First Citizens Bank (NC) Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

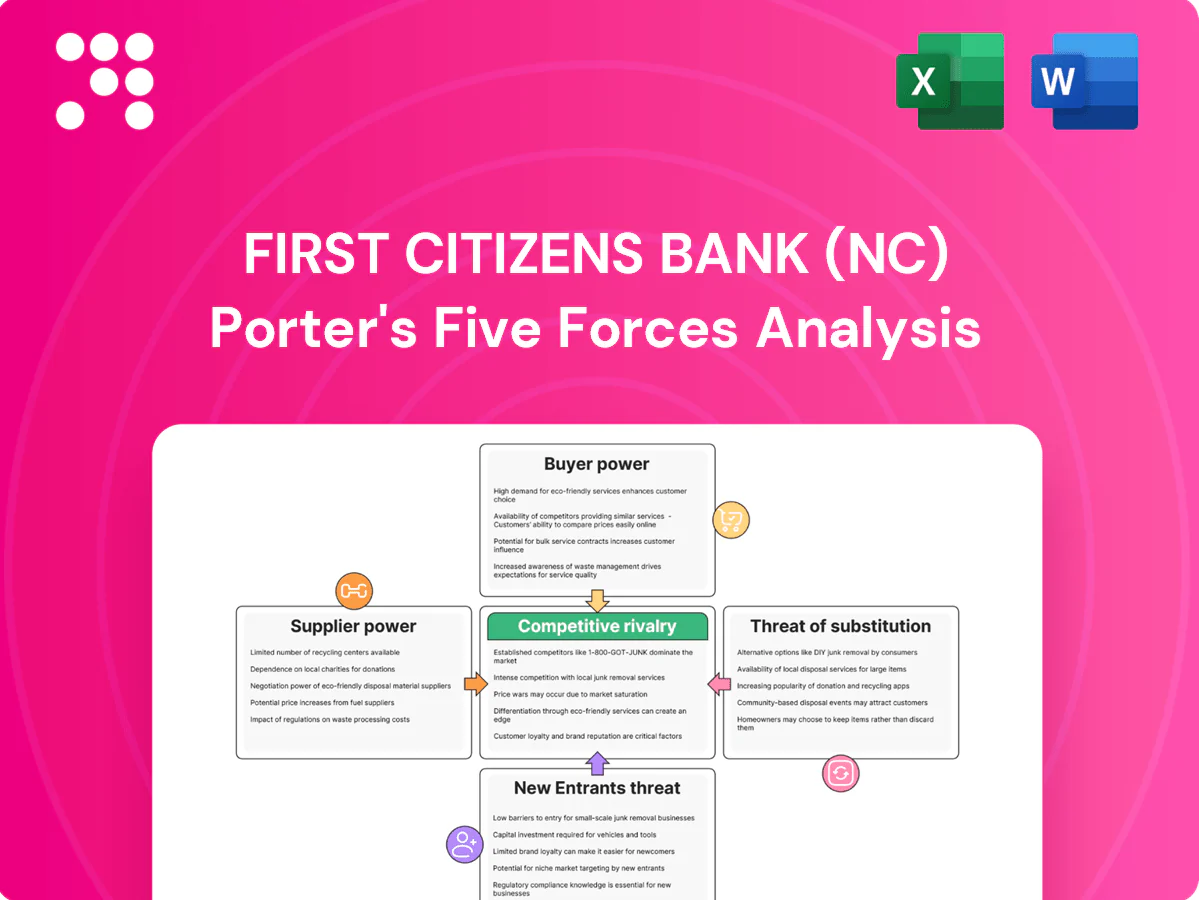

First Citizens Bank (NC) faces moderate buyer power, intense rivalry among regional banks, high regulatory barriers limiting new entrants, manageable supplier power, and rising fintech substitutes pressuring margins. This snapshot highlights strategic pressure points and growth levers. Want detailed force ratings, visuals and tailored implications? Unlock the full Porter's Five Forces Analysis to get the complete report.

Suppliers Bargaining Power

Core technology vendors concentration

First Citizens relies on a handful of core banking platform providers and payment networks, concentrating supplier leverage over pricing and service terms. Switching cores is costly, risky, and multi-year, which raises the bank’s dependence on incumbent vendors and slows technology-driven product cycles. Vendors can influence pricing, service levels, and innovation cadence through roadmap control and prioritization. Multi-vendor strategies and building internal tech talent partially mitigate supplier power.

