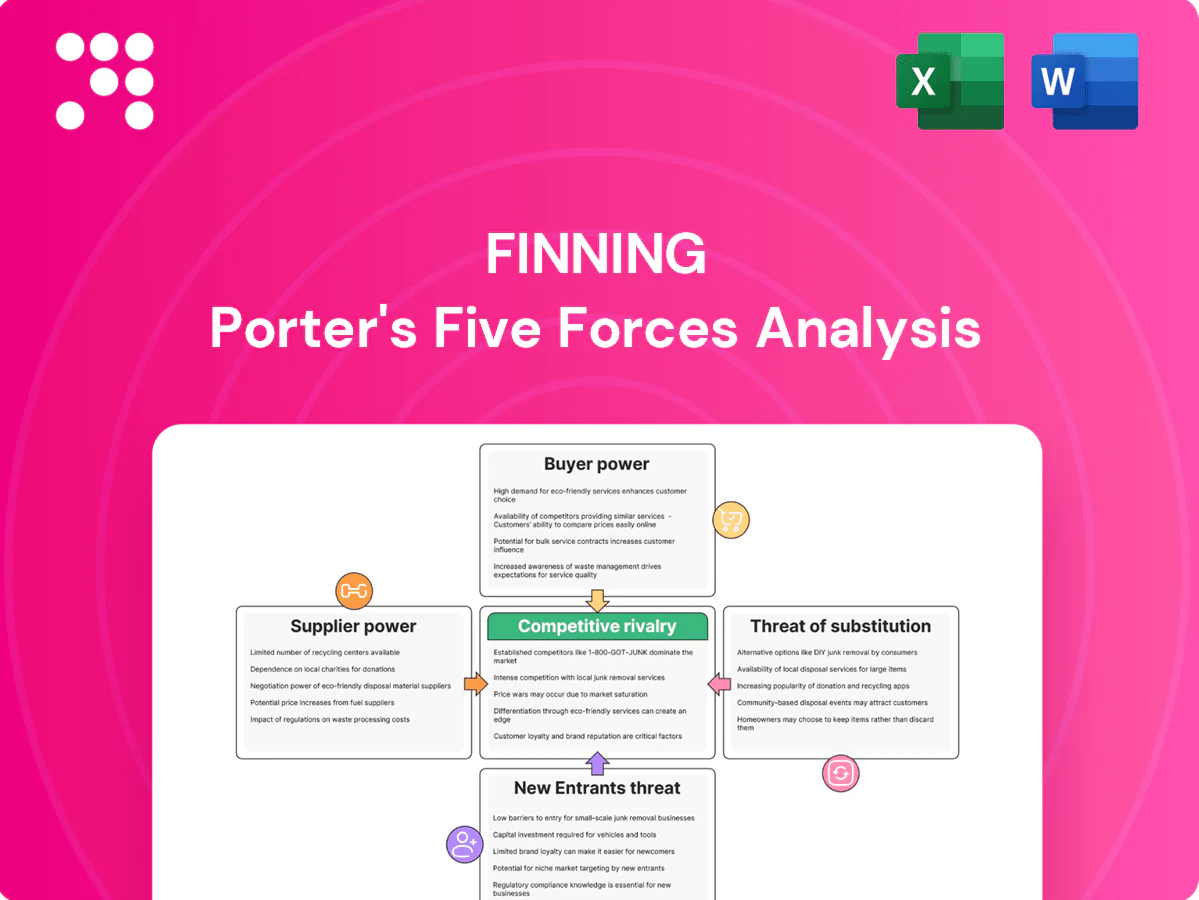

Finning’s Porter's Five Forces highlights supplier concentration, aftermarket service leverage, and moderate threat of substitutes amid heavy capital barriers; buyer bargaining and rivalry vary by geography and product mix. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Finning’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Caterpillar

Finning is highly dependent on Caterpillar as its primary OEM, giving CAT outsized leverage over pricing, allocation and product roadmaps through exclusive dealer agreements that lock Finning into OEM terms. Any supply disruption or strategic policy change at CAT directly constrains equipment availability and compresses Finning’s margins. CAT’s entrenched brand and IP create high switching barriers, limiting Finning’s negotiating flexibility and strategic alternatives.

