First Bank PESTLE Analysis

Skip the Research. Get the Strategy.

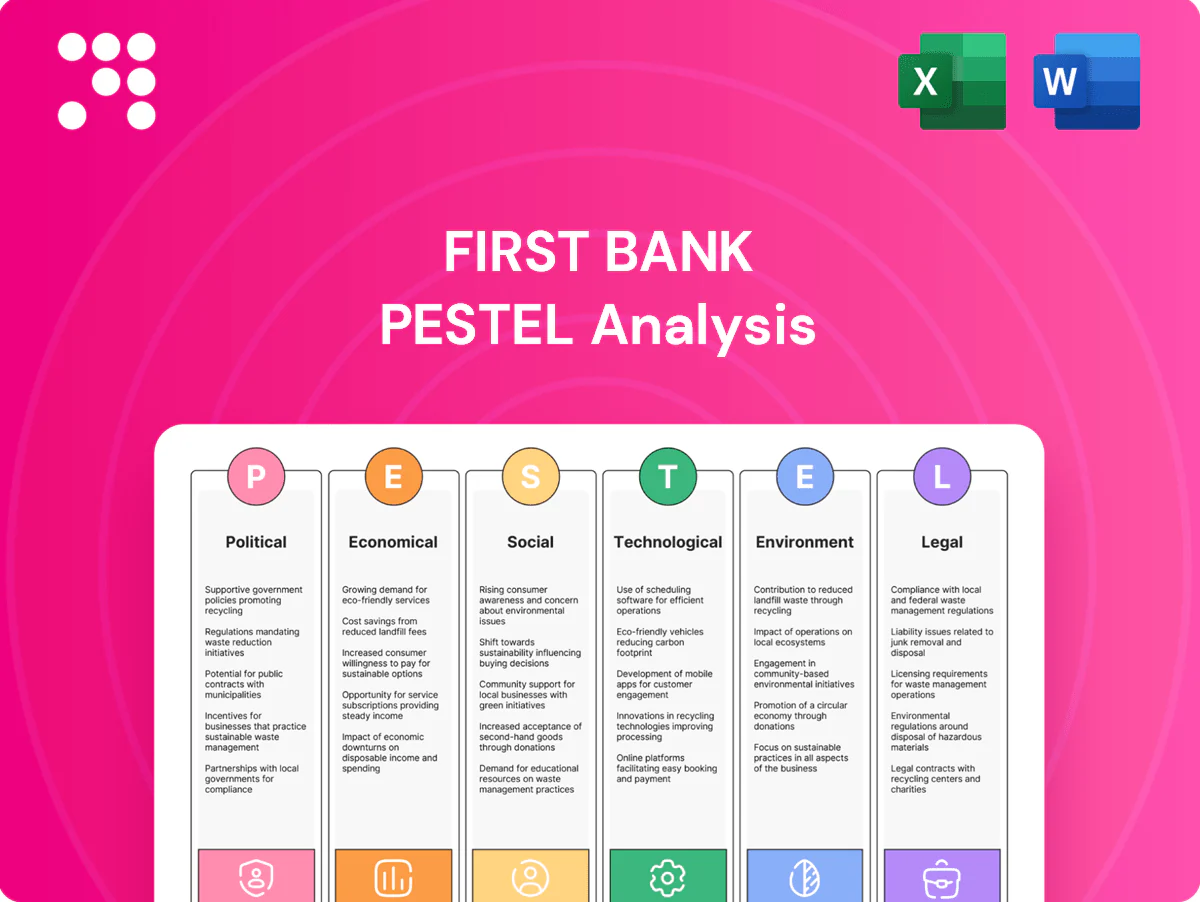

Gain a strategic edge with our PESTLE Analysis of First Bank. Explore how political, economic, social, technological, legal and environmental forces shape its risk and opportunity profile. Buy the full report to access actionable insights, data tables, and ready-to-use slides for investment or strategy decisions.

Political factors

Regulatory policy direction

Regulatory priorities—consumer protection, fair lending, AML—drive FirstBank product design and pushed industry compliance spend to roughly $74.5 billion in 2023, raising unit costs on mortgages, cards and SMB loans. Post‑election shifts can tighten or loosen mortgage, credit card and small‑business constraints; FirstBank must track federal and state rulemaking calendars and comment periods to anticipate change. Proactive engagement reduces disruption and speeds approvals.

