First Citizens Bank (NC) Business Model Canvas

Unlock the strategic Business Model Canvas of a regional bank: revenue, channels, partners.

Unlock the full strategic blueprint behind First Citizens Bank (NC)’s Business Model Canvas and see how it converts customer relationships, digital channels, and commercial lending into sustainable revenue. This concise, actionable canvas highlights key partners, cost structure, and growth levers to inform investment or strategy decisions. Download the complete Word and Excel files for a ready-to-use, section-by-section playbook.

Partnerships

Core banking and fintech providers

Alliances with core processors, cloud vendors, and fintechs give First Citizens — post-CIT acquisition in 2022 — secure, scalable banking capabilities that support digital onboarding, payments, fraud tools, and data analytics. These partners enable co-development that accelerates feature rollouts and improves customer experience, lowering time-to-market and operational risk. Integration with fintechs and cloud platforms underpins omnichannel delivery across the bank’s national footprint.

Payment networks and processors

Ties with major card networks and ACH rails (NACHA reported 30.2 billion ACH payments in 2023) plus merchant acquirers enable First Citizens to issue cards and process transactions broadly and quickly. These partnerships speed settlement, lower failure rates, and use joint risk controls to curb fraud and chargebacks. Economies of scale improve interchange economics, cutting per-transaction costs materially for the bank.

Correspondent banks and syndication partners

Partner correspondent banks facilitate wire clearing, FX and international services, enabling global payments and treasury flows; in 2024 First Citizens used these networks to support cross-border client activity. Loan syndication partners share risk on large credits, expanding lending capacity and diversifying exposure, improving balance sheet flexibility. Clients gain access to larger, more complex financings, often in the high‑hundreds of millions to multibillion-dollar range.

Advisory, legal, and compliance firms

External advisory, legal, and compliance firms bolster First Citizens Bank’s credit, legal, tax, and regulatory expertise, advising on complex structures, workouts, and shifting rules to enable safe growth. Independent validation from these partners strengthens governance and model risk management, enhancing audit readiness and regulatory responsiveness.

- External expertise: credit, legal, tax, regulatory

- Complex matters: structures and workouts

- Validation: governance and model risk

- Outcome: audit readiness and safe growth

Community, SBA, and industry associations

Partnerships with the SBA, roughly 7,000 local chambers of commerce, and community groups expand First Citizens Bank (NC) small-business lending reach by leveraging SBA 7(a) guarantees (up to 85% for loans up to $150,000, 75% above) and localized referral networks. Programs provide technical assistance and partial guarantees to improve borrower credit access and support community development alignment, boosting visibility, brand trust, and referral volume.

- Tags: SBA-guarantees

- Tags: local-chambers

- Tags: community-outreach

- Tags: borrower-technical-assistance

Alliances speed digital onboarding, payments & fraud analytics; ACH 30.2B (2023), SBA up to 85%

Alliances with core processors, cloud vendors, and fintechs (post‑CIT 2022) deliver scalable digital onboarding, payments, fraud tools and analytics, cutting time‑to‑market. Card networks and ACH rails (NACHA 30.2B ACH in 2023) + acquirers speed settlement and lower costs. Correspondent banks and syndication partners support cross‑border flows and large financings in 2024. SBA, chambers and community groups expand small‑business reach via SBA guarantees.