Limited Alternative OEMs

There are effectively five dominant global heavy-equipment OEMs—Caterpillar, Komatsu, Volvo CE, Hitachi and John Deere—limiting equivalent alternatives for Finning and constraining sourcing options. Many OEMs stipulate exclusive territories, blocking multi-brand hedging. Proprietary platforms lack substitutable parts, increasing OEM supplier power and strengthening their bargaining positions in negotiations.

Parts and Technology Control

Caterpillar in 2024 retained tight control over parts catalogs, software, telematics and diagnostic tools, anchoring aftermarket work to OEM standards. Its proprietary machine-health ecosystems link service outcomes and data access to Cat-approved channels. Access fees, tooling mandates and certification rules raise Finning’s operating and compliance costs. Rapid supplier-driven tech cycles force higher inventory turnover and continuous training investment.

Volume and Territory Offsets

Finning’s scale across Canada, UK/Ireland and South America makes it the world’s largest Caterpillar dealer as of 2024, providing meaningful volume leverage and operational importance to CAT. Geographic exclusivity and long-term relationships help secure allocations and rebate arrangements, and performance-based incentives can partially rebalance supplier bargaining power. These benefits are contingent on meeting OEM KPIs and regional performance thresholds.

- Global reach: three territories (Canada, UK/Ireland, South America) — largest CAT dealer in 2024

- Commercial levers: allocations, rebates, exclusivity

- Counterbalance: performance-based incentives tied to OEM KPIs

Broader Supply Chain Exposure

- Supplier concentration: OEM specs limit alternatives

- Inventory: CAD 1.9bn (FY2023) reflects parts exposure

- Upstream power: commodities, freight, geopolitics

- Margin risk: engine/electronics tightness compresses dealer margins

Concentrated OEM power squeezes dealer margins; inventory exposure CAD 1.9bn

Finning's supplier power is concentrated: Caterpillar is the primary OEM, giving CAT pricing, allocation and tech leverage that constrains margins and alternatives. Inventory exposure (CAD 1.9bn FY2023) and OEM exclusivity limit multi-sourcing while five global OEMs restrict substitutes. Finning's scale (world's largest CAT dealer in 2024) provides some volume leverage and rebate/incentive offsets.

| Metric | Value |

|---|---|

| Primary OEM | Caterpillar |

| Inventory | CAD 1.9bn (FY2023) |

| Dealer status | World's largest CAT dealer (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Finning that evaluates competitive rivalry, supplier and buyer power, barriers to entry, and threat of substitutes, identifying disruptive forces and strategic levers affecting market share and profitability. Fully editable for inclusion in investor materials, strategy decks, or academic projects.

Concise one-sheet Finning Porter’s Five Forces that turns complex competitive analysis into quick decisions—customize pressures, swap data, and export to slides instantly.

Customers Bargaining Power

Large Industrial Customers

Mines, construction firms and utilities are sophisticated buyers with professional procurement teams that leverage scale, competitive tenders and lifecycle-cost analyses to drive supplier margins down. Project-driven lumpiness increases price sensitivity and can shift orders between quarters, while multi-year framework agreements (typically 2–5 years) trade lower unit price for volume certainty. Large customers therefore exert high bargaining power over Finning.

High Switching Costs

Installed fleets and operator familiarity with Cat create strong lock-in, reinforced by proprietary parts and service networks tied to hundreds of thousands of Caterpillar machines globally (2024). Telematics, warranties and consolidated service histories further bind customers to CAT platforms, making cross-brand moves costly. Switching risks downtime, retraining and logistics expenses, so these frictions materially temper buyer power in the aftermarket.

Rental vs Purchase Options

Availability of rental and used equipment gives customers tactical flexibility, letting them match capacity to short-term project needs rather than committing capex.