Government-backed lending

Government-backed programs like SBA 7(a) (maximum loan size $5,000,000) and GSE support (conforming limit $726,200 in most areas) boost loan demand and shift credit risk to guarantors. Participation can expand originations and fee income but increases documentation, compliance and audit burden. Annual FHFA and budget-driven rule changes can quickly alter caps and pricing. Diversifying exposure limits program-driven volatility.

Local community priorities

As a community-focused bank, municipal partnerships and local development agendas directly influence branch placement and outreach, affecting retail deposit catchment and SME lending pipelines. The $1.2 trillion Bipartisan Infrastructure Law elevates municipal projects that can boost deposits and commercial lending. Political support for financial inclusion, including the CDFI Funds' ~$3 billion ARP allocation, creates grant and CRA-related opportunities and strengthens market access and reputation.

Geopolitical stability

Geopolitical instability raises funding costs, reduces risk appetite, and increases FX-linked client demand even for domestic banks; US 10-year yields stood around 4.1% in mid-2025, reflecting tighter global funding. Market volatility in 2024–25 forced higher capital and liquidity buffers; sanctions regimes require rigorous screening and controls, and preparedness limits operational and reputational loss.

- Funding costs: higher global yields (~4.1% US 10y)

- Risk appetite: reduced, more conservative lending

- Liquidity: raised capital/liquidity buffers in 2024–25

- Compliance: strict sanctions screening lowers reputational risk

Public trust and oversight

Political scrutiny intensified after the 2023 US bank failures (Silicon Valley Bank, Signature, First Republic), pushing regulators to emphasize stress tests again and the Federal Reserve's annual Dodd-Frank exercises covering 23 firms in 2024. Transparent governance and increased community lending improve relations with policymakers; swift incident response reduces enforcement and reputational risk, while consistent messaging preserves franchise value.

- Scrutiny: 2023 bank failures x3

- Stress-tests: 23 banks in 2024

- Mitigation: swift response lowers enforcement risk

- Reputation: governance + community investment

Regulation, AML and fair-lending raise costs; US 10y at ~4.1%

Regulatory focus on consumer protection, AML and fair lending (industry compliance spend $74.5B in 2023) raises unit costs; rule changes post‑election can quickly affect mortgages, cards and SMB lending. Government programs (SBA 7(a) max $5,000,000; conforming limit $726,200) expand originations but add compliance burden. Geopolitical stress lifted US 10y to ~4.1% mid‑2025, increasing funding costs and conservative lending; 2023 saw 3 bank failures and 23 banks underwent stress tests in 2024.

| Metric | Value/Year |

|---|---|

| Compliance spend | $74.5B (2023) |

| US 10y yield | ~4.1% (mid‑2025) |

| SBA 7(a) cap | $5,000,000 |

| Conforming loan limit | $726,200 |

| Infra law | $1.2T |

| CDFI ARP | ~$3B |

| Bank failures | 3 (2023) |

| Stress tests | 23 banks (2024) |

What is included in the product

Explores how macro-environmental forces uniquely impact First Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each category supported by relevant data and current trends. Designed for executives and investors, the analysis offers forward-looking insights to inform strategy, risk management, and scenario planning.

A concise, visually segmented PESTLE summary of First Bank that’s drop‑in ready for slides or reports, easily shareable for quick alignment across teams and ideal for clarifying external risks during planning sessions.

Economic factors

Interest rate cycles

Net interest margin depends on rate levels, pace and deposit betas; with the US federal funds rate at 5.25–5.50% in mid-2025 banks reported industry NIMs near 3.0–3.5%, but rapid hikes or cuts can stress funding and compress spreads as deposit betas rise. Balance-sheet hedging and fast product repricing are critical to protect margin. Scenario planning aligns growth with risk appetite and liquidity stress tests.