| Partner | Impact | 2023/24 datapoint |

|---|---|---|

| ACH/networks | Transaction scale | 30.2B ACH (2023) |

| SBA & community | SMB access | Up to 85% guarantee |

What is included in the product

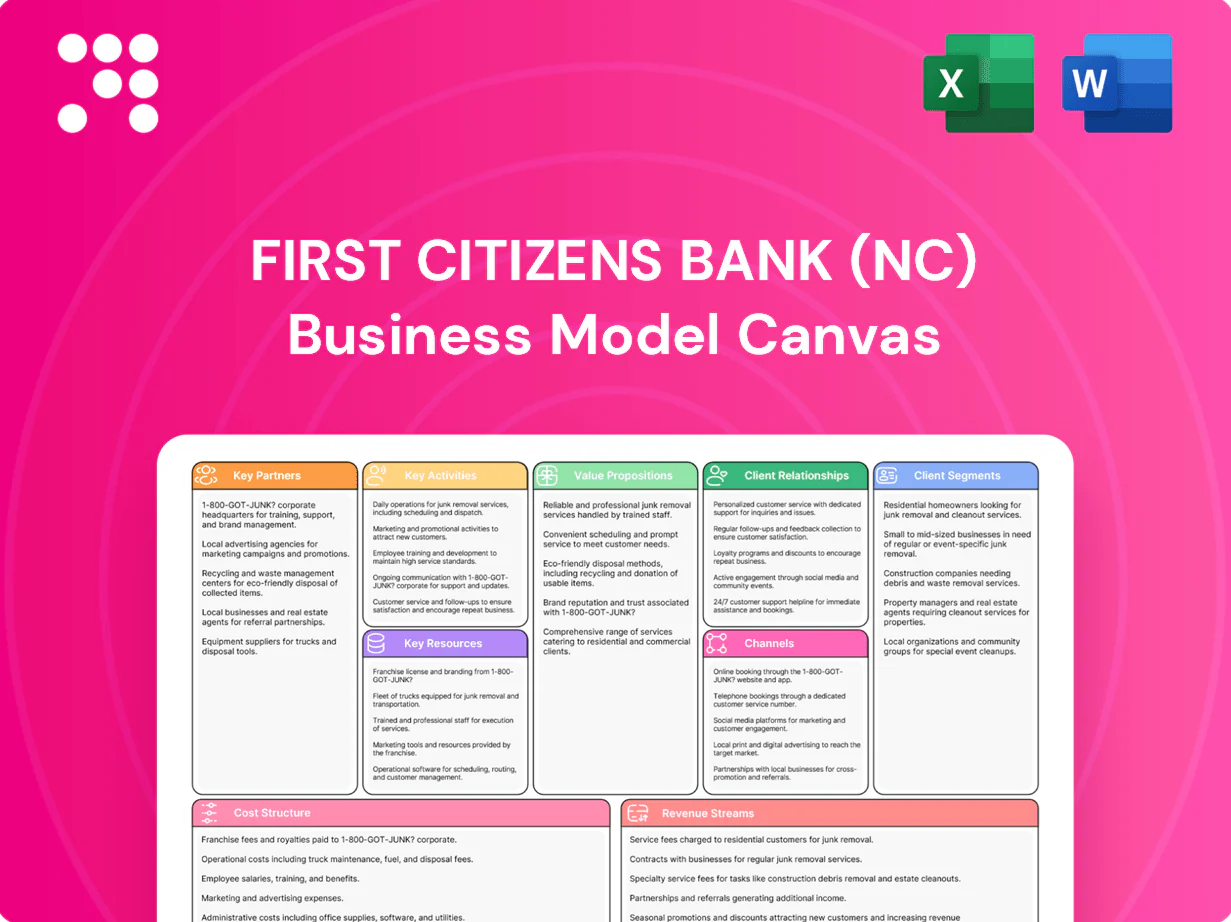

A comprehensive Business Model Canvas for First Citizens Bank (NC) detailing customer segments, value propositions, channels, revenue streams and key activities across the 9 BMC blocks. Tailored for presentations and investor discussions, it includes competitive advantages, SWOT-linked insights and operational validation to inform strategic decisions.

High-level view of First Citizens Bank’s business model with editable cells, helping teams pinpoint customer pain points, revenue streams, and cost drivers quickly for faster strategic decisions.

Activities

Deposit gathering and treasury services

Designing competitive deposit products anchors low-cost funding for First Citizens, whose deposit base reached approximately $136.6 billion in 2024, supporting margin stability. Cash management, liquidity tools, and payment solutions deepen client relationships and boost fee income. Active pricing and analytics optimize mix and duration, while stable core deposits enable prudent loan growth and balance-sheet resilience.

Lending and credit underwriting

Consumer, mortgage, small-business, and commercial lending drive First Citizens Bank’s core earnings, supported by robust underwriting, collateral management, and ongoing portfolio monitoring to control credit risk. Industry and geographic diversification reduce concentration risk across the loan book. Continuous review cycles and tightened credit discipline reinforce underwriting standards and loss mitigation. Risk-adjusted pricing and stress testing guide new originations.