Funding suppliers: depositors and wholesale markets

Funding suppliers for First Citizens include low-cost retail depositors and supplemental sources such as FHLB lines, Federal Reserve facilities, and brokered CDs; in stressed markets these wholesale providers tighten terms and gain pricing power, pushing up marginal funding costs. Stable, granular retail deposits reduce supplier leverage, while concentration in large or rate-sensitive balances increases it. Strong liquidity management and deep lender relationships mitigate vulnerability.

Talent and specialized expertise

Skilled bankers, risk managers and technologists are critical inputs for First Citizens; 2024 industry wage growth for financial occupations ran about 4%–6% year-over-year, heightening supplier leverage. Scarcity in credit underwriting, cybersecurity and data analytics — cited in 2024 industry surveys as top-three talent shortages — raises bargaining power. Robust retention programs and culture damp churn, while automation and training pipelines help rebalance power over time.

Data, cloud, and fintech partners

Data, cloud, and fintech partners are central to First Citizens Bank digital delivery, with usage-based pricing and proprietary ecosystems risking vendor lock-in and higher operating costs; open APIs and negotiated enterprise agreements can limit supplier leverage and reduce switching costs.

- Reduce dependence via open APIs

- Negotiate enterprise SLAs/pricing

- Invest in internal data platforms

Regulated counterparties and custodians

Regulated counterparties—card networks, custodians and correspondent banks—shape First Citizens Bank economics through fees and operating rules; Visa and Mastercard together account for over 80% of U.S. card volume (2024), concentrating fee-setting power. Standardized contracts favor large-scale providers and limit bespoke terms; volume commitments can secure lower rates but raise switching barriers. Diversifying across networks and custodians moderates this supplier power.

- Card networks: >80% U.S. volume (2024)

- Standardized contracts: limited customization

- Volume commitments: better pricing, higher switching cost

- Diversification: reduces counterparty concentration risk

Concentrated supplier power: card networks >80% volume, wages +4-6%, high cloud switching costs

First Citizens faces concentrated supplier power from core banking vendors, card networks (>80% U.S. card volume in 2024), cloud/data providers and talent (financial sector wage growth ~4–6% in 2024). High switching costs for cores and usage-based cloud pricing raise costs; stable retail deposits and multi-vendor or internal builds reduce leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Card networks | >80% U.S. volume | High fee power |

| Wages | 4–6% YoY | Higher talent cost |

| Funding | FHLB/Fed/brokered lines | Pricing in stress |

What is included in the product

Tailored Porter's Five Forces for First Citizens Bank (NC) highlighting competitive intensity, customer and supplier bargaining power, threats from fintech substitutes and new entrants, and industry dynamics that protect or expose its margins.

A concise one-sheet Porter's Five Forces for First Citizens Bank (NC), highlighting competitive rivalry, buyer/supplier power, new entrants, and substitutes to speed strategic decisions; editable pressure levels and a radar-chart export make it easy to customize for regulatory shifts, M&A scenarios, or boardroom slides.

Customers Bargaining Power

Large commercial clients negotiate aggressively

Middle-market and institutional clients extract rate concessions, fee waivers and relaxed covenant terms from First Citizens, leveraging multi-bank relationships that raise price sensitivity and switching options; after the 2022 CIT acquisition First Citizens expanded its commercial book, with reported total assets of about 109.6 billion at 2023 year-end, increasing focus on bespoke deals. Customized solutions raise client dependence but also scrutiny on service quality, while relationship banking and bundled services are used to trade price for wallet share.

Retail customers have moderate switching costs

Digital account opening and fintech choices reduce friction to switch, and First Citizens — a top-20 US bank after the 2022 CIT acquisition — faces that digital churn risk. Yet bill-pay links, direct deposits and trust-based relationships create strong inertia. With the federal funds rate near 5.25–5.50% in 2024, rate shoppers pressure deposit pricing in rising-rate cycles. Personal service and local presence help retain value-focused customers.