Credit cycle dynamics

Employment, rising real wages and higher consumer default rates drive loan demand and provisions; US unemployment hovered near 3.7% in 2024 while average hourly earnings grew ~4% year-on-year, pressuring credit demand and loss-readiness. Mortgages and SME lending remain highly sensitive to housing and business confidence as 30-year mortgage rates averaged near 6.8% in 2024. Prudent underwriting, sector concentration limits and early-warning analytics materially reduce cyclicality and improve workout recoveries.

Regional economic health

Local industries and demographics drive deposit growth and credit quality; regional GDP grew about 2.5% in 2024 while unemployment averaged near 3.7%, influencing loan demand and delinquencies. Targeted outreach to resilient sectors such as healthcare and logistics helps stabilize NIMs and earnings. Community development lending expands housing and SME credit, catalyzing growth. Geographic diversification tempers local shocks and concentration risk.

Inflation and costs

Inflation pressures noninterest expenses and clients’ debt‑service capacity; Nigeria headline inflation was 22.8% in December 2023, intensifying credit risk and provisioning needs. Pricing discipline and fee optimization help protect ROA while efficiency programs and digital adoption lower unit costs. Stress tests should explicitly model stagflation scenarios and higher long‑run rates.

- Inflation impact on expenses and NPLs

- Pricing and fee optimization to protect ROA

- Digital adoption reduces unit costs

- Stagflation scenarios in stress tests

Capital and liquidity conditions

Market funding spreads and deposit flows materially affect First Bank’s growth trajectory as wider spreads raise funding costs while deposit retention supports lending; Basel III liquidity ratios set the 100% regulatory floor for LCR and NSFR. Strong LCR/NSFR and contingency funding lines bolster resilience, while retained earnings in a private structure fund measured organic expansion; transparent metrics (ratios, stress tests) reassure stakeholders.

- Regulatory floor: LCR/NSFR 100%

- Funding spreads drive loan pricing

- Retained earnings fund organic growth

- Transparent metrics build stakeholder confidence

Regulation, AML and fair-lending raise costs; US 10y at ~4.1%

Net interest margin sensitive to fed funds 5.25–5.50% (mid‑2025) with industry NIMs ~3.0–3.5%; unemployment ~3.7% and avg hourly earnings +4% drive loan demand; Nigeria inflation 22.8% (Dec 2023) and regional GDP ~2.5% (2024) pressure provisioning and costs.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| NIM | 3.0–3.5% |

| Unemployment | 3.7% |

What You See Is What You Get

First Bank PESTLE Analysis

The preview shown here is the exact First Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; this is the final file. After checkout you’ll instantly download the identical document as displayed.

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE Analysis of First Bank. Explore how political, economic, social, technological, legal and environmental forces shape its risk and opportunity profile. Buy the full report to access actionable insights, data tables, and ready-to-use slides for investment or strategy decisions.

Political factors

Regulatory policy direction

Regulatory priorities—consumer protection, fair lending, AML—drive FirstBank product design and pushed industry compliance spend to roughly $74.5 billion in 2023, raising unit costs on mortgages, cards and SMB loans. Post‑election shifts can tighten or loosen mortgage, credit card and small‑business constraints; FirstBank must track federal and state rulemaking calendars and comment periods to anticipate change. Proactive engagement reduces disruption and speeds approvals.

Government-backed lending

Government-backed programs like SBA 7(a) (maximum loan size $5,000,000) and GSE support (conforming limit $726,200 in most areas) boost loan demand and shift credit risk to guarantors. Participation can expand originations and fee income but increases documentation, compliance and audit burden. Annual FHFA and budget-driven rule changes can quickly alter caps and pricing. Diversifying exposure limits program-driven volatility.

Local community priorities

As a community-focused bank, municipal partnerships and local development agendas directly influence branch placement and outreach, affecting retail deposit catchment and SME lending pipelines. The $1.2 trillion Bipartisan Infrastructure Law elevates municipal projects that can boost deposits and commercial lending. Political support for financial inclusion, including the CDFI Funds' ~$3 billion ARP allocation, creates grant and CRA-related opportunities and strengthens market access and reputation.

Geopolitical stability

Geopolitical instability raises funding costs, reduces risk appetite, and increases FX-linked client demand even for domestic banks; US 10-year yields stood around 4.1% in mid-2025, reflecting tighter global funding. Market volatility in 2024–25 forced higher capital and liquidity buffers; sanctions regimes require rigorous screening and controls, and preparedness limits operational and reputational loss.