Risk, compliance, and cybersecurity

Enterprise risk management at First Citizens governs credit, market, liquidity and operational risks across a ~$190B balance sheet (2024), using stress testing and ICAAP. Compliance programs track federal/state banking rules and consumer protections, with AML/KYC controls and SAR filings. Multi-layered cyber defenses protect data, identity and transactions; quarterly tabletop exercises, annual penetration tests and an incident response plan support resilience.

Digital product development

Digital product development at First Citizens accelerates online and mobile usability to boost adoption, leveraging the bank’s scale of over $100 billion in assets (post‑CIT acquisition) to fund platform upgrades. API integrations enable embedded finance and partner offerings, while data-driven personalization lifts engagement and cross-sell. Agile delivery shortens innovation cycles and speeds time-to-market.

- api-enabled partnerships

- personalization via analytics

- agile sprints for faster releases

Relationship management and advisory

Bankers deliver tailored guidance to individuals and businesses via financial planning, lending structuring, and cash‑flow insights, driving measurable value; regular reviews surface needs and retention risks while thought leadership builds trust and loyalty. After the CIT acquisition (closed Dec 2022), First Citizens expanded into a top‑25 U.S. bank with roughly $95B in assets (2023).

- Advisory-led revenue uplift: higher wallet share and retention

- Regular reviews uncover cross-sell opportunities and attrition risks

- Thought leadership boosts NPS and long-term loyalty

Deposits, cash management and lending drive growth on a $190B balance sheet

Designing competitive deposit products ($136.6B deposits, 2024) and cash management services anchor low‑cost funding and fee income. Lending across consumer, mortgage, SMB and commercial lines drives core earnings on a ~$190B balance sheet (2024) with disciplined underwriting and stress testing. Digital, API partnerships and advisory banking deepen relationships and lift cross-sell and retention.

| Metric | 2024 |

|---|---|

| Total deposits | $136.6B |

| Balance sheet | ~$190B |

Full Document Unlocks After Purchase

Business Model Canvas

You’re viewing the actual First Citizens Bank (NC) Business Model Canvas document, not a mockup—this preview is a direct excerpt from the final file you’ll receive. Upon purchase you’ll get the exact same, fully formatted and editable Business Model Canvas in Word and Excel. No placeholder content, no surprises—ready to use, present, and adapt.

Unlock the strategic Business Model Canvas of a regional bank: revenue, channels, partners.

Unlock the full strategic blueprint behind First Citizens Bank (NC)’s Business Model Canvas and see how it converts customer relationships, digital channels, and commercial lending into sustainable revenue. This concise, actionable canvas highlights key partners, cost structure, and growth levers to inform investment or strategy decisions. Download the complete Word and Excel files for a ready-to-use, section-by-section playbook.

Partnerships

Core banking and fintech providers

Alliances with core processors, cloud vendors, and fintechs give First Citizens — post-CIT acquisition in 2022 — secure, scalable banking capabilities that support digital onboarding, payments, fraud tools, and data analytics. These partners enable co-development that accelerates feature rollouts and improves customer experience, lowering time-to-market and operational risk. Integration with fintechs and cloud platforms underpins omnichannel delivery across the bank’s national footprint.

Payment networks and processors

Ties with major card networks and ACH rails (NACHA reported 30.2 billion ACH payments in 2023) plus merchant acquirers enable First Citizens to issue cards and process transactions broadly and quickly. These partnerships speed settlement, lower failure rates, and use joint risk controls to curb fraud and chargebacks. Economies of scale improve interchange economics, cutting per-transaction costs materially for the bank.

Correspondent banks and syndication partners

Partner correspondent banks facilitate wire clearing, FX and international services, enabling global payments and treasury flows; in 2024 First Citizens used these networks to support cross-border client activity. Loan syndication partners share risk on large credits, expanding lending capacity and diversifying exposure, improving balance sheet flexibility. Clients gain access to larger, more complex financings, often in the high‑hundreds of millions to multibillion-dollar range.