SMBs seek integrated cash management

Small businesses, which account for 99.9% of US firms, increasingly prefer bundled payments, treasury and lending to reduce vendor complexity, raising the bar for First Citizens to offer end-to-end cash management. Integration lowers switching but drives demand for near-100% uptime and rapid support, shifting pricing power toward service reliability. Industry-specific solutions (healthcare, construction) can restore bank leverage by embedding services into client workflows.

Wealth and advisory clients expect performance

Wealth and advisory clients now benchmark fees to outcomes and digital UX, with robo-advisor AUM surpassing 1 trillion in 2024 and average advisory fees about 0.82%, increasing client price sensitivity. Transparent pricing and low-cost robo alternatives raise bargaining power, forcing First Citizens to show clear ROI. Trusted advisors and holistic planning let the bank justify premium pricing, but fiduciary standards demand documented value to protect margins.

- Fee sensitivity: average advisory fee ~0.82% (2024)

- Robo threat: robo AUM >1 trillion (2024)

- Value levers: holistic planning, trust, fiduciary compliance

Rate environment amplifies buyer sensitivity

Rate environment amplifies buyer sensitivity at First Citizens: in 2024 industry deposit betas ran near 35%, pushing depositors to demand higher yields or shift to money market alternatives; borrowers delayed or refinanced as loan spreads widened, squeezing NIM and shifting mix by segment; elasticity differs across retail, commercial and wealth clients, so active repricing and segmented offers are used to manage pricing power.

- 2024 deposit beta ~35%

- Retail more rate‑sensitive than commercial

- Repricing and targeted offers limit NIM erosion

Middle-market clients extract concessions; bank has $109.6B assets

Customers wield moderate-to-high bargaining power: middle-market and institutional clients extract concessions as First Citizens grew to ~$109.6B assets post-2022 CIT deal, while fintech and digital UX raise switching risk. Wealth clients benchmark fees (avg 0.82% advisory) against robo AUM >1T, and 2024 deposit beta ~35% with fed funds ~5.25–5.50% heighten rate sensitivity.

| Metric | Value |

|---|---|

| Total assets (2023 YE) | $109.6B |

| Advisory fee (avg 2024) | 0.82% |

| Robo AUM (2024) | >$1T |

| Deposit beta (2024) | ~35% |

| Fed funds (2024) | 5.25–5.50% |

Preview Before You Purchase

First Citizens Bank (NC) Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for First Citizens Bank (NC) you’ll receive immediately after purchase—no placeholders or samples. The full document is professionally formatted and ready to download and use the moment you buy. Purchase grants instant access to this identical file.

A Must-Have Tool for Decision-Makers

First Citizens Bank (NC) faces moderate buyer power, intense rivalry among regional banks, high regulatory barriers limiting new entrants, manageable supplier power, and rising fintech substitutes pressuring margins. This snapshot highlights strategic pressure points and growth levers. Want detailed force ratings, visuals and tailored implications? Unlock the full Porter's Five Forces Analysis to get the complete report.

Suppliers Bargaining Power

Core technology vendors concentration

First Citizens relies on a handful of core banking platform providers and payment networks, concentrating supplier leverage over pricing and service terms. Switching cores is costly, risky, and multi-year, which raises the bank’s dependence on incumbent vendors and slows technology-driven product cycles. Vendors can influence pricing, service levels, and innovation cadence through roadmap control and prioritization. Multi-vendor strategies and building internal tech talent partially mitigate supplier power.

Funding suppliers: depositors and wholesale markets

Funding suppliers for First Citizens include low-cost retail depositors and supplemental sources such as FHLB lines, Federal Reserve facilities, and brokered CDs; in stressed markets these wholesale providers tighten terms and gain pricing power, pushing up marginal funding costs. Stable, granular retail deposits reduce supplier leverage, while concentration in large or rate-sensitive balances increases it. Strong liquidity management and deep lender relationships mitigate vulnerability.

Talent and specialized expertise

Skilled bankers, risk managers and technologists are critical inputs for First Citizens; 2024 industry wage growth for financial occupations ran about 4%–6% year-over-year, heightening supplier leverage. Scarcity in credit underwriting, cybersecurity and data analytics — cited in 2024 industry surveys as top-three talent shortages — raises bargaining power. Robust retention programs and culture damp churn, while automation and training pipelines help rebalance power over time.