Rental dampens capital purchases for Finning and introduces rate competition and utilization risk as idle fleet depresses margins.

Customers can arbitrage between rent, lease, and buy across cycles, increasing leverage to negotiate lower upfront pricing and more favorable contract terms.

Cyclical Demand Volatility

End-markets for Finning are commodity- and macro-sensitive, with IMF projecting world GDP growth at about 3.0% in 2024, driving swing in equipment demand; downturns see buyers extract deeper discounts, extended payment terms and service concessions, while upcycles and scarcity restore pricing leverage to Finning; procurement timing materially alters negotiating dynamics.

- Downturn: heavier discounting, longer terms

- Upcycle: scarcity increases Finning pricing power

- Procurement timing = key negotiating lever

Lifecycle Value Expectations

Customers now judge lifecycle value by total cost of ownership—fuel efficiency, uptime, resale and service response—with SLAs and predictive maintenance considered table stakes; industry studies in 2024 report predictive maintenance can cut maintenance costs by 10–40% and materially improve uptime, forcing buyers to scrutinize price versus measurable productivity gains. Finning must justify any premium with quantified output and uptime metrics.

- TOC focus: fuel, uptime, resale, service

- SLAs & predictive maintenance: table stakes (2024: maintenance savings 10–40%)

- Data transparency elevates price/value scrutiny

- Finning must prove premiums via measurable productivity/outcome metrics

Buyers press price; OEM telematics lock-in limits switching; predictive saves 10–40%

Large, sophisticated buyers (frameworks 2–5y) exert high price leverage, but operator lock-in to Cat parts/services and telematics (hundreds of thousands Cat machines globally, 2024) reduces aftermarket switching. Rental/used markets and cyclical demand (IMF 2024 world GDP ~3.0%) boost buyer tactics. Predictive maintenance cuts costs 10–40% (2024), forcing value-based pricing.

| Metric | 2024 |

|---|---|

| World GDP growth | ~3.0% |

| Predictive maintenance savings | 10–40% |

| Framework length | 2–5 years |

Preview the Actual Deliverable

Finning Porter's Five Forces Analysis

This preview is the exact Finning Porter's Five Forces Analysis you'll receive—no placeholders or samples. The full, professionally formatted document is ready for immediate download and use upon purchase. It contains actionable insights on competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications.

Go Beyond the Preview—Access the Full Strategic Report

Finning’s Porter's Five Forces highlights supplier concentration, aftermarket service leverage, and moderate threat of substitutes amid heavy capital barriers; buyer bargaining and rivalry vary by geography and product mix. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Finning’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Caterpillar

Finning is highly dependent on Caterpillar as its primary OEM, giving CAT outsized leverage over pricing, allocation and product roadmaps through exclusive dealer agreements that lock Finning into OEM terms. Any supply disruption or strategic policy change at CAT directly constrains equipment availability and compresses Finning’s margins. CAT’s entrenched brand and IP create high switching barriers, limiting Finning’s negotiating flexibility and strategic alternatives.

Limited Alternative OEMs

There are effectively five dominant global heavy-equipment OEMs—Caterpillar, Komatsu, Volvo CE, Hitachi and John Deere—limiting equivalent alternatives for Finning and constraining sourcing options. Many OEMs stipulate exclusive territories, blocking multi-brand hedging. Proprietary platforms lack substitutable parts, increasing OEM supplier power and strengthening their bargaining positions in negotiations.

Parts and Technology Control

Caterpillar in 2024 retained tight control over parts catalogs, software, telematics and diagnostic tools, anchoring aftermarket work to OEM standards. Its proprietary machine-health ecosystems link service outcomes and data access to Cat-approved channels. Access fees, tooling mandates and certification rules raise Finning’s operating and compliance costs. Rapid supplier-driven tech cycles force higher inventory turnover and continuous training investment.