- Funding costs: higher global yields (~4.1% US 10y)

- Risk appetite: reduced, more conservative lending

- Liquidity: raised capital/liquidity buffers in 2024–25

- Compliance: strict sanctions screening lowers reputational risk

Public trust and oversight

Political scrutiny intensified after the 2023 US bank failures (Silicon Valley Bank, Signature, First Republic), pushing regulators to emphasize stress tests again and the Federal Reserve's annual Dodd-Frank exercises covering 23 firms in 2024. Transparent governance and increased community lending improve relations with policymakers; swift incident response reduces enforcement and reputational risk, while consistent messaging preserves franchise value.

- Scrutiny: 2023 bank failures x3

- Stress-tests: 23 banks in 2024

- Mitigation: swift response lowers enforcement risk

- Reputation: governance + community investment

Regulation, AML and fair-lending raise costs; US 10y at ~4.1%

Regulatory focus on consumer protection, AML and fair lending (industry compliance spend $74.5B in 2023) raises unit costs; rule changes post‑election can quickly affect mortgages, cards and SMB lending. Government programs (SBA 7(a) max $5,000,000; conforming limit $726,200) expand originations but add compliance burden. Geopolitical stress lifted US 10y to ~4.1% mid‑2025, increasing funding costs and conservative lending; 2023 saw 3 bank failures and 23 banks underwent stress tests in 2024.

| Metric | Value/Year |

|---|---|

| Compliance spend | $74.5B (2023) |

| US 10y yield | ~4.1% (mid‑2025) |

| SBA 7(a) cap | $5,000,000 |

| Conforming loan limit | $726,200 |

| Infra law | $1.2T |

| CDFI ARP | ~$3B |

| Bank failures | 3 (2023) |

| Stress tests | 23 banks (2024) |

What is included in the product

Explores how macro-environmental forces uniquely impact First Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each category supported by relevant data and current trends. Designed for executives and investors, the analysis offers forward-looking insights to inform strategy, risk management, and scenario planning.

A concise, visually segmented PESTLE summary of First Bank that’s drop‑in ready for slides or reports, easily shareable for quick alignment across teams and ideal for clarifying external risks during planning sessions.

Economic factors

Interest rate cycles

Net interest margin depends on rate levels, pace and deposit betas; with the US federal funds rate at 5.25–5.50% in mid-2025 banks reported industry NIMs near 3.0–3.5%, but rapid hikes or cuts can stress funding and compress spreads as deposit betas rise. Balance-sheet hedging and fast product repricing are critical to protect margin. Scenario planning aligns growth with risk appetite and liquidity stress tests.

Credit cycle dynamics

Employment, rising real wages and higher consumer default rates drive loan demand and provisions; US unemployment hovered near 3.7% in 2024 while average hourly earnings grew ~4% year-on-year, pressuring credit demand and loss-readiness. Mortgages and SME lending remain highly sensitive to housing and business confidence as 30-year mortgage rates averaged near 6.8% in 2024. Prudent underwriting, sector concentration limits and early-warning analytics materially reduce cyclicality and improve workout recoveries.

Regional economic health

Local industries and demographics drive deposit growth and credit quality; regional GDP grew about 2.5% in 2024 while unemployment averaged near 3.7%, influencing loan demand and delinquencies. Targeted outreach to resilient sectors such as healthcare and logistics helps stabilize NIMs and earnings. Community development lending expands housing and SME credit, catalyzing growth. Geographic diversification tempers local shocks and concentration risk.

Inflation and costs

Inflation pressures noninterest expenses and clients’ debt‑service capacity; Nigeria headline inflation was 22.8% in December 2023, intensifying credit risk and provisioning needs. Pricing discipline and fee optimization help protect ROA while efficiency programs and digital adoption lower unit costs. Stress tests should explicitly model stagflation scenarios and higher long‑run rates.