Data, cloud, and fintech partners

Data, cloud, and fintech partners are central to First Citizens Bank digital delivery, with usage-based pricing and proprietary ecosystems risking vendor lock-in and higher operating costs; open APIs and negotiated enterprise agreements can limit supplier leverage and reduce switching costs.

- Reduce dependence via open APIs

- Negotiate enterprise SLAs/pricing

- Invest in internal data platforms

Regulated counterparties and custodians

Regulated counterparties—card networks, custodians and correspondent banks—shape First Citizens Bank economics through fees and operating rules; Visa and Mastercard together account for over 80% of U.S. card volume (2024), concentrating fee-setting power. Standardized contracts favor large-scale providers and limit bespoke terms; volume commitments can secure lower rates but raise switching barriers. Diversifying across networks and custodians moderates this supplier power.

- Card networks: >80% U.S. volume (2024)

- Standardized contracts: limited customization

- Volume commitments: better pricing, higher switching cost

- Diversification: reduces counterparty concentration risk

Concentrated supplier power: card networks >80% volume, wages +4-6%, high cloud switching costs

First Citizens faces concentrated supplier power from core banking vendors, card networks (>80% U.S. card volume in 2024), cloud/data providers and talent (financial sector wage growth ~4–6% in 2024). High switching costs for cores and usage-based cloud pricing raise costs; stable retail deposits and multi-vendor or internal builds reduce leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Card networks | >80% U.S. volume | High fee power |

| Wages | 4–6% YoY | Higher talent cost |

| Funding | FHLB/Fed/brokered lines | Pricing in stress |

What is included in the product

Tailored Porter's Five Forces for First Citizens Bank (NC) highlighting competitive intensity, customer and supplier bargaining power, threats from fintech substitutes and new entrants, and industry dynamics that protect or expose its margins.

A concise one-sheet Porter's Five Forces for First Citizens Bank (NC), highlighting competitive rivalry, buyer/supplier power, new entrants, and substitutes to speed strategic decisions; editable pressure levels and a radar-chart export make it easy to customize for regulatory shifts, M&A scenarios, or boardroom slides.

Customers Bargaining Power

Large commercial clients negotiate aggressively

Middle-market and institutional clients extract rate concessions, fee waivers and relaxed covenant terms from First Citizens, leveraging multi-bank relationships that raise price sensitivity and switching options; after the 2022 CIT acquisition First Citizens expanded its commercial book, with reported total assets of about 109.6 billion at 2023 year-end, increasing focus on bespoke deals. Customized solutions raise client dependence but also scrutiny on service quality, while relationship banking and bundled services are used to trade price for wallet share.

Retail customers have moderate switching costs

Digital account opening and fintech choices reduce friction to switch, and First Citizens — a top-20 US bank after the 2022 CIT acquisition — faces that digital churn risk. Yet bill-pay links, direct deposits and trust-based relationships create strong inertia. With the federal funds rate near 5.25–5.50% in 2024, rate shoppers pressure deposit pricing in rising-rate cycles. Personal service and local presence help retain value-focused customers.

SMBs seek integrated cash management

Small businesses, which account for 99.9% of US firms, increasingly prefer bundled payments, treasury and lending to reduce vendor complexity, raising the bar for First Citizens to offer end-to-end cash management. Integration lowers switching but drives demand for near-100% uptime and rapid support, shifting pricing power toward service reliability. Industry-specific solutions (healthcare, construction) can restore bank leverage by embedding services into client workflows.

Wealth and advisory clients expect performance

Wealth and advisory clients now benchmark fees to outcomes and digital UX, with robo-advisor AUM surpassing 1 trillion in 2024 and average advisory fees about 0.82%, increasing client price sensitivity. Transparent pricing and low-cost robo alternatives raise bargaining power, forcing First Citizens to show clear ROI. Trusted advisors and holistic planning let the bank justify premium pricing, but fiduciary standards demand documented value to protect margins.

- Fee sensitivity: average advisory fee ~0.82% (2024)

- Robo threat: robo AUM >1 trillion (2024)

- Value levers: holistic planning, trust, fiduciary compliance

Rate environment amplifies buyer sensitivity

Rate environment amplifies buyer sensitivity at First Citizens: in 2024 industry deposit betas ran near 35%, pushing depositors to demand higher yields or shift to money market alternatives; borrowers delayed or refinanced as loan spreads widened, squeezing NIM and shifting mix by segment; elasticity differs across retail, commercial and wealth clients, so active repricing and segmented offers are used to manage pricing power.