Volume and Territory Offsets

Finning’s scale across Canada, UK/Ireland and South America makes it the world’s largest Caterpillar dealer as of 2024, providing meaningful volume leverage and operational importance to CAT. Geographic exclusivity and long-term relationships help secure allocations and rebate arrangements, and performance-based incentives can partially rebalance supplier bargaining power. These benefits are contingent on meeting OEM KPIs and regional performance thresholds.

- Global reach: three territories (Canada, UK/Ireland, South America) — largest CAT dealer in 2024

- Commercial levers: allocations, rebates, exclusivity

- Counterbalance: performance-based incentives tied to OEM KPIs

Broader Supply Chain Exposure

- Supplier concentration: OEM specs limit alternatives

- Inventory: CAD 1.9bn (FY2023) reflects parts exposure

- Upstream power: commodities, freight, geopolitics

- Margin risk: engine/electronics tightness compresses dealer margins

Concentrated OEM power squeezes dealer margins; inventory exposure CAD 1.9bn

Finning's supplier power is concentrated: Caterpillar is the primary OEM, giving CAT pricing, allocation and tech leverage that constrains margins and alternatives. Inventory exposure (CAD 1.9bn FY2023) and OEM exclusivity limit multi-sourcing while five global OEMs restrict substitutes. Finning's scale (world's largest CAT dealer in 2024) provides some volume leverage and rebate/incentive offsets.

| Metric | Value |

|---|---|

| Primary OEM | Caterpillar |

| Inventory | CAD 1.9bn (FY2023) |

| Dealer status | World's largest CAT dealer (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Finning that evaluates competitive rivalry, supplier and buyer power, barriers to entry, and threat of substitutes, identifying disruptive forces and strategic levers affecting market share and profitability. Fully editable for inclusion in investor materials, strategy decks, or academic projects.

Concise one-sheet Finning Porter’s Five Forces that turns complex competitive analysis into quick decisions—customize pressures, swap data, and export to slides instantly.

Customers Bargaining Power

Large Industrial Customers

Mines, construction firms and utilities are sophisticated buyers with professional procurement teams that leverage scale, competitive tenders and lifecycle-cost analyses to drive supplier margins down. Project-driven lumpiness increases price sensitivity and can shift orders between quarters, while multi-year framework agreements (typically 2–5 years) trade lower unit price for volume certainty. Large customers therefore exert high bargaining power over Finning.

High Switching Costs

Installed fleets and operator familiarity with Cat create strong lock-in, reinforced by proprietary parts and service networks tied to hundreds of thousands of Caterpillar machines globally (2024). Telematics, warranties and consolidated service histories further bind customers to CAT platforms, making cross-brand moves costly. Switching risks downtime, retraining and logistics expenses, so these frictions materially temper buyer power in the aftermarket.

Rental vs Purchase Options

Availability of rental and used equipment gives customers tactical flexibility, letting them match capacity to short-term project needs rather than committing capex.

Rental dampens capital purchases for Finning and introduces rate competition and utilization risk as idle fleet depresses margins.

Customers can arbitrage between rent, lease, and buy across cycles, increasing leverage to negotiate lower upfront pricing and more favorable contract terms.

Cyclical Demand Volatility

End-markets for Finning are commodity- and macro-sensitive, with IMF projecting world GDP growth at about 3.0% in 2024, driving swing in equipment demand; downturns see buyers extract deeper discounts, extended payment terms and service concessions, while upcycles and scarcity restore pricing leverage to Finning; procurement timing materially alters negotiating dynamics.

- Downturn: heavier discounting, longer terms

- Upcycle: scarcity increases Finning pricing power

- Procurement timing = key negotiating lever

Lifecycle Value Expectations

Customers now judge lifecycle value by total cost of ownership—fuel efficiency, uptime, resale and service response—with SLAs and predictive maintenance considered table stakes; industry studies in 2024 report predictive maintenance can cut maintenance costs by 10–40% and materially improve uptime, forcing buyers to scrutinize price versus measurable productivity gains. Finning must justify any premium with quantified output and uptime metrics.