Advisory, legal, and compliance firms

External advisory, legal, and compliance firms bolster First Citizens Bank’s credit, legal, tax, and regulatory expertise, advising on complex structures, workouts, and shifting rules to enable safe growth. Independent validation from these partners strengthens governance and model risk management, enhancing audit readiness and regulatory responsiveness.

- External expertise: credit, legal, tax, regulatory

- Complex matters: structures and workouts

- Validation: governance and model risk

- Outcome: audit readiness and safe growth

Community, SBA, and industry associations

Partnerships with the SBA, roughly 7,000 local chambers of commerce, and community groups expand First Citizens Bank (NC) small-business lending reach by leveraging SBA 7(a) guarantees (up to 85% for loans up to $150,000, 75% above) and localized referral networks. Programs provide technical assistance and partial guarantees to improve borrower credit access and support community development alignment, boosting visibility, brand trust, and referral volume.

- Tags: SBA-guarantees

- Tags: local-chambers

- Tags: community-outreach

- Tags: borrower-technical-assistance

Alliances speed digital onboarding, payments & fraud analytics; ACH 30.2B (2023), SBA up to 85%

Alliances with core processors, cloud vendors, and fintechs (post‑CIT 2022) deliver scalable digital onboarding, payments, fraud tools and analytics, cutting time‑to‑market. Card networks and ACH rails (NACHA 30.2B ACH in 2023) + acquirers speed settlement and lower costs. Correspondent banks and syndication partners support cross‑border flows and large financings in 2024. SBA, chambers and community groups expand small‑business reach via SBA guarantees.

| Partner | Impact | 2023/24 datapoint |

|---|---|---|

| ACH/networks | Transaction scale | 30.2B ACH (2023) |

| SBA & community | SMB access | Up to 85% guarantee |

What is included in the product

A comprehensive Business Model Canvas for First Citizens Bank (NC) detailing customer segments, value propositions, channels, revenue streams and key activities across the 9 BMC blocks. Tailored for presentations and investor discussions, it includes competitive advantages, SWOT-linked insights and operational validation to inform strategic decisions.

High-level view of First Citizens Bank’s business model with editable cells, helping teams pinpoint customer pain points, revenue streams, and cost drivers quickly for faster strategic decisions.

Activities

Deposit gathering and treasury services

Designing competitive deposit products anchors low-cost funding for First Citizens, whose deposit base reached approximately $136.6 billion in 2024, supporting margin stability. Cash management, liquidity tools, and payment solutions deepen client relationships and boost fee income. Active pricing and analytics optimize mix and duration, while stable core deposits enable prudent loan growth and balance-sheet resilience.

Lending and credit underwriting

Consumer, mortgage, small-business, and commercial lending drive First Citizens Bank’s core earnings, supported by robust underwriting, collateral management, and ongoing portfolio monitoring to control credit risk. Industry and geographic diversification reduce concentration risk across the loan book. Continuous review cycles and tightened credit discipline reinforce underwriting standards and loss mitigation. Risk-adjusted pricing and stress testing guide new originations.

Risk, compliance, and cybersecurity

Enterprise risk management at First Citizens governs credit, market, liquidity and operational risks across a ~$190B balance sheet (2024), using stress testing and ICAAP. Compliance programs track federal/state banking rules and consumer protections, with AML/KYC controls and SAR filings. Multi-layered cyber defenses protect data, identity and transactions; quarterly tabletop exercises, annual penetration tests and an incident response plan support resilience.

Digital product development

Digital product development at First Citizens accelerates online and mobile usability to boost adoption, leveraging the bank’s scale of over $100 billion in assets (post‑CIT acquisition) to fund platform upgrades. API integrations enable embedded finance and partner offerings, while data-driven personalization lifts engagement and cross-sell. Agile delivery shortens innovation cycles and speeds time-to-market.

- api-enabled partnerships

- personalization via analytics

- agile sprints for faster releases

Relationship management and advisory

Bankers deliver tailored guidance to individuals and businesses via financial planning, lending structuring, and cash‑flow insights, driving measurable value; regular reviews surface needs and retention risks while thought leadership builds trust and loyalty. After the CIT acquisition (closed Dec 2022), First Citizens expanded into a top‑25 U.S. bank with roughly $95B in assets (2023).

- Advisory-led revenue uplift: higher wallet share and retention

- Regular reviews uncover cross-sell opportunities and attrition risks

- Thought leadership boosts NPS and long-term loyalty

Deposits, cash management and lending drive growth on a $190B balance sheet

Designing competitive deposit products ($136.6B deposits, 2024) and cash management services anchor low‑cost funding and fee income. Lending across consumer, mortgage, SMB and commercial lines drives core earnings on a ~$190B balance sheet (2024) with disciplined underwriting and stress testing. Digital, API partnerships and advisory banking deepen relationships and lift cross-sell and retention.

| Metric | 2024 |

|---|---|

| Total deposits | $136.6B |

| Balance sheet | ~$190B |

Full Document Unlocks After Purchase

Business Model Canvas

You’re viewing the actual First Citizens Bank (NC) Business Model Canvas document, not a mockup—this preview is a direct excerpt from the final file you’ll receive. Upon purchase you’ll get the exact same, fully formatted and editable Business Model Canvas in Word and Excel. No placeholder content, no surprises—ready to use, present, and adapt.

Original: $10.00

-65%$10.00

$3.50Description

Unlock the strategic Business Model Canvas of a regional bank: revenue, channels, partners.

Unlock the full strategic blueprint behind First Citizens Bank (NC)’s Business Model Canvas and see how it converts customer relationships, digital channels, and commercial lending into sustainable revenue. This concise, actionable canvas highlights key partners, cost structure, and growth levers to inform investment or strategy decisions. Download the complete Word and Excel files for a ready-to-use, section-by-section playbook.

Partnerships

Core banking and fintech providers

Alliances with core processors, cloud vendors, and fintechs give First Citizens — post-CIT acquisition in 2022 — secure, scalable banking capabilities that support digital onboarding, payments, fraud tools, and data analytics. These partners enable co-development that accelerates feature rollouts and improves customer experience, lowering time-to-market and operational risk. Integration with fintechs and cloud platforms underpins omnichannel delivery across the bank’s national footprint.

Payment networks and processors

Ties with major card networks and ACH rails (NACHA reported 30.2 billion ACH payments in 2023) plus merchant acquirers enable First Citizens to issue cards and process transactions broadly and quickly. These partnerships speed settlement, lower failure rates, and use joint risk controls to curb fraud and chargebacks. Economies of scale improve interchange economics, cutting per-transaction costs materially for the bank.

Correspondent banks and syndication partners

Partner correspondent banks facilitate wire clearing, FX and international services, enabling global payments and treasury flows; in 2024 First Citizens used these networks to support cross-border client activity. Loan syndication partners share risk on large credits, expanding lending capacity and diversifying exposure, improving balance sheet flexibility. Clients gain access to larger, more complex financings, often in the high‑hundreds of millions to multibillion-dollar range.

Advisory, legal, and compliance firms

External advisory, legal, and compliance firms bolster First Citizens Bank’s credit, legal, tax, and regulatory expertise, advising on complex structures, workouts, and shifting rules to enable safe growth. Independent validation from these partners strengthens governance and model risk management, enhancing audit readiness and regulatory responsiveness.

- External expertise: credit, legal, tax, regulatory

- Complex matters: structures and workouts

- Validation: governance and model risk

- Outcome: audit readiness and safe growth

Community, SBA, and industry associations

Partnerships with the SBA, roughly 7,000 local chambers of commerce, and community groups expand First Citizens Bank (NC) small-business lending reach by leveraging SBA 7(a) guarantees (up to 85% for loans up to $150,000, 75% above) and localized referral networks. Programs provide technical assistance and partial guarantees to improve borrower credit access and support community development alignment, boosting visibility, brand trust, and referral volume.