- 2024 deposit beta ~35%

- Retail more rate‑sensitive than commercial

- Repricing and targeted offers limit NIM erosion

Middle-market clients extract concessions; bank has $109.6B assets

Customers wield moderate-to-high bargaining power: middle-market and institutional clients extract concessions as First Citizens grew to ~$109.6B assets post-2022 CIT deal, while fintech and digital UX raise switching risk. Wealth clients benchmark fees (avg 0.82% advisory) against robo AUM >1T, and 2024 deposit beta ~35% with fed funds ~5.25–5.50% heighten rate sensitivity.

| Metric | Value |

|---|---|

| Total assets (2023 YE) | $109.6B |

| Advisory fee (avg 2024) | 0.82% |

| Robo AUM (2024) | >$1T |

| Deposit beta (2024) | ~35% |

| Fed funds (2024) | 5.25–5.50% |

Preview Before You Purchase

First Citizens Bank (NC) Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for First Citizens Bank (NC) you’ll receive immediately after purchase—no placeholders or samples. The full document is professionally formatted and ready to download and use the moment you buy. Purchase grants instant access to this identical file.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

First Citizens Bank (NC) faces moderate buyer power, intense rivalry among regional banks, high regulatory barriers limiting new entrants, manageable supplier power, and rising fintech substitutes pressuring margins. This snapshot highlights strategic pressure points and growth levers. Want detailed force ratings, visuals and tailored implications? Unlock the full Porter's Five Forces Analysis to get the complete report.

Suppliers Bargaining Power

Core technology vendors concentration

First Citizens relies on a handful of core banking platform providers and payment networks, concentrating supplier leverage over pricing and service terms. Switching cores is costly, risky, and multi-year, which raises the bank’s dependence on incumbent vendors and slows technology-driven product cycles. Vendors can influence pricing, service levels, and innovation cadence through roadmap control and prioritization. Multi-vendor strategies and building internal tech talent partially mitigate supplier power.

Funding suppliers: depositors and wholesale markets

Funding suppliers for First Citizens include low-cost retail depositors and supplemental sources such as FHLB lines, Federal Reserve facilities, and brokered CDs; in stressed markets these wholesale providers tighten terms and gain pricing power, pushing up marginal funding costs. Stable, granular retail deposits reduce supplier leverage, while concentration in large or rate-sensitive balances increases it. Strong liquidity management and deep lender relationships mitigate vulnerability.

Talent and specialized expertise

Skilled bankers, risk managers and technologists are critical inputs for First Citizens; 2024 industry wage growth for financial occupations ran about 4%–6% year-over-year, heightening supplier leverage. Scarcity in credit underwriting, cybersecurity and data analytics — cited in 2024 industry surveys as top-three talent shortages — raises bargaining power. Robust retention programs and culture damp churn, while automation and training pipelines help rebalance power over time.

Data, cloud, and fintech partners

Data, cloud, and fintech partners are central to First Citizens Bank digital delivery, with usage-based pricing and proprietary ecosystems risking vendor lock-in and higher operating costs; open APIs and negotiated enterprise agreements can limit supplier leverage and reduce switching costs.

- Reduce dependence via open APIs

- Negotiate enterprise SLAs/pricing

- Invest in internal data platforms

Regulated counterparties and custodians

Regulated counterparties—card networks, custodians and correspondent banks—shape First Citizens Bank economics through fees and operating rules; Visa and Mastercard together account for over 80% of U.S. card volume (2024), concentrating fee-setting power. Standardized contracts favor large-scale providers and limit bespoke terms; volume commitments can secure lower rates but raise switching barriers. Diversifying across networks and custodians moderates this supplier power.

- Card networks: >80% U.S. volume (2024)

- Standardized contracts: limited customization

- Volume commitments: better pricing, higher switching cost

- Diversification: reduces counterparty concentration risk

Concentrated supplier power: card networks >80% volume, wages +4-6%, high cloud switching costs

First Citizens faces concentrated supplier power from core banking vendors, card networks (>80% U.S. card volume in 2024), cloud/data providers and talent (financial sector wage growth ~4–6% in 2024). High switching costs for cores and usage-based cloud pricing raise costs; stable retail deposits and multi-vendor or internal builds reduce leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Card networks | >80% U.S. volume | High fee power |

| Wages | 4–6% YoY | Higher talent cost |

| Funding | FHLB/Fed/brokered lines | Pricing in stress |

What is included in the product

Tailored Porter's Five Forces for First Citizens Bank (NC) highlighting competitive intensity, customer and supplier bargaining power, threats from fintech substitutes and new entrants, and industry dynamics that protect or expose its margins.

A concise one-sheet Porter's Five Forces for First Citizens Bank (NC), highlighting competitive rivalry, buyer/supplier power, new entrants, and substitutes to speed strategic decisions; editable pressure levels and a radar-chart export make it easy to customize for regulatory shifts, M&A scenarios, or boardroom slides.

Customers Bargaining Power

Large commercial clients negotiate aggressively

Middle-market and institutional clients extract rate concessions, fee waivers and relaxed covenant terms from First Citizens, leveraging multi-bank relationships that raise price sensitivity and switching options; after the 2022 CIT acquisition First Citizens expanded its commercial book, with reported total assets of about 109.6 billion at 2023 year-end, increasing focus on bespoke deals. Customized solutions raise client dependence but also scrutiny on service quality, while relationship banking and bundled services are used to trade price for wallet share.

Retail customers have moderate switching costs

Digital account opening and fintech choices reduce friction to switch, and First Citizens — a top-20 US bank after the 2022 CIT acquisition — faces that digital churn risk. Yet bill-pay links, direct deposits and trust-based relationships create strong inertia. With the federal funds rate near 5.25–5.50% in 2024, rate shoppers pressure deposit pricing in rising-rate cycles. Personal service and local presence help retain value-focused customers.

SMBs seek integrated cash management

Small businesses, which account for 99.9% of US firms, increasingly prefer bundled payments, treasury and lending to reduce vendor complexity, raising the bar for First Citizens to offer end-to-end cash management. Integration lowers switching but drives demand for near-100% uptime and rapid support, shifting pricing power toward service reliability. Industry-specific solutions (healthcare, construction) can restore bank leverage by embedding services into client workflows.

Wealth and advisory clients expect performance

Wealth and advisory clients now benchmark fees to outcomes and digital UX, with robo-advisor AUM surpassing 1 trillion in 2024 and average advisory fees about 0.82%, increasing client price sensitivity. Transparent pricing and low-cost robo alternatives raise bargaining power, forcing First Citizens to show clear ROI. Trusted advisors and holistic planning let the bank justify premium pricing, but fiduciary standards demand documented value to protect margins.

- Fee sensitivity: average advisory fee ~0.82% (2024)

- Robo threat: robo AUM >1 trillion (2024)

- Value levers: holistic planning, trust, fiduciary compliance

Rate environment amplifies buyer sensitivity

Rate environment amplifies buyer sensitivity at First Citizens: in 2024 industry deposit betas ran near 35%, pushing depositors to demand higher yields or shift to money market alternatives; borrowers delayed or refinanced as loan spreads widened, squeezing NIM and shifting mix by segment; elasticity differs across retail, commercial and wealth clients, so active repricing and segmented offers are used to manage pricing power.

- 2024 deposit beta ~35%

- Retail more rate‑sensitive than commercial

- Repricing and targeted offers limit NIM erosion

Middle-market clients extract concessions; bank has $109.6B assets

Customers wield moderate-to-high bargaining power: middle-market and institutional clients extract concessions as First Citizens grew to ~$109.6B assets post-2022 CIT deal, while fintech and digital UX raise switching risk. Wealth clients benchmark fees (avg 0.82% advisory) against robo AUM >1T, and 2024 deposit beta ~35% with fed funds ~5.25–5.50% heighten rate sensitivity.

| Metric | Value |

|---|---|

| Total assets (2023 YE) | $109.6B |

| Advisory fee (avg 2024) | 0.82% |

| Robo AUM (2024) | >$1T |

| Deposit beta (2024) | ~35% |

| Fed funds (2024) | 5.25–5.50% |

Preview Before You Purchase

First Citizens Bank (NC) Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for First Citizens Bank (NC) you’ll receive immediately after purchase—no placeholders or samples. The full document is professionally formatted and ready to download and use the moment you buy. Purchase grants instant access to this identical file.