- TOC focus: fuel, uptime, resale, service

- SLAs & predictive maintenance: table stakes (2024: maintenance savings 10–40%)

- Data transparency elevates price/value scrutiny

- Finning must prove premiums via measurable productivity/outcome metrics

Buyers press price; OEM telematics lock-in limits switching; predictive saves 10–40%

Large, sophisticated buyers (frameworks 2–5y) exert high price leverage, but operator lock-in to Cat parts/services and telematics (hundreds of thousands Cat machines globally, 2024) reduces aftermarket switching. Rental/used markets and cyclical demand (IMF 2024 world GDP ~3.0%) boost buyer tactics. Predictive maintenance cuts costs 10–40% (2024), forcing value-based pricing.

| Metric | 2024 |

|---|---|

| World GDP growth | ~3.0% |

| Predictive maintenance savings | 10–40% |

| Framework length | 2–5 years |

Preview the Actual Deliverable

Finning Porter's Five Forces Analysis

This preview is the exact Finning Porter's Five Forces Analysis you'll receive—no placeholders or samples. The full, professionally formatted document is ready for immediate download and use upon purchase. It contains actionable insights on competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications.

Description

Go Beyond the Preview—Access the Full Strategic Report

Finning’s Porter's Five Forces highlights supplier concentration, aftermarket service leverage, and moderate threat of substitutes amid heavy capital barriers; buyer bargaining and rivalry vary by geography and product mix. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Finning’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Caterpillar

Finning is highly dependent on Caterpillar as its primary OEM, giving CAT outsized leverage over pricing, allocation and product roadmaps through exclusive dealer agreements that lock Finning into OEM terms. Any supply disruption or strategic policy change at CAT directly constrains equipment availability and compresses Finning’s margins. CAT’s entrenched brand and IP create high switching barriers, limiting Finning’s negotiating flexibility and strategic alternatives.

Limited Alternative OEMs

There are effectively five dominant global heavy-equipment OEMs—Caterpillar, Komatsu, Volvo CE, Hitachi and John Deere—limiting equivalent alternatives for Finning and constraining sourcing options. Many OEMs stipulate exclusive territories, blocking multi-brand hedging. Proprietary platforms lack substitutable parts, increasing OEM supplier power and strengthening their bargaining positions in negotiations.

Parts and Technology Control

Caterpillar in 2024 retained tight control over parts catalogs, software, telematics and diagnostic tools, anchoring aftermarket work to OEM standards. Its proprietary machine-health ecosystems link service outcomes and data access to Cat-approved channels. Access fees, tooling mandates and certification rules raise Finning’s operating and compliance costs. Rapid supplier-driven tech cycles force higher inventory turnover and continuous training investment.

Volume and Territory Offsets

Finning’s scale across Canada, UK/Ireland and South America makes it the world’s largest Caterpillar dealer as of 2024, providing meaningful volume leverage and operational importance to CAT. Geographic exclusivity and long-term relationships help secure allocations and rebate arrangements, and performance-based incentives can partially rebalance supplier bargaining power. These benefits are contingent on meeting OEM KPIs and regional performance thresholds.

- Global reach: three territories (Canada, UK/Ireland, South America) — largest CAT dealer in 2024

- Commercial levers: allocations, rebates, exclusivity

- Counterbalance: performance-based incentives tied to OEM KPIs

Broader Supply Chain Exposure

- Supplier concentration: OEM specs limit alternatives

- Inventory: CAD 1.9bn (FY2023) reflects parts exposure

- Upstream power: commodities, freight, geopolitics

- Margin risk: engine/electronics tightness compresses dealer margins

Concentrated OEM power squeezes dealer margins; inventory exposure CAD 1.9bn

Finning's supplier power is concentrated: Caterpillar is the primary OEM, giving CAT pricing, allocation and tech leverage that constrains margins and alternatives. Inventory exposure (CAD 1.9bn FY2023) and OEM exclusivity limit multi-sourcing while five global OEMs restrict substitutes. Finning's scale (world's largest CAT dealer in 2024) provides some volume leverage and rebate/incentive offsets.

| Metric | Value |

|---|---|

| Primary OEM | Caterpillar |

| Inventory | CAD 1.9bn (FY2023) |

| Dealer status | World's largest CAT dealer (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Finning that evaluates competitive rivalry, supplier and buyer power, barriers to entry, and threat of substitutes, identifying disruptive forces and strategic levers affecting market share and profitability. Fully editable for inclusion in investor materials, strategy decks, or academic projects.