- Tags: SBA-guarantees

- Tags: local-chambers

- Tags: community-outreach

- Tags: borrower-technical-assistance

Alliances speed digital onboarding, payments & fraud analytics; ACH 30.2B (2023), SBA up to 85%

Alliances with core processors, cloud vendors, and fintechs (post‑CIT 2022) deliver scalable digital onboarding, payments, fraud tools and analytics, cutting time‑to‑market. Card networks and ACH rails (NACHA 30.2B ACH in 2023) + acquirers speed settlement and lower costs. Correspondent banks and syndication partners support cross‑border flows and large financings in 2024. SBA, chambers and community groups expand small‑business reach via SBA guarantees.

| Partner | Impact | 2023/24 datapoint |

|---|---|---|

| ACH/networks | Transaction scale | 30.2B ACH (2023) |

| SBA & community | SMB access | Up to 85% guarantee |

What is included in the product

A comprehensive Business Model Canvas for First Citizens Bank (NC) detailing customer segments, value propositions, channels, revenue streams and key activities across the 9 BMC blocks. Tailored for presentations and investor discussions, it includes competitive advantages, SWOT-linked insights and operational validation to inform strategic decisions.

High-level view of First Citizens Bank’s business model with editable cells, helping teams pinpoint customer pain points, revenue streams, and cost drivers quickly for faster strategic decisions.

Activities

Deposit gathering and treasury services

Designing competitive deposit products anchors low-cost funding for First Citizens, whose deposit base reached approximately $136.6 billion in 2024, supporting margin stability. Cash management, liquidity tools, and payment solutions deepen client relationships and boost fee income. Active pricing and analytics optimize mix and duration, while stable core deposits enable prudent loan growth and balance-sheet resilience.

Lending and credit underwriting

Consumer, mortgage, small-business, and commercial lending drive First Citizens Bank’s core earnings, supported by robust underwriting, collateral management, and ongoing portfolio monitoring to control credit risk. Industry and geographic diversification reduce concentration risk across the loan book. Continuous review cycles and tightened credit discipline reinforce underwriting standards and loss mitigation. Risk-adjusted pricing and stress testing guide new originations.

Risk, compliance, and cybersecurity

Enterprise risk management at First Citizens governs credit, market, liquidity and operational risks across a ~$190B balance sheet (2024), using stress testing and ICAAP. Compliance programs track federal/state banking rules and consumer protections, with AML/KYC controls and SAR filings. Multi-layered cyber defenses protect data, identity and transactions; quarterly tabletop exercises, annual penetration tests and an incident response plan support resilience.

Digital product development

Digital product development at First Citizens accelerates online and mobile usability to boost adoption, leveraging the bank’s scale of over $100 billion in assets (post‑CIT acquisition) to fund platform upgrades. API integrations enable embedded finance and partner offerings, while data-driven personalization lifts engagement and cross-sell. Agile delivery shortens innovation cycles and speeds time-to-market.

- api-enabled partnerships

- personalization via analytics

- agile sprints for faster releases

Relationship management and advisory

Bankers deliver tailored guidance to individuals and businesses via financial planning, lending structuring, and cash‑flow insights, driving measurable value; regular reviews surface needs and retention risks while thought leadership builds trust and loyalty. After the CIT acquisition (closed Dec 2022), First Citizens expanded into a top‑25 U.S. bank with roughly $95B in assets (2023).

- Advisory-led revenue uplift: higher wallet share and retention

- Regular reviews uncover cross-sell opportunities and attrition risks

- Thought leadership boosts NPS and long-term loyalty

Deposits, cash management and lending drive growth on a $190B balance sheet

Designing competitive deposit products ($136.6B deposits, 2024) and cash management services anchor low‑cost funding and fee income. Lending across consumer, mortgage, SMB and commercial lines drives core earnings on a ~$190B balance sheet (2024) with disciplined underwriting and stress testing. Digital, API partnerships and advisory banking deepen relationships and lift cross-sell and retention.

| Metric | 2024 |

|---|---|

| Total deposits | $136.6B |

| Balance sheet | ~$190B |

Full Document Unlocks After Purchase

Business Model Canvas

You’re viewing the actual First Citizens Bank (NC) Business Model Canvas document, not a mockup—this preview is a direct excerpt from the final file you’ll receive. Upon purchase you’ll get the exact same, fully formatted and editable Business Model Canvas in Word and Excel. No placeholder content, no surprises—ready to use, present, and adapt.