- Inflation impact on expenses and NPLs

- Pricing and fee optimization to protect ROA

- Digital adoption reduces unit costs

- Stagflation scenarios in stress tests

Capital and liquidity conditions

Market funding spreads and deposit flows materially affect First Bank’s growth trajectory as wider spreads raise funding costs while deposit retention supports lending; Basel III liquidity ratios set the 100% regulatory floor for LCR and NSFR. Strong LCR/NSFR and contingency funding lines bolster resilience, while retained earnings in a private structure fund measured organic expansion; transparent metrics (ratios, stress tests) reassure stakeholders.

- Regulatory floor: LCR/NSFR 100%

- Funding spreads drive loan pricing

- Retained earnings fund organic growth

- Transparent metrics build stakeholder confidence

Regulation, AML and fair-lending raise costs; US 10y at ~4.1%

Net interest margin sensitive to fed funds 5.25–5.50% (mid‑2025) with industry NIMs ~3.0–3.5%; unemployment ~3.7% and avg hourly earnings +4% drive loan demand; Nigeria inflation 22.8% (Dec 2023) and regional GDP ~2.5% (2024) pressure provisioning and costs.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| NIM | 3.0–3.5% |

| Unemployment | 3.7% |

What You See Is What You Get

First Bank PESTLE Analysis

The preview shown here is the exact First Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; this is the final file. After checkout you’ll instantly download the identical document as displayed.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE Analysis of First Bank. Explore how political, economic, social, technological, legal and environmental forces shape its risk and opportunity profile. Buy the full report to access actionable insights, data tables, and ready-to-use slides for investment or strategy decisions.

Political factors

Regulatory policy direction

Regulatory priorities—consumer protection, fair lending, AML—drive FirstBank product design and pushed industry compliance spend to roughly $74.5 billion in 2023, raising unit costs on mortgages, cards and SMB loans. Post‑election shifts can tighten or loosen mortgage, credit card and small‑business constraints; FirstBank must track federal and state rulemaking calendars and comment periods to anticipate change. Proactive engagement reduces disruption and speeds approvals.

Government-backed lending

Government-backed programs like SBA 7(a) (maximum loan size $5,000,000) and GSE support (conforming limit $726,200 in most areas) boost loan demand and shift credit risk to guarantors. Participation can expand originations and fee income but increases documentation, compliance and audit burden. Annual FHFA and budget-driven rule changes can quickly alter caps and pricing. Diversifying exposure limits program-driven volatility.

Local community priorities

As a community-focused bank, municipal partnerships and local development agendas directly influence branch placement and outreach, affecting retail deposit catchment and SME lending pipelines. The $1.2 trillion Bipartisan Infrastructure Law elevates municipal projects that can boost deposits and commercial lending. Political support for financial inclusion, including the CDFI Funds' ~$3 billion ARP allocation, creates grant and CRA-related opportunities and strengthens market access and reputation.

Geopolitical stability

Geopolitical instability raises funding costs, reduces risk appetite, and increases FX-linked client demand even for domestic banks; US 10-year yields stood around 4.1% in mid-2025, reflecting tighter global funding. Market volatility in 2024–25 forced higher capital and liquidity buffers; sanctions regimes require rigorous screening and controls, and preparedness limits operational and reputational loss.

- Funding costs: higher global yields (~4.1% US 10y)

- Risk appetite: reduced, more conservative lending

- Liquidity: raised capital/liquidity buffers in 2024–25

- Compliance: strict sanctions screening lowers reputational risk

Public trust and oversight

Political scrutiny intensified after the 2023 US bank failures (Silicon Valley Bank, Signature, First Republic), pushing regulators to emphasize stress tests again and the Federal Reserve's annual Dodd-Frank exercises covering 23 firms in 2024. Transparent governance and increased community lending improve relations with policymakers; swift incident response reduces enforcement and reputational risk, while consistent messaging preserves franchise value.

- Scrutiny: 2023 bank failures x3

- Stress-tests: 23 banks in 2024

- Mitigation: swift response lowers enforcement risk

- Reputation: governance + community investment

Regulation, AML and fair-lending raise costs; US 10y at ~4.1%

Regulatory focus on consumer protection, AML and fair lending (industry compliance spend $74.5B in 2023) raises unit costs; rule changes post‑election can quickly affect mortgages, cards and SMB lending. Government programs (SBA 7(a) max $5,000,000; conforming limit $726,200) expand originations but add compliance burden. Geopolitical stress lifted US 10y to ~4.1% mid‑2025, increasing funding costs and conservative lending; 2023 saw 3 bank failures and 23 banks underwent stress tests in 2024.

| Metric | Value/Year |

|---|---|

| Compliance spend | $74.5B (2023) |

| US 10y yield | ~4.1% (mid‑2025) |

| SBA 7(a) cap | $5,000,000 |

| Conforming loan limit | $726,200 |

| Infra law | $1.2T |

| CDFI ARP | ~$3B |

| Bank failures | 3 (2023) |

| Stress tests | 23 banks (2024) |

What is included in the product

Explores how macro-environmental forces uniquely impact First Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each category supported by relevant data and current trends. Designed for executives and investors, the analysis offers forward-looking insights to inform strategy, risk management, and scenario planning.

A concise, visually segmented PESTLE summary of First Bank that’s drop‑in ready for slides or reports, easily shareable for quick alignment across teams and ideal for clarifying external risks during planning sessions.

Economic factors

Interest rate cycles

Net interest margin depends on rate levels, pace and deposit betas; with the US federal funds rate at 5.25–5.50% in mid-2025 banks reported industry NIMs near 3.0–3.5%, but rapid hikes or cuts can stress funding and compress spreads as deposit betas rise. Balance-sheet hedging and fast product repricing are critical to protect margin. Scenario planning aligns growth with risk appetite and liquidity stress tests.

Credit cycle dynamics

Employment, rising real wages and higher consumer default rates drive loan demand and provisions; US unemployment hovered near 3.7% in 2024 while average hourly earnings grew ~4% year-on-year, pressuring credit demand and loss-readiness. Mortgages and SME lending remain highly sensitive to housing and business confidence as 30-year mortgage rates averaged near 6.8% in 2024. Prudent underwriting, sector concentration limits and early-warning analytics materially reduce cyclicality and improve workout recoveries.

Regional economic health

Local industries and demographics drive deposit growth and credit quality; regional GDP grew about 2.5% in 2024 while unemployment averaged near 3.7%, influencing loan demand and delinquencies. Targeted outreach to resilient sectors such as healthcare and logistics helps stabilize NIMs and earnings. Community development lending expands housing and SME credit, catalyzing growth. Geographic diversification tempers local shocks and concentration risk.

Inflation and costs

Inflation pressures noninterest expenses and clients’ debt‑service capacity; Nigeria headline inflation was 22.8% in December 2023, intensifying credit risk and provisioning needs. Pricing discipline and fee optimization help protect ROA while efficiency programs and digital adoption lower unit costs. Stress tests should explicitly model stagflation scenarios and higher long‑run rates.

- Inflation impact on expenses and NPLs

- Pricing and fee optimization to protect ROA

- Digital adoption reduces unit costs

- Stagflation scenarios in stress tests

Capital and liquidity conditions

Market funding spreads and deposit flows materially affect First Bank’s growth trajectory as wider spreads raise funding costs while deposit retention supports lending; Basel III liquidity ratios set the 100% regulatory floor for LCR and NSFR. Strong LCR/NSFR and contingency funding lines bolster resilience, while retained earnings in a private structure fund measured organic expansion; transparent metrics (ratios, stress tests) reassure stakeholders.

- Regulatory floor: LCR/NSFR 100%

- Funding spreads drive loan pricing

- Retained earnings fund organic growth

- Transparent metrics build stakeholder confidence

Regulation, AML and fair-lending raise costs; US 10y at ~4.1%

Net interest margin sensitive to fed funds 5.25–5.50% (mid‑2025) with industry NIMs ~3.0–3.5%; unemployment ~3.7% and avg hourly earnings +4% drive loan demand; Nigeria inflation 22.8% (Dec 2023) and regional GDP ~2.5% (2024) pressure provisioning and costs.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| NIM | 3.0–3.5% |

| Unemployment | 3.7% |

What You See Is What You Get

First Bank PESTLE Analysis

The preview shown here is the exact First Bank PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. No placeholders or teasers; this is the final file. After checkout you’ll instantly download the identical document as displayed.