Concise one-sheet Finning Porter’s Five Forces that turns complex competitive analysis into quick decisions—customize pressures, swap data, and export to slides instantly.

Customers Bargaining Power

Large Industrial Customers

Mines, construction firms and utilities are sophisticated buyers with professional procurement teams that leverage scale, competitive tenders and lifecycle-cost analyses to drive supplier margins down. Project-driven lumpiness increases price sensitivity and can shift orders between quarters, while multi-year framework agreements (typically 2–5 years) trade lower unit price for volume certainty. Large customers therefore exert high bargaining power over Finning.

High Switching Costs

Installed fleets and operator familiarity with Cat create strong lock-in, reinforced by proprietary parts and service networks tied to hundreds of thousands of Caterpillar machines globally (2024). Telematics, warranties and consolidated service histories further bind customers to CAT platforms, making cross-brand moves costly. Switching risks downtime, retraining and logistics expenses, so these frictions materially temper buyer power in the aftermarket.

Rental vs Purchase Options

Availability of rental and used equipment gives customers tactical flexibility, letting them match capacity to short-term project needs rather than committing capex.

Rental dampens capital purchases for Finning and introduces rate competition and utilization risk as idle fleet depresses margins.

Customers can arbitrage between rent, lease, and buy across cycles, increasing leverage to negotiate lower upfront pricing and more favorable contract terms.

Cyclical Demand Volatility

End-markets for Finning are commodity- and macro-sensitive, with IMF projecting world GDP growth at about 3.0% in 2024, driving swing in equipment demand; downturns see buyers extract deeper discounts, extended payment terms and service concessions, while upcycles and scarcity restore pricing leverage to Finning; procurement timing materially alters negotiating dynamics.

- Downturn: heavier discounting, longer terms

- Upcycle: scarcity increases Finning pricing power

- Procurement timing = key negotiating lever

Lifecycle Value Expectations

Customers now judge lifecycle value by total cost of ownership—fuel efficiency, uptime, resale and service response—with SLAs and predictive maintenance considered table stakes; industry studies in 2024 report predictive maintenance can cut maintenance costs by 10–40% and materially improve uptime, forcing buyers to scrutinize price versus measurable productivity gains. Finning must justify any premium with quantified output and uptime metrics.

- TOC focus: fuel, uptime, resale, service

- SLAs & predictive maintenance: table stakes (2024: maintenance savings 10–40%)

- Data transparency elevates price/value scrutiny

- Finning must prove premiums via measurable productivity/outcome metrics

Buyers press price; OEM telematics lock-in limits switching; predictive saves 10–40%

Large, sophisticated buyers (frameworks 2–5y) exert high price leverage, but operator lock-in to Cat parts/services and telematics (hundreds of thousands Cat machines globally, 2024) reduces aftermarket switching. Rental/used markets and cyclical demand (IMF 2024 world GDP ~3.0%) boost buyer tactics. Predictive maintenance cuts costs 10–40% (2024), forcing value-based pricing.

| Metric | 2024 |

|---|---|

| World GDP growth | ~3.0% |

| Predictive maintenance savings | 10–40% |

| Framework length | 2–5 years |

Preview the Actual Deliverable

Finning Porter's Five Forces Analysis

This preview is the exact Finning Porter's Five Forces Analysis you'll receive—no placeholders or samples. The full, professionally formatted document is ready for immediate download and use upon purchase. It contains actionable insights on competